VISION OF COUNCIL

"A thriving and friendly community

that recognises our history and embraces cultural diversity and economic

opportunity, whilst nurturing our unique natural and built environment."

AGENDA

FOR THE

Audit and Risk Committee

Meeting

12 February 2019

"A

thriving and friendly community that recognises our history and embraces

cultural diversity and economic opportunity, whilst nurturing our unique

natural and built environment."

OUR MISSION

“To

deliver affordable and quality Local Government services.”

CORE

VALUES OF THE SHIRE

The core

values that underpin the achievement of the

mission

will be based on a strong customer service

focus and a

positive attitude:

Communication

Integrity

Respect

Innovation

Transparency

Courtesy

DISCLAIMER

The purpose of Council Meetings is to discuss, and where possible,

make resolutions about items appearing on the agenda. Whilst Council has

the power to resolve such items and may in fact, appear to have done so at the

meeting, no person should rely on or act on the basis of such decision or on

any advice or information provided by a Member or Officer, or on the content of

any discussion occurring, during the course of the meeting.

Persons should be aware that the provisions of the Local

Government Act 1995 (Section 5.25 (e)) establish procedures for revocation or

rescission of a Council decision. No person should rely on the decisions

made by Council until formal advice of the Council decision is received by that

person. The Shire of Broome expressly disclaims liability for any loss or

damage suffered by any person as a result of relying on or acting on the basis

of any resolution of Council, or any advice or information provided by a Member

or Officer, or the content of any discussion occurring, during the course of

the Council meeting.

Should you

require this document in an alternative format please contact us.

Agenda – Audit and

Risk Committee Meeting 12 February 2019 Page 1 of 4

NOTICE OF MEETING

Dear Committee Member,

The next Audit and Risk Committee of

the Shire of Broome will be held on Tuesday, 12 February 2019 in the Committee

Room, Corner Weld and Haas Streets, Broome, commencing at 3.00pm.

Regards

S MASTROLEMBO

Chief Executive Officer

08/02/2019

Agenda – Audit and

Risk Committee Meeting 12 February 2019 Page 1 of 4

|

Recommendation:

That the Minutes of the

Audit and Risk Committee held on 13 November 2018, as published and

circulated, be confirmed as a true and accurate record of that meeting.

|

Agenda – Audit and

Risk Committee Meeting 12 February 2019 Page 1 of 4

|

5.1 COMPLIANCE

AUDIT RETURN 2018

LOCATION/ADDRESS: Nil

APPLICANT: Nil

FILE: LCR02

AUTHOR: Manager

Governance

CONTRIBUTOR/S: Nil

RESPONSIBLE

OFFICER: Director

Corporate Services

DISCLOSURE

OF INTEREST: Nil

DATE OF REPORT: 1

February 2019

|

|

SUMMARY: The

purpose of this report is to present to the Audit and Risk Committee the 2018

Compliance Audit Return for review, and for a recommendation to Council to

adopt the 2018 Compliance Audit Return for submission to the Department of

Local Government, Sport and Cultural Industries (DLGSC) by 31 March 2019.

