Agenda –

Audit Committee Meeting 11 October 2016 Page 6 of 7

|

5.1 ANNUAL

FINANCIAL REPORT & AUDIT REPORT 2015/2016

LOCATION/ADDRESS: Nil

APPLICANT: Nil

FILE: FRE02

AUTHOR: Coordinator

Financial Services

CONTRIBUTOR/S: Manager

Financial Services

RESPONSIBLE

OFFICER: Director

Corporate Services

DISCLOSURE

OF INTEREST: Nil

DATE OF REPORT: 6

October 2016

|

|

SUMMARY: The

Audit Committee is required to consider and recommend to Council, the

adoption of the annual financial report, examine the audit and management

reports, and review the report prepared by the Chief Executive Officer.

|

BACKGROUND

Previous

Considerations

Nil

Pursuant to Section 7.9 of the Local

Government Act 1995 (LGA), an Auditor is required to examine the

accounts and annual financial report submitted by a local government for audit.

The Auditor is also required, by 31 December following the financial year to

which the accounts and report relate, prepare a report thereon and forward a

copy of that report to:

(a)

Mayor or President; and

(b)

The Chief Executive Officer; and

(c)

The Minister

Furthermore, in accordance with

Regulation 10(4) of the Local Government (Audit) Regulations 1996 (Audit

Regulations), where it is considered appropriate to do so, the Auditor

may prepare a Management Report to accompany the Auditor’s Report, which

is also to be forwarded to the persons specified in Section 7.9 of the LGA.

On finalisation of the Shire’s

2015/2016 final audit, the Auditors presented their initial findings to the

Audit Committee for consideration at an informal briefing session held

Wednesday 21 September 2016 which was attended by Shire President Ron Johnston

and Councillor Desiree Male.

The Audit Committee is required to

examine the reports of the auditor after receiving a report from the Chief

Executive Officer (CEO) on the matters reported and:

· Determine

if any matters raised require action to be taken by the local government; and

· Ensure

that appropriate action is taken in respect of those matters.

The Audit Committee is also required

to review a report prepared by the CEO on any actions taken in respect of any

matters raised in the report of the auditor and presents the report to Council

for adoption. A copy of the report is to be forwarded to the Minister prior to

the end of the next financial year or 6 months after the last report prepared

by the auditor is received, whichever is the latest in time.

An analysis of the 2015/2016

operating result is provided in this report and how it compares to the

forecasted outcomes of the Shire’s adopted Integrated Planning and

Reporting Framework. As a background, the 2015/2016 Annual Financial Report

discloses the results of the fourth year of implementation of the newly

legislated Integrated Planning and Reporting Framework. The plans contained in

the framework provide funding strategies to ensure Council can meet its adopted

strategic objectives, while maintaining and forecasting impacts on the

Shire’s future financial sustainability.

As reported to Council in the three

preceding years in regards to the 2012/2013, 2013/2014 and 2014/2015 Annual

Financial Reports, the Shire’s 2015/2016 Annual Budget process continued

to place significant focus on a number of ‘informing

strategies’. As part of the budget finalisation it was still

evident in the fourth year since the introduction of the integrated planning

framework, that the desired allocations toward capital renewal outlined within

the 2013 Asset Management Plans are not being achieved.

The draft 2016-2030 Shire of Broome

Long Term Financial Plan and draft Strategic Community Plan 2015-2025 and

Corporate Business Plan 2015-2019 were presented to Councillors at workshops

held in February 2015 which informed the 2015/2016 annual budget process. The

SCP and CBP were adopted at the SMC held 19 February 2015, including the

organisational restructure which resulted in $1.8M savings in employee costs

per annum. The revised 2015-2030 LTFP was received by Council at the Special

Meeting of Council (SMC) held 13 August 2015 along with adoption of the

2015/2016 annual budget.

The Shire’s LTFP was reviewed

in December 2015 and again in May 2016 to inform the 2016/2017 budget process

and the desk top review of the 2016/17 Corporate Business Plan. The

Shire’s Asset Management Plans are currently undergoing a full review as

part of the full integrated planning framework review.

The Audit Committee is requested to

consider and recommend adoption of the annual financial report to Council.

COMMENT

Chief Executive Officer’s

Report to the Audit Committee

Following is the CEO’s report

to the Audit Committee on matters arising from the audit and management

reports. Extracts from the audit and management reports are indented in

italics.

Audit Report

There were no matters of statutory

non-compliance reported.

Management Report

The Auditor’s Management Report

provides an overview of the approach undertaken in respect of the annual audit

process and the associated outcomes of the audit. The Management Report also

identifies any findings that, whilst generally not material in relation to the

overall audit of the financial report, are considered relevant to the day to day

operations of the Shire.

1. Matters Identified

There were

no issues identified.

