Agenda – Ordinary

Meeting of Council 19 October 2017 Page 5 of 6

|

12.1 MINUTES

OF THE AUDIT COMMITTEE MEETING HELD 16 OCTOBER 2017

LOCATION/ADDRESS: Nil

APPLICANT: Nil

FILE: FRE02

AUTHOR: Acting

Director Corporate Services

CONTRIBUTOR/S: Nil

RESPONSIBLE

OFFICER: Director

Corporate Services

DISCLOSURE

OF INTEREST: Nil

DATE OF REPORT: 16

October 2017

|

|

SUMMARY: This

report presents to Council the minutes of the Audit Committee Meeting held 16

October 2017 for receipt and endorsement of the Audit Committee’s

recommendation to adopt the 2016/2017 Annual Financial Report, the Audit and

Management reports, and the report prepared by the Chief Executive Officer

for the financial year ended 30 June 2017. Additionally, Council is requested

to endorse the proposed allocation of the net operating surplus from

2016/2017.

The report also presents Audit Committee recommendations

in relation to the Better Practice Review Report prepared by the Department

of Local Government and Communities.

|

BACKGROUND

Previous

Considerations

Nil

Department of

Local Government and Communities Better Practice Review Program

The Local Government Better Practice

Review (BPR) Program is an initiative undertaken by the Department of Local

Government and Communities (DLGC) to recognise and promote good practice in

Western Australian country local governments. The BPR Program is part of

the State Government’s Country Local Government Fund (CLGF) Capacity

Building Program.

The program has been designed to

acknowledge areas of better practice whilst encouraging improvement in the way

local governments conduct their activities to ensure good governance and build

the capacity of the local government sector.

Whilst the BPR report addresses some

legislative requirements, it is important to note that this is not a compliance

exercise, and feedback is focused on recognising current better practice, as

well as building the capacity of the Shire to achieve better practice across a

range of operations into the future.

Officers initially completed a

self-assessment checklist and provided detailed information and documentation

to the DLGC. An onsite review was conducted in May 2016 where Department

officers met with identified Shire of Broome staff and concluded by attending

the Ordinary Meeting of Council held 26 May 2016.

Annual Financial Report &

Audit Report 2016/2017

Pursuant to Section 7.9 of the Local

Government Act 1995 (LGA), an Auditor is required to examine the

accounts and annual financial report submitted by a local government for audit.

The Auditor is also required, by 31 December following the financial year to

which the accounts and report relate, prepare a report thereon and forward a

copy of that report to:

(a)

Mayor or President; and

(b)

The Chief Executive Officer; and

(c)

The Minister.

Furthermore, in accordance with

Regulation 10(4) of the Local Government (Audit) Regulations 1996 (Audit

Regulations), where it is considered appropriate to do so, the Auditor

may prepare a Management Report to accompany the Auditor’s Report, which

is also to be forwarded to the persons specified in Section 7.9 of the LGA.

On finalisation of the Shire’s

2016/2017 final audit, the Auditors presented their initial findings to the

Audit Committee for consideration at an informal briefing session held Wednesday

6 September 2017, which was attended by Acting Shire President Harold Tracey

and Councillor Desiree Male.

The signed Auditor’s Report was

received dated 3 October 2017. On 16 October 2017, the Audit Committee examined

the reports of the auditor after receiving a report from the Chief Executive

Officer (CEO) on the matters reported and:

· Determined

if any matters raised require action to be taken by the local government;

· Ensured

that appropriate action is taken in respect of those matters;

· Reviewed

the reports prepared by the CEO on any actions taken in respect of any matters

raised in the report of the auditor; and

· Recommended

the audited financial report to Council for adoption.

A copy of

the audited financial report is to be forwarded to the Minister within 6 months

of receipt of the Auditor’s Report.

An analysis of the 2016/2017

operating result is provided in this report and how it compares to the

forecasted outcomes of the Shire’s adopted Integrated Planning and

Reporting Framework. As a background, the 2016/2017 Annual Financial Report

discloses the results of the fifth year of implementation of the legislated

Integrated Planning and Reporting Framework. The plans contained in the

framework provide funding strategies to ensure Council can meet its adopted

strategic objectives, while maintaining and forecasting impacts on the

Shire’s future financial sustainability.

The Strategic Community Plan (SCP)

2017-2027 and Corporate Business Plan (CBP) 2017-2021 were adopted by Council

at the Ordinary Meeting of Council (OMC) on 15 December 2016 and a revised

2017-2032 Long Term Financial Plan (LTFP) was also received by Council at the

December 2016 OMC. The Shire’s LTFP was reviewed in November 2016

to support the review of the SCP and CBP. These plans informed the

2017/2018 annual budget process.

The Shire’s Asset Management

Plans are currently undergoing a full review as part of the mandated integrated

planning framework review process. This review is expected to be finalised in

October with the draft Combined Infrastructure Asset Management Plan presented

to Council in November.

COMMENT

Department of Local Government and

Communities Better Practice Review Program

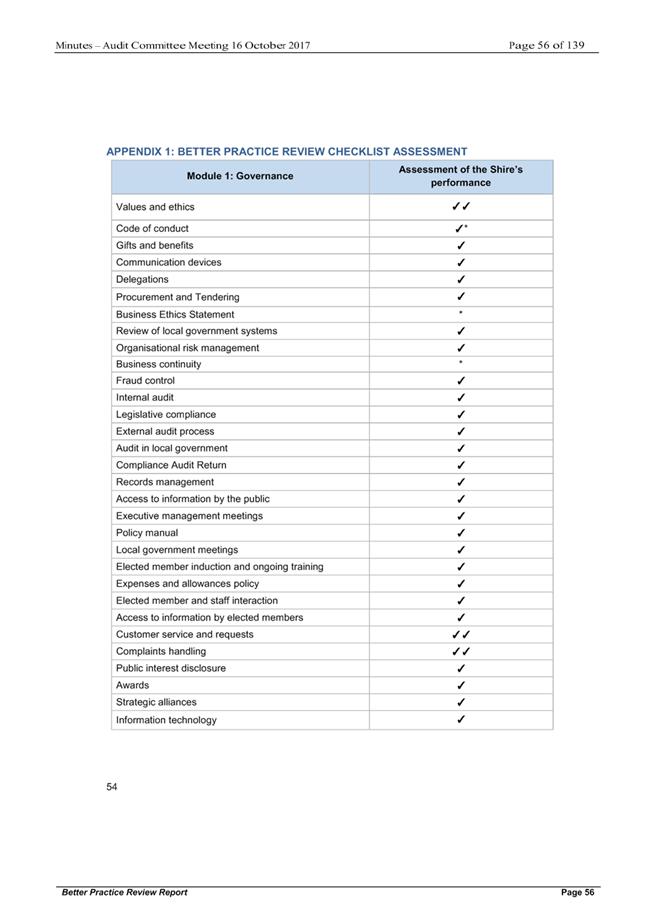

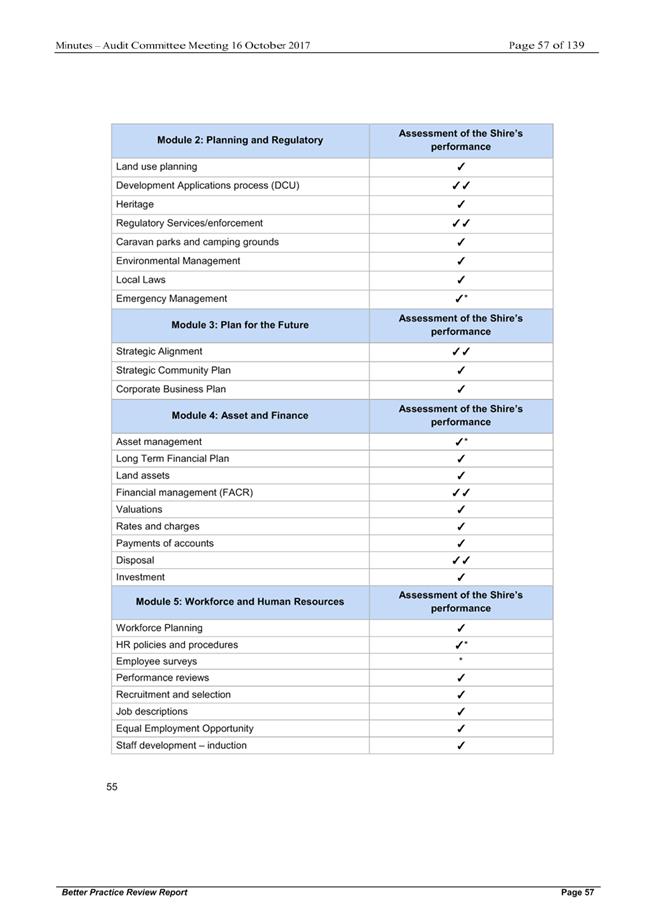

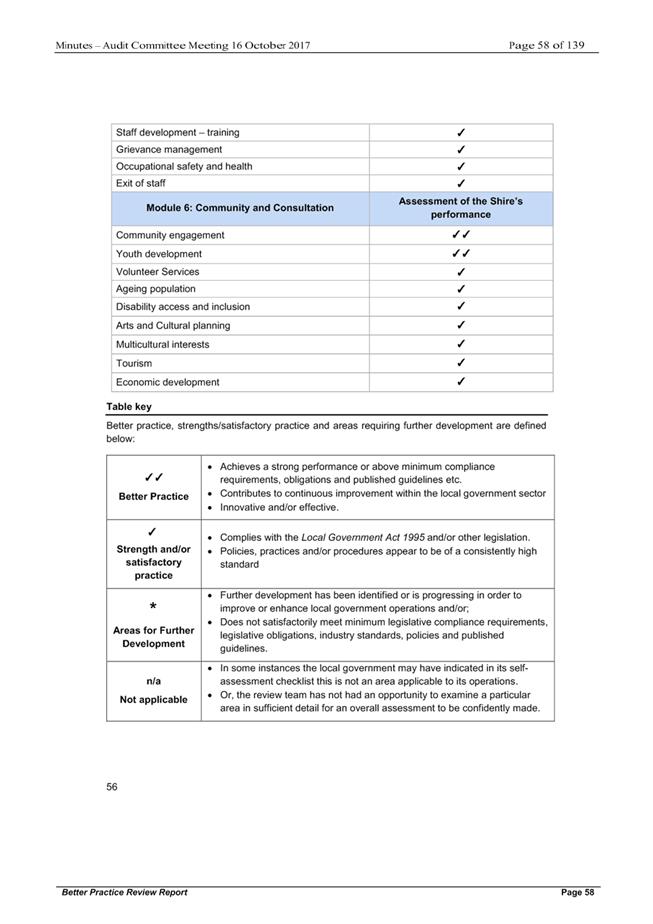

The report identifies areas of better

practice, strengths and areas for further development under the headings of

Governance; Planning and Regulatory; Plan for the Future; Assets and Finance;

Workforce Planning and Human Resource Management; and Community and

Consultation.

The review found “that

the Shire is a high-performing local government which functions well;

displaying a positive organisational culture, good governance and an emphasis

on continuous improvement and innovation across all parts of the organisation.”

“Although the Shire is

performing well, it should be noted there is still room for improvement, and

accordingly, areas for further development have been identified through this

report.”

“The Shire is commended

for the quality and scope of work it has done to date, in addition to the work,

and improvements, it looks to undertake, going forward.”

It should be noted that although the

review was undertaken in May 2016 the finalised BPR document was only received

by the Shire late in May 2017. Delivery of the final document was impacted by

the transition of State Government following the caretaker period prior to and

during the March 2017 State Election.

Following the election, the new

Minister for Local Government issued a letter of acknowledgement to the Shire

President congratulating the Council and staff for the high level of better

practice at the Shire and commending the organisation’s commitment to

innovation. The letter reiterated the comments in the BPR relating to the Shire

being a high performing local government with positive culture, good governance

and an emphasis on continual improvement and innovation.