|

BACKGROUND

Previous

Considerations

OMC 23 March 2004 Item

9.1.3

OMC 22 March 2005 Item

9.1.2

OMC 11 April 2006 Item

9.1.4

OMC 15 March 2007 Item

10.4

OMC 13 March 2008 Item

10.1

OMC 24 March 2009 Item

10.3

OMC 18 March 2010 Item

10.1

OMC 17 March 2011 Item

10.2

OMC 15 March 2012 Item

9.4.2

OMC 21 March 2013 Item

10.2

OMC 27 February 2014 Item

10.4

OMC 26 February 2015 Item

10.1

OMC 25 February 2016 Item

10.3

OMC 23 February 2017 Item

10.3

OMC 22 February 2018 Item

10.4

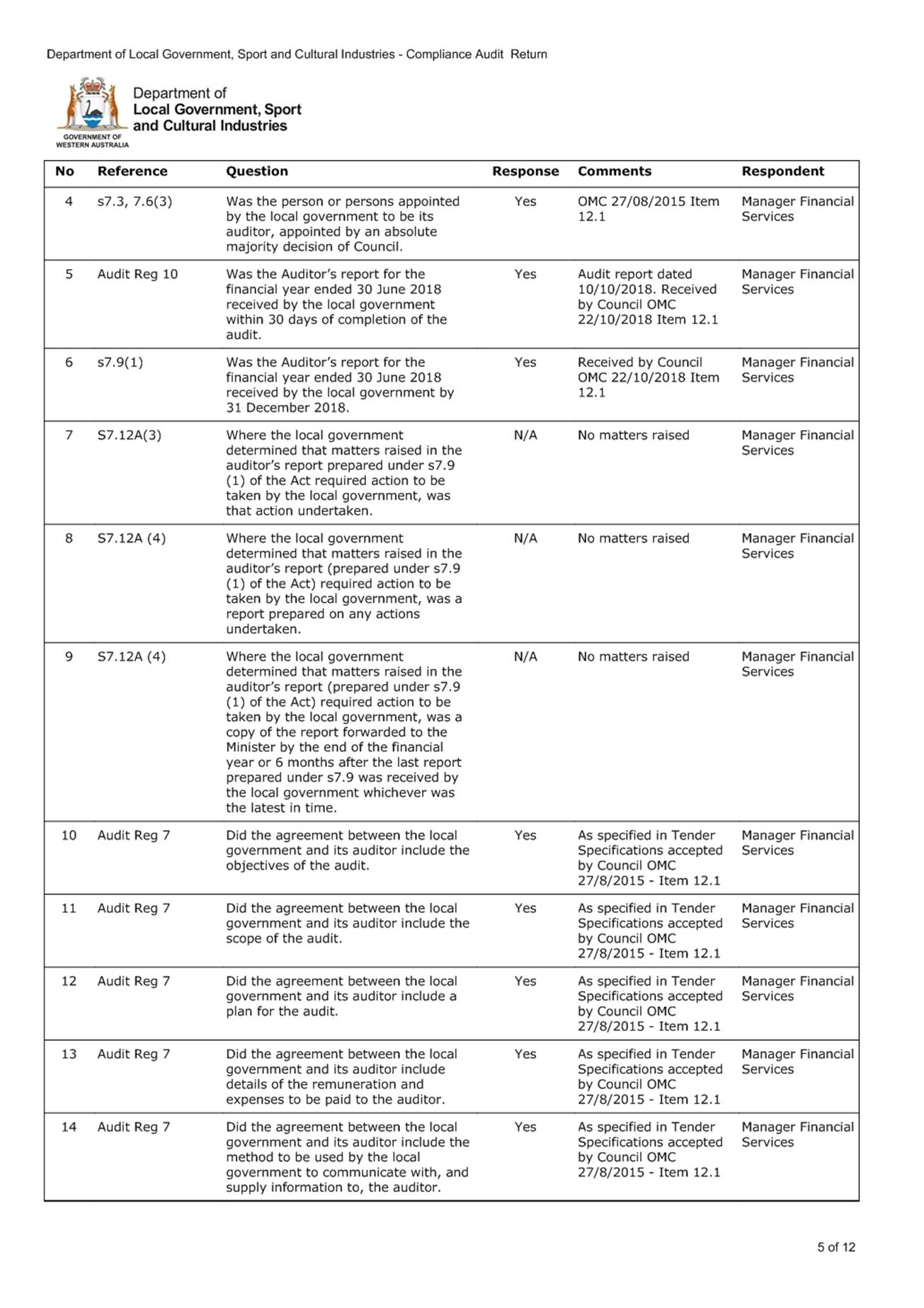

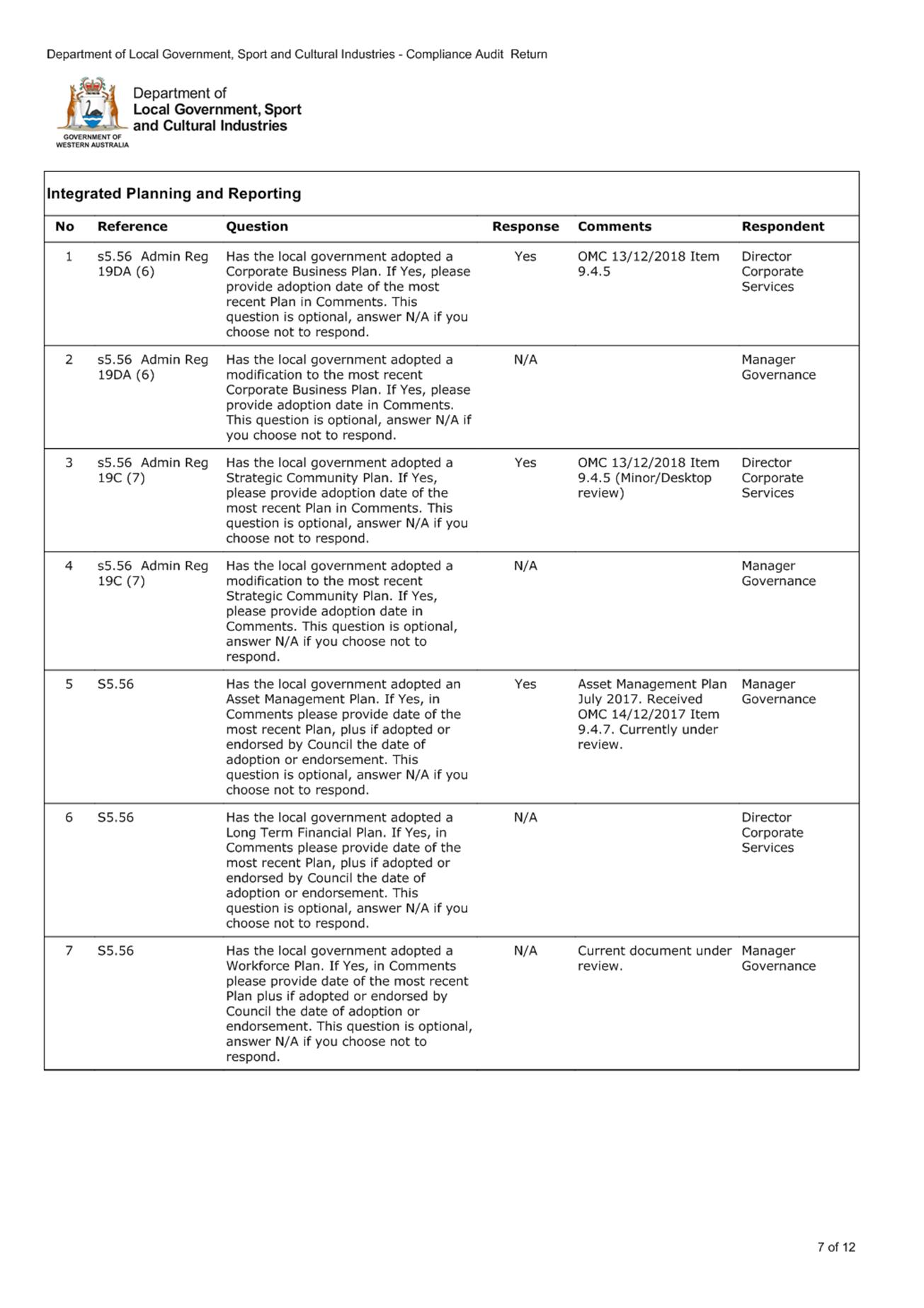

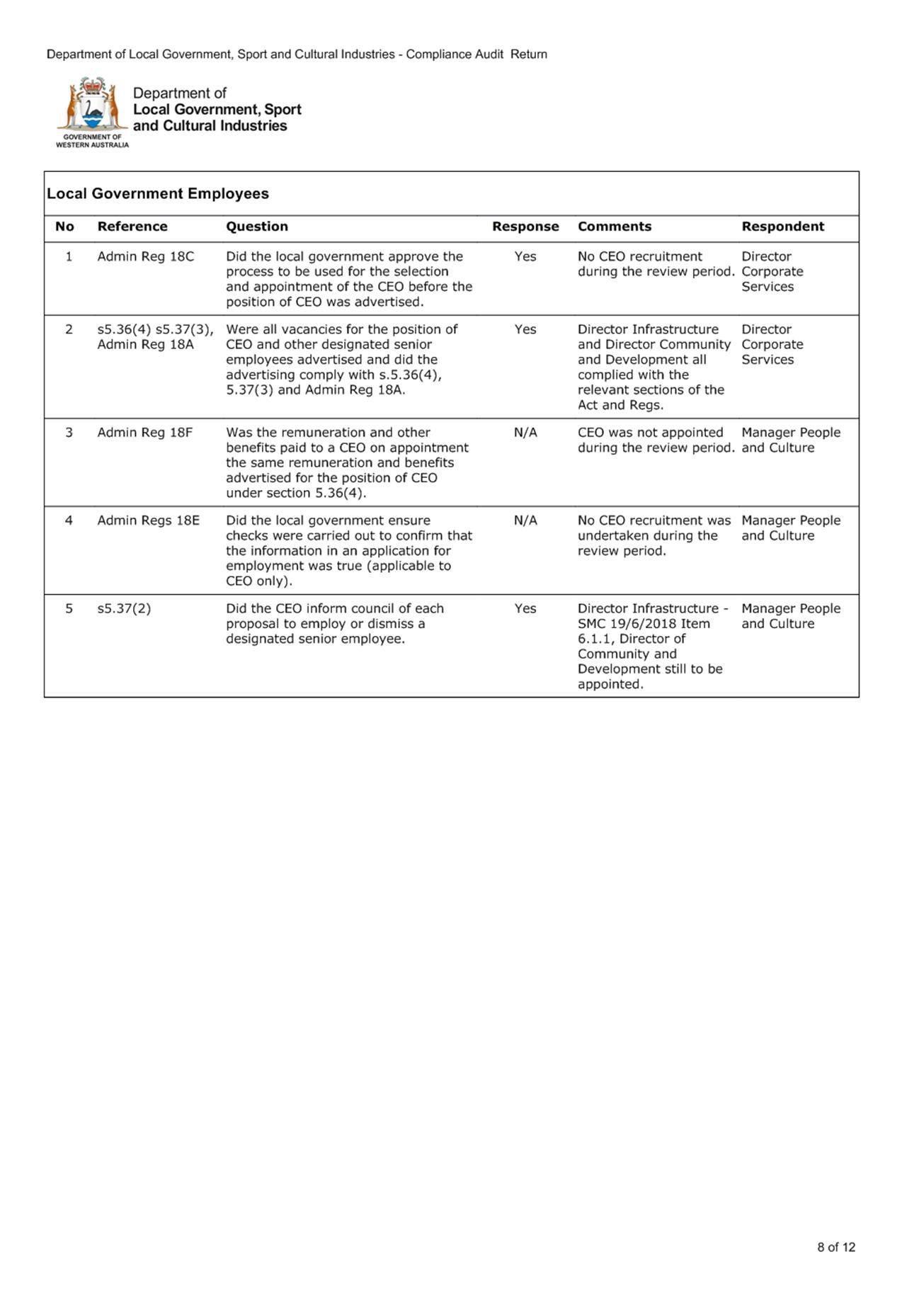

Section 7.13(1)(i) of the Local

Government Act 1995 requires that each local government carry out a compliance

audit for the period 1 January to 31 December each year. The Compliance

Audit is an in-house self audit that is undertaken by staff.

In accordance with Regulation 14 of

the Local Government (Audit) Regulations 1996 the Audit and Risk

Committee is to review the Compliance Audit Return (CAR) and is to report to

Council the results of that review. The CAR is to be:

1. presented

to an Ordinary Meeting of Council

2. adopted

by Council; and

3. recorded

in the minutes of the meeting at which it is adopted.

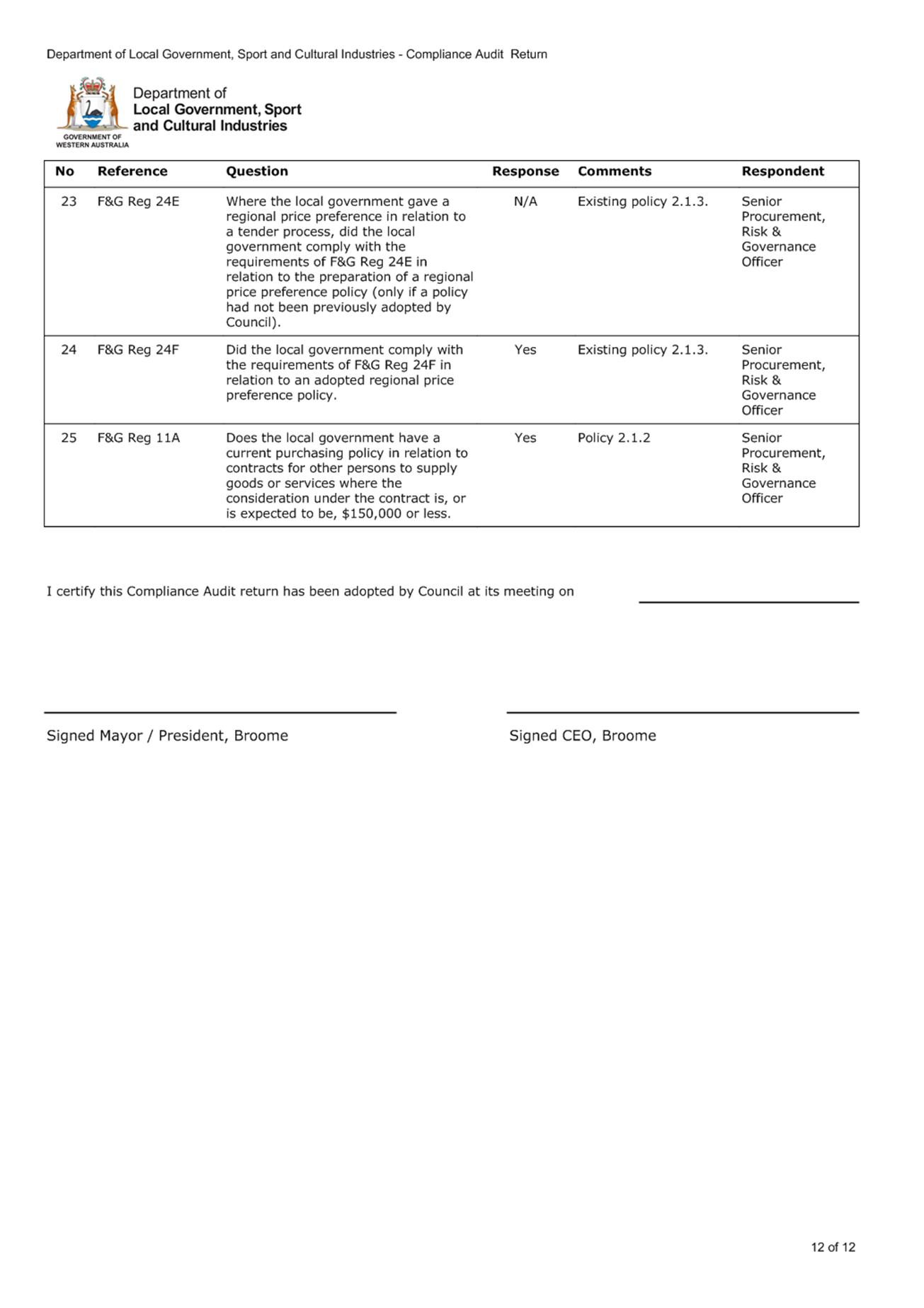

Following the adoption by Council of

the CAR, a certified copy of the return, along with the relevant section of the

minutes and any additional information detailing the contents of the return are

to be submitted to the DLGSC by 31 March 2019.

The return requires the Shire

President and the Chief Executive Officer to certify that the statutory

obligations of the Shire of Broome have been complied with.