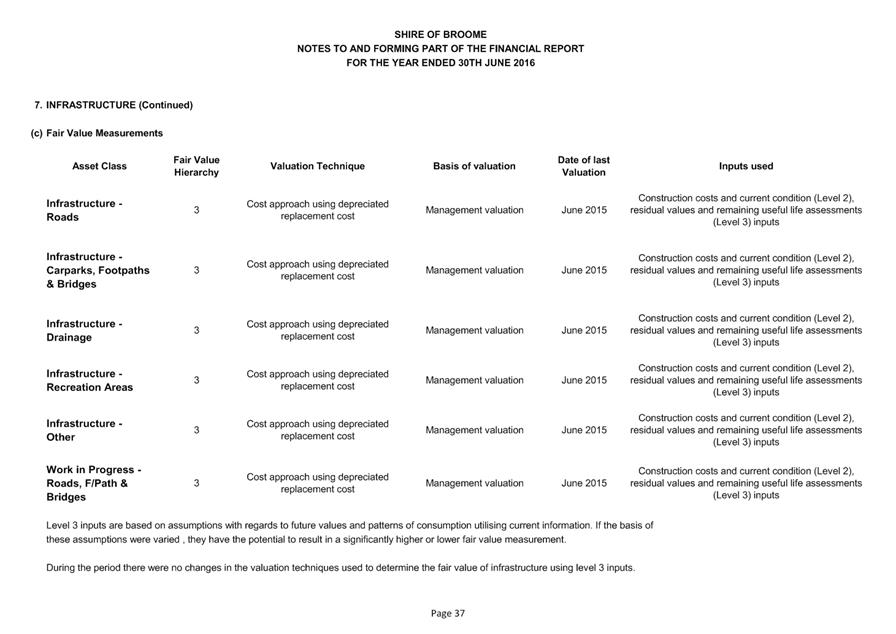

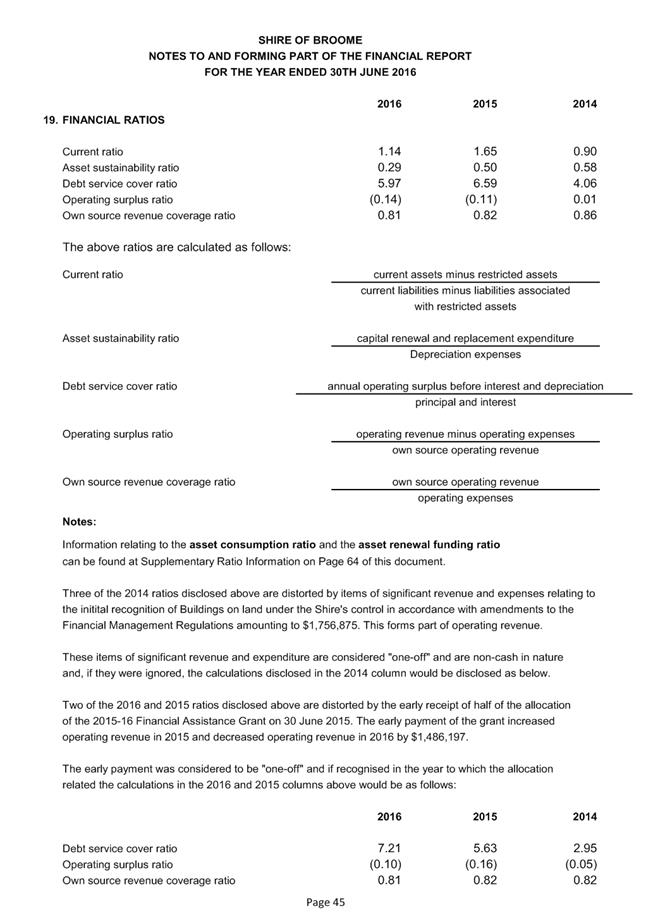

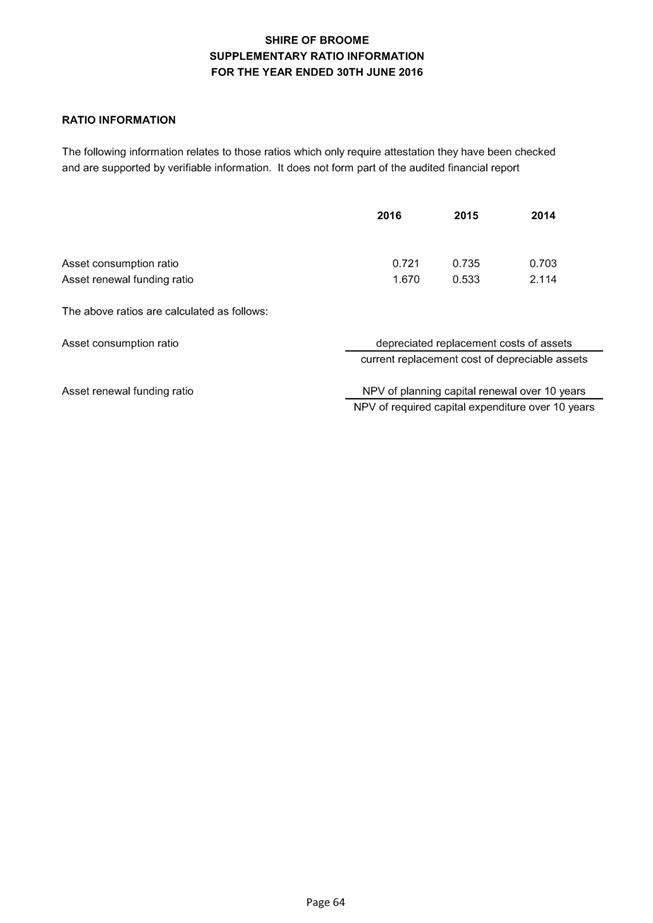

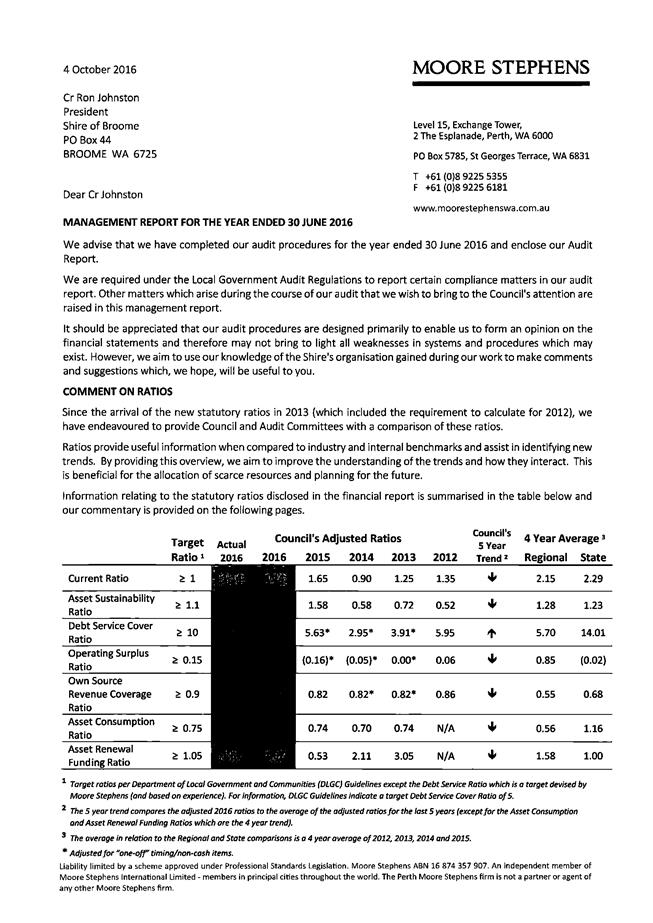

The Auditor provided comment on the

Shire’s ratios, in particular the impact of the revaluation of

infrastructure assets conducted during the year ended 30 June 2015 on the Asset

Sustainability Ratio. 2015/2016 is the first full year of operations

since the revaluation and the full impact of the increase in depreciation was

realised.

Management is identifying strategies

to address the concerns relating to the condition assessment and remaining

useful life which contributed to the higher level of depreciation.

The Auditor’s comments on

ratios is specifically discussed within the Management Report, as appended to

the 2015/2016 Annual Financial Report as Attachment 2 to this report.

2. Audit Adjustments

Following the presentation of the

Draft 2015/2016 Financial Report to the Auditor, officers actioned one

amendment for an accrued liability in line with materiality risks.

3. Other Matters

There were no identified matters of

fraud to report and there were no disagreements with management about

significant accounting matters.