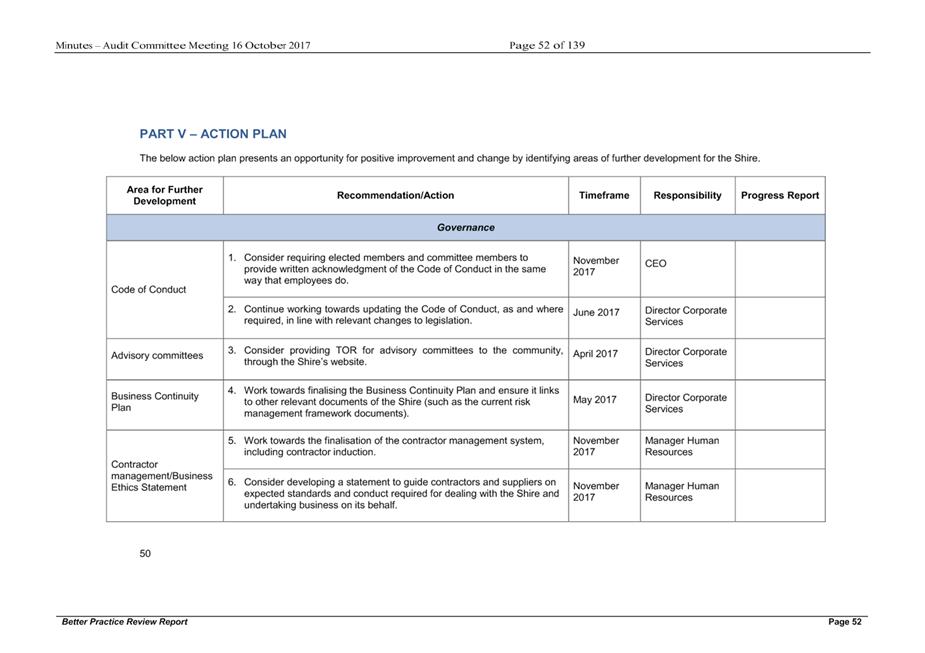

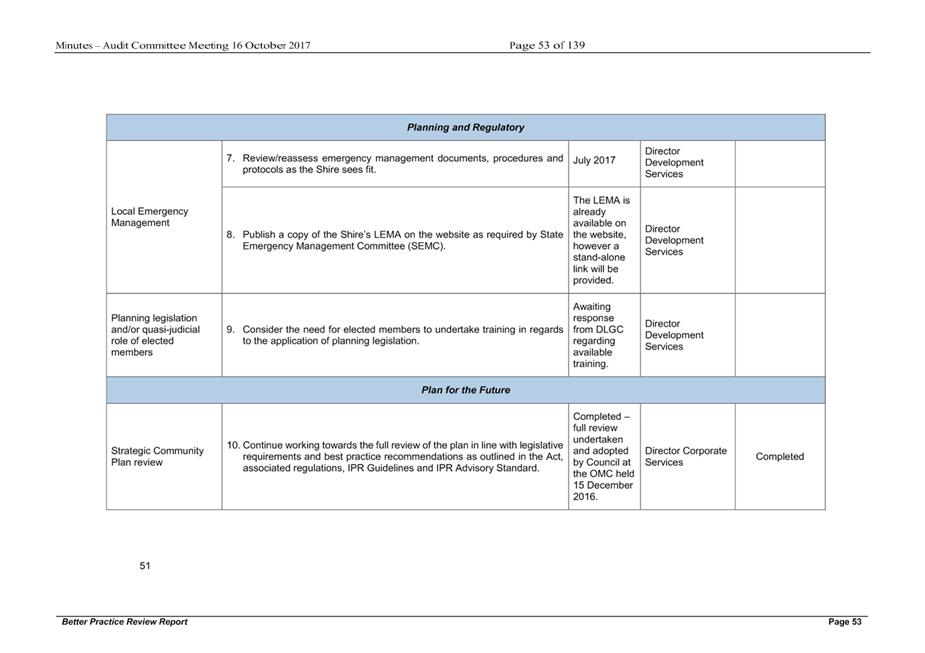

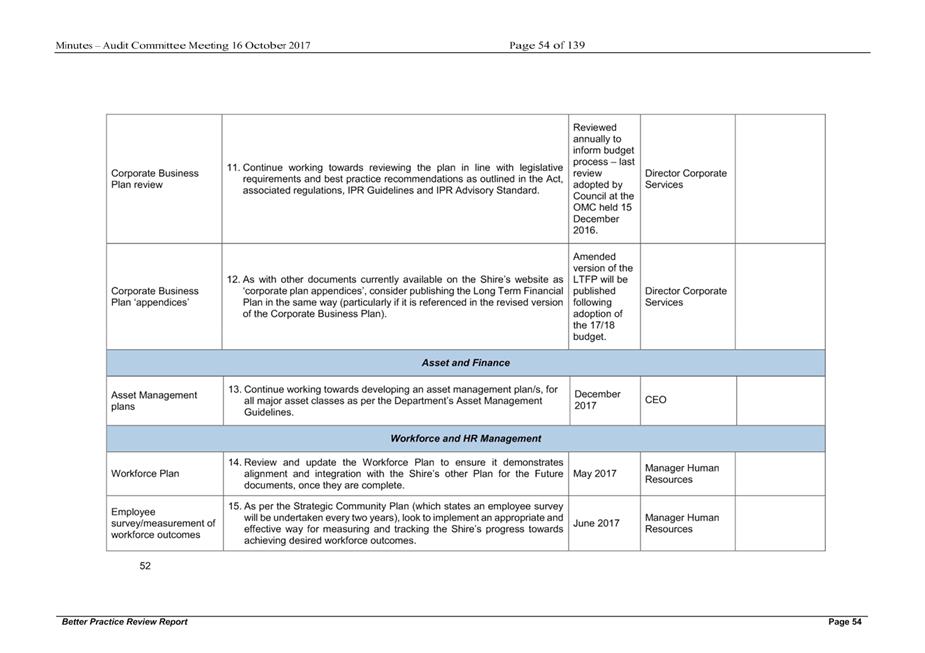

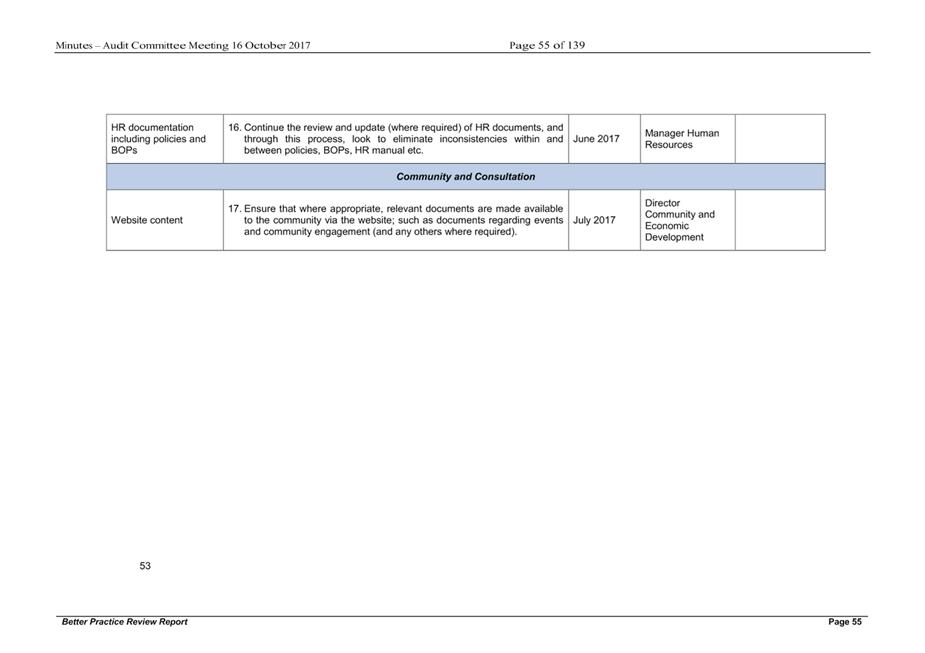

The review also provided an action

plan identifying areas that the Shire could focus on to further improve

operations. These improvements were noted as being “minor in

nature” and will be updated and the resulting action plan presented at

the next Audit Committee meeting.

Annual Financial Report &

Audit Report 2016/2017

Chief Executive Officer’s

Report

Following is the CEO’s report

on matters arising from the audit and management reports. Extracts from the

audit and management reports are indented in italics.

Audit Report

There were no matters of statutory

non-compliance reported.

Management Report

The Auditor’s Management Report

provides an overview of the approach undertaken in respect of the annual audit

process and the associated outcomes of the audit. The Management Report also

identifies any findings that, whilst generally not material in relation to the

overall audit of the financial report, are considered relevant to the day to

day operations of the Shire.

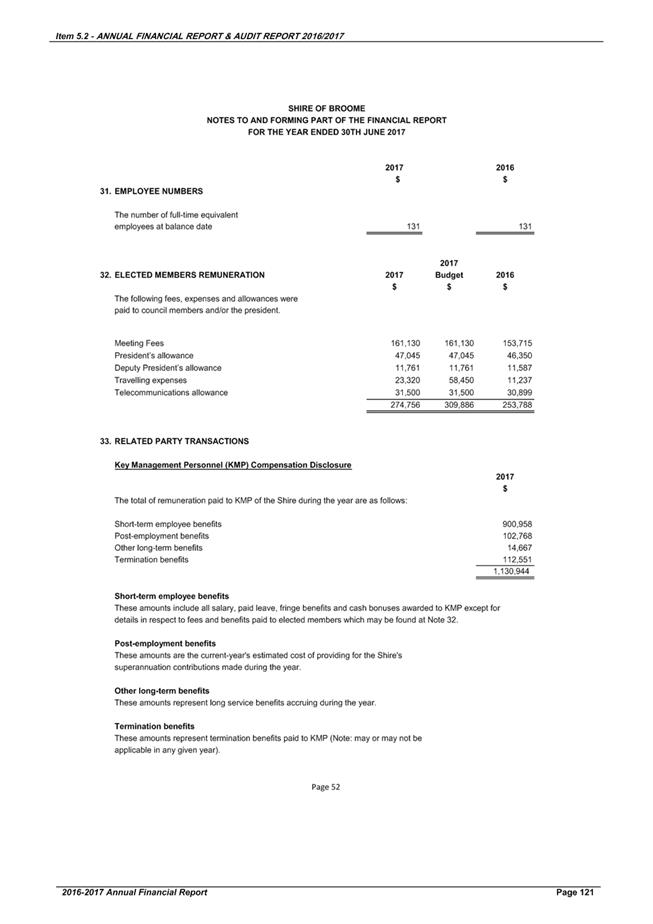

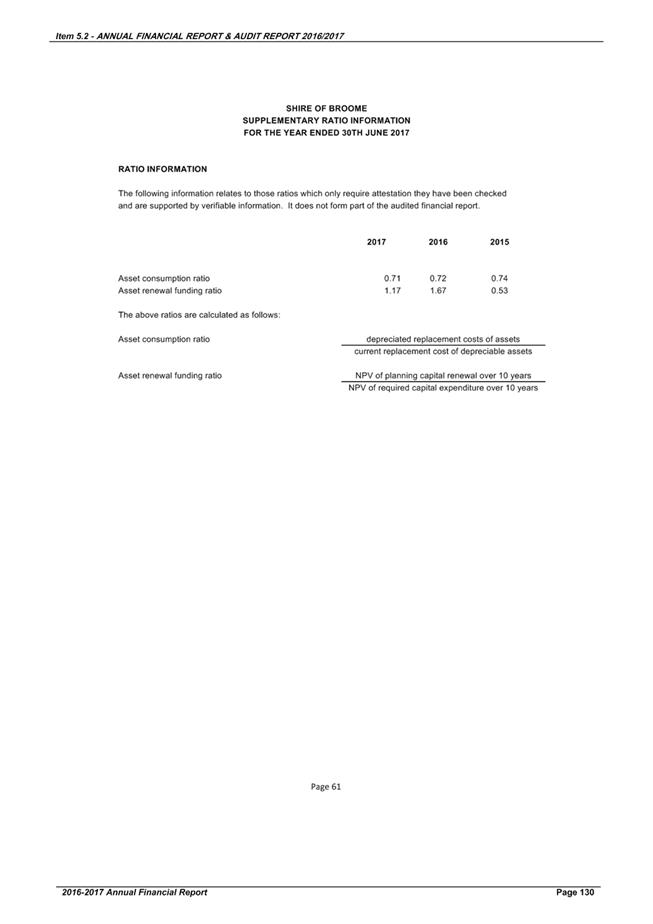

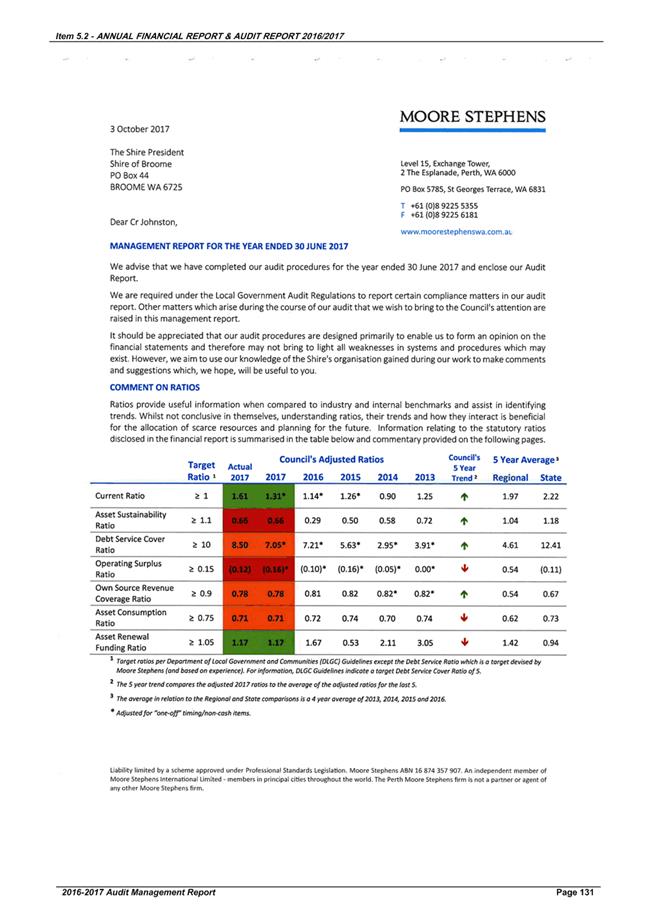

1. Matters Identified

There were

no issues identified.