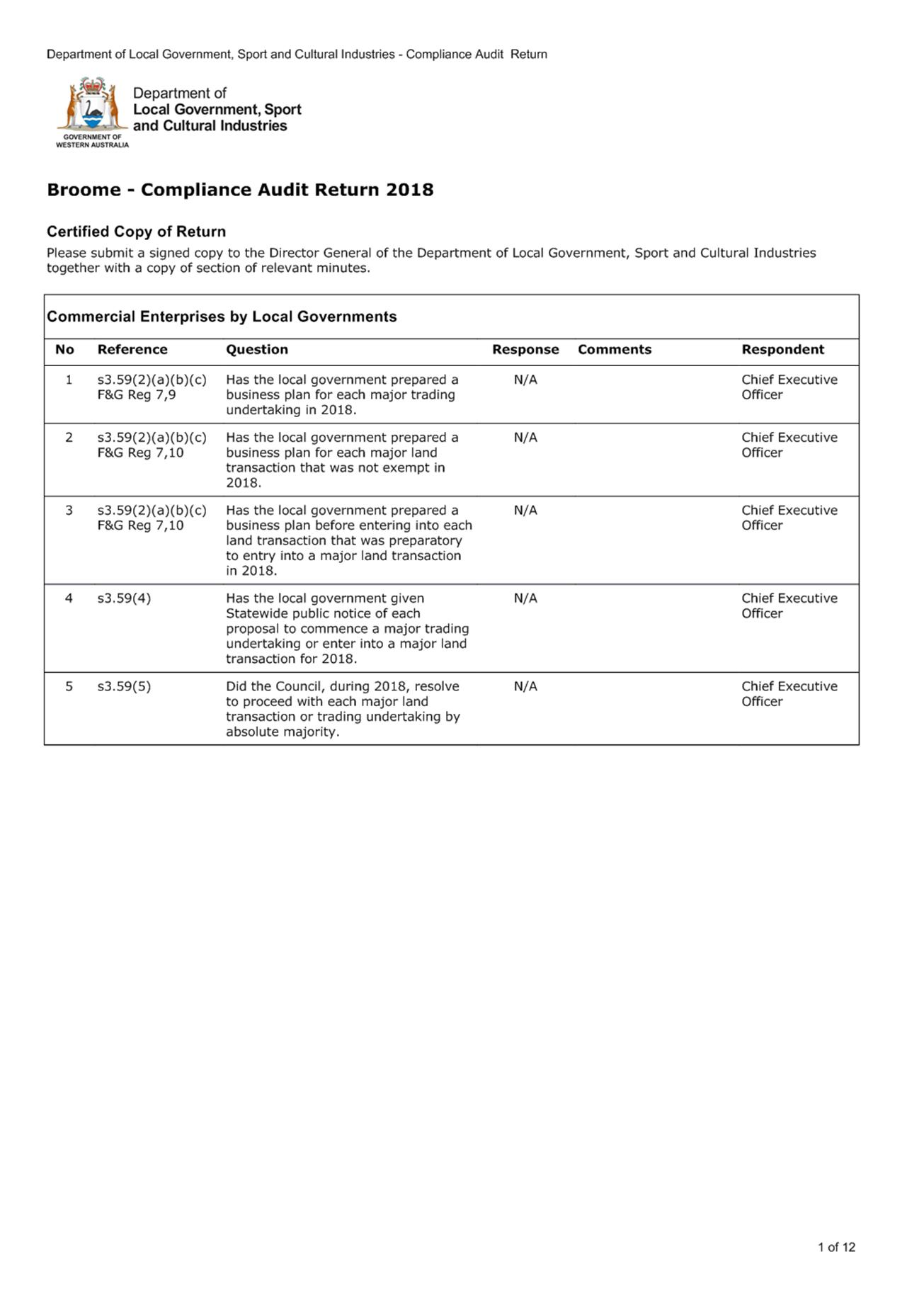

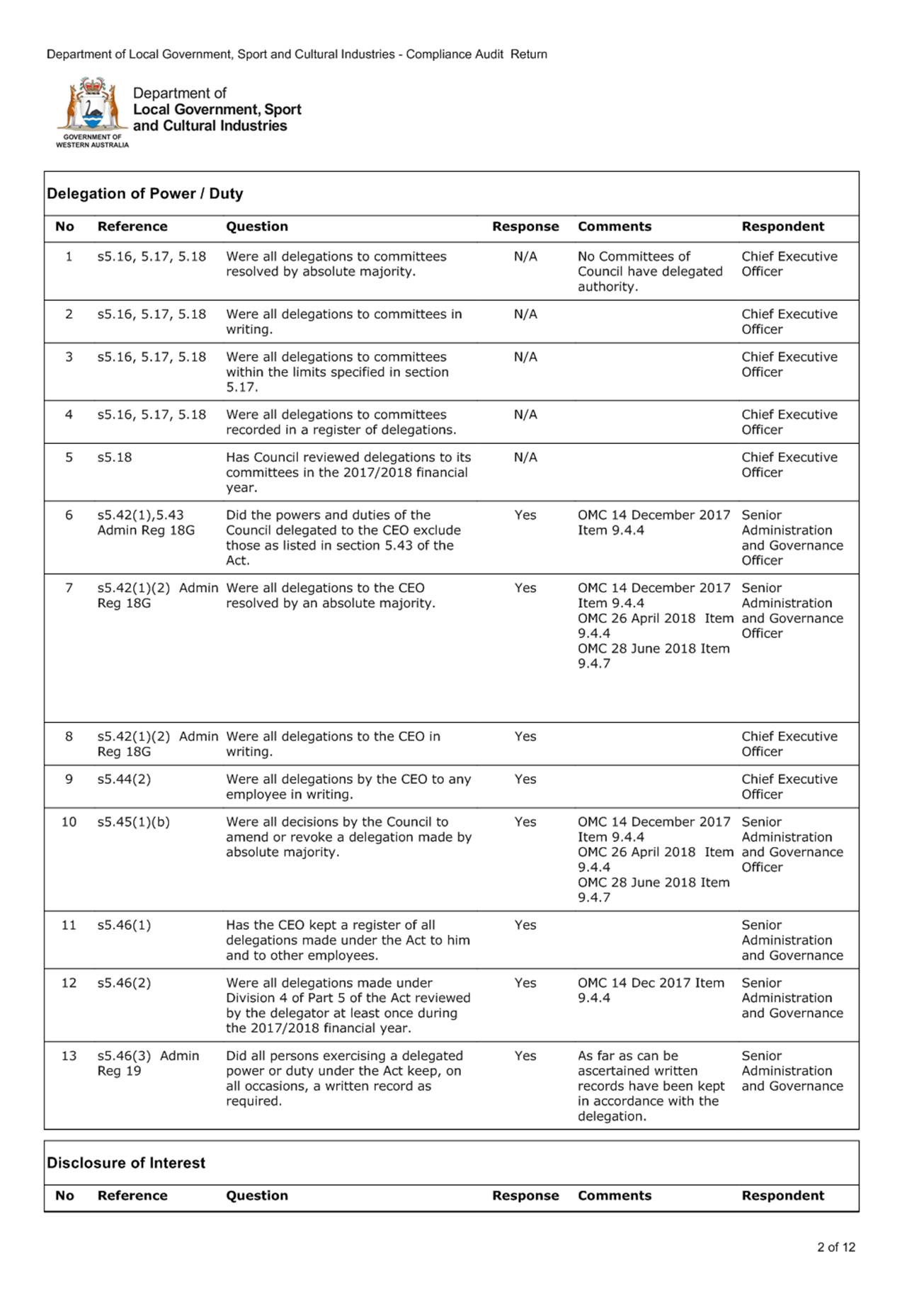

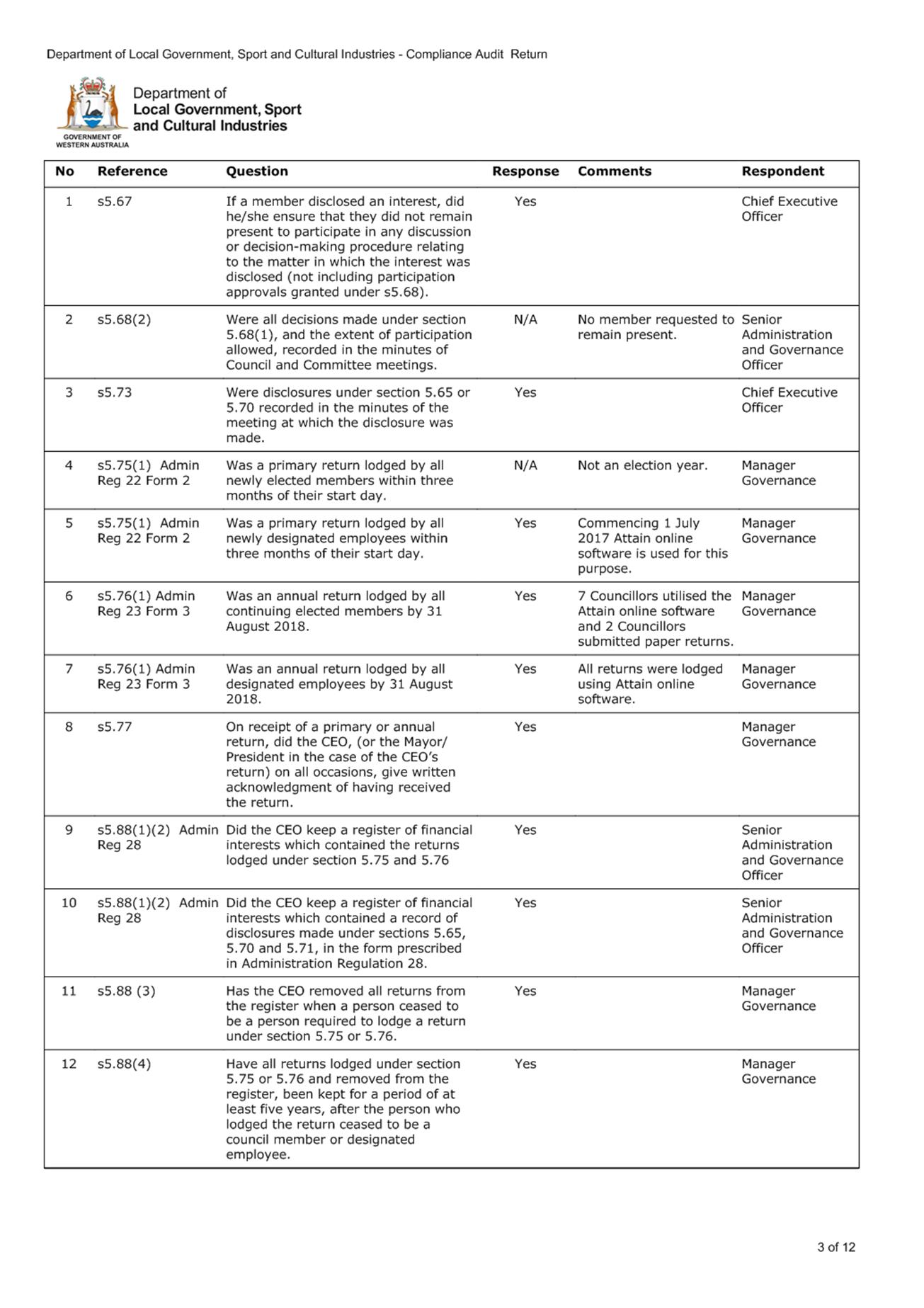

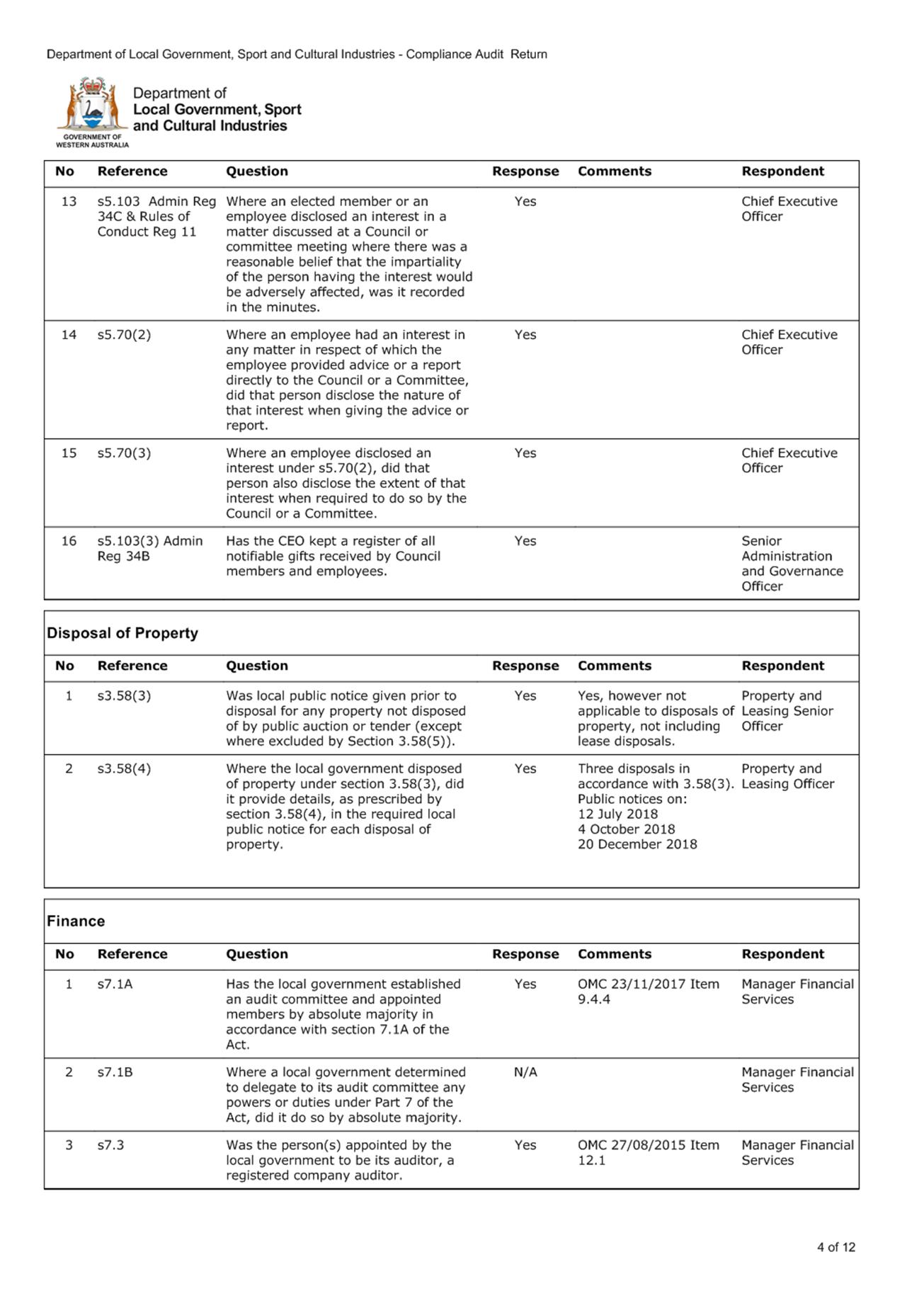

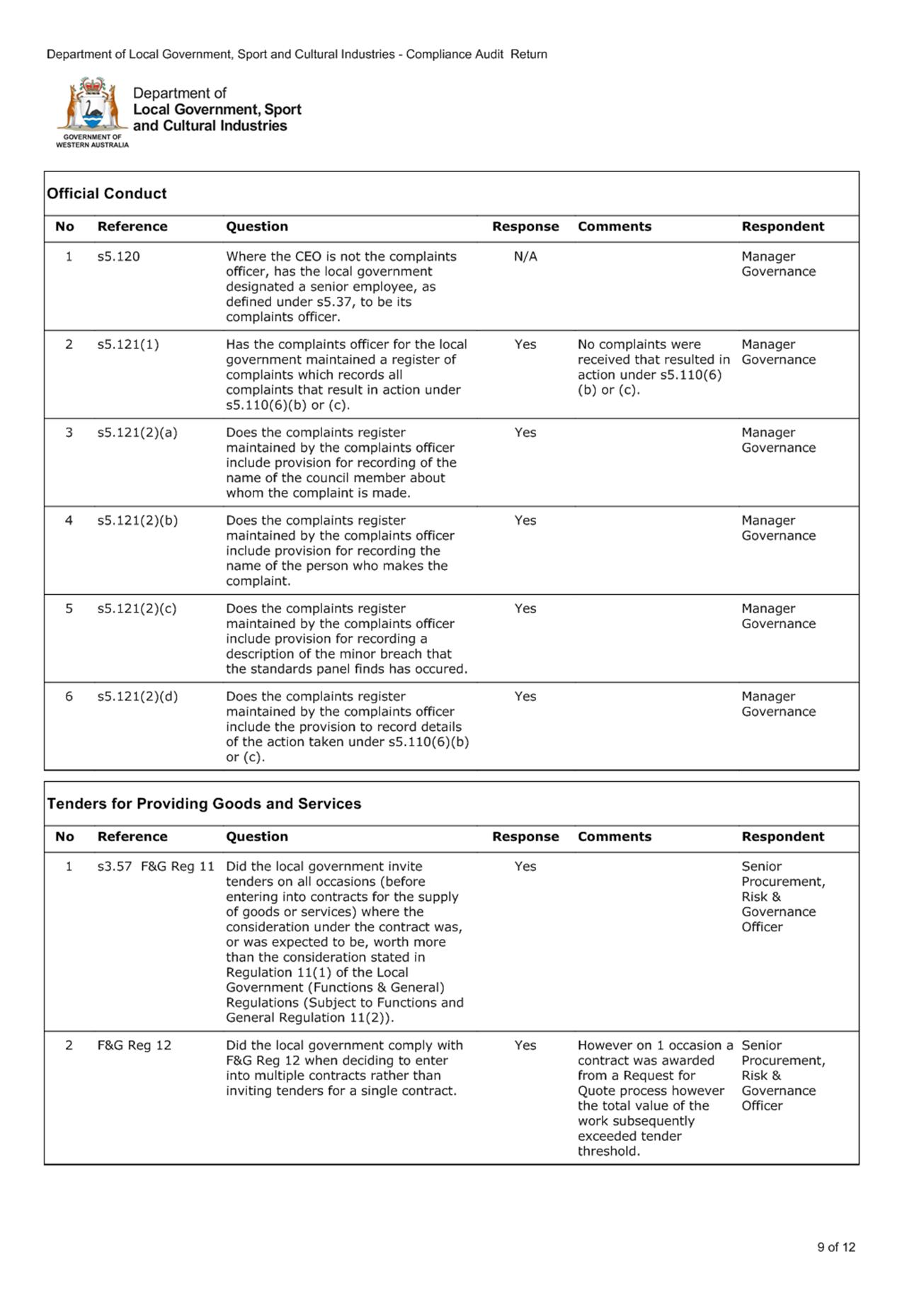

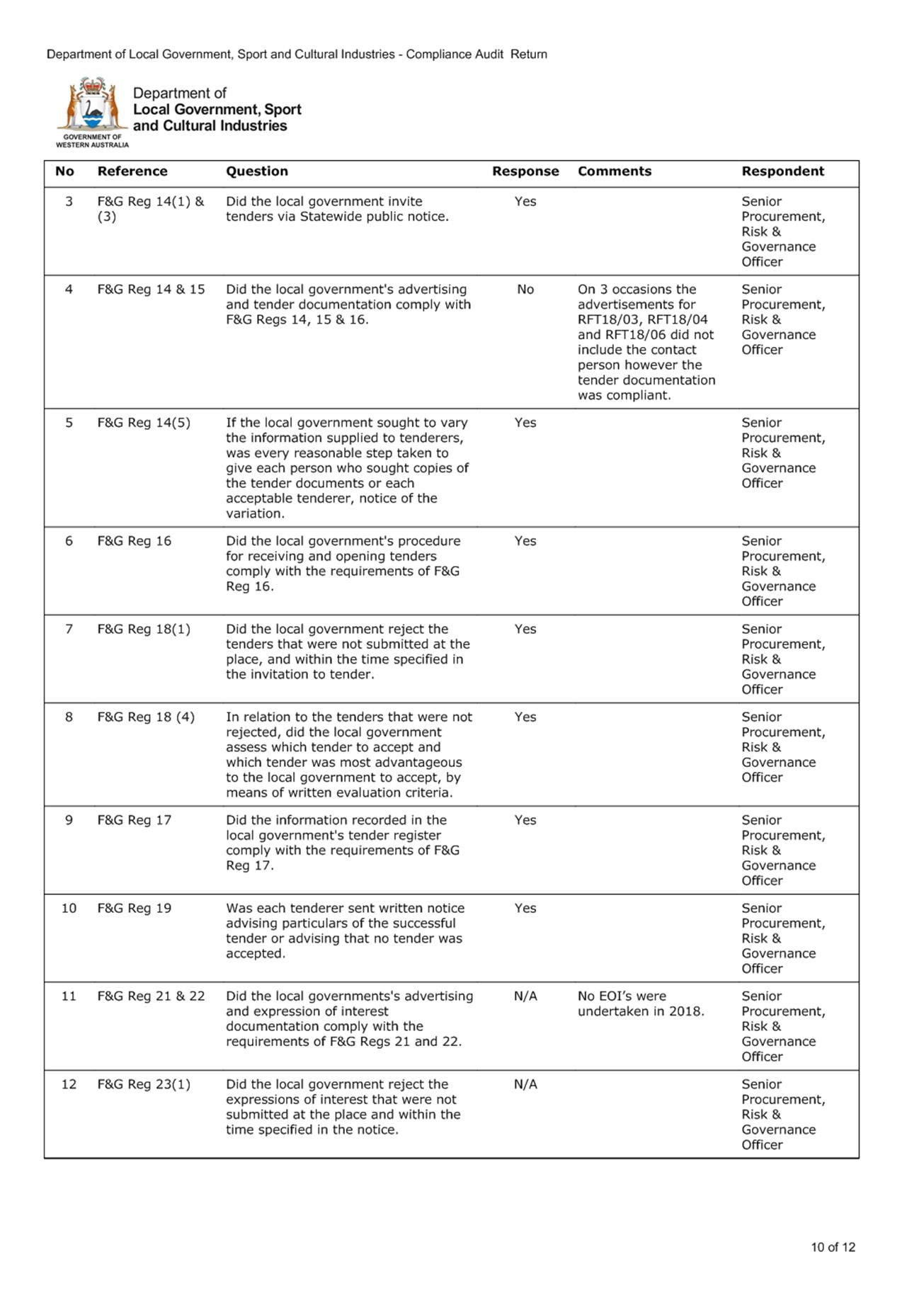

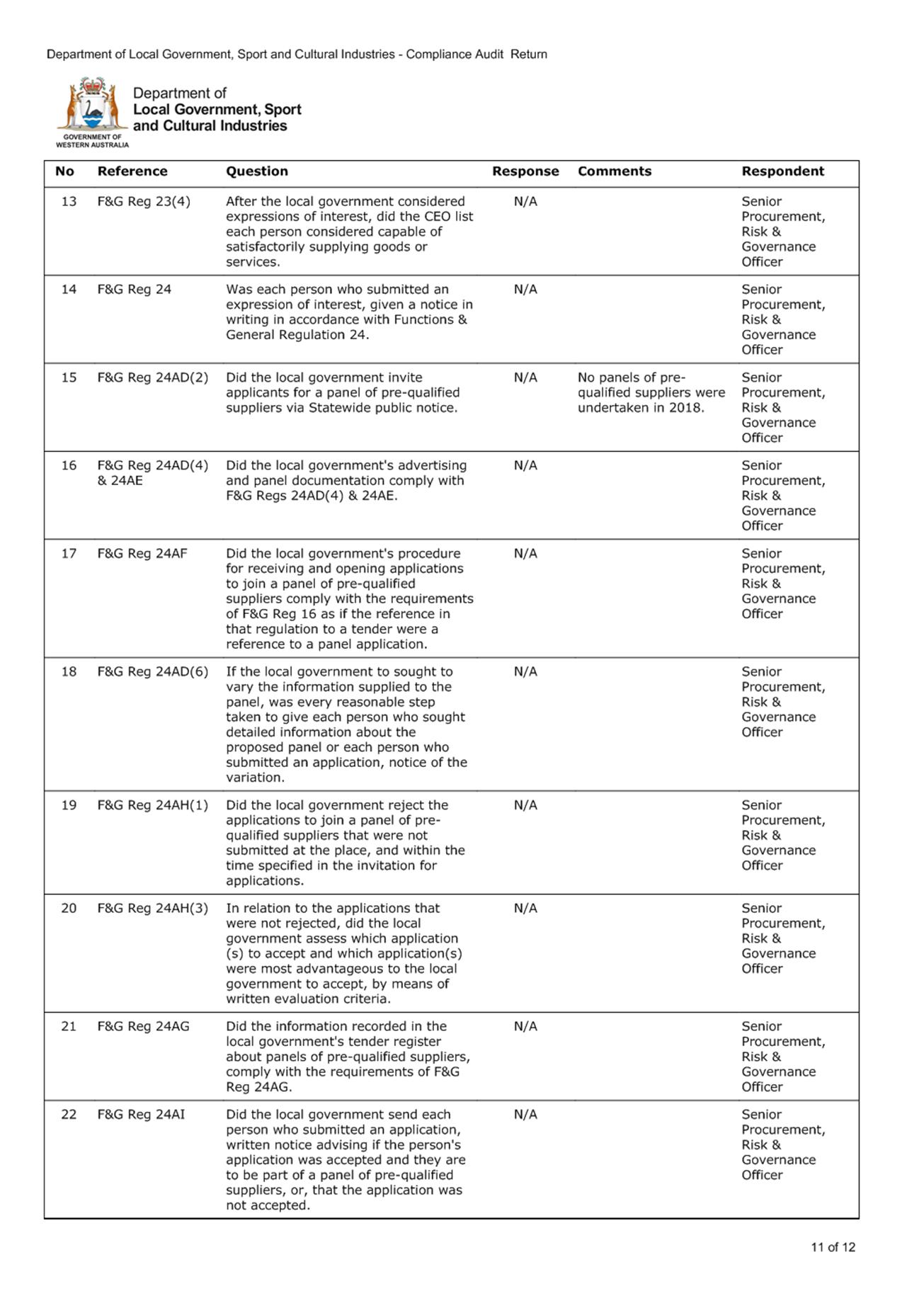

COMMENT

The CAR for the period 1 January to

31 December 2018 continues in the reduced format introduced in 2011 with

questions focused on high risk areas of compliance and statutory reporting as

prescribed in Regulation 13 of the Local Government (Audit) Regulations

1996. The 2017 CAR was extended to include 7

optional questions relating to Integrated Planning and Reporting and this year

has been extended further to include 2 optional questions relating to

regulation 17 of the Local Government (Audit) Regulations 1996. It is

noted that the question relating to Elections has been removed from the 2018

CAR.

The 2018 CAR includes a total of 94

questions and focuses on the following areas of compliance:

· Commercial

Enterprises by Local Governments

· Delegation

of Power/Duty

· Disclosure

of Interest

· Disposal of

Property

· Finance

· Integrated

Planning and Reporting (optional)

· Local

Government Employees

· Official

Conduct

· Tenders for

Providing Goods and Services.

The 2018 CAR has been completed in

consultation with officers responsible for the various areas contained in the

return, and reviewed by the Executive Management Group and the Chief Executive

Officer.

The 2018 Compliance Audit reveals a

compliance rating of 98.9% with 1 area of non-compliance of the 94 areas

audited. The non-compliance related to the omission of details of a contact

person for 3 tender advertisements as required under Regulation 14 of the Local

Government (Functions and General) Regulations 1996.

This compares to:

2017 Compliance

Audit – 0 areas of non-compliance of the 94 areas audited (100%)

2016 Compliance

Audit – 1 area of non-compliance of the 87 areas audited (98.8%)

2015 Compliance

Audit – 0 areas of non-compliance of the 87 areas audited (100%)

2014

Compliance Audit – 1 area of non-compliance of the 78 areas audited

(98.7%)

2013 Compliance

Audit – 0 areas of non-compliance of the 78 areas audited (100%)

2012 Compliance

Audit – 8 areas of non-compliance of 78 areas audited (89.7%)

2011

Compliance Audit – 1 area of non-compliance of 78 areas audited (98.7%)

2010

Compliance Audit – 1 area of non-compliance of 283 areas audited

(99.6%)

2009 Compliance

Audit – 4 areas of non-compliance of 347 areas audited (98.8%)

2008

Compliance Audit – 2 areas of non-compliance of 311 areas audited

(99.4%

2007

Compliance Audit – 13 areas of non-compliance of 271 areas audited

(96.1%)

2006

Compliance Audit – 21 areas of non-compliance of 271 areas audited

(92.3%)

2005

Compliance Audit – 23 areas of non-compliance of 306 areas audited

(92.5%)

2004

Audit – 18 areas of non-compliance and 147 areas audited (87.8%).

CONSULTATION

Nil

STATUTORY ENVIRONMENT

Local Government Act 1995

7.13 Regulations

as to audits

(1) Regulations

may make provision –

(i) requiring