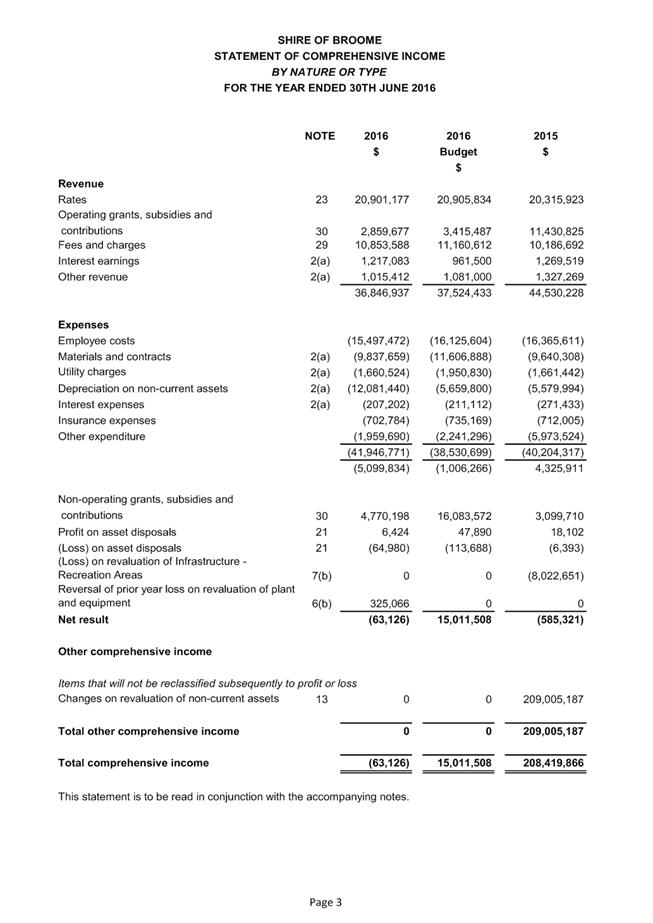

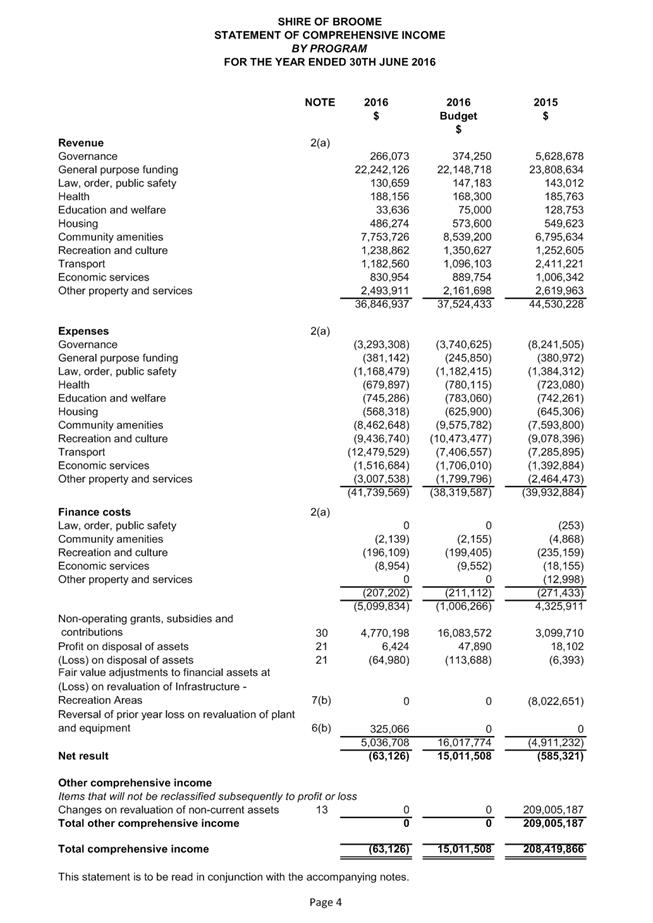

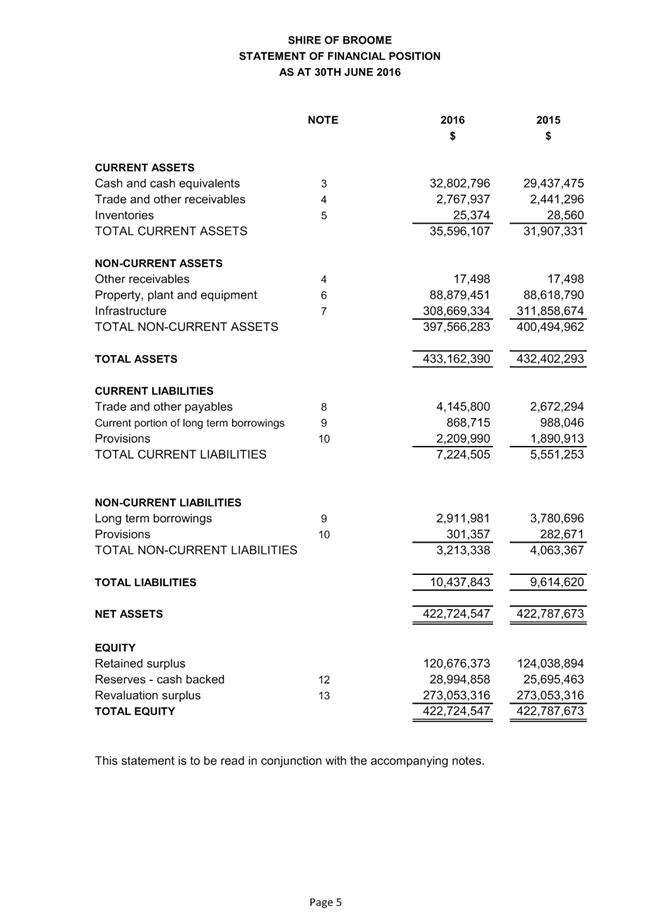

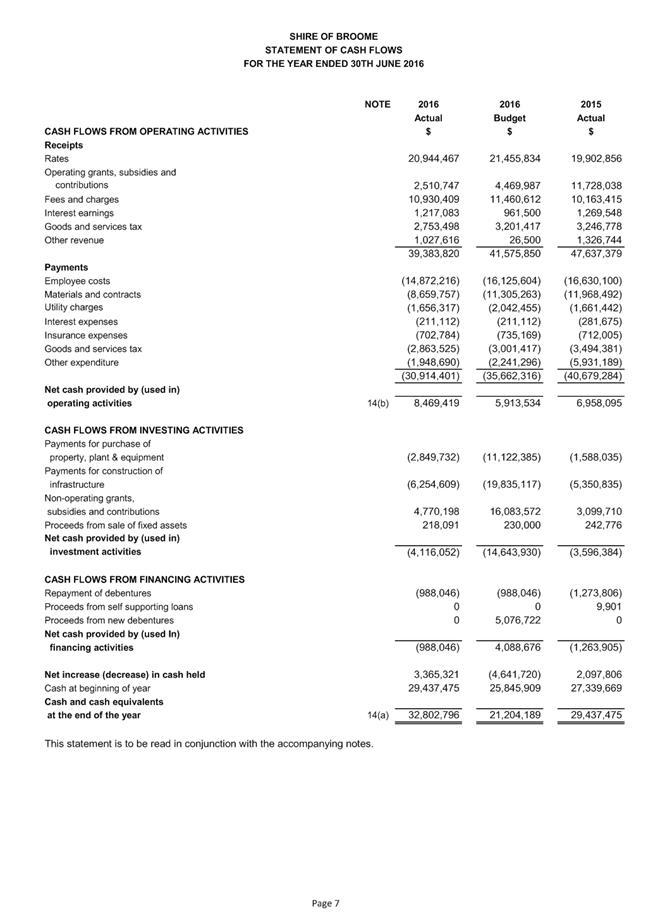

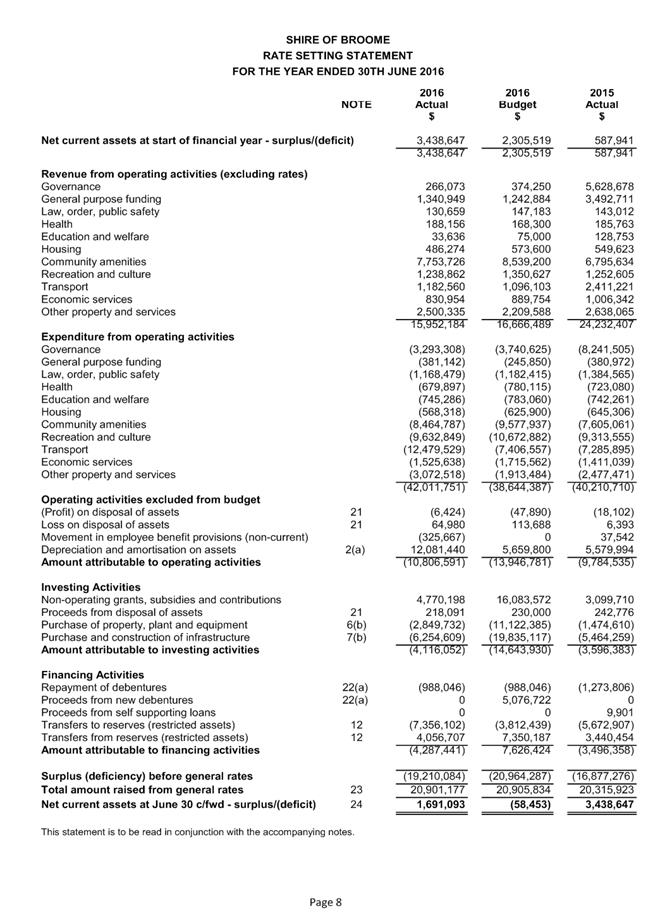

2015/2016 Operating Result

The financial year ended 30 June 2016

resulted in the following carried forward operating surplus:

$

601,252 Budgeted 2015/2016 operating

surplus (as per 2016/2017 adopted annual

budget)

$1,691,093

Actual 2015/2016 operating surplus

Note, this surplus is exclusive of

non-cash transactions such as depreciation and the effects of asset revaluation

gains or losses.

The year end operating surplus result

for 2015/2016 occurred through a number of factors. $730K is attributable to

projects or activities which were not complete as at 30 June 2016 and are

proposed to be carried forward into 2016/2017.

Other factors include a number of

budget analysis and reviews to realise organisational savings across the Shire.

These include savings in fringe benefits tax and other employee expenses (other

than wages) of $246K and unspent materials and contracts across primarily

operating activities/projects of $580K. Savings in utilities of $87K include

anticipated increases in electricity utilities which did not occur as

previously estimated and implementation of public open space strategies to

reduce water usage. Savings of $109K in plant repairs, parts, fuel and tyres

which was primarily the result of anticipated fuel increases not occurring.

Interim and back rates have sourced additional rates revenue of $46K as

developments have finalised, and reviews of non-rateable properties in the

Shire’s database have been undertaken. Additional interest revenue of

$41K was earned in the period.

However, these savings were offset by

a number of target shortfalls in income. These include $307K in fees and

charges revenue from pool inspections, Civic Centre venue user charges, Haynes

Oval and Pavilion usage, power reimbursements for the use of Father McMahon

Sports field and statutory building and application fees, as well as a

shortfall in projected rental income from staff housing and the reimbursement

of income previously raised for the Telstra Broome West Site Depot in 2014-15.