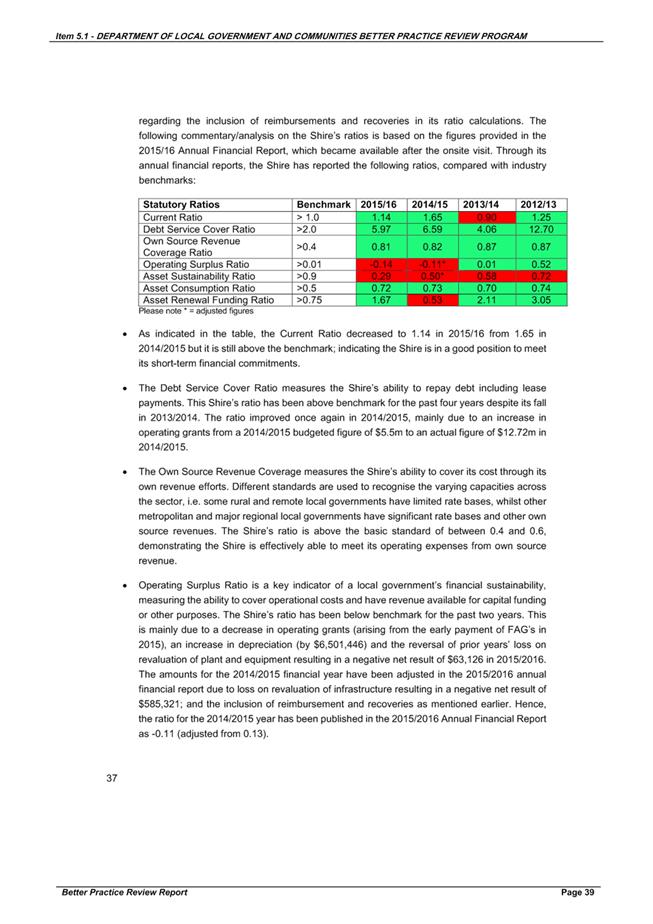

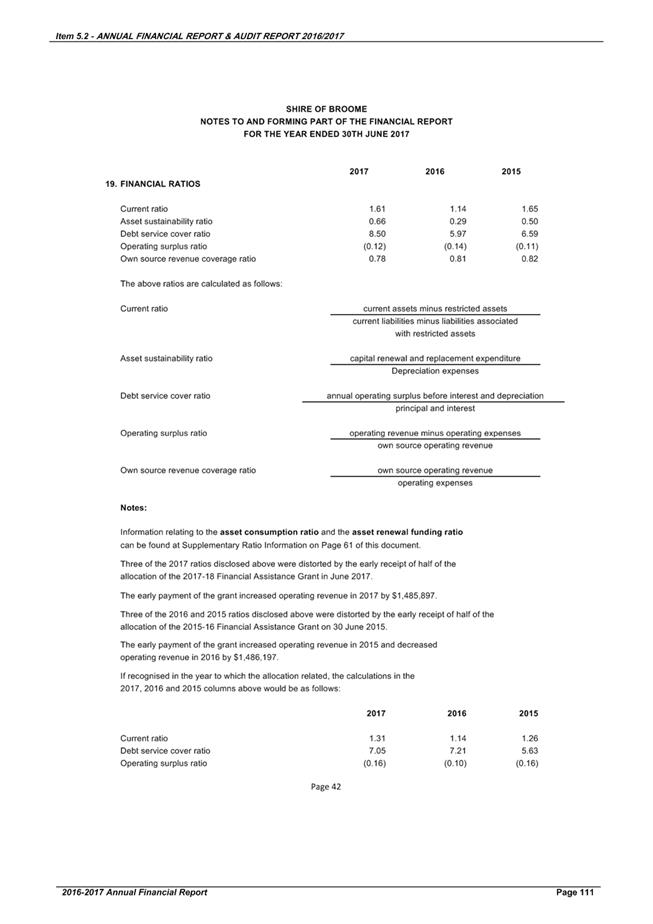

The Auditor provided comment on the

Shire’s ratios, in particular the Asset Sustainability Ratio and the

impact on depreciation resulting from the revaluation of infrastructure assets

conducted during the year ended 30 June 2015. The Auditor noted that this

ratio has improved in the current year but is still below the five year

Regional and State average.

The Auditor also noted the downward

trend of the Shire’s Operating Surplus Ratio over the past five years and

highlighted that Council and Management will need to consider ways to improve

the position by either increasing revenue or decreasing expenditure, or both.

It should be noted however, that the higher levels of depreciation as mentioned

above, have also impacted this ratio.

The concerns relating to the

condition assessment and remaining useful life which contributed to the higher

level of depreciation have been addressed in the revised Asset Management Plan

due to be presented to Council in November 2017. This will be

incorporated in the fair value valuation on infrastructure assets due by 30

June 2018, with the effects realised in the 2018/2019 financial year.

The Auditor’s comments on

ratios are specifically discussed within the Management Report, as appended to

the 2016/2017 Annual Financial Report.

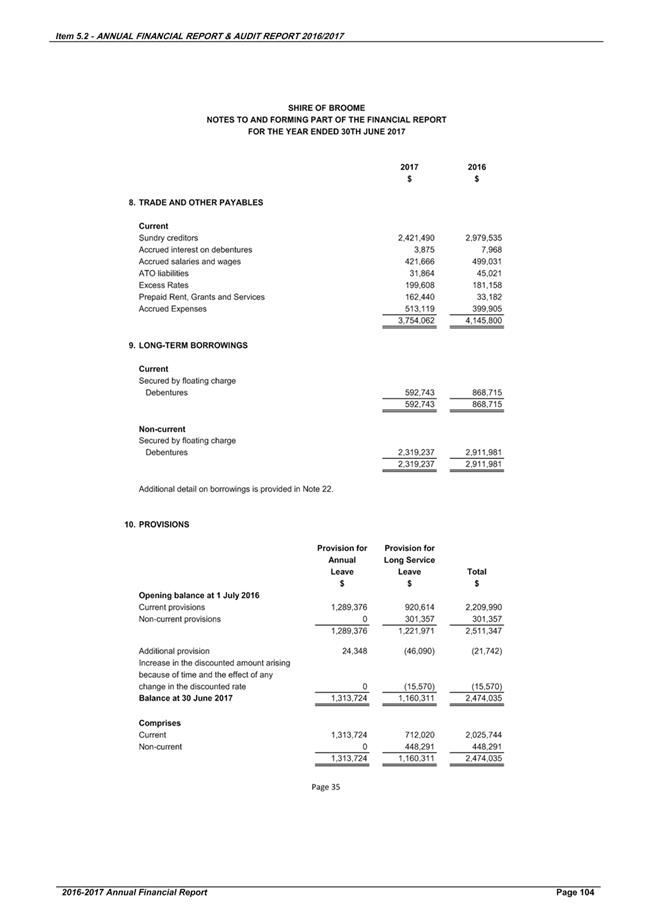

2. Audit Adjustments

Following the presentation of the

draft 2016/2017 Financial Report to the Auditor, there were no amendments

required to be actioned.

3. Other Matters

There were no identified matters of

fraud to report and there were no disagreements with management about

significant accounting matters.