local governments to carry out, in the prescribed manner and in a form approved

by the Minister, an audit of compliance with such statutory requirements as are

prescribed whether those requirements are –

(i) of

a financial nature or not; or

(ii) under

this Act or another written law.

Local Government (Audit)

Regulations 1996

13. Prescribed

statutory requirements for which compliance audit needed (Act s.

7.13(1)(i))

For

the purposes of section 7.13(1)(i) the statutory requirements set forth in

the Table to this regulation are prescribed.

Table

|

Local Government

Act 1995

|

|

s. 3.57

|

s. 3.58(3) and (4)

|

s. 3.59(2), (4)

and (5)

|

|

s. 5.16

|

s. 5.17

|

s. 5.18

|

|

s. 5.36(4)

|

s. 5.37(2) and (3)

|

s. 5.42

|

|

s. 5.43

|

s. 5.44(2)

|

s. 5.45(1)(b)

|

|

s. 5.46

|

s. 5.67

|

s. 5.68(2)

|

|

s. 5.70

|

s. 5.73

|

s. 5.75

|

|

s. 5.76

|

s. 5.77

|

s. 5.88

|

|

s. 5.89A

|

s. 5.103

|

s. 5.120

|

|

s. 5.121

|

s. 7.1A

|

s. 7.1B

|

|

s. 7.3

|

s. 7.6(3)

|

s. 7.9(1)

|

|

s. 7.12A

|

|

|

|

Local Government

(Administration) Regulations 1996

|

|

r. 18A

|

r. 18C

|

r. 18E

|

|

r. 18F

|

r. 18G

|

r. 19

|

|

r. 19C

|

r. 19DA

|

r. 22

|

|

r. 23

|

r. 28

|

r. 34B

|

|

r. 34C

|

|

|

Local Government

(Audit) Regulations 1996

|

|

r. 7

|

r. 10

|

|

|

Local Government

(Elections) Regulations 1997

|

|

r. 30G

|

|

|

|

Local Government

(Functions and General) Regulations 1996

|

|

r. 7

|

r. 9

|

r. 10

|

|

r. 11A

|

r. 11

|

r. 12

|

|

r. 14(1), (3)

and (5)

|

r. 15

|

r. 16

|

|

r. 17

|

r. 18(1) and (4)

|

r. 19

|

|

r. 21

|

r. 22

|

r. 23

|

|

r. 24

|

r. 24AD(2), (4)

and (6)

|

r. 24AE

|

|

r. 24AF

|

r. 24AG

|

r. 24AH(1)

and (3)

|

|

r. 24AI

|

r. 24E

|

r. 24F

|

|

Local Government

(Rules of Conduct) Regulations 2007

|

|

r. 11

|

|

|

[Regulation

13 inserted in Gazette 23 Apr 1999 p. 1722‑4; amended in

Gazette 1 Jun 2004

p. 1917; 31 Mar 2005 p. 1042‑3; 30 Sep 2005

p. 4418-20; 21 Dec 2010 p. 6758-61;

30 Dec 2011 p. 5579-80; 18 Sep 2015 p. 3813; 26 Jun 2018 p.

2386.]

14. Compliance

audits by local governments

(1) A

local government is to carry out a compliance audit for the period 1 January to

31 December in each year.

(2) After

carrying out a compliance audit the local government is to prepare a compliance

audit return in a form approved by the Minister.

(3A) The

local government’s audit committee is to review the compliance audit

return and is to report to the council the results of that review.

(3) After

the audit committee has reported to the council under subregulation (3A), the

compliance audit return is to be —

(a) presented

to the council at a meeting of the council; and

(b) adopted

by the council; and

(c) recorded

in the minutes of the meeting at which it is adopted.

[Regulation

14 inserted in Gazette 23 Apr 1999 p. 1724‑5; amended in Gazette 30 Dec

2011 p. 5580-1.]

15. Compliance

audit return, certified copy of etc. to be given to Departmental CEO

(1) After

the compliance audit return has been presented to the council in accordance with