The 2016/2017 Annual Budget that was

adopted at the Ordinary Meeting of Council held 30 June 2016, adopted an

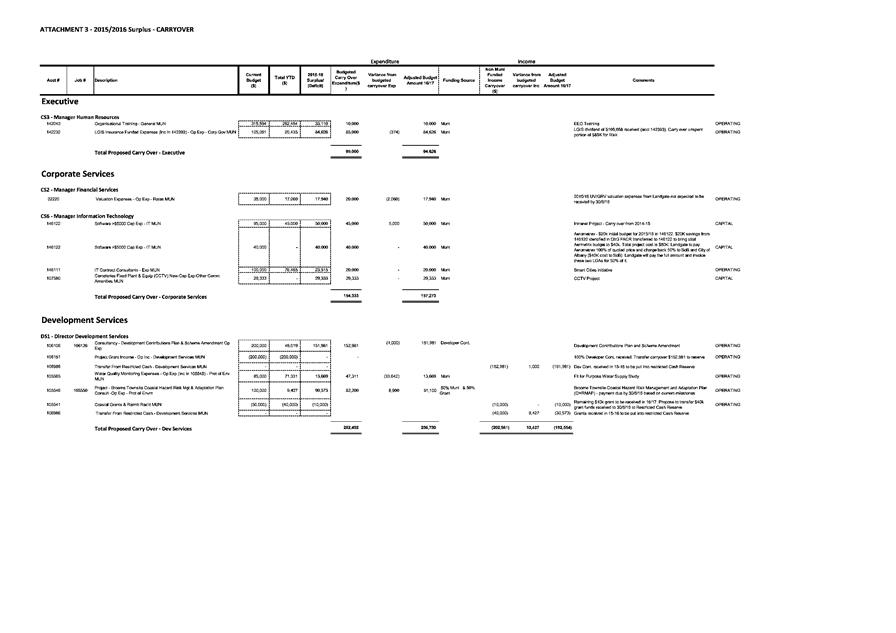

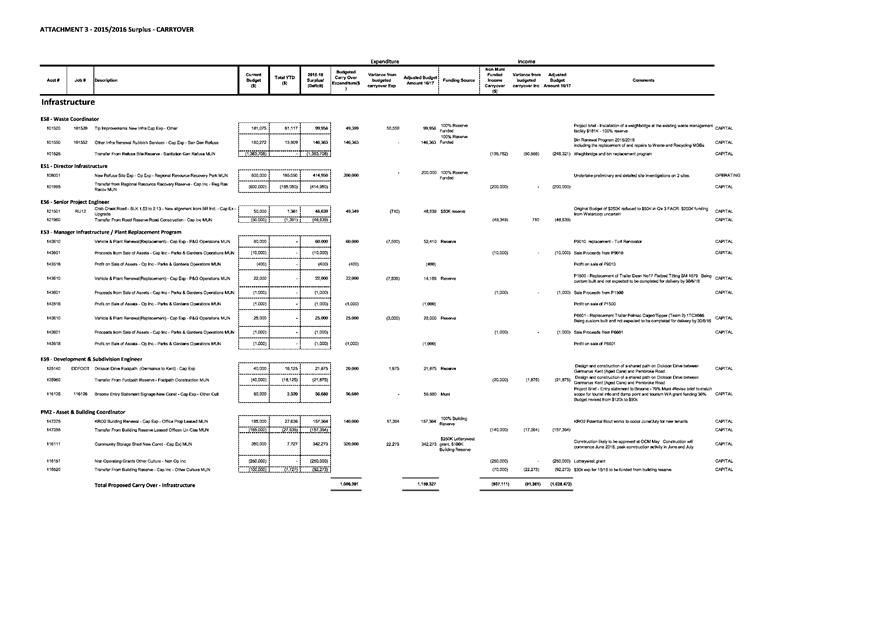

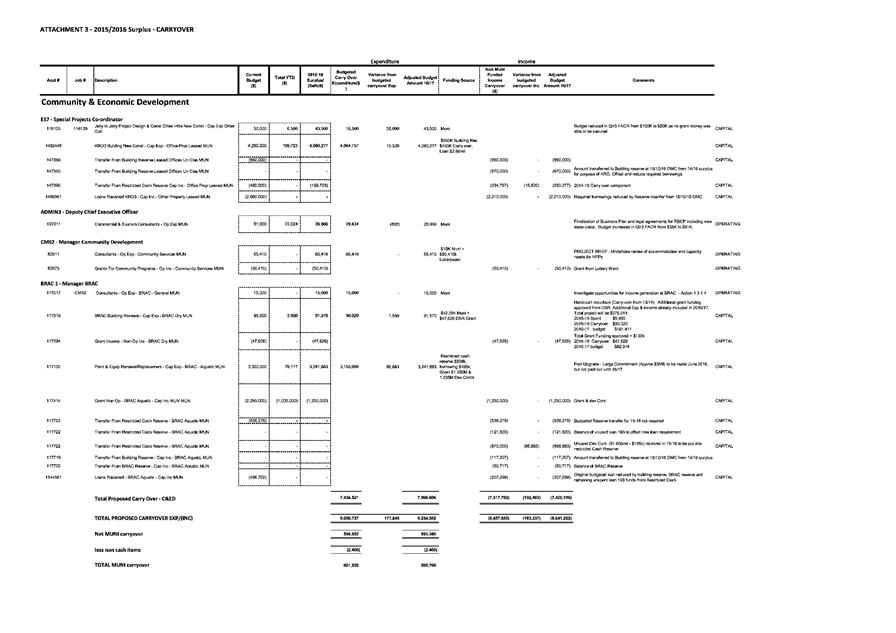

estimated brought forward operating surplus of $601,252. This was comprised of

a number of operating and capital projects which are detailed in Attachment 3.

The estimated budgeted surplus was

calculated prior to the close of financial year processing. The actual brought

forward surplus for these projects, as adjusted for final actual expenditure or

income is $595,760.

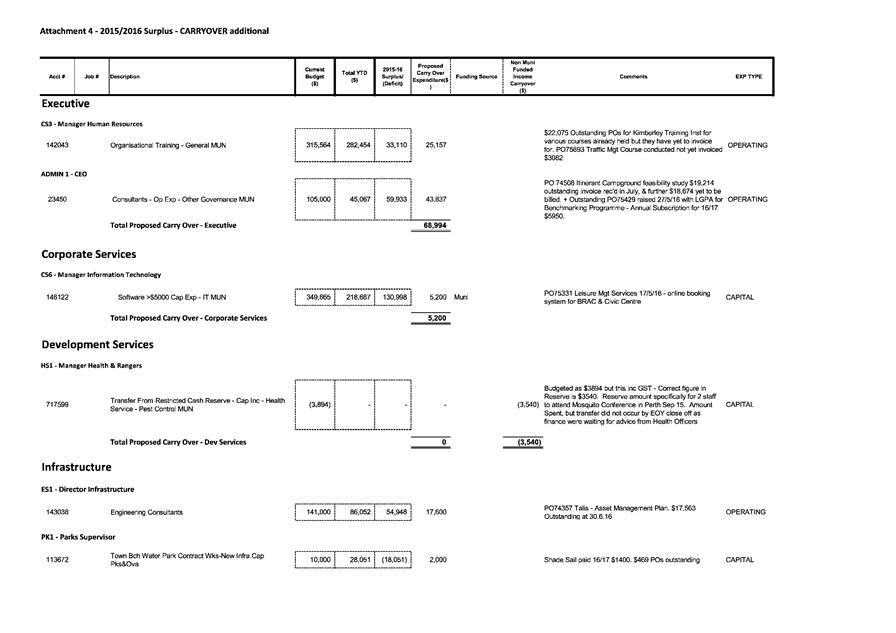

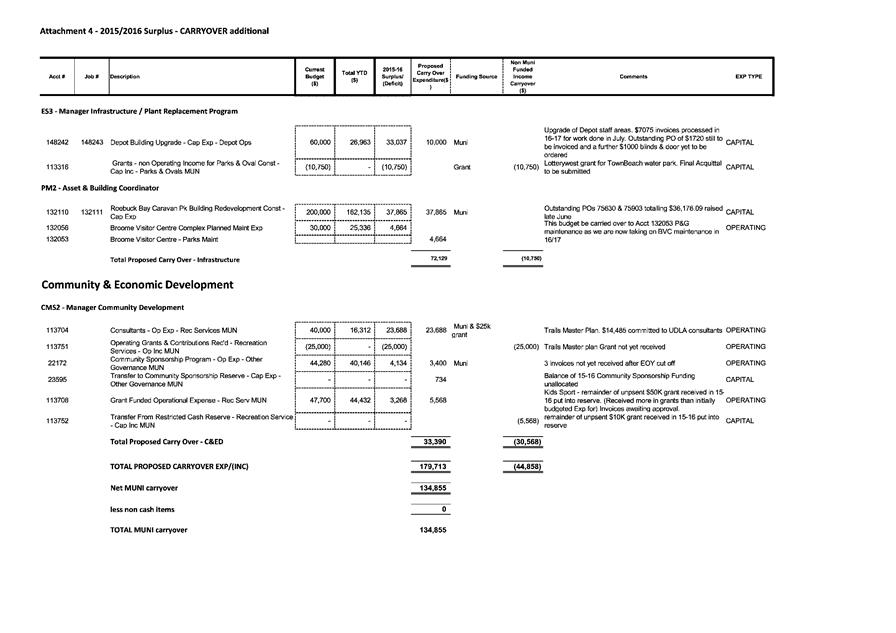

A further $134,855 of the carried

forward surplus pertains to operating activities or capital projects which were

not completed as expected, by 30 June 2016. These projects or operational

activities are listed in Attachment 4. The amounts represent expenditure

committed prior to 30 June 2016 either by executed contract or purchase orders,

where work was not completed or supplier invoices not received, by close of

financial year processing.