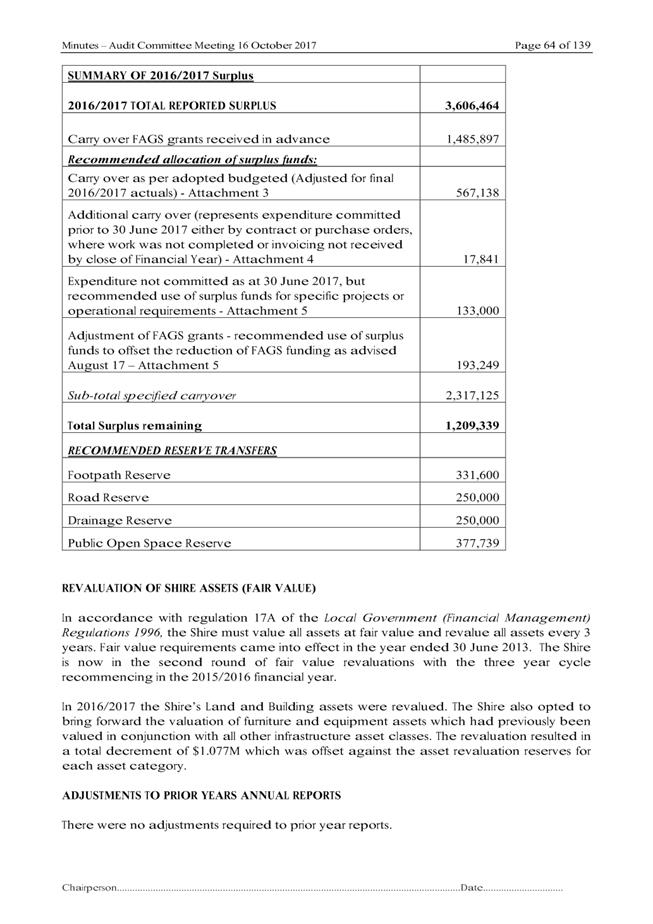

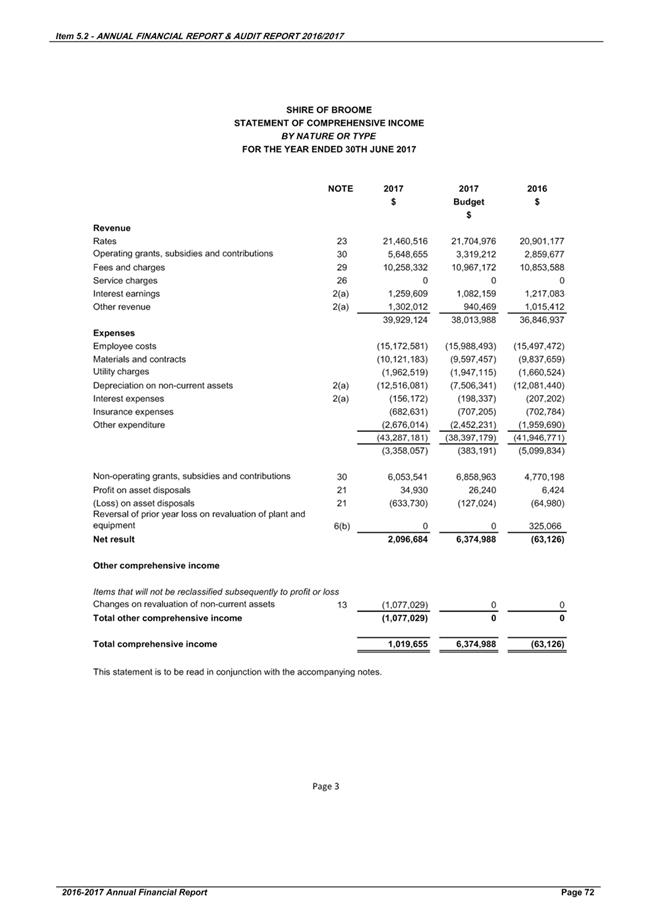

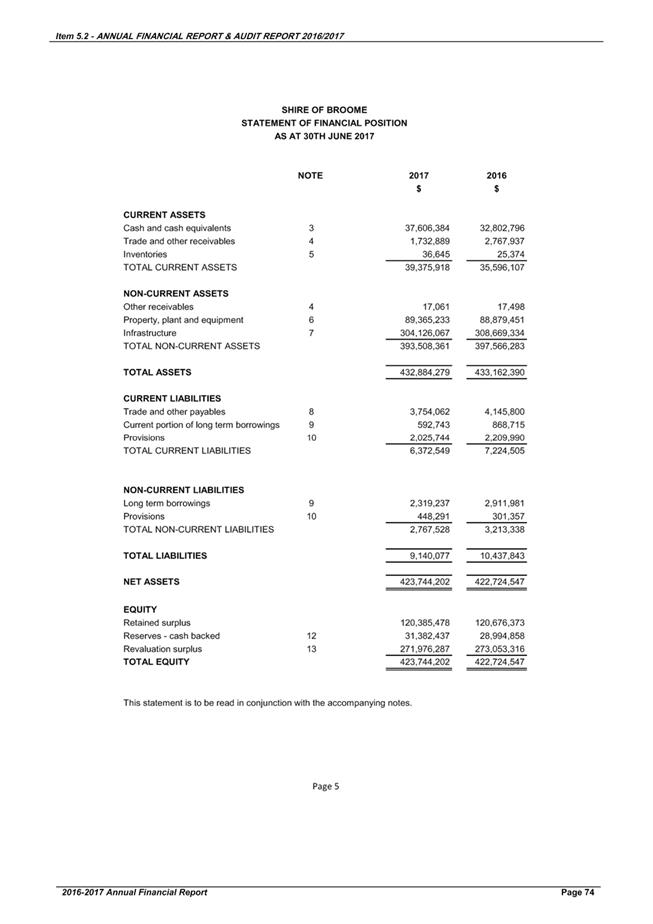

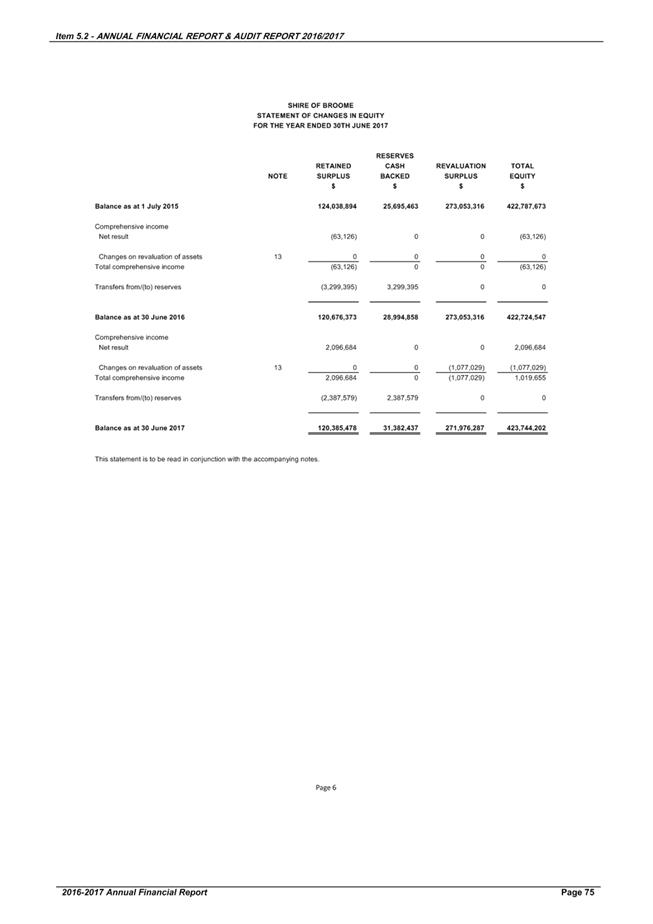

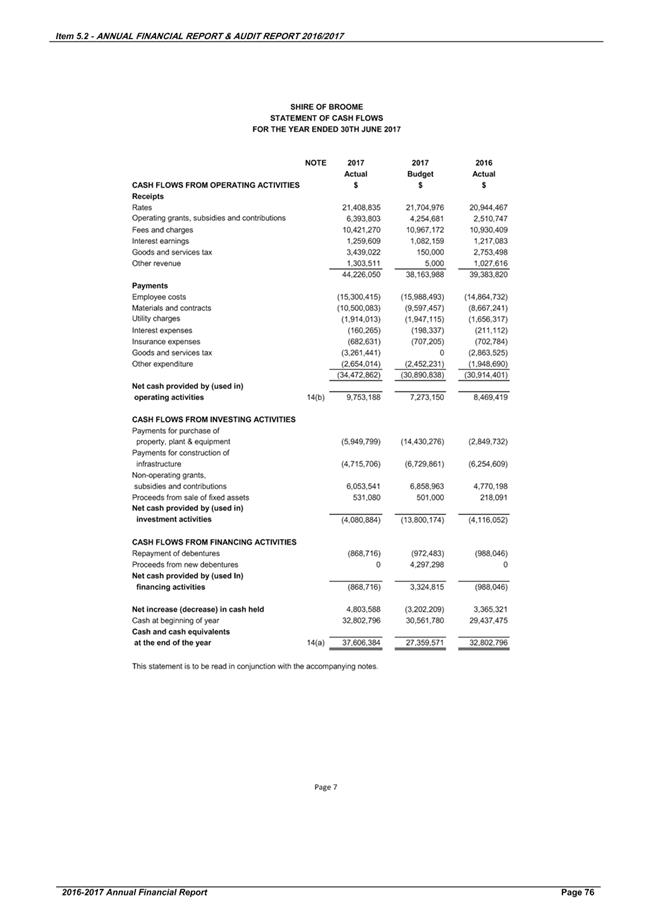

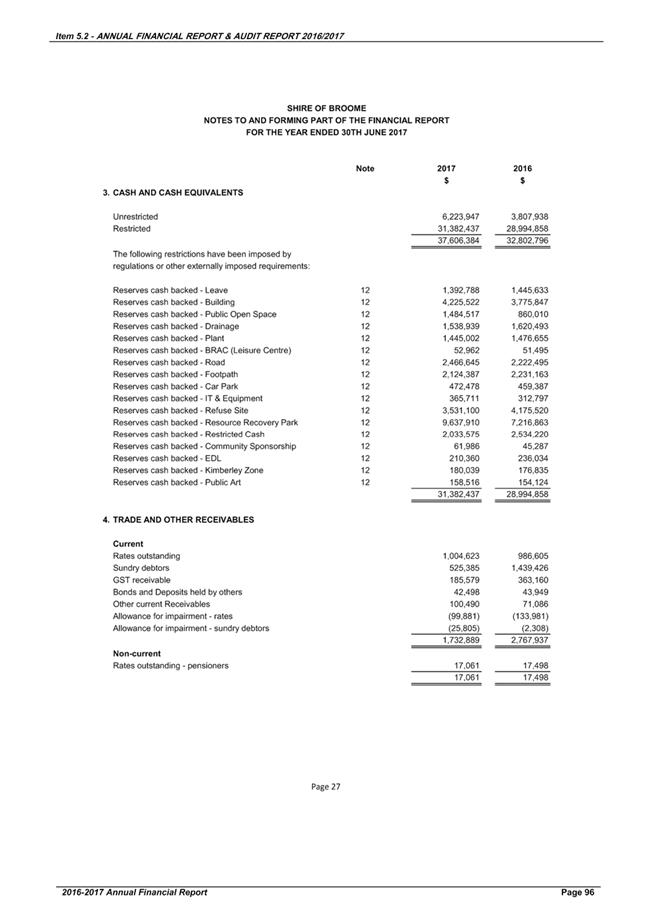

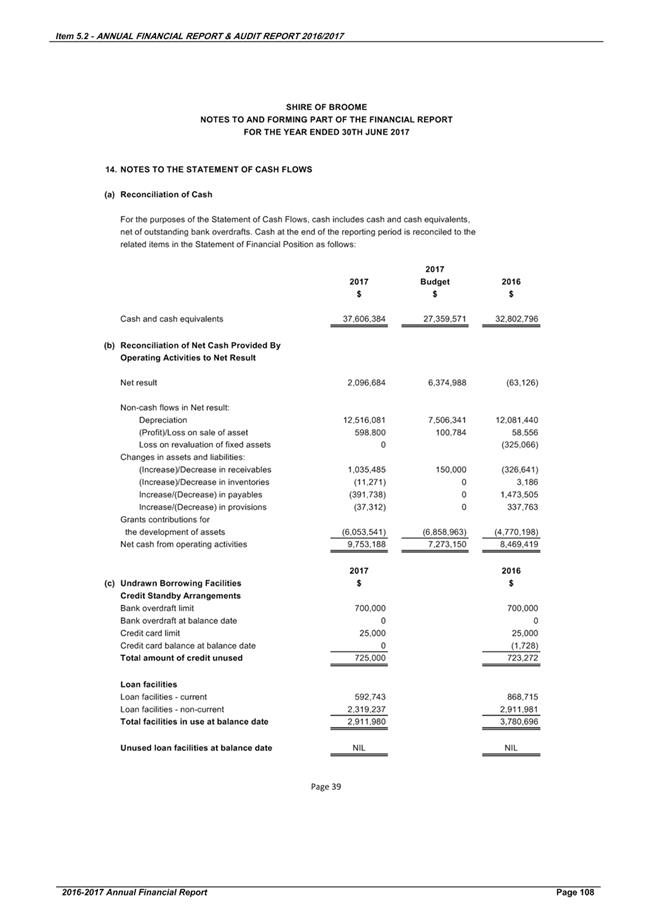

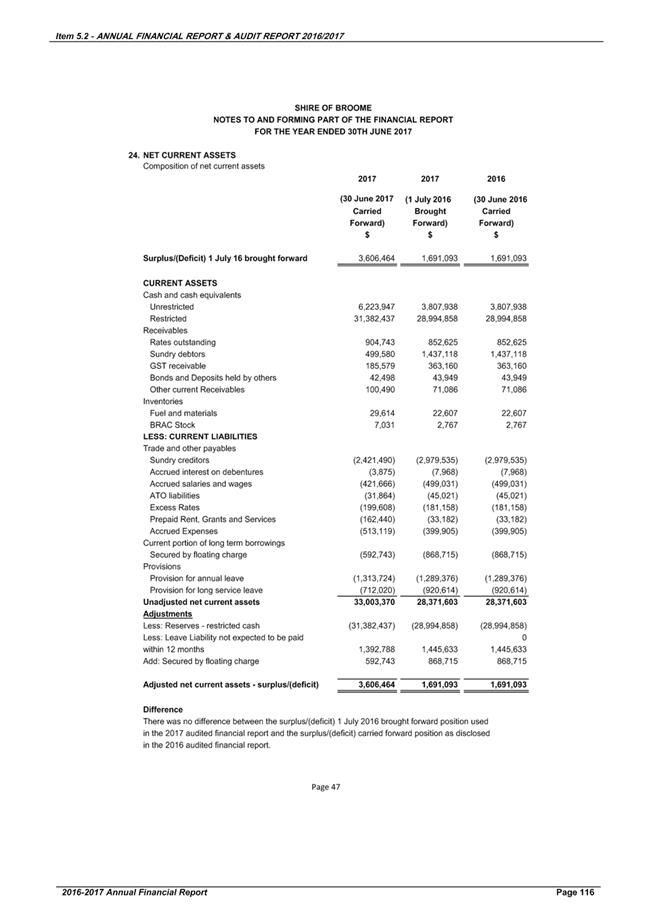

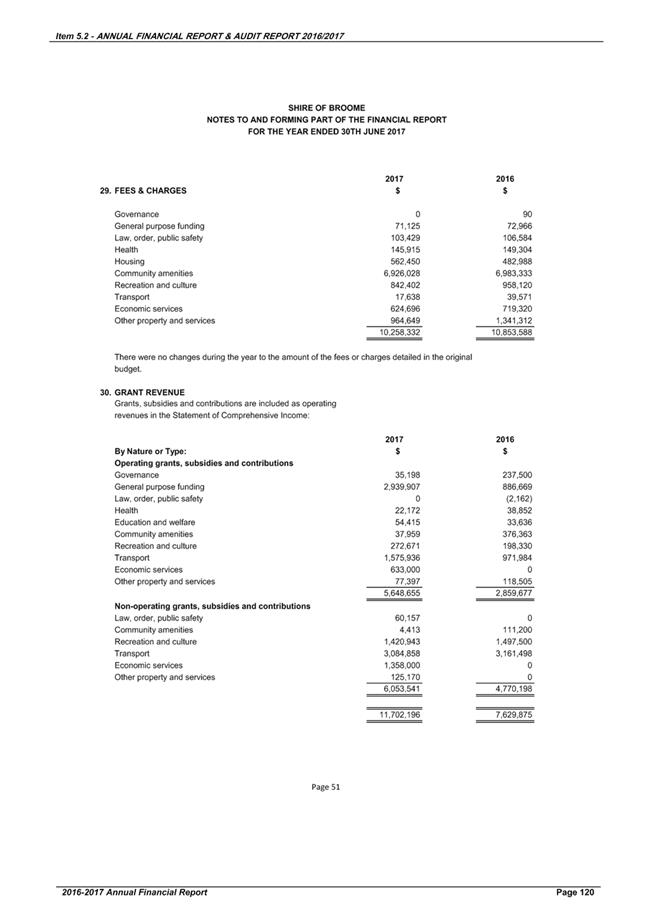

2016/2017 Operating Result

The financial year ended 30 June 2017

resulted in the following carried forward operating surplus:

$1,879,323 Budgeted

2016/2017 operating surplus (as per 2017/2018 adopted annual

budget)

$3,606,464

Actual 2016/2017 operating surplus

Note, this surplus is exclusive of

non-cash transactions such as depreciation and the effects of asset revaluation

gains or losses.