regulation 14(3) a certified copy of the return together with —

(a) a

copy of the relevant section of the minutes referred to in regulation 14(3)(c);

and

(b) any

additional information explaining or qualifying the compliance audit,

is to be submitted to the

Departmental CEO by 31 March next following the period to which the return

relates.

(2) In

this regulation —

certified

in relation to a compliance audit return means signed by —

(a) the

mayor or president; and

(b) the

CEO.

[Regulation 15

inserted in Gazette 23 Apr 1999 p. 1725; amended in Gazette 26

Jun 2018 p. 2386.]

POLICY IMPLICATIONS

Nil

FINANCIAL IMPLICATIONS

Nil

RISK

The Local Government Act 1995

requires that each local government carry out a compliance audit for the period

1 January to 31 December each year. The compliance audit is an in-house

self audit that is undertaken by staff and is to be submitted to the DLGSC by

31 March each year.

The risk is Extreme if this date is

not met as it results in non-compliance with the legislative requirements of

the Local Government Act 1995 and Local Government (Audit)

Regulations 1996, and loss of reputation with the DLGSC. The

likelihood of this occurring is rare as the Compliance Audit Return has been prepared

well in advance for presentation to Council on the 28 February 2019.

STRATEGIC IMPLICATIONS

Our

Organisation Goal – Continually enhance the Shire’s organisational

capacity to service the needs of a growing community:

Improved systems, processes and

compliance

VOTING REQUIREMENTS

Simple Majority

|

REPORT RECOMMENDATION:

That the Audit and Risk Committee recommends that

Council:

1. Adopts the

attached 2018 Compliance Audit Return as the official return for the Shire of

Broome; and

2. Requests

the Chief Executive Officer to submit the certified return and a copy of the

minutes relative to this report to the Department of Local Government, Sport

and Cultural Industries prior to 31 March 2019.

|

Attachments

|

1.

|

2018 Compliance Audit Return

|

|

Item 5.1 - COMPLIANCE AUDIT RETURN 2018

|

Agenda –

Audit and Risk Committee Meeting 12 February 2019 Page 1 of 4

|

5.2 2ND

QUARTER FINANCE AND COSTING REVIEW 2018-19

LOCATION/ADDRESS: Nil

APPLICANT: Nil

FILE: FRE02

AUTHOR: Manager

Financial Services

CONTRIBUTOR/S: Nil

RESPONSIBLE

OFFICER: Director

Corporate Services

DISCLOSURE

OF INTEREST: Nil

DATE OF REPORT: 6

February 2018

|

|

SUMMARY: The

Audit Committee is requested to consider results of the 2nd Quarter Finance

and Costing Review (FACR) of the Shire’s budget for the period ended 31

December 2018, including forecast estimates and budget recommendations to 30

June 2019.

|

BACKGROUND

Previous

Considerations

OMC 28 June 2018 Item

12.2

OMC 22 November 2018 Item

10.3

Quarter 1

Finance and Costing Review

The Shire of

Broome has carried out its 2nd Quarter Finance and Costing Review (FACR) for

the 2018/19 Financial Year. This Review of the 2018-2019 Annual Budget is based

on actuals and commitments for the first six months of the year from 1 July

2018 to 31 December 2018, and forecasts for the remainder of the financial

year.