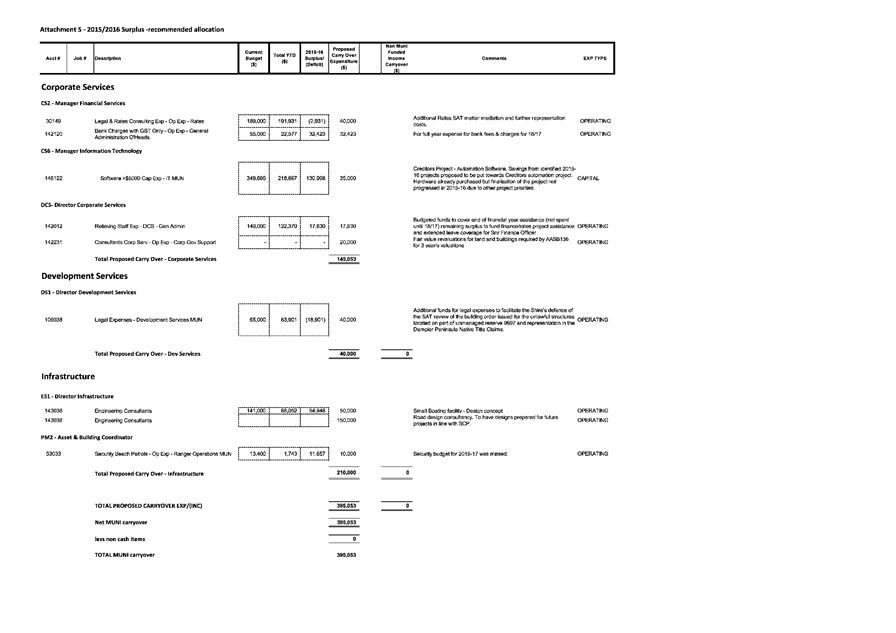

It is recommended that $395,053 of

the surplus be utilised for those operational activities or capital projects

listed in Attachment 5. The proposed items mainly pertain to expected

additional legal expenses which have arisen as a result of recent events and

$150,000 for engineering consultants.

In relation to the additional

expenditure for engineering consultants, it is proposed to adjust the timing of

the initial design work for infrastructure projects to allow better timing of

delivery within the financial year. Major infrastructure projects can not

commence until detailed plans and designs have been completed. Currently,

our budget process includes the design and construction phase within the same

financial year. Not being able to commence the design phase until adoption of

the budget, most often means that the project is not ready to commence actual

construction until after the completion of the wet season. It also means that

the Shire is not prepared when opportunities arise for additional grant

funding. Having projects ‘ready on the shelf’ will allow the

Shire to react quickly to such opportunities.

It is proposed that $150,000 of the

surplus funds go towards design of future infrastructure projects (in line with

the Shire’s Corporate Business Plan and Strategic Community Plan). A

detailed design proposal also allows for more accurate costings for

construction, so preparing the design in advance of the budget year of

construction, will ensure more accurate budgeting.

It is recommended that the balance of

unallocated funds of $565,425 be transferred to reserves.

It is proposed that $150,000 be

transferred to the Plant Reserve for the specific purpose of funding the

purchase and installation of a generator for the Shire Administration

Building. Business interruption was a key risk factor in the development

of the Shire’s Business Continuity Plan (BCP) which is currently being

finalised. An expectation exists within the community and state government that

the Shire would lead any recovery from a disaster event, however one of the

major factors impacting the Shire’s ability to provide that support is

the lack of backup power required to get business systems online as soon as

possible after a disaster event. The purpose of the original electrical access

upgrade at the Administration building was to enable an externally sourced back

up generator to be mobilised in case of a disaster event. However, there are

some limitations with this approach due to the availability from the supplier

and the capacity to only support limited areas within the building. Therefore,

the provision is proposed as a risk mitigation strategy as part of the

finalisation of the Business Continuity Plan to be considered.

It is recommended that the balance of

$415,425 be transferred to the Building Reserve to offset and reduce the

anticipated borrowings required for the construction of the new Kimberley

Regional Offices (KRO) building.

The 2016/2017 budget for the KRO

construction (adjusted for 2015/2016 final actual expenditure) is as follows:

|

|

2016/2017

Budgeted Funding Source

|

|

|

2016-17 Estimated Total Expenditure

|

Building Reserve

|

Restricted

Cash Reserve (Prior years unspent allocation)

|

Loan

|

|

KRO 3

Building Construction

|

$5,960,277

|

$1,620,000

|

$250,277

|

$4,090,000

|

The proposed reserve provision would

further reduce the loan component to $3,674,575.

A summary of the recommended surplus

allocation is as follows:

|

SUMMARY OF 2015-16 Surplus

|

|

|

2015-16 TOTAL REPORTED SURPLUS

|

1,691,093

|

|

Recommended allocation of surplus funds:

|

|

|

Carry over as per adopted budgeted (Adjusted for final

2015-16 actuals) Attachment 3

|

595,760

|

|

Additional carry over (represents expenditure committed

prior to 30 June 2016 either by contract or purchase orders, where work was

not completed or invoicing not received by close of Financial Year)