The 2017/2018 Annual Budget that was

adopted at the Ordinary Meeting of Council held 29 June 2017, adopted an

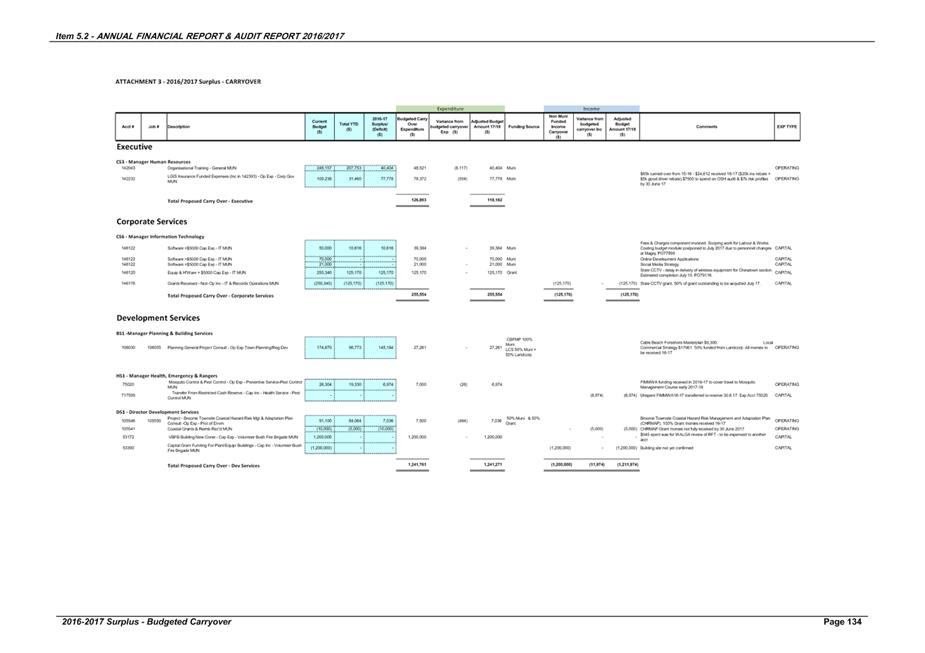

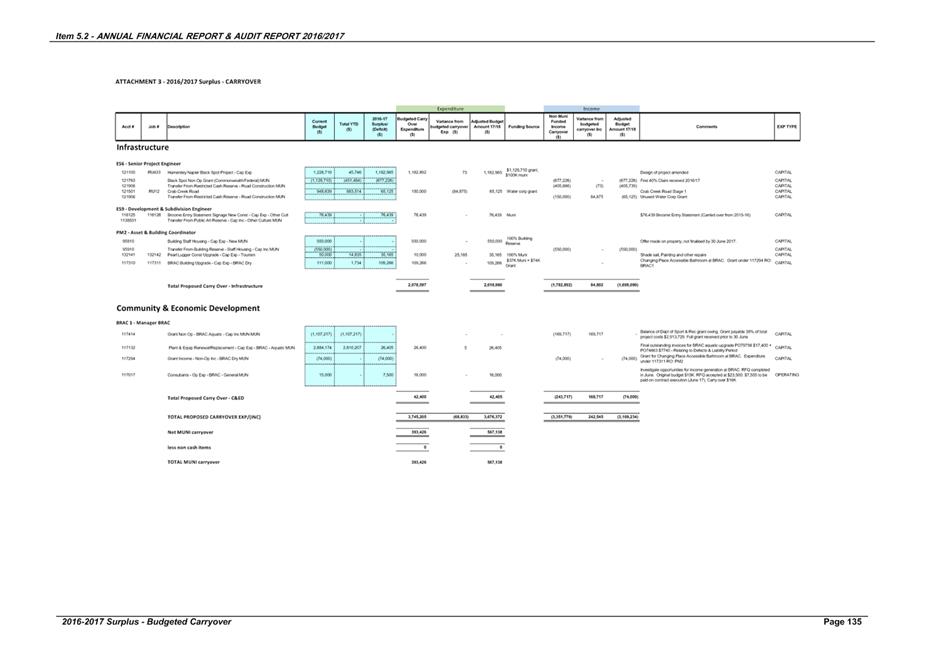

estimated brought forward operating surplus of $1,879,323 from 2016/2017. This

was comprised of $1,485,897 Financial Assistance Grants received in advance and

the balance of $393,426 comprising estimated surpluses from operating and

capital projects that were not completed prior to the close of the financial

year as detailed in Attachment 3 of item 5.2 of the Minutes of Audit Committee

meeting. The estimated budgeted surplus was calculated prior to the close of

financial year processing. The actual brought forward surplus for these

projects, as adjusted for final actual expenditure or income is $567,138.

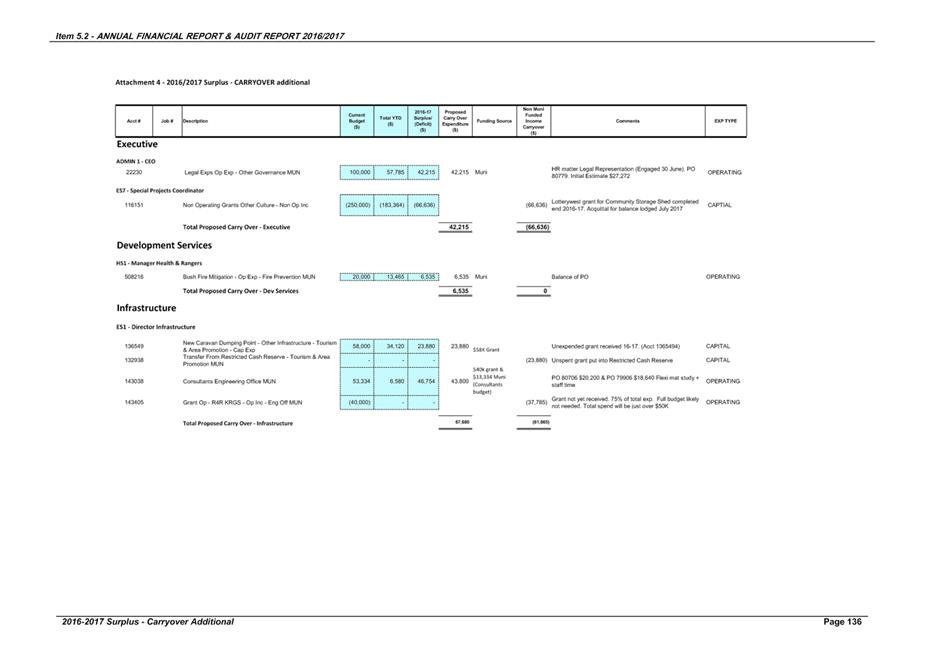

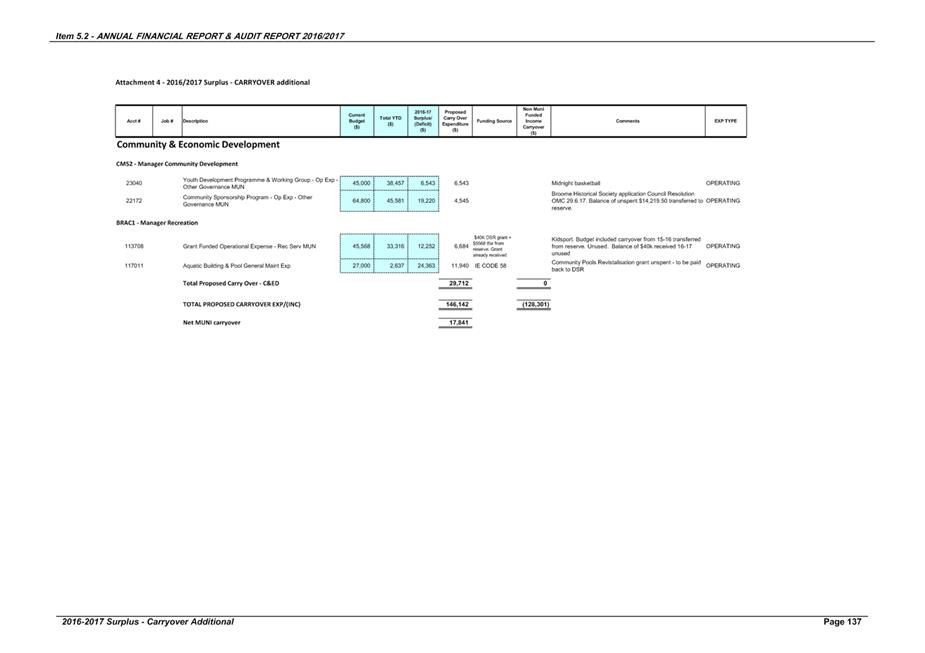

A further $17,841 of the carried

forward surplus pertains to operating activities or capital projects which were

not completed as expected, by 30 June 2017. The amounts represent expenditure

committed prior to 30 June 2017 either by executed contract or purchase orders,

where work was not completed or supplier invoices not received, by close of

financial year processing.

Other factors contributing to the

surplus include savings in salaries and wages and fringe benefits tax of $448K,

unspent materials and contracts across primarily operating activities/projects

of $1.6M, and savings of $30K in plant repairs, parts, fuel and tyres.

Additional interest revenue of $152K was earned in the period.

However, these savings were offset by

a number of target shortfalls in income. This included a reduction in expected

fees and charges income of $76K primarily due to the decline in building and

planning activities.

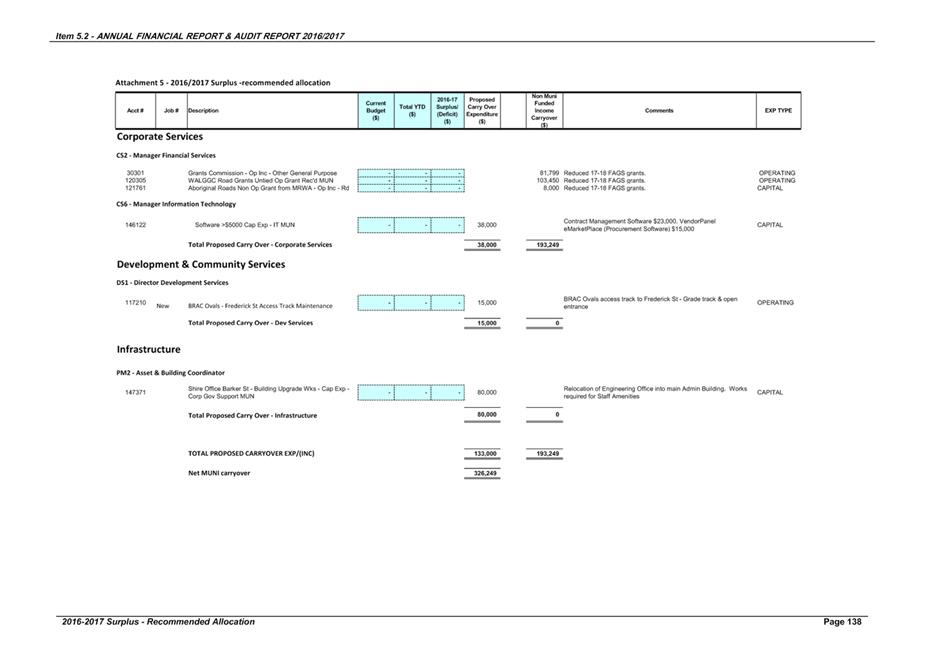

It is proposed that $133,000 of the

surplus funds be utilised for those operational activities including business

system improvements, minor building works required to the Administration

building to accommodate the relocation of the engineering department and to

improve access to the BRAC sporting grounds from Frederick St, consistent with

funds already committed for other upgrade projects in this precinct in the

2017/2018 budget.

It is proposed that $193,249 of the

surplus funds go towards funding the shortfall of Finance Assistance Grants for

2017/2018. On 17 August 2017, advice was received from the WA Local

Government Grants Commission, that the final 2017/2018 Financial Assistance

Grants allocation had been reduced from previous indications given in May/June

2017. The reduction has affected all Local Governments in WA and was a result

of new census data affecting the distribution of allocations to the States. The

final allocation was $193,249 less than what had been budgeted in the 2017/2018

Adopted Budget.