This process aims

to highlight over and under expenditure of funds and over and under achievement

of income targets for the benefit of Executive and Responsible Officers to

ensure good fiscal management of their projects and programs.

Once this process

is completed, a report is compiled identifying budgets requiring amendments to

be adopted by Council. Additionally, a summary provides the financial impact of

all proposed budget amendments to the Shire of Broome’s adopted

end-of-year forecast, in order to assist Council to make an informed decision.

It should be

noted that the 2018/2019 annual budget was adopted at the Ordinary Meeting of

Council on 28 June 2018 as a balanced budget. There have been further amendments

adopted by Council as part of the Annual Financial Statements for the use of

additional carried forward surplus. The result of all amendments prior to the 2nd

Quarter FACR is a $207,628 deficit upon the Shire of Broome’s forecast

end of year position. This $207,628 of opening deficit relates mainly to the

following adopted budget amendments to date:

· $40,000

additional contribution to the Events Economic Tourism Development funding

program as per the adopted minutes OMC 26/4/18 to amend 2018-19 budget upon

adoption.

· $100,000

towards seed funding payable to the revised Broome Future Alliance Ltd as per

the adopted minutes of the OMC on 28 June 2018.

· $187,272

deficit arising from Q1 FACR which included the following high-dollar value

expenditure put forward:

o Additional legal fees &

Dampier Peninsula NT Appeals - $75,000

o Singapore Flights –

$58,000

o FAGS reduction in Aboriginal

Access Road grants - $44,000

o Extra plant growing for

capital projects - $32,000

o BRAC road base for asbestos mitigation

- $26,000

COMMENT

The 2nd Quarter

FACR commenced on 30 January 2019. The results from this process indicate a

deficit forecast financial position to 30 June 2019 of $127,235 should Council

approve the proposed budget amendments.

The net deficit forecasted included

the $100,000 towards seed funding payable to the revised Broome Future Alliance

Ltd as per the adopted minutes of the OMC on 28 June 2018 and $40,000

additional contribution to the Events Economic Tourism Development funding

program as per the adopted minutes OMC 26/4/18 amending 2018-19 budget.

The above figure represents a budget

forecast should all expenditure and income occur as expected. It does not

represent the actual end-of-year position which can only be determined as part

of the normal annual financial processes at the end of the financial year.