Attachment 4

|

134,855

|

|

Expenditure not committed as at 30 June 2016, but

recommended use of surplus funds for specific projects or operational

requirements. Attachment 5

|

395,053

|

|

Sub-total specified carryover

|

1,125,668

|

|

Total Surplus remaining

|

565,425

|

|

RECOMMENDED RESERVE TRANSFERS

|

|

|

Building Reserve - KRO

|

415,425

|

|

Plant Reserve – BCP actions

|

150,000

|

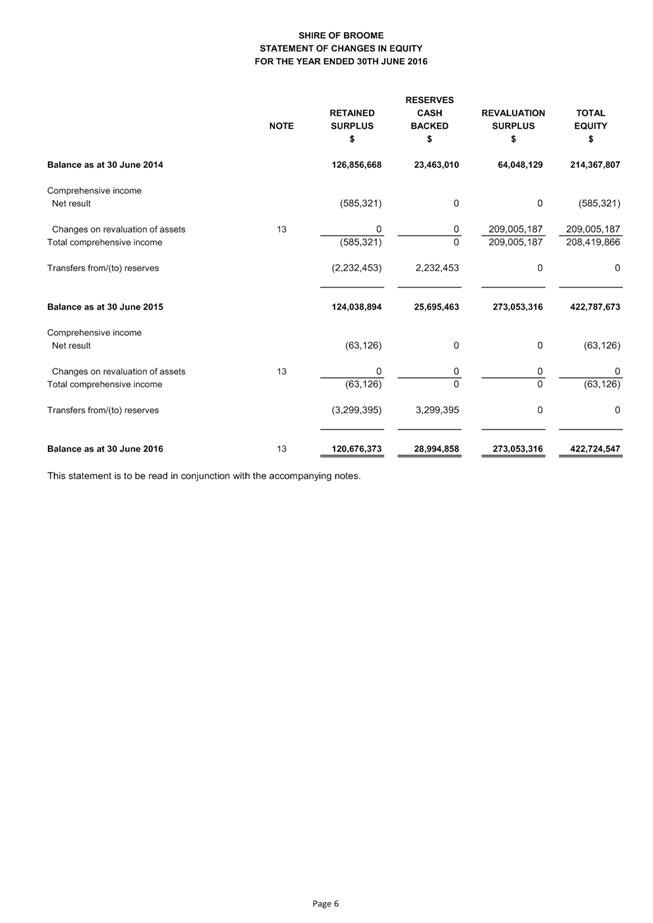

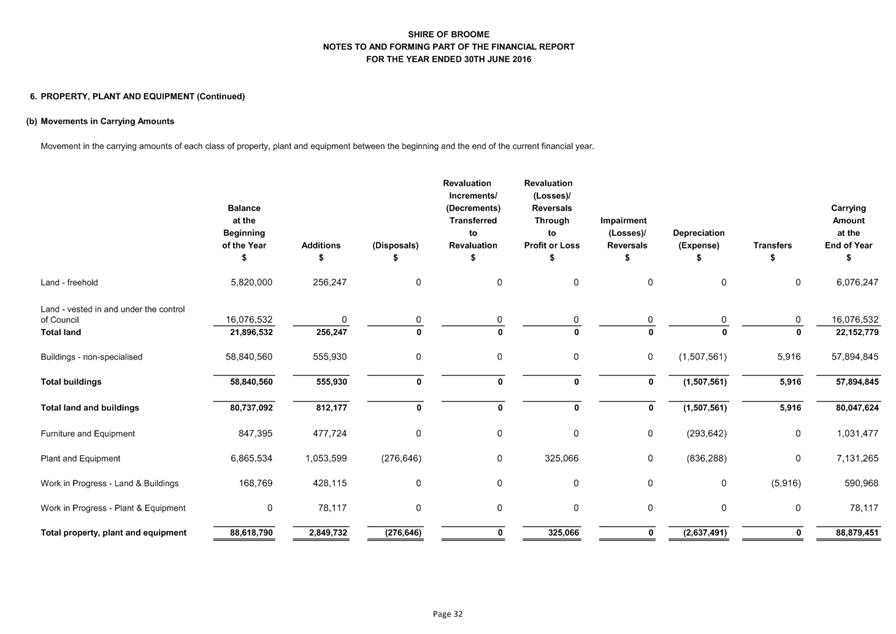

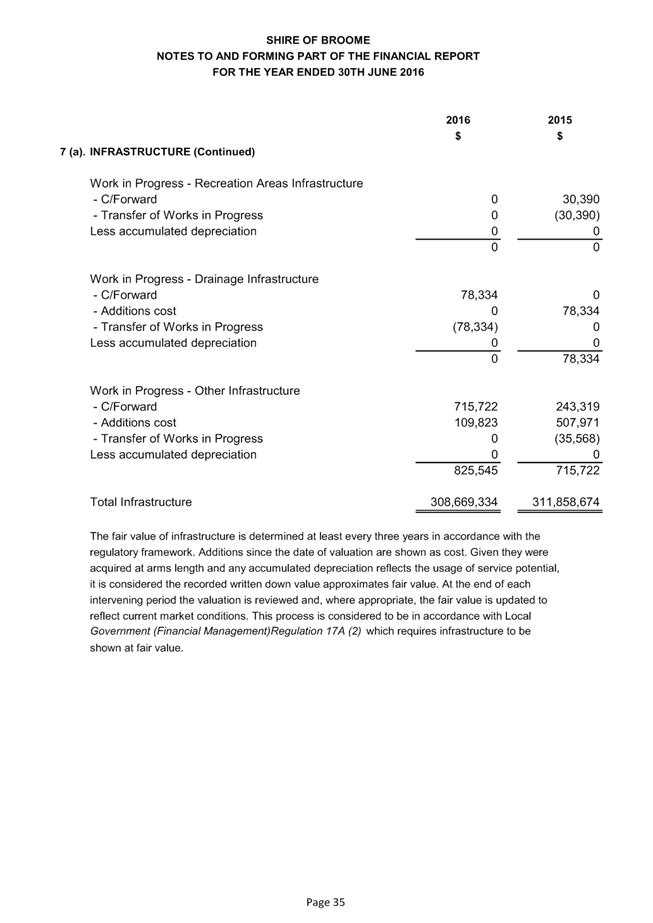

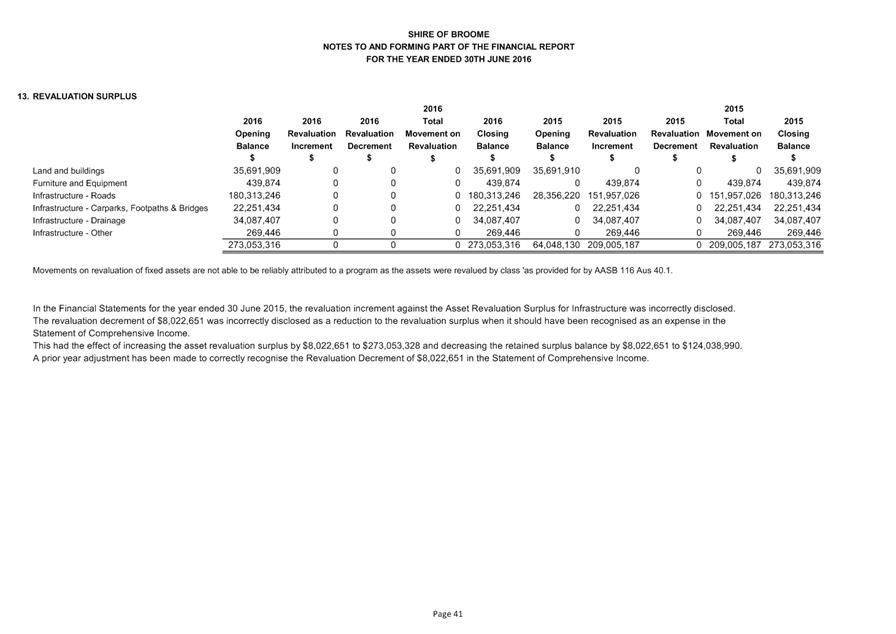

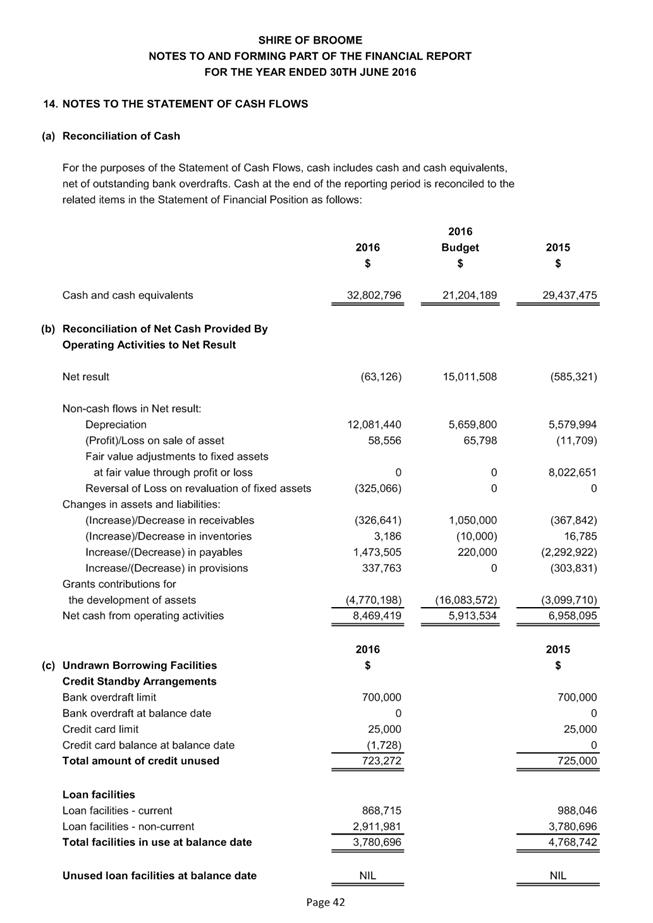

Revaluation of Shire Assets (Fair Value)