It is recommended that the balance of

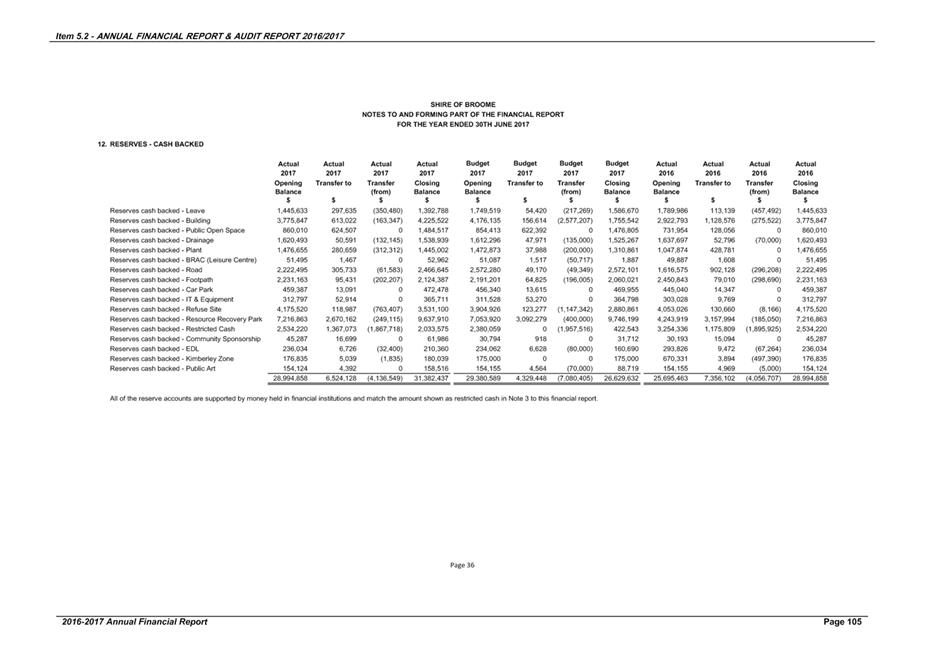

unallocated funds of $1.289M be transferred to reserves.

It is proposed that $331,600 be

transferred to the Footpath Reserve for the specific purpose of leveraging

grant funding from the Department of Transport for a shared path from Conti

Foreshore to Town Beach. The Shire has progressed an expression of interest to

a grant proposal stage and if successful, would receive matching grant funds

through the Western Australian Bicycle Network grants program.

It is proposed that $250K be

transferred to the Road Reserve and Drainage Reserve respectively for renewal,

and the balance of $377,739 be transferred to the Public Open Space reserve to

offset and reduce proposed borrowings required for the Town Beach Redevelopment

Project adopted in the 2017/2018 annual budget.

A summary of the recommended surplus

allocation is as follows:

|

SUMMARY OF 2016/2017 Surplus

|

|

|

2016/2017 TOTAL REPORTED SURPLUS

|

3,606,464

|

|

Carry over FAGS grants received in advance

|

1,485,897

|

|

Recommended allocation of surplus funds:

|

|

|

Carry over as per adopted budgeted (Adjusted for final

2016/2017 actuals) - Attachment 3 of item 5.2 of the Minutes of Audit

Committee meeting

|

567,138

|

|

Additional carry over (represents expenditure committed

prior to 30 June 2017 either by contract or purchase orders, where work was

not completed or invoicing not received by close of Financial Year) -

Attachment 4 of item 5.2 of the Minutes of Audit Committee meeting

|

17,841

|

|

Expenditure not committed as at 30 June 2017, but

recommended use of surplus funds for specific projects or operational

requirements - Attachment 5 of item 5.2 of the Minutes of Audit

Committee meeting

|

133,000

|

|

Adjustment of FAGS grants - recommended use of surplus

funds to offset the reduction of FAGS funding as advised August 17 –

Attachment 5 of item 5.2 of the Minutes of Audit Committee meeting

|

193,249

|

|

Sub-total specified carryover

|

2,317,125

|

|

Total Surplus remaining

|

1,209,339

|

|

RECOMMENDED RESERVE TRANSFERS

|

|

|

Footpath Reserve

|

331,600

|

|

Road Reserve

|

250,000

|

|

Drainage Reserve

|

250,000

|

|

Public Open Space Reserve

|

377,739

|

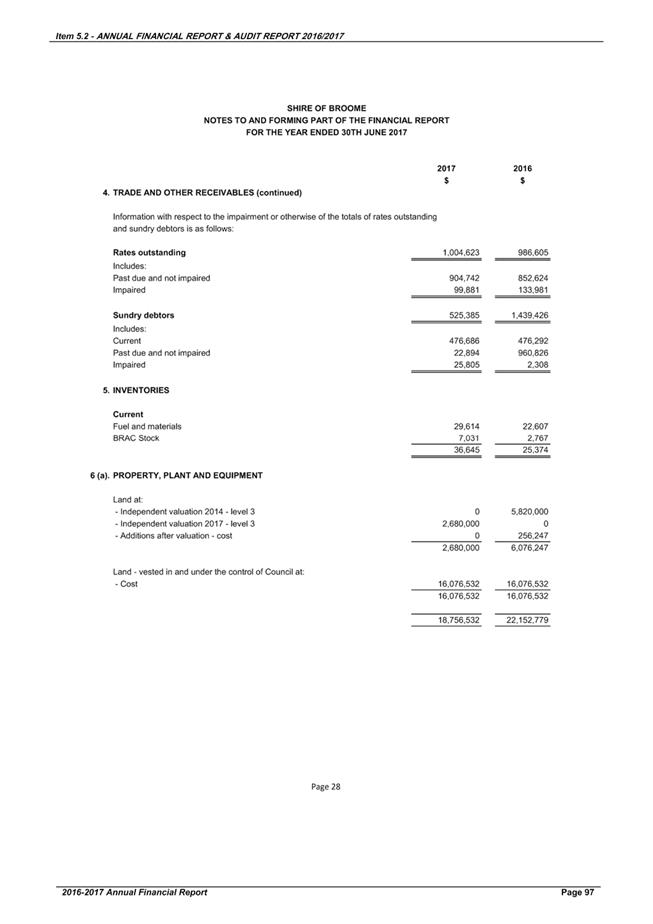

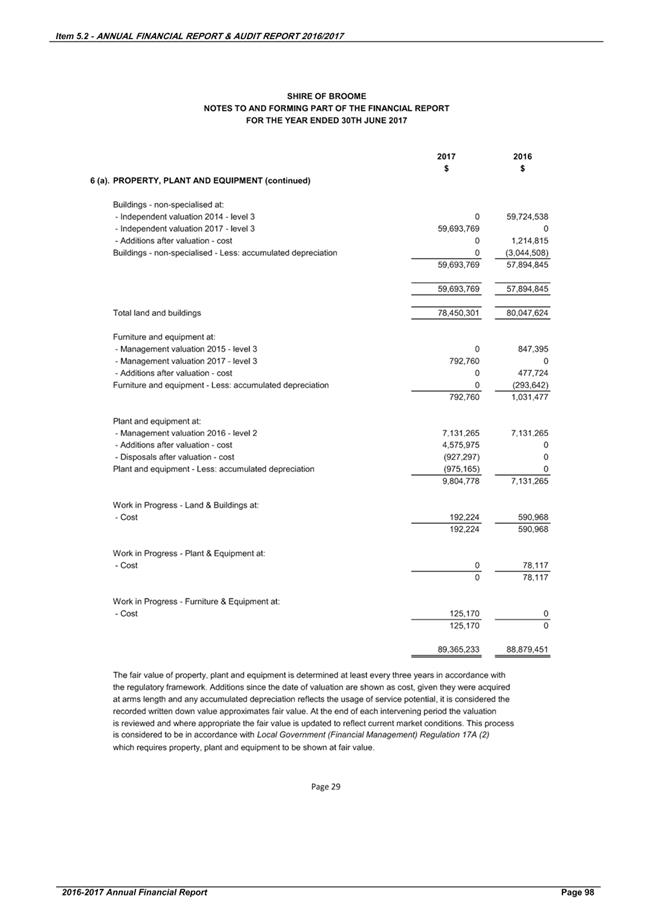

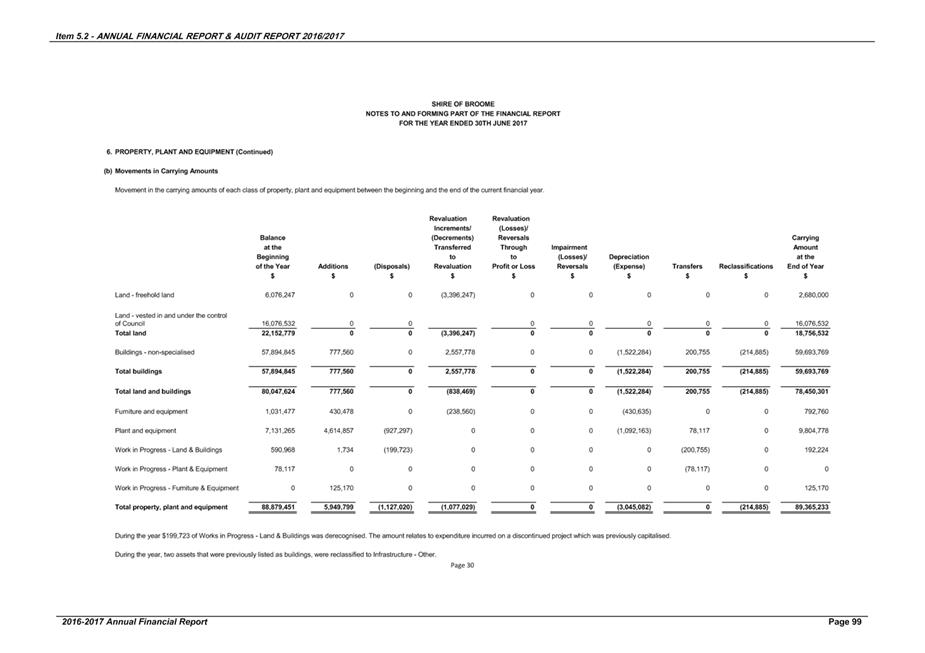

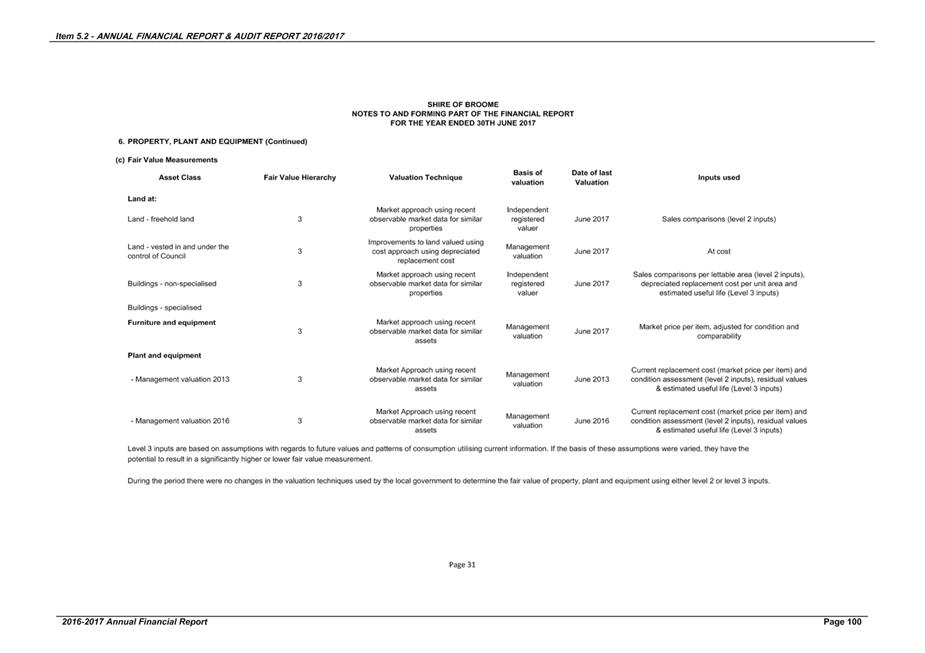

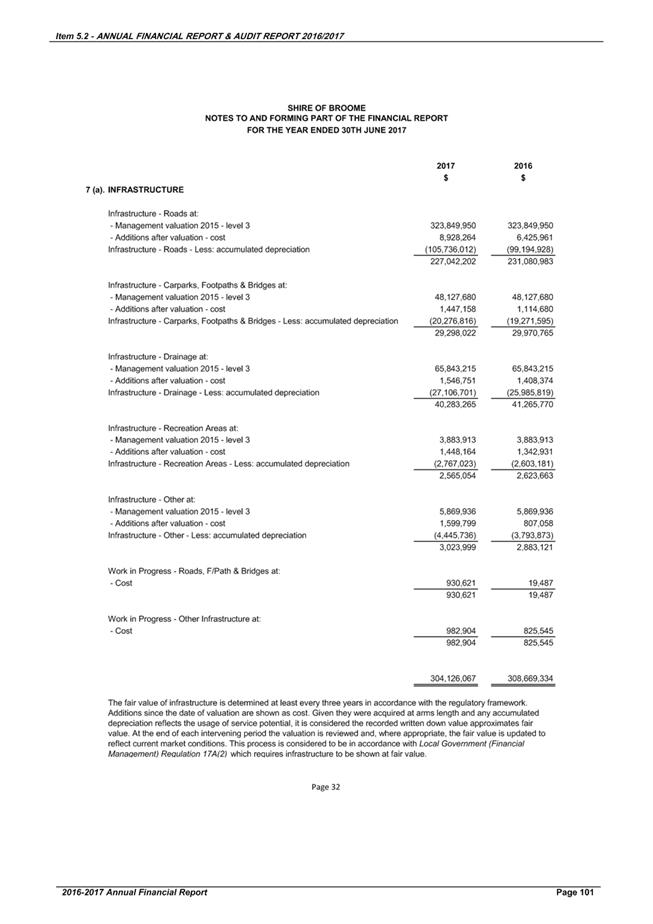

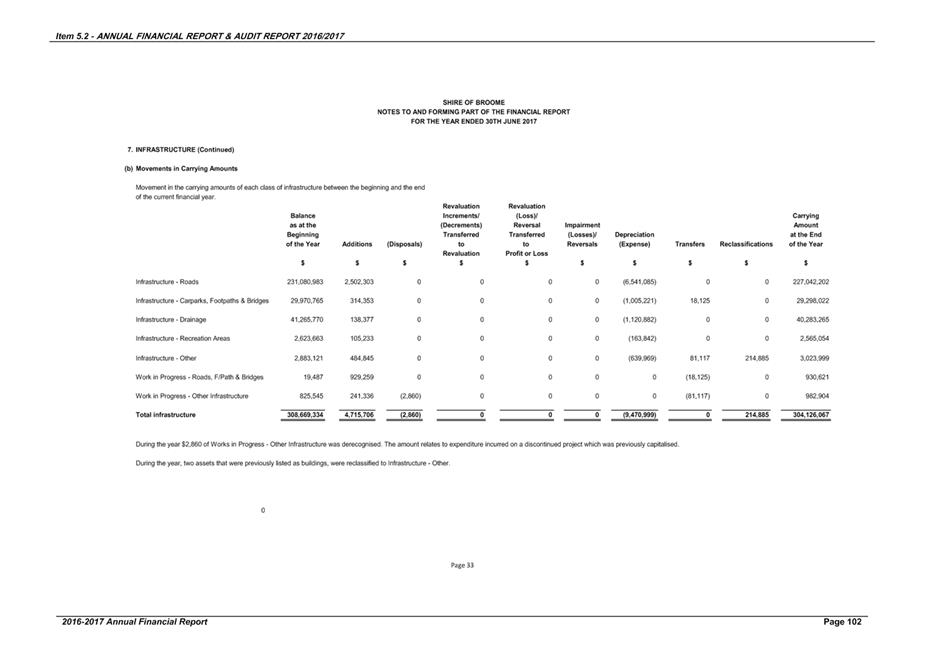

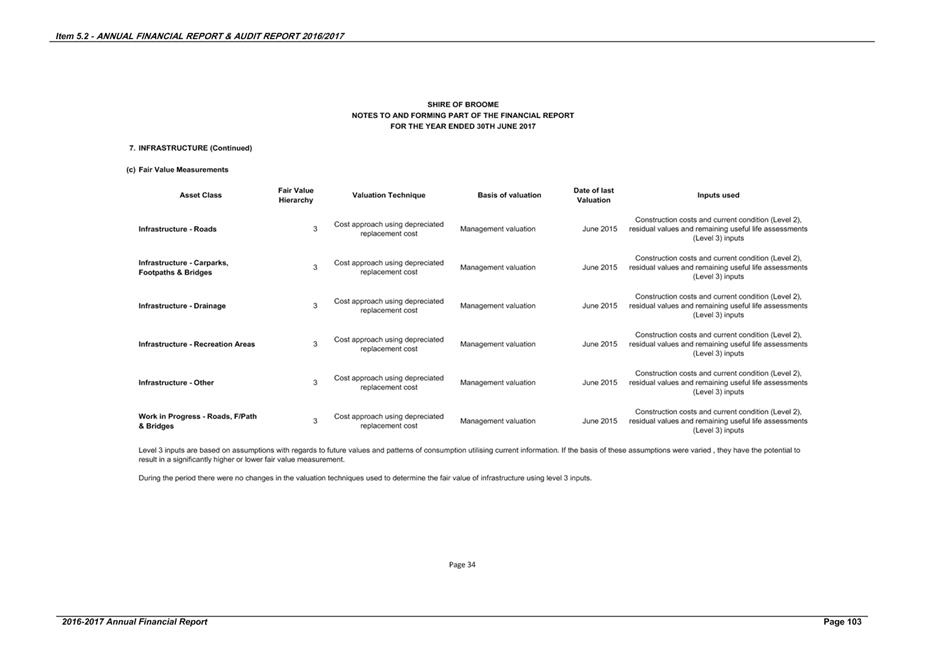

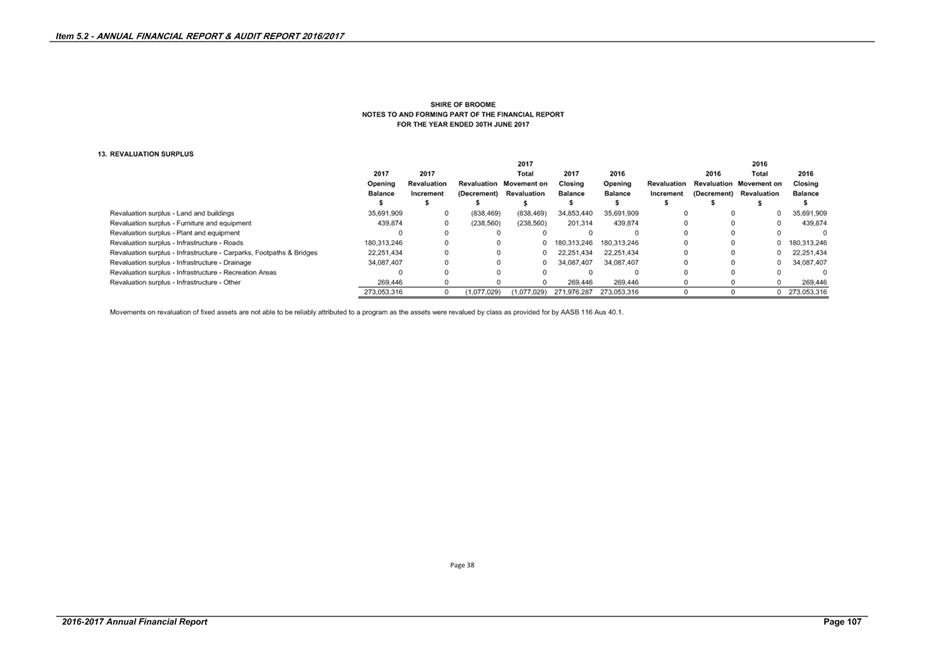

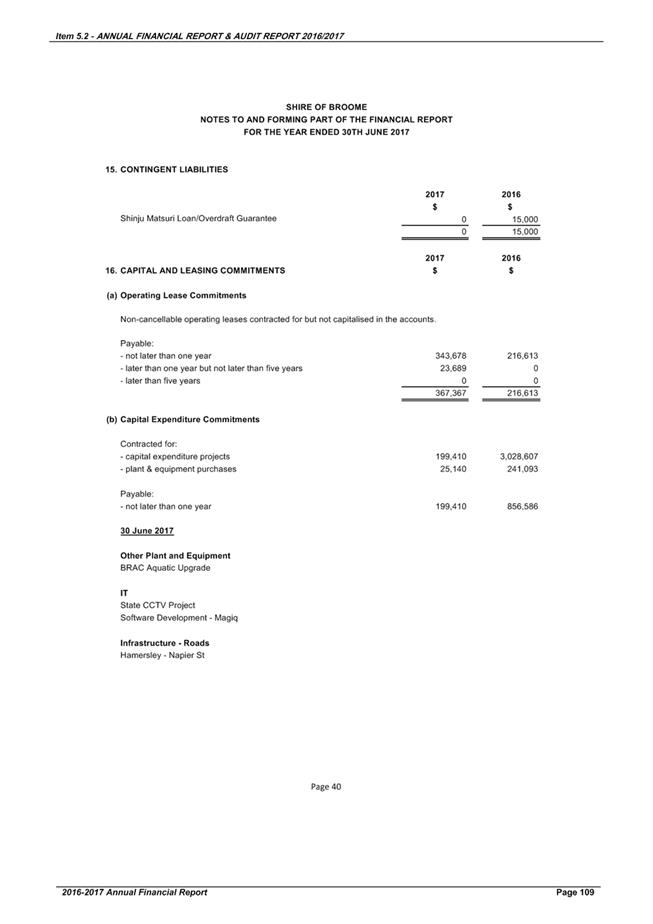

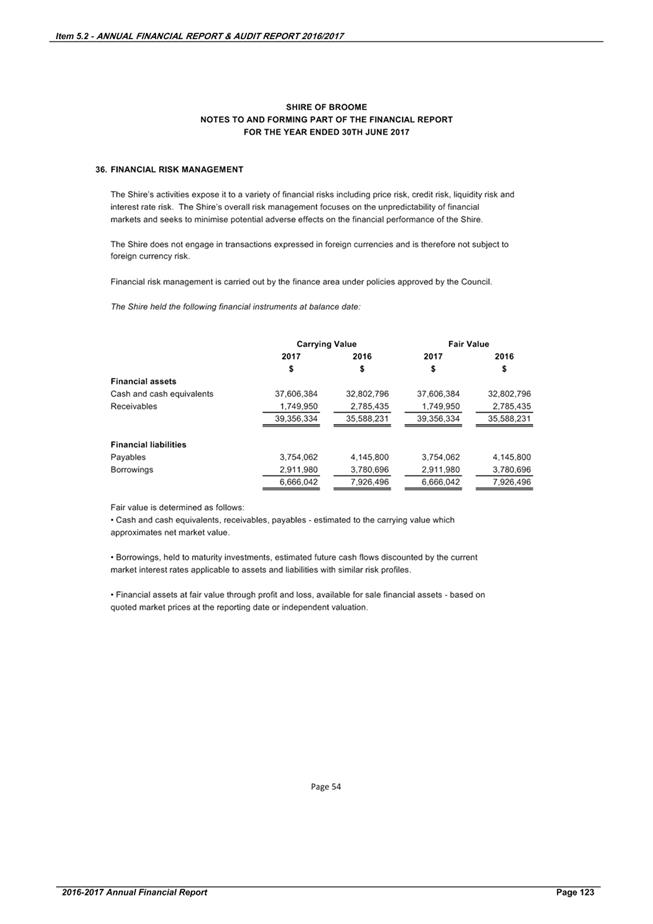

Revaluation of Shire Assets (Fair Value)

In accordance with regulation 17A of

the Local Government (Financial Management) Regulations 1996, the Shire

must value all assets at fair value and revalue all assets every 3 years. Fair

value requirements came into effect in the year ended 30 June 2013. The

Shire is now in the second round of fair value revaluations with the three-year

cycle recommencing in the 2015/2016 financial year.

In 2016/2017 the Shire’s Land

and Building assets were revalued. The Shire also opted to bring forward the

valuation of furniture and equipment assets which had previously been valued in

conjunction with all other infrastructure asset classes. The revaluation

resulted in a total decrement of $1.077M which was offset against the asset

revaluation reserves for each asset category.

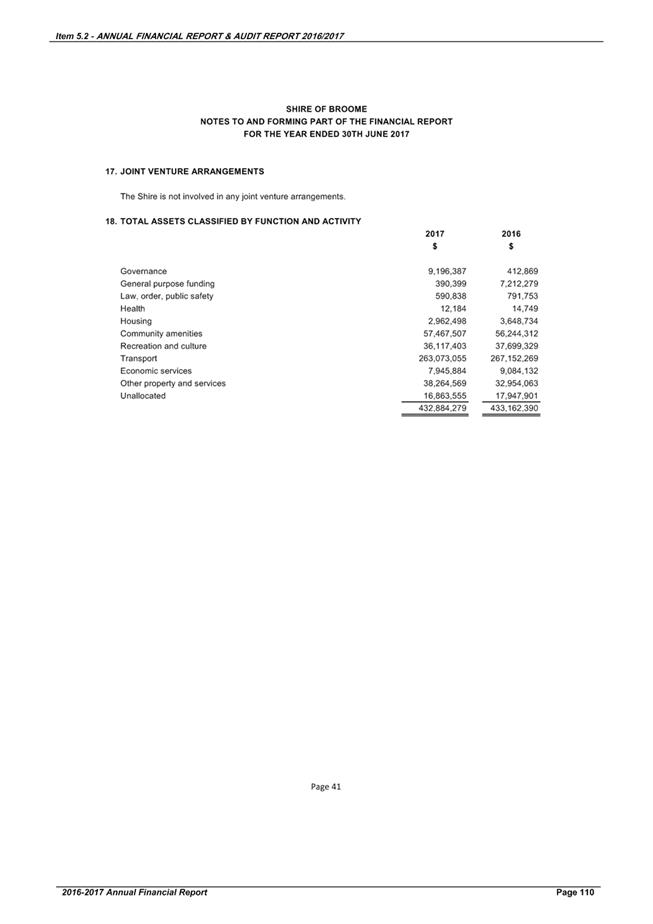

ADJUSTMENTS TO PRIOR YEARS ANNUAL

REPORTS

There were no adjustments required to

prior year reports.