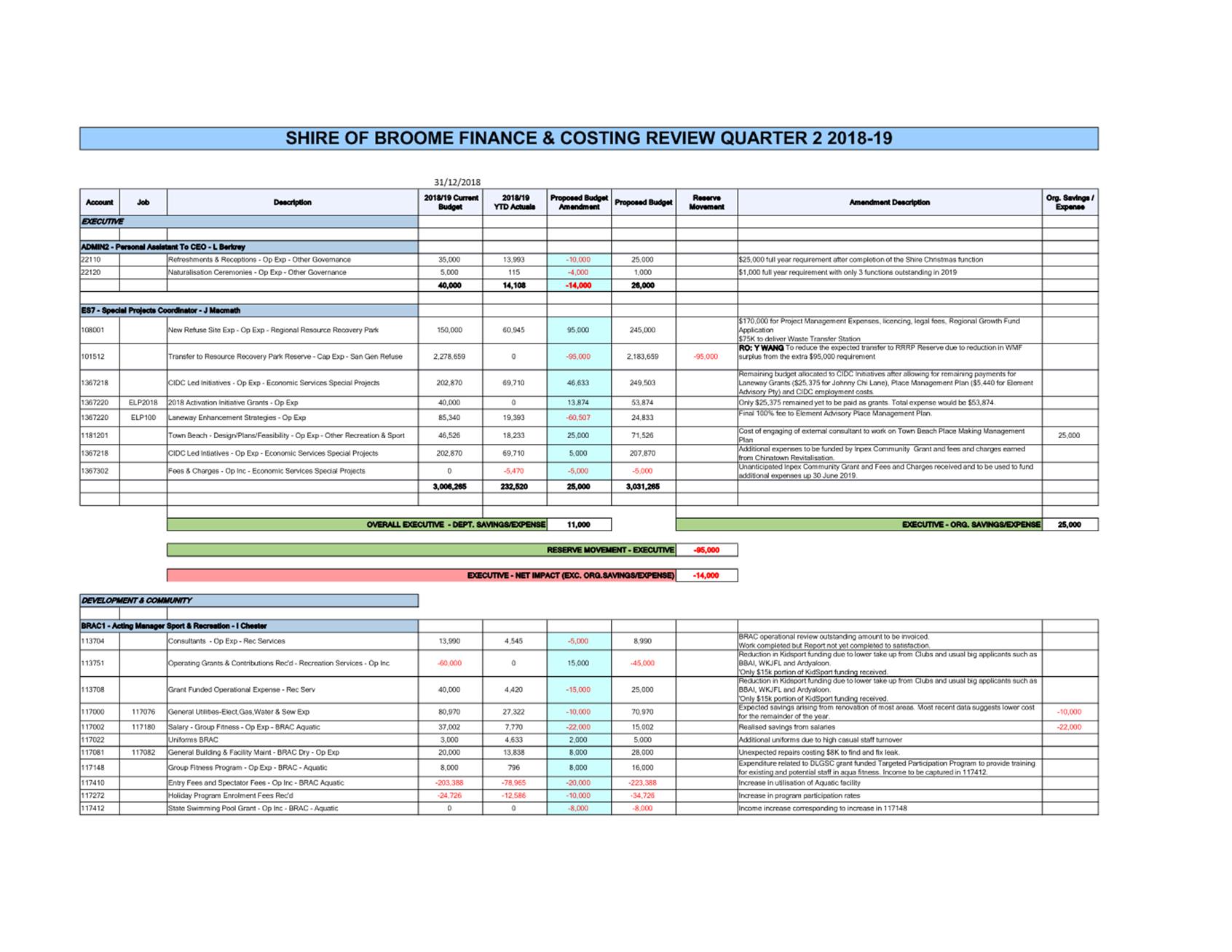

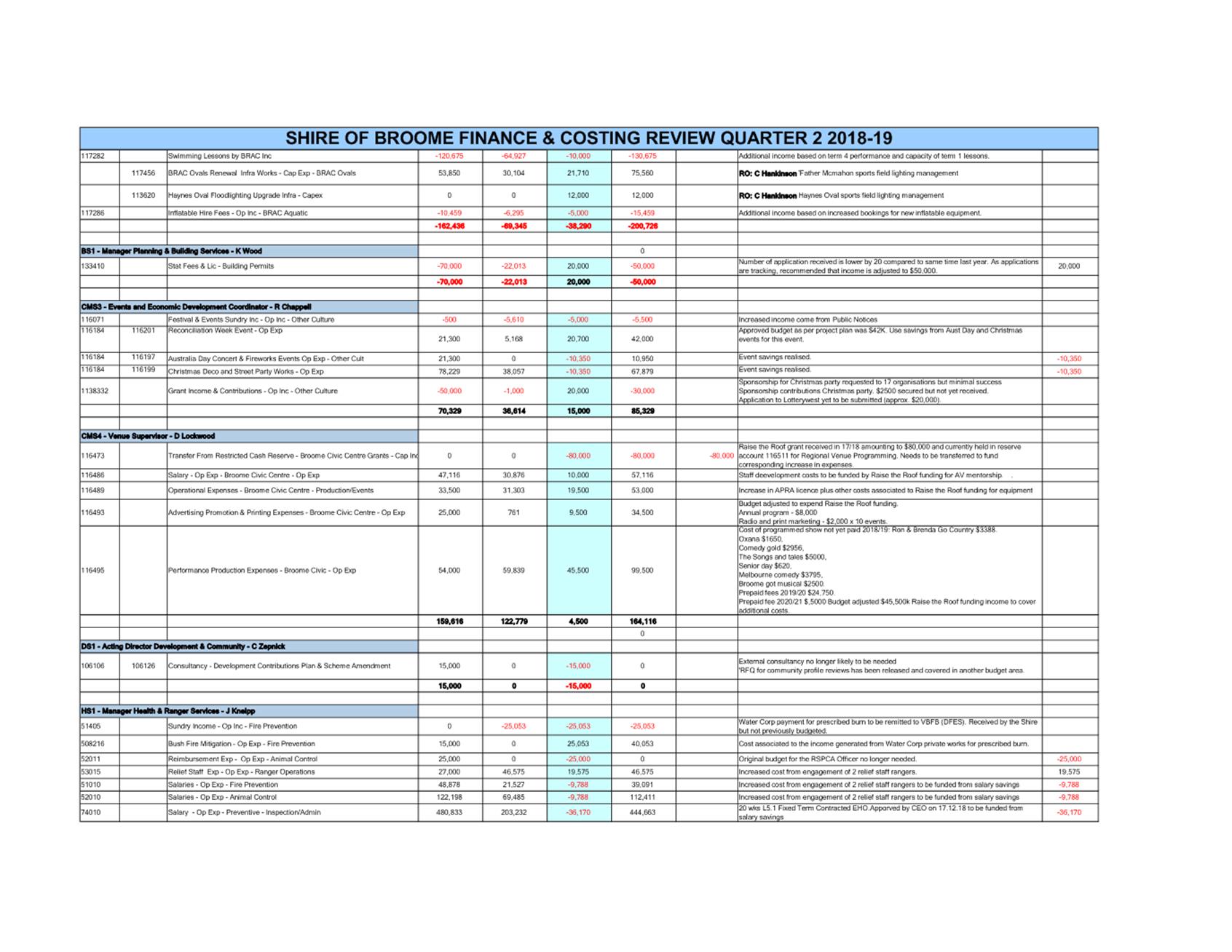

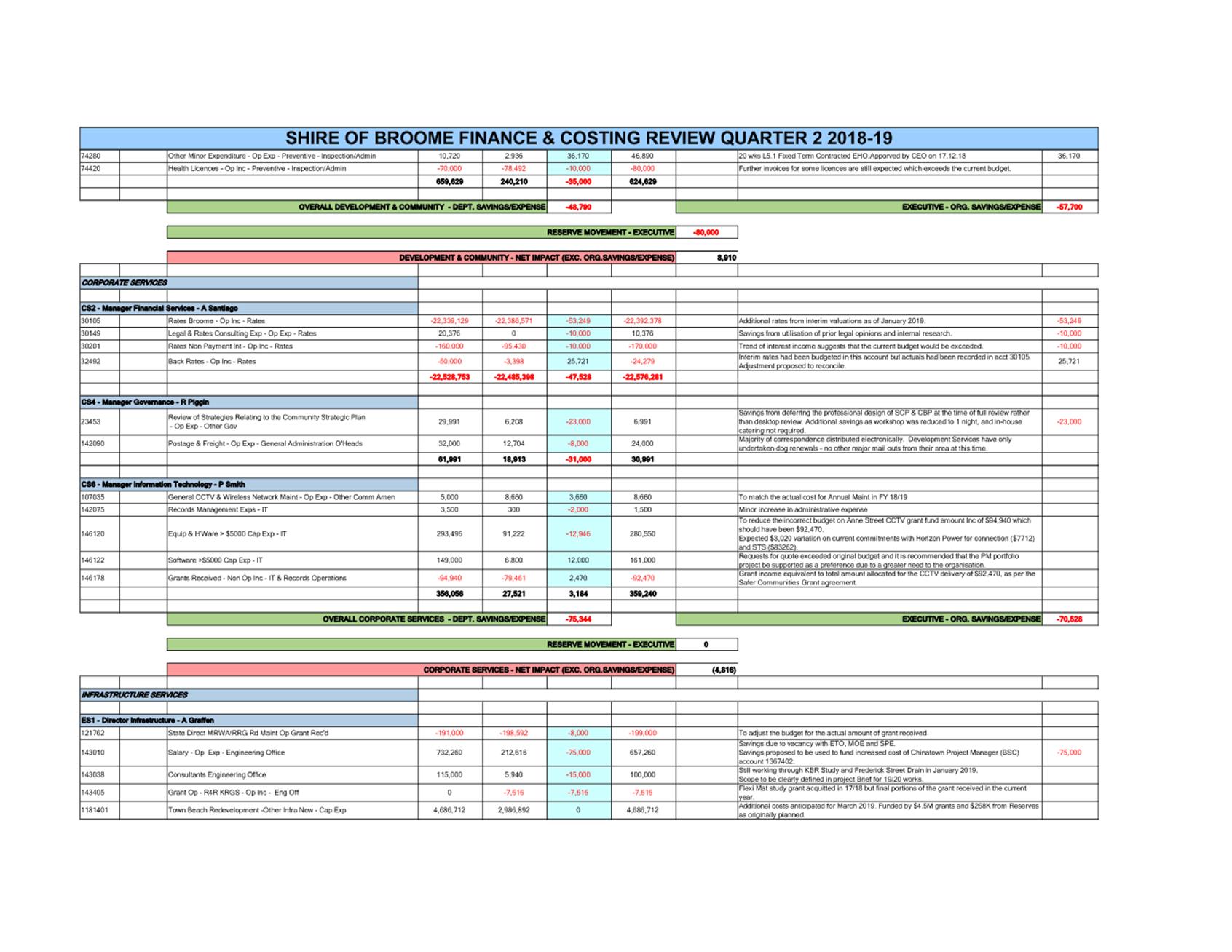

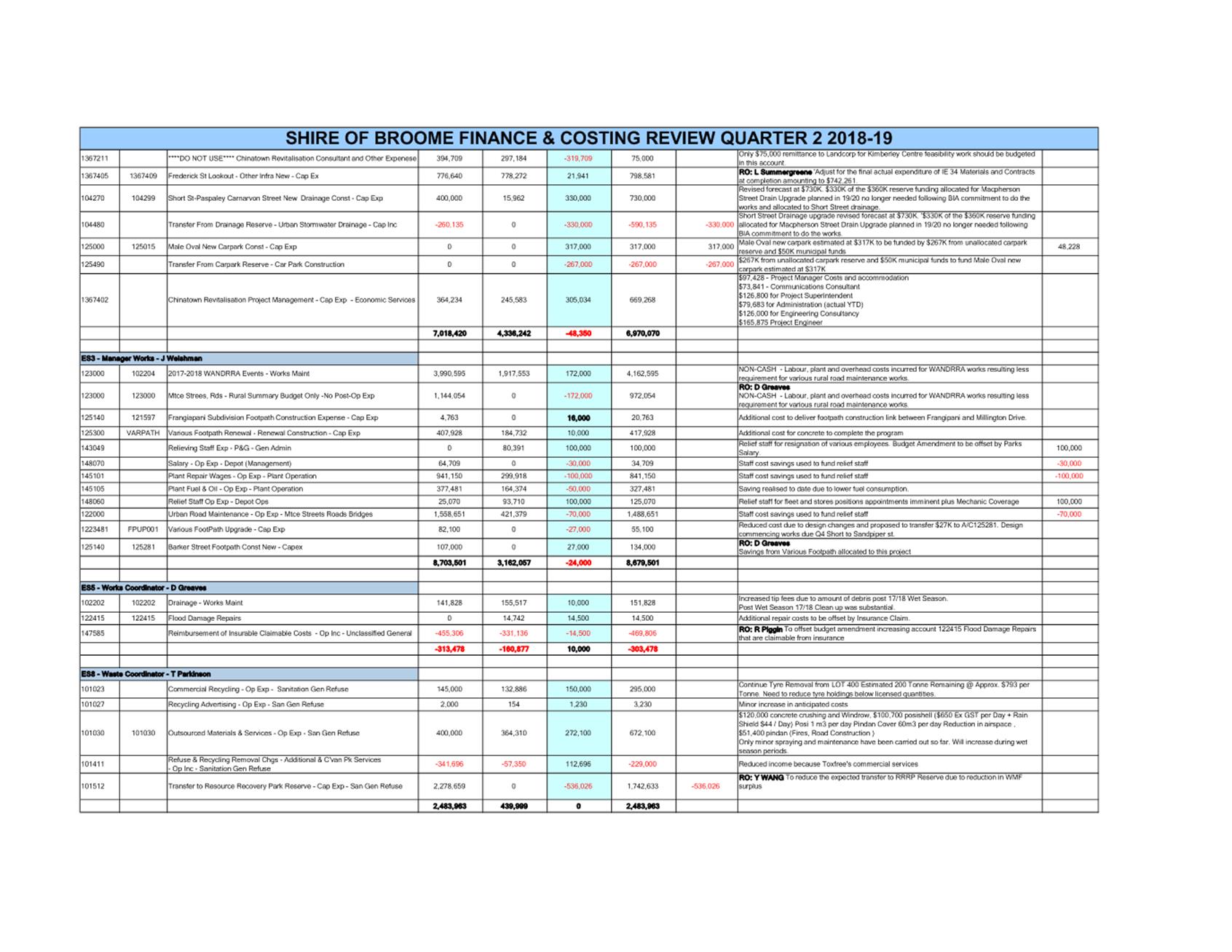

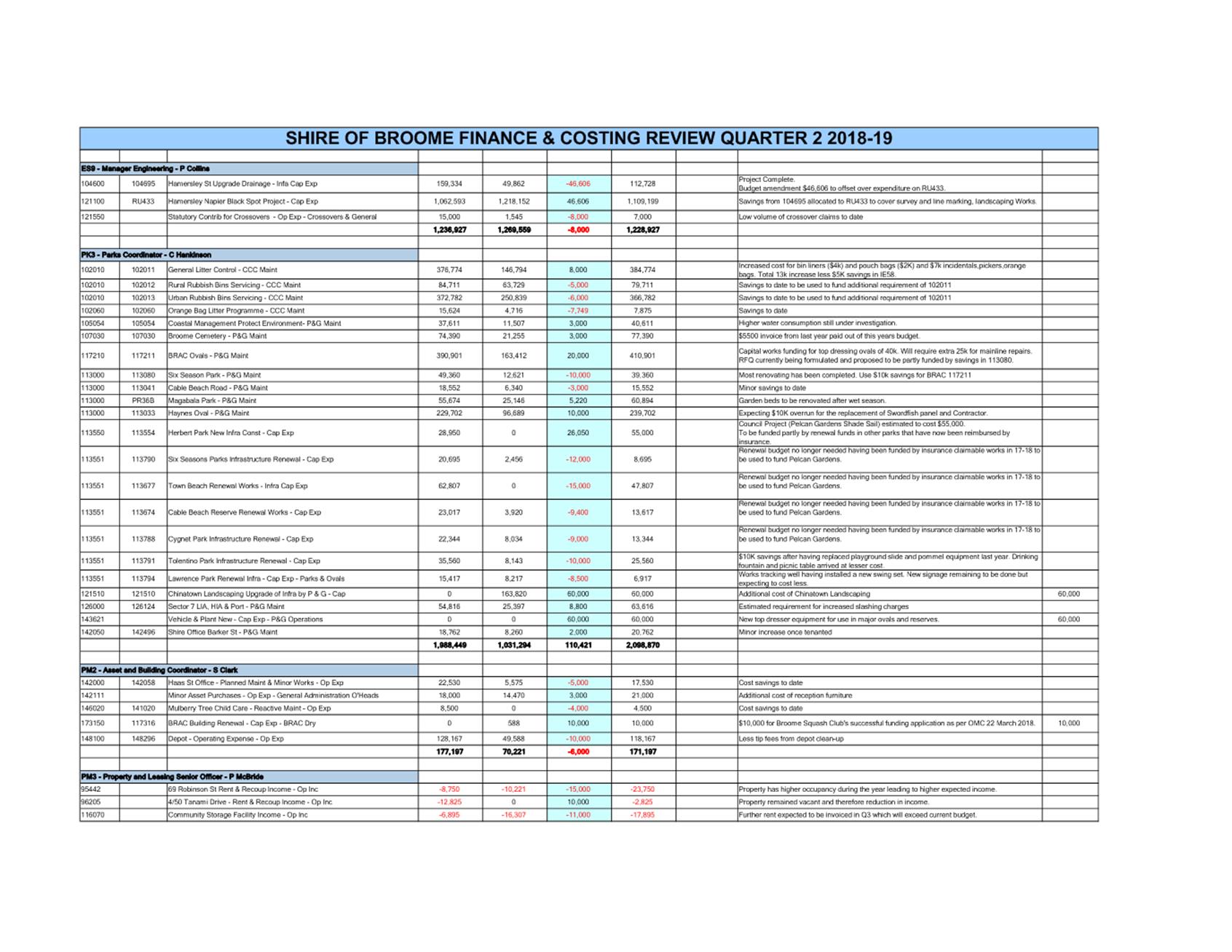

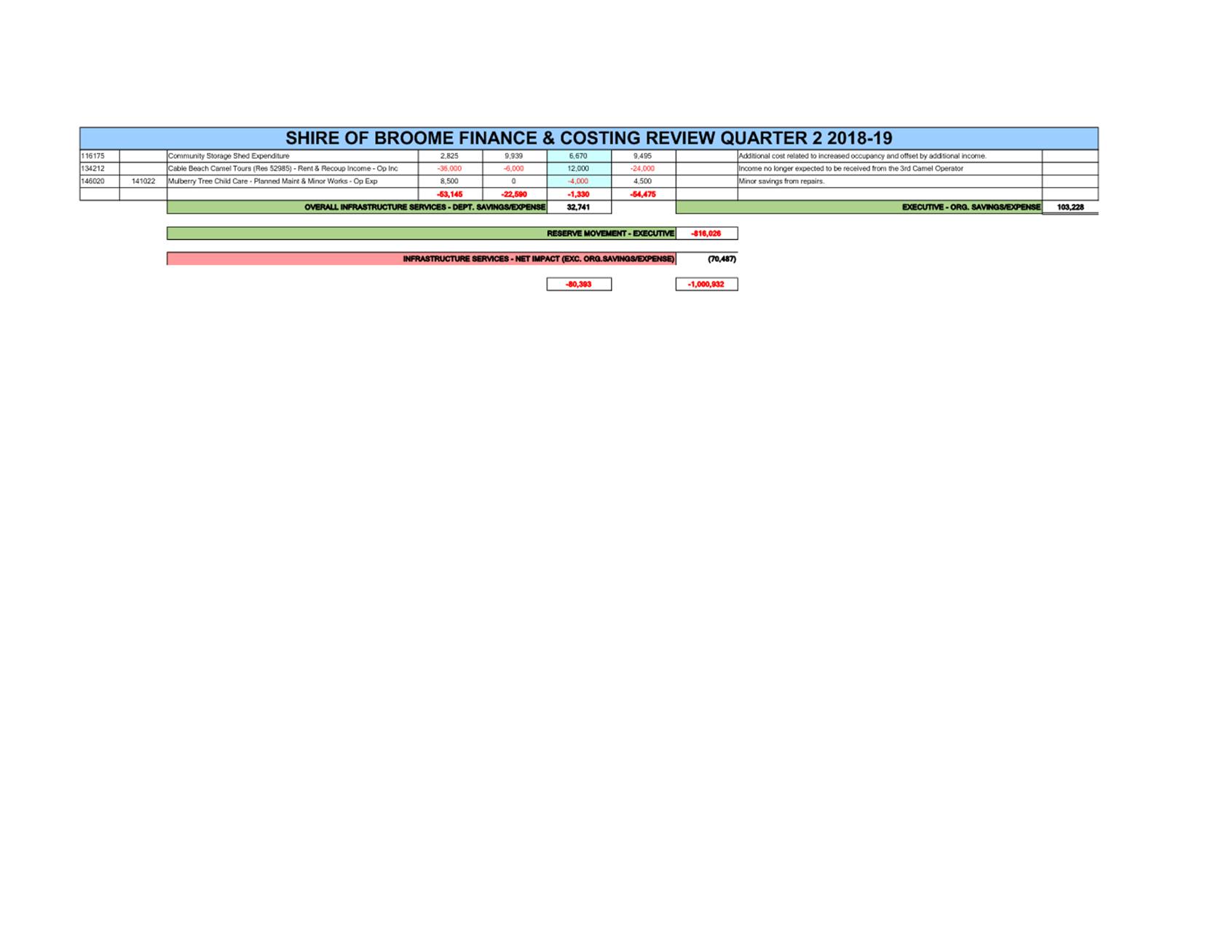

A comprehensive list of accounts

(refer to Attachment 1) has been included for perusal by the committee and

summarised by Directorate.

A summary of

the results follows:

|

|

|

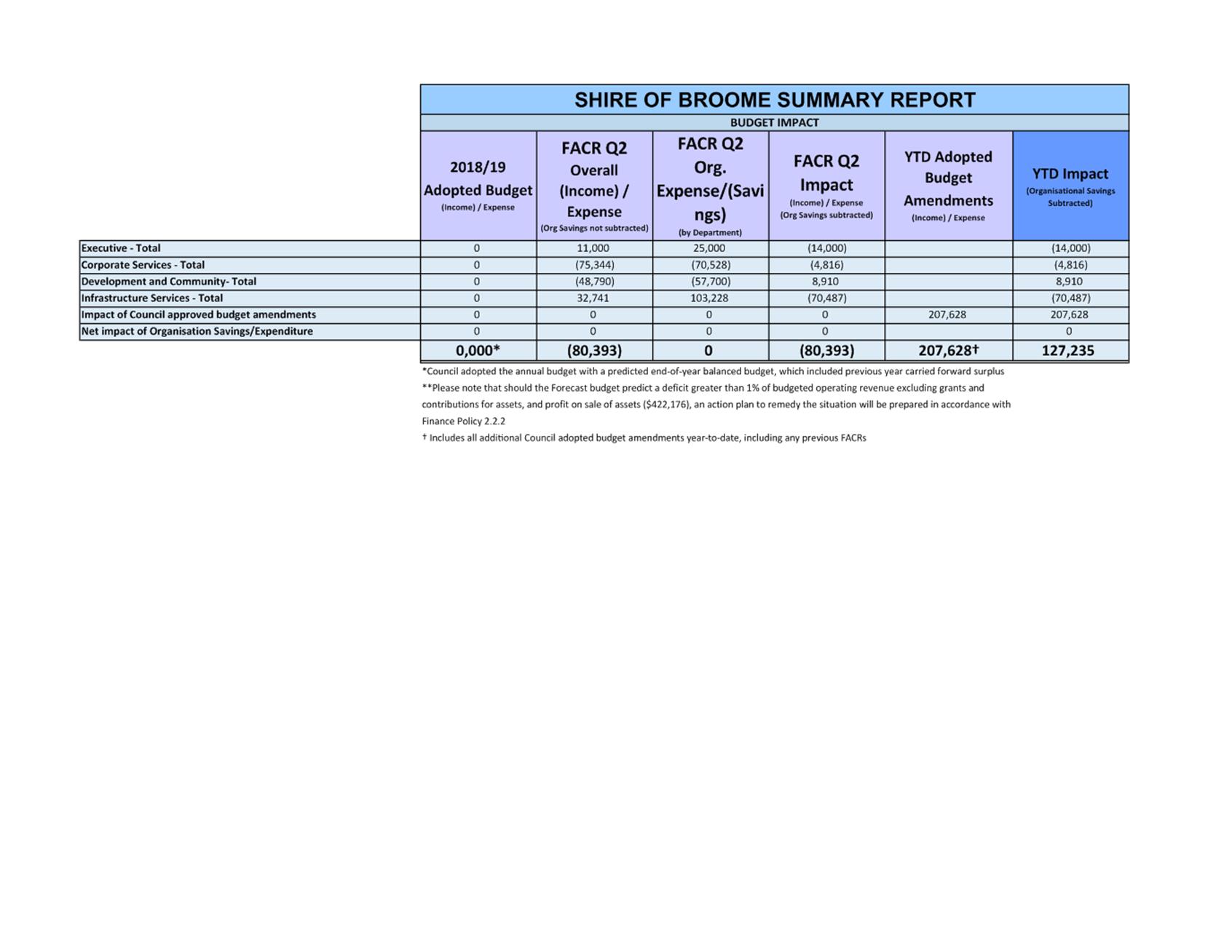

SHIRE OF

BROOME SUMMARY REPORT

|

|

|

|

BUDGET

IMPACT

|

|

|

|

2018/19

Adopted Budget

(Income) / Expense

|

FACR Q2

Overall (Income) / Expense

(Org Savings not subtracted)

|

FACR Q2

Org. Expense/(Savings)

(by Department)

|

FACR Q2

Impact

(Income) / Expense

(Org Savings subtracted)

|

YTD

Adopted Budget Amendments

(Income) / Expense

|

YTD

Impact

(Organisational Savings Subtracted)

|

|

Executive

- Total

|

0

|

11,000

|

25,000

|

(14,000)

|

|

(14,000)

|

|

Corporate

Services - Total

|

0

|

(75,344)

|

(70,528)

|

(4,816)

|

|

(4,816)

|

|

Development

and Community- Total

|

0

|

(48,790)

|

(57,700)

|

8,910

|

|

8,910

|

|

Infrastructure

Services - Total

|

0

|

32,741

|

103,228

|

(70,487)

|

|

(70,487)

|

|

Impact

of Council approved budget amendments

|

0

|

0

|

0

|

0

|

207,628

|

207,628

|

|

Net

impact of Organisation Savings/Expenditure

|

0

|

0

|

0

|

0

|

|

0

|

|

|

|

|

0,000*

|

(80,393)

|

0

|

(80,393)

|

207,628†

|

127,235

|

CONSULTATION

All amendments have been proposed

after consultation with Executive and Responsible Officers at the Shire.

STATUTORY ENVIRONMENT

Local Government (Financial Management) Regulation 1996

r33A. Review of Budget

(1) Between

1 January and 31 March in each financial year a local government is to carry

out a review of its annual budget for that year.

(2A) The review of an annual budget for a

financial year must —

(a) consider the local

government’s financial performance in the period beginning on 1 July and

ending no earlier than 31 December in that financial year; and

(b) consider the local

government’s financial position as at the date of the review; and

(c) review the outcomes for the end

of that financial year that are forecast in the budget.

(2) Within

30 days after a review of the annual budget of a local government is carried

out it is to be submitted to the council.

(3) A

council is to consider a review submitted to it and is to determine* whether or

not to adopt the review, any parts of the review or any recommendations made in

the review.

*Absolute majority required.

(4) Within

30 days after a council has made a determination, a copy of the review and

determination is to be provided to the Department.

Local Government Act 1995

6.8. Expenditure from municipal fund not included in annual budget

1) A local government

is not to incur expenditure from its municipal fund for an additional purpose

except where the expenditure —

(a) is incurred in a financial year

before the adoption of the annual budget by the local government;

(b) is authorised in advance by

resolution*; or

(c) is authorised in advance by the

mayor or president in an emergency.

(1a) In subsection (1) —

“additional purpose” means a purpose for