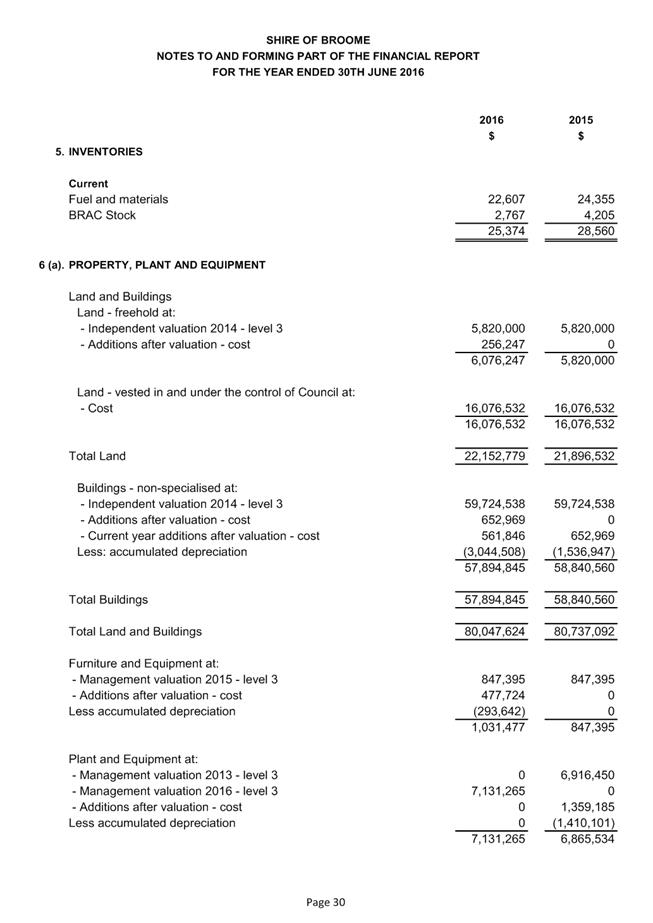

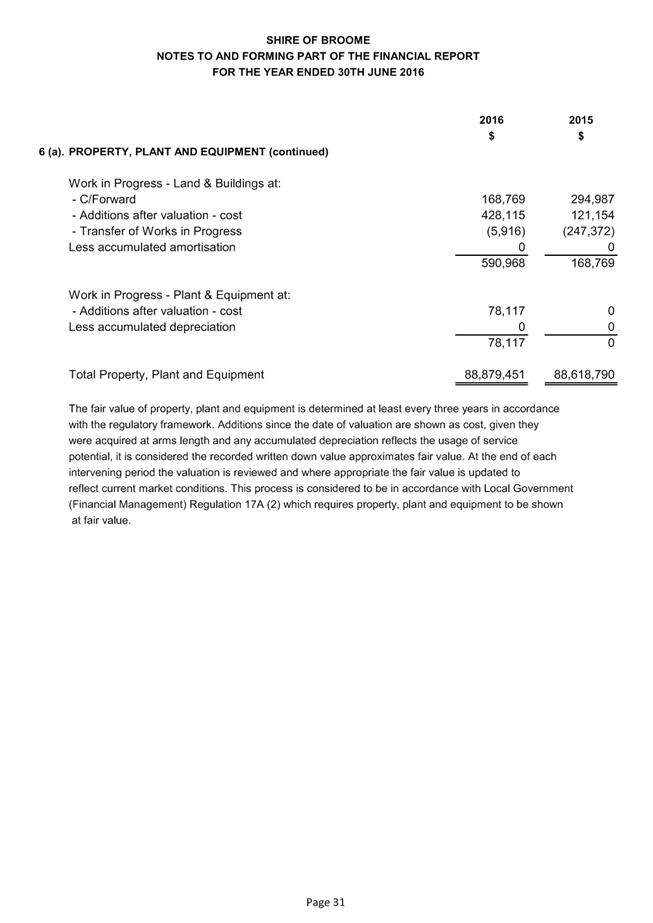

In accordance with regulation 17A of

the Local Government (Financial Management) Regulations 1996, the Shire

must value all assets at fair value and revalue all assets every 3 years. Fair

value requirements came into effect in the year ended 30 June 2013. The

Shire is now in the second round of fair value revaluations with the three year

cycle recommencing in the 2015/2016 financial year for the revaluation of plant

and equipment assets.

The initial fair value valuation for

plant and equipment in 2012/2013 resulted in a decrement (or loss) which was

shown in the profit and loss of the annual report. The revaluation of plant and

equipment for 2015/2016 resulted in an increase to the fair value. In

accordance with AAS accounting standards this increment must first be offset

against any prior year decrement (or loss) and any credit balance is then to go

to revaluation reserve. The increment recognised in 2015/2016 of $325,066

did not fully offset the prior year revaluation loss.

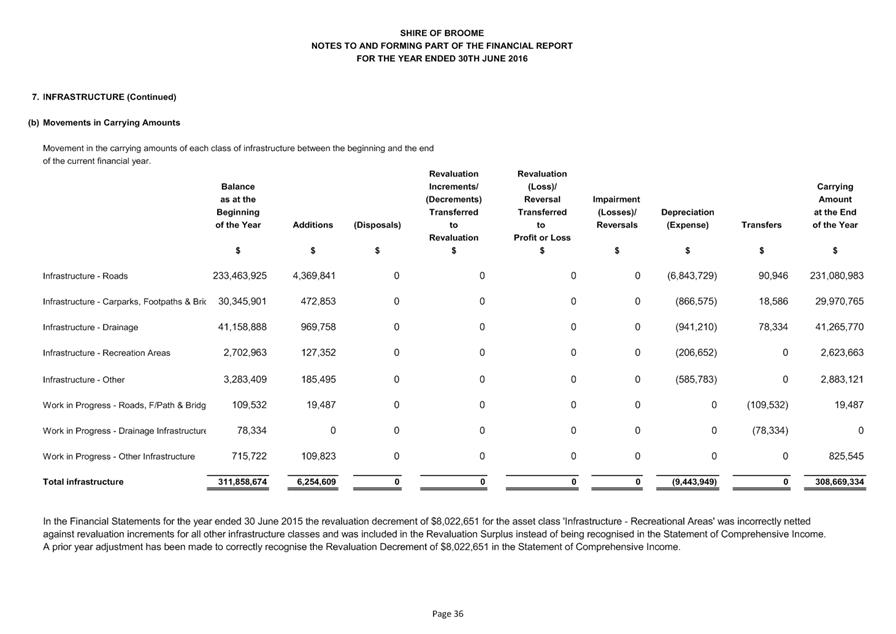

ADJUSTMENTS TO PRIOR YEARS ANNUAL

REPORTS

Following completion and acceptance

of the final audited 2014/2015 annual report, it was brought to the

Shires’ attention by the Department of Local Government and Communities,

that the reported treatment of the fair value valuation of all other assets

which occurred in 2014/2015 was incorrect.

For the year ended 30 June 2015, the

Shire was required to value all other asset classes at fair value. i.e. those

assets that did not fall under the classes of plant and equipment or land and

buildings.

The result of the valuation was an increment

to each of the classes of ‘Roads’, ‘Carparks, footpaths and

bridges’, ‘Drainage Infrastructure’ and ‘Other

Infrastructure’ totalling $208,565,314 and a decrement to the asset class

‘Recreation Infrastructure’ of $(8,022,651). The combined

impact was an increase in value of $200,542,663. The overall total increment

across all the classes combined, was reported in the Statement of Comprehensive

Income as an increment to the revaluation surplus. This was incorrect. The

decrement for the class ‘Recreation infrastructure’ of $(8,022,651)

should have been reported separately in the statement of comprehensive income

(profit and loss).

A prior year adjustment was completed

as part of the 2015/2016 annual report preparation to rectify this error.

The recognition of the decrement through the profit and loss has no impact on

the carried forward surplus which is calculated excluding non-cash items.

Further adjustments were made to

2014/2015 reports in relation to the categorisation of utility expenses and reimbursements.

Telephone expenses have previously been reported under the nature and type of

utility expenses when they should have been categorised as materials and

contracts. Similarly, reimbursements have previously been reported

as operating grants, subsidies and contributions when they should have been

reported as other revenue. The 2015/2016 report has been prepared with the

correct categorisations and adjustments were made to the report for 2014/2015

for comparative purposes. There is nil impact to the net result.

CONSULTATION

Nil

STATUTORY ENVIRONMENT

Local

Government Act 1995

6.4. Financial

report

(1) A

local government is to prepare an annual financial report for the preceding

financial year and such other financial reports as are prescribed.

(2) The

financial report is to —

(a) be

prepared and presented in the manner and form prescribed; and

(b) contain

the prescribed information.