CONSULTATION

Department of Local Government and

Communities

STATUTORY ENVIRONMENT

Department of Local Government and

Communities Better Practice Review Program

Nil.

Annual Financial Report &

Audit Report 2016/2017

Local

Government Act 1995

6.4. Financial

report

(1) A

local government is to prepare an annual financial report for the preceding

financial year and such other financial reports as are prescribed.

(2) The

financial report is to —

(a) be

prepared and presented in the manner and form prescribed; and

(b) contain

the prescribed information.

(3) By

30 September following each financial year or such extended time as the

Minister allows, a local government is to submit to its

auditor —

(a) the

accounts of the local government, balanced up to the last day of the preceding

financial year; and

(b) the

annual financial report of the local government for the preceding financial

year.

7.9. Audit

to be conducted

(1) An

auditor is required to examine the accounts and annual financial report

submitted for audit and, by the 31 December next following the financial

year to which the accounts and report relate or such later date as may be

prescribed, to prepare a report thereon and forward a copy of that report

to —

(a) the

mayor or president; and

(b) the

CEO of the local government; and

(c) the

Minister.

(2) Without

limiting the generality of subsection (1), where the auditor considers

that —

(a) there

is any error or deficiency in an account or financial report submitted for

audit; or

(b) any

money paid from, or due to, any fund or account of a local government has been

or may have been misapplied to purposes not authorised by law; or

(c) there

is a matter arising from the examination of the accounts and annual financial

report that needs to be addressed by the local government, details of that

error, deficiency, misapplication or matter, are to be included in the report

by the auditor.

(3) The

Minister may direct the auditor of a local government to examine a particular

aspect of the accounts and the annual financial report submitted for audit by

that local government and to —

(a) prepare

a report thereon; and

(b) forward

a copy of that report to the Minister,

and

that direction has effect according to its terms.

(4) If

the Minister considers it appropriate to do so, the Minister is to forward a

copy of the report referred to in subsection (3), or part of that report,

to the CEO of the local government to be dealt with under section 7.12A.

7.12A. Duties

of local government with respect to audits

(1) A

local government is to do everything in its power to —

(a) assist

the auditor of the local government to conduct an audit and carry out his or

her other duties under this Act in respect of the local government; and

(b) ensure

that audits are conducted successfully and expeditiously.

(2) Without

limiting the generality of subsection (1), a local government is to meet

with the auditor of the local government at least once in every year.

(3) A

local government is to examine the report of the auditor prepared under

section 7.9(1), and any report prepared under section 7.9(3)

forwarded to it, and is to —

(a) determine

if any matters raised by the report, or reports, require action to be taken by

the local government; and

(b) ensure

that appropriate action is taken in respect of those matters.

(4) A

local government is to —

(a) prepare

a report on any actions under subsection (3) in respect of an audit

conducted in respect of a financial year; and

(b) forward

a copy of that report to the Minister, by the end of the next financial year,

or 6 months after the last report prepared under section 7.9 is

received by the local government, whichever is the latest in time.

5.54. Acceptance

of annual reports

(1) Subject

to subsection (2), the annual report for a financial year is to be

accepted* by the local government no later than 31 December after that

financial year.

* Absolute majority required.

(2) If

the auditor’s report is not available in time for the annual report for a

financial year to be accepted by 31 December after that financial year,

the annual report is to be accepted by the local government no later than 2

months after the auditor’s report becomes available.

Local Government (Audit) Regulations

1996

10. Report

by auditor

(4)

Where it is considered by the

auditor to be appropriate to do so, the auditor is to prepare a management

report to accompany the auditor’s report and to forward a copy of the

management report to the persons specified in section 7.9(1) with the

auditor’s report.

Local Government (Financial

Management) Regulations 1996

17A Assets,

valuation of for financial reports etc.

(1) In

this regulation —

fair value,

in relation to an asset, means the fair value of the asset measured in

accordance with the AAS.

(2) Subject

to subregulation (3), the value of an asset shown in a local

government’s financial reports must be the fair value of the asset.

(3) A

local government must show in each financial report —

(a) for

the financial year ending on 30 June 2013, the fair value of all of

the assets of the local government that are plant and equipment; and

(b) for

the financial year ending on 30 June 2014, the fair value of all of

the assets of the local government —

(i) that

are plant and equipment; and

(ii) that

are —

(I) land

and buildings; or

(II) infrastructure;

and

(c) for

a financial year ending on or after 30 June 2015, the fair value of

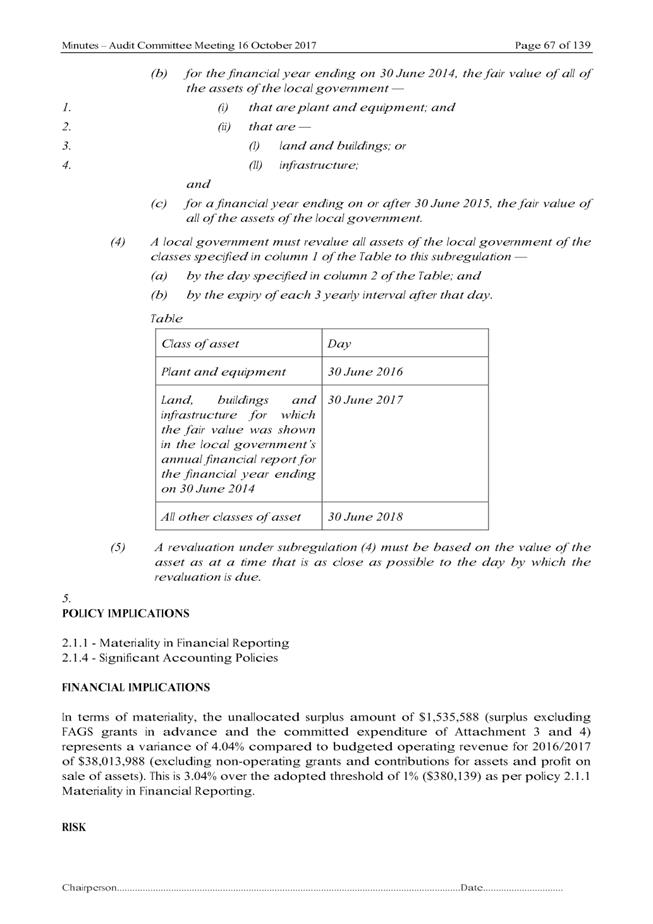

all of the assets of the local government.

(4) A

local government must revalue all assets of the local government of the classes

specified in column 1 of the Table to this subregulation —

(a) by

the day specified in column 2 of the Table; and

(b) by

the expiry of each 3 yearly interval after that day.

Table

|

Class of asset

|

Day

|

|

Plant and equipment

|

30 June 2016

|

|

Land, buildings and infrastructure for which the fair

value was shown in the local government’s annual financial report for

the financial year ending on 30 June 2014

|

30 June 2017

|

|

All other classes of asset

|

30 June 2018

|

(5) A

revaluation under subregulation (4) must be based on the value of the

asset as at a time that is as close as possible to the day by which the

revaluation is due.

POLICY IMPLICATIONS

2.1.1 - Materiality in Financial

Reporting

2.1.4 - Significant Accounting

Policies

FINANCIAL IMPLICATIONS

In terms of materiality, the

unallocated surplus amount of $1,535,588 (surplus excluding FAGS grants in

advance and committed expenditure) represents a variance of 4.04% compared to

budgeted operating revenue for 2016/2017 of $38,013,988 (excluding

non-operating grants and contributions for assets and profit on sale of

assets). This is 3.04% over the adopted threshold of 1% ($380,139) as per

Policy 2.1.1 Materiality in Financial Reporting.

RISK

The audited Annual Financial Report

is a key control measure used to report to Council and its stakeholders to

provide assurance that all systems, processes and controls have been

established by the CEO to minimise the risk of any material misstatement or

loss caused by fraud or error. The audit findings indicate areas requiring

improvement and management have implemented measures to review processes. The

report measures Council’s financial capacity to achieve its adopted

strategic and operational objectives. A material variance indicates areas

requiring investigation such as budget estimation/formulation, workforce

management and Council’s overall resource capacity to achieve its

strategic objectives.

Should this not be adopted by

Council, the adoption of the 2016/2017 Annual Report to be presented at the

October Ordinary Meeting of Council and Council’s ability to schedule the

Annual Electors Meeting (AEM) in December as planned could be impacted. This

poses a high risk due to the possible likelihood of occurring and the impact of

a significant delay to major deliverables.

In regards to the proposed allocation

of the 2016/2017 surplus, should the Council make alternative recommendations,

the long term financial impacts of such should be analysed to ensure there are

no adverse impacts to Council’s future financial sustainability and

should be in line with the LTFP. In line with Council’s risk ratings, the

risk is assessed as extreme where the financial impact is greater than $150,000

and the likelihood of this occurring is possible. To mitigate these risks, the

report recommendations are required to be adopted.

STRATEGIC

IMPLICATIONS

Our People Goal – Foster a

community environment that is accessible, affordable, inclusive, healthy and safe:

Encourage communication.

Identify affordable services and

initiatives to satisfy community needs.

Our Prosperity Goal – Create

the means to enable local jobs creation and lifestyle affordability for the

current and future population:

Encourage the provision of affordable

land for residential, industrial, commercial and community use.

Our Organisation Goal –

Continually enhance the Shire’s organisational capacity to service the

needs or a growing community:

Develop an organisational culture

that strives for service excellence.

Review and analyse strategic and

operational plans.

Manage resource allocation.

Manage staff attraction and

retention.

Improve systems, processes and

compliance.

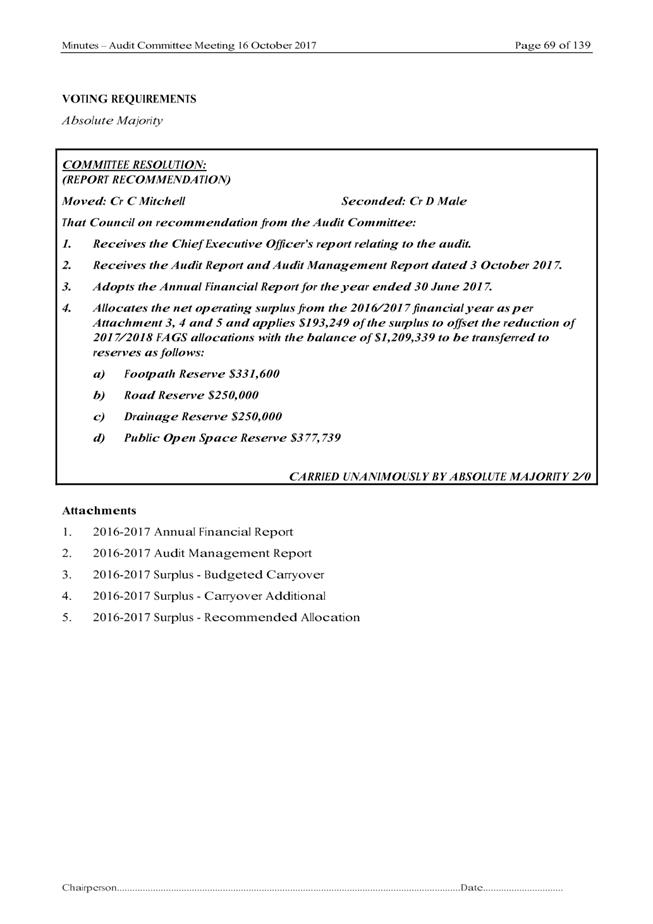

VOTING REQUIREMENTS

Simple Majority

|

COMMITTEE RECOMMENDATION 1:

That Council on recommendation from the Audit

Committee:

1. Receives the

Better Practice Review Report from the Department of Local Government and

Communities;

2. Notes the

identified areas where the Shire of Broome operates at a ‘better practice’

level; and

3. Requests that

the Chief Executive Officer review the actions plan provided and present an

updated action plan to Council via the Audit Committee.

|

|

VOTING REQUIREMENTS

Absolute Majority

|

|

COMMITTEE RECOMMENDATION 2:

That Council on recommendation from the Audit

Committee:

1. Receives

the Chief Executive Officer’s report relating to the audit.

2. Receives the

Audit Report and Audit Management Report dated 3 October 2017.

3. Adopts

the Annual Financial Report for the year ended 30 June 2017.

4. Allocates

the net operating surplus from the 2016/2017 financial year as per Attachment

3, 4 and 5 of item 5.2 of the

Minutes of Audit Committee meeting and applies $193,249 of the surplus

to offset the reduction of 2017/2018 FAGS allocations with the balance of

$1,209,339 to be transferred to reserves as follows:

a) Footpath

Reserve $331,600

b) Road

Reserve $250,000

c) Drainage

Reserve $250,000

d) Public

Open Space Reserve $377,739

(Absolute Majority Required)

|

Attachments

|

1.

|

Minutes of Audit

Committee Meeting held 16 October 2017

|