which no expenditure estimate is included in the local government’s

annual budget.

POLICY IMPLICATIONS

2.1.1 Materiality in Financial

Reporting

It should be

noted that according to the materiality threshold set in Policy 2.1.1

Materiality in Financial Reporting, should a deficit achieve 1% of

Shire’s operating revenue ($422,176) the Shire must formulate an action

plan to remedy the over expenditure.

FINANCIAL IMPLICATIONS

The net result of the 2nd

Quarter FACR estimates is a budget deficit position of $127,235 to 30

June 2019.

RISK

The Finance and Costing Review (FACR)

seeks to provide a best estimate of the end-of-year position for the Shire of

Broome at 30 June 2019. Contained within the report are recommendations of

amendments to budgets which have financial implications on the estimate of the

end-of-year position.

The review does not, however, seek to

make amendments below the materiality threshold unless strictly necessary. The

materiality thresholds are set at $10,000 for operating budgets and $20,000 for

capital budgets. Should a number of accounts exceed their budget within these

thresholds, it poses a risk that the predicted final end-of-year position may

be understated.

In order to mitigate this risk, the

CEO enacted the FACRs to run quarterly and Executive examine each job and

account to ensure compliance. In addition, the monthly report provides variance

reporting highlighting any discrepancies against budget.

It should also be noted that should

Council decide not to adopt the recommendations, it could lead to some initiatives

being delayed or cancelled in order to offset the additional expenditure

associated with running the Shire’s operations.

STRATEGIC

IMPLICATIONS

Our People

Goal – Foster a community environment that is accessible, affordable,

inclusive, healthy and safe:

Effective communication

Affordable services and initiatives

to satisfy community need

Our

Prosperity Goal – Create the means to enable local jobs creation and

lifestyle affordability for the current and future population:

Affordable and equitable services and

infrastructure

Key economic development strategies

for the Shire which are aligned to regional outcomes working through recognised

planning and development groups/committees

Our

Organisation Goal – Continually enhance the Shire’s organisational

capacity to service the needs of a growing community:

An organisational culture that

strives for service excellence

Sustainable and integrated strategic

and operational plans

Responsible resource allocation

Improved systems, processes and

compliance

VOTING REQUIREMENTS

Absolute Majority

|

REPORT

RECOMMENDATION:

That the Audit and Risk Committee recommends that

Council:

1. Receives the

2nd Quarter Finance and Costing Review Report for the period ended 31

December 2018;

2. Adopts the

operating and capital budget amendment recommendations for the year ended 30

June 2019 as attached; and

3. Notes a

forecast end-of-year position to 30 June 2019 of a $127,235 deficit

position.

(Absolute

Majority Required)

|

Attachments

|

1.

|

2018/19 Q2 Finance and

Costing Review Report

|

|

Item 5.2 - 2ND QUARTER FINANCE AND COSTING REVIEW

2018-19

|

Agenda –

Audit and Risk Committee Meeting 12 February 2019 Page 1 of 4