(3) By

30 September following each financial year or such extended time as the

Minister allows, a local government is to submit to its

auditor —

(a) the

accounts of the local government, balanced up to the last day of the preceding

financial year; and

(b) the

annual financial report of the local government for the preceding financial

year.

7.9. Audit

to be conducted

(1) An

auditor is required to examine the accounts and annual financial report

submitted for audit and, by the 31 December next following the financial

year to which the accounts and report relate or such later date as may be

prescribed, to prepare a report thereon and forward a copy of that report

to —

(a) the

mayor or president; and

(b) the

CEO of the local government; and

(c) the

Minister.

(2) Without

limiting the generality of subsection (1), where the auditor considers

that —

(a) there

is any error or deficiency in an account or financial report submitted for

audit; or

(b) any

money paid from, or due to, any fund or account of a local government has been

or may have been misapplied to purposes not authorised by law; or

(c) there

is a matter arising from the examination of the accounts and annual financial

report that needs to be addressed by the local government, details of that

error, deficiency, misapplication or matter, are to be included in the report

by the auditor.

(3) The

Minister may direct the auditor of a local government to examine a particular

aspect of the accounts and the annual financial report submitted for audit by

that local government and to —

(a) prepare

a report thereon; and

(b) forward

a copy of that report to the Minister,

and

that direction has effect according to its terms.

(4) If

the Minister considers it appropriate to do so, the Minister is to forward a

copy of the report referred to in subsection (3), or part of that report,

to the CEO of the local government to be dealt with under section 7.12A.

7.12A. Duties

of local government with respect to audits

(1) A

local government is to do everything in its power to —

(a) assist

the auditor of the local government to conduct an audit and carry out his or

her other duties under this Act in respect of the local government; and

(b) ensure

that audits are conducted successfully and expeditiously.

(2) Without

limiting the generality of subsection (1), a local government is to meet

with the auditor of the local government at least once in every year.

(3) A

local government is to examine the report of the auditor prepared under

section 7.9(1), and any report prepared under section 7.9(3)

forwarded to it, and is to —

(a) determine

if any matters raised by the report, or reports, require action to be taken by

the local government; and

(b) ensure

that appropriate action is taken in respect of those matters.

(4) A

local government is to —

(a) prepare

a report on any actions under subsection (3) in respect of an audit

conducted in respect of a financial year; and

(b) forward

a copy of that report to the Minister, by the end of the next financial year,

or 6 months after the last report prepared under section 7.9 is

received by the local government, whichever is the latest in time.

5.54. Acceptance

of annual reports

(1) Subject

to subsection (2), the annual report for a financial year is to be

accepted* by the local government no later than 31 December after that

financial year.

* Absolute majority required.

(2) If

the auditor’s report is not available in time for the annual report for a

financial year to be accepted by 31 December after that financial year,

the annual report is to be accepted by the local government no later than 2

months after the auditor’s report becomes available.

Local Government (Audit)

Regulations 1996

10. Report

by auditor

(4)

Where it is considered by the

auditor to be appropriate to do so, the auditor is to prepare a management

report to accompany the auditor’s report and to forward a copy of the

management report to the persons specified in section 7.9(1) with the

auditor’s report.

Local Government (Financial

Management) Regulations 1996

17A Assets,

valuation of for financial reports etc.

(1) In

this regulation —

fair value,

in relation to an asset, means the fair value of the asset measured in

accordance with the AAS.

(2) Subject

to subregulation (3), the value of an asset shown in a local

government’s financial reports must be the fair value of the asset.

(3) A

local government must show in each financial report —

(a) for

the financial year ending on 30 June 2013, the fair value of all of

the assets of the local government that are plant and equipment; and

(b) for

the financial year ending on 30 June 2014, the fair value of all of

the assets of the local government —

(i) that

are plant and equipment; and

(ii) that

are —

(I) land

and buildings; or

(II) infrastructure;

and

(c) for

a financial year ending on or after 30 June 2015, the fair value of

all of the assets of the local government.

(4) A

local government must revalue all assets of the local government of the classes

specified in column 1 of the Table to this subregulation —

(a) by

the day specified in column 2 of the Table; and

(b) by

the expiry of each 3 yearly interval after that day.

Table

|

Class of asset

|

Day

|

|

Plant and equipment

|

30 June 2016

|

|

Land, buildings and infrastructure for which the fair

value was shown in the local government’s annual financial report for

the financial year ending on 30 June 2014

|

30 June 2017

|

|

All other classes of asset

|

30 June 2018

|

(5) A

revaluation under subregulation (4) must be based on the value of the

asset as at a time that is as close as possible to the day by which the

revaluation is due.

POLICY IMPLICATIONS

2.1.1 - Materiality in Financial

Reporting

2.1.4 - Significant Accounting

Policies

FINANCIAL IMPLICATIONS

In terms of materiality, the

unallocated surplus amount of $960,478 (surplus excluding the committed

expenditure of Attachment 2 and 3) represents a variance of 2.56% compared to

budgeted operating revenue for 2015/2016 of $37,524,433 (excluding

non-operating grants and contributions for assets and profit on sale of

assets). This is 1.56% over the adopted threshold of 1% ($375,244) as per

policy 2.1.1 Materiality in Financial Reporting.

RISK

The audited Annual Financial Report

is a key control measure used to report to Council and its stakeholders to

provide assurance that all systems, processes and controls have been

established by the CEO to minimise the risk of any material misstatement or

loss caused by fraud or error. The audit findings indicate areas requiring

improvement and management have implemented measures to review processes. The

report measures Council’s financial capacity to achieve its adopted

strategic and operational objectives. A material variance indicates areas

requiring investigation such as budget estimation/formulation, workforce management

and Council’s overall resource capacity to achieve its strategic

objectives.

The recommendation by the Audit

Committee to Council for the adoption of the Annual Financial Report, Audit and

Management Report and CEO’s report is a key statutory compliance matter.

Should this not be recommended for adoption, this will cause a delay in

Council’s adoption of the 2015/2016 Annual Report to be presented at the

October Ordinary Meeting of Council, which will flow on to delaying the Annual

Electors Meeting (AEM). This poses a high risk due to the possible likelihood

of occurring and the impact of a significant delay to major deliverables.

In regards to the proposed allocation

of the 2015/2016 surplus, should the Audit Committee make alternative

recommendations, the long term financial impacts of such should be analysed to

ensure there are no adverse impacts to Council’s future financial

sustainability and should be in line with the adopted LTFP. In line with

Council’s risk ratings, the risk is assessed as extreme where the

financial impact is greater than $150,000 and the likelihood of this occurring

is possible. To mitigate these risks, the report recommendations are required

to be adopted.

STRATEGIC

IMPLICATIONS

Our People Goal – Foster a

community environment that is accessible, affordable, inclusive, healthy and

safe:

Encourage communication.

Identify affordable services and

initiatives to satisfy community needs.

Our Prosperity Goal – Create

the means to enable local jobs creation and lifestyle affordability for the

current and future population:

Encourage the provision of affordable

land for residential, industrial, commercial and community use.

Our Organisation Goal –

Continually enhance the Shire’s organisational capacity to service the

needs or a growing community:

Develop an organisational culture

that strives for service excellence.

Review and analyse strategic and

operational plans.

Manage resource allocation.

Manage staff attraction and

retention.

Improve systems, processes and

compliance.

VOTING REQUIREMENTS

Absolute Majority

|

REPORT RECOMMENDATION:

That Council on recommendation from the Audit

Committee:

1. Receives

the Chief Executive Officer’s report relating to the audit.

2. Receives

the Audit Report and Audit Management Report dated 4 October 2016.

3. Adopts

the Annual Financial Report for the year ended 30 June 2016.

4. Allocates the

net operating surplus from the 2015/2016 financial year as per Attachment

3, 4 and 5 with the balance of $565,425 to be transferred to reserves as follows:

a) $415,425

to Building Reserve - for the purpose of offsetting proposed loan funding

for the new KRO building;

b) $150,000

to Plant Reserve – for the purpose of Business Continuity Plan action.

(Absolute Majority Required)

|

Attachments

|

1.

|

2015-2016 Annual

Financial Report

|

|

2.

|

2015-2016 Audit

Management Report

|

|

3.

|

2015-2016 Surplus -

Budgeted Carryover

|

|

4.

|

2015-2016 Surplus -

Carryover Additional

|

|

5.

|

2015-2016 Surplus -

Recommended Allocation

|