Agenda – Audit and

Risk Committee Meeting 10 February 2021 Page 1 of 2

|

5.1 2nd

QUARTER FINANCE AND COSTING REVIEW 2020-21

LOCATION/ADDRESS: Nil

APPLICANT: Nil

FILE: FRE02

AUTHOR: Manager

Financial Services

CONTRIBUTOR/S: Nil

RESPONSIBLE

OFFICER: Director

Corporate Services

DISCLOSURE

OF INTEREST: Nil

|

|

SUMMARY:

The Audit and Risk Committee

is requested to consider results of the 2nd Quarter Finance and Costing

Review (FACR) of the Shire’s budget for the period ended 31 December

2020, including forecast estimates and budget recommendations to 30 June

2021.

|

BACKGROUND

Previous

Considerations

OMC 25 June 2020 Item

9.3.2

OMC 19 November 2020 Item

10.1

Quarter 2

Finance and Costing Review

The Shire of

Broome has carried out its 2nd Quarter Finance and Costing Review (FACR) for

the 2020-21 financial year. This review of the 2020-21 Annual Budget is based

on actuals and commitments for the first three months of the year from 1 July

2020 to 31 December 2021, and forecasts for the remainder of the financial

year.

This process aims

to highlight over and under expenditure of funds and over and under achievement

of income targets for the benefit of Executive and Responsible Officers to

ensure good fiscal management of their projects and programs.

Once this process

is completed, a report is compiled identifying budgets requiring amendments to

be adopted by Council. Additionally, a summary provides the financial impact of

all proposed budget amendments to the Shire of Broome’s adopted end-of-year

forecast, to assist Council to make an informed decision.

It should be

noted that the 2020-21 annual budget was adopted at the Ordinary Meeting of

Council on 25 June 2020 as a balanced budget.

COMMENT

The Quarter 2

FACR commenced on 27 January 2021. The results from this process indicate a

deficit forecast financial position to 30 June 2021 of $311,093 should Council

approve the proposed budget amendments.

The above figure represents a budget

forecast should all expenditure and income occur as expected. It does not

represent the actual end-of-year position, which can only be determined as part

of the financial year's normal annual financial processes.

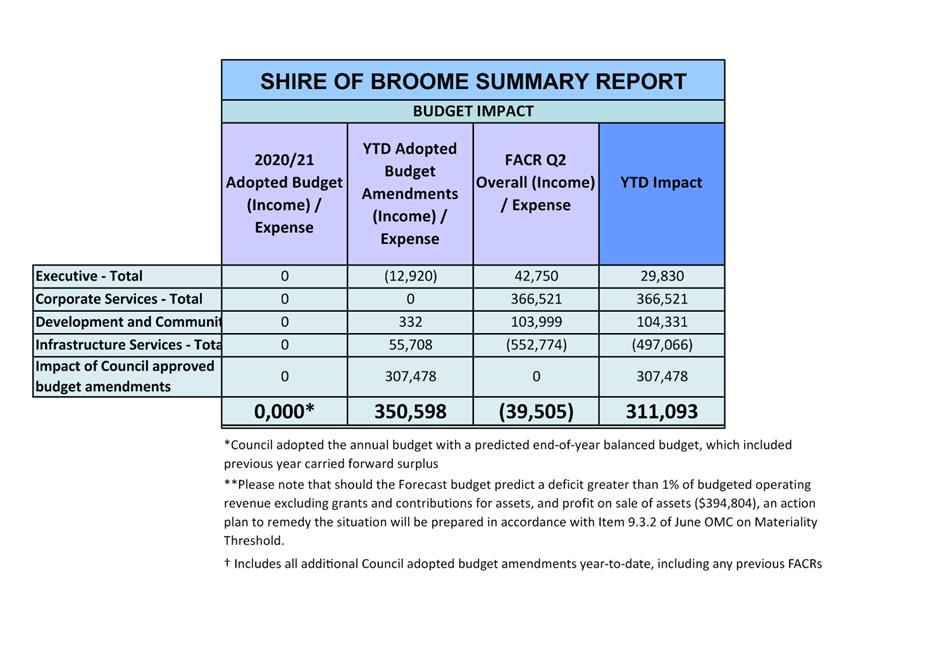

At the start of the Q2 FACR, a net

deficit of $350,598 was forecasted which arose from past budget amendments

adopted by Council, including Q1 FACR. The Q2 FACR identified net savings of

$39,505, resulting in a cumulative net deficit forecast of $311,093.

There were a total of 146 budget

amendments proposed at Q2 FACR which made up the $69,985 net surplus for the

quarter. There is no single transaction to which this net surplus is

attributed. However, the most significant amendments among these are as

follows:

· $529K net deficit

from reduced interest income on municipal funds deposit

· $584K of net

savings from the Broome Golf Club Redevelopment

· $296K of income

and expenditure for additional LRCI funding available to be utilised for the

Town Beach Carpark Construction

· $219K of

additional Blackspot funding for Gu Winckel project with a corresponding

increase in expenditure of $136K

· $160K grants

received from the ‘In The House’ grants to be utilised for Civic

Centre shows

· $100K savings from

Frederick Drainage (KBR Report) Project from undertaking the work internally.

The proposed budget amendments also

included income and expenses of equal amount totalling $2,322,544 to recognise

the transfer of Broome Motocross Complex by the Development WA to the Shire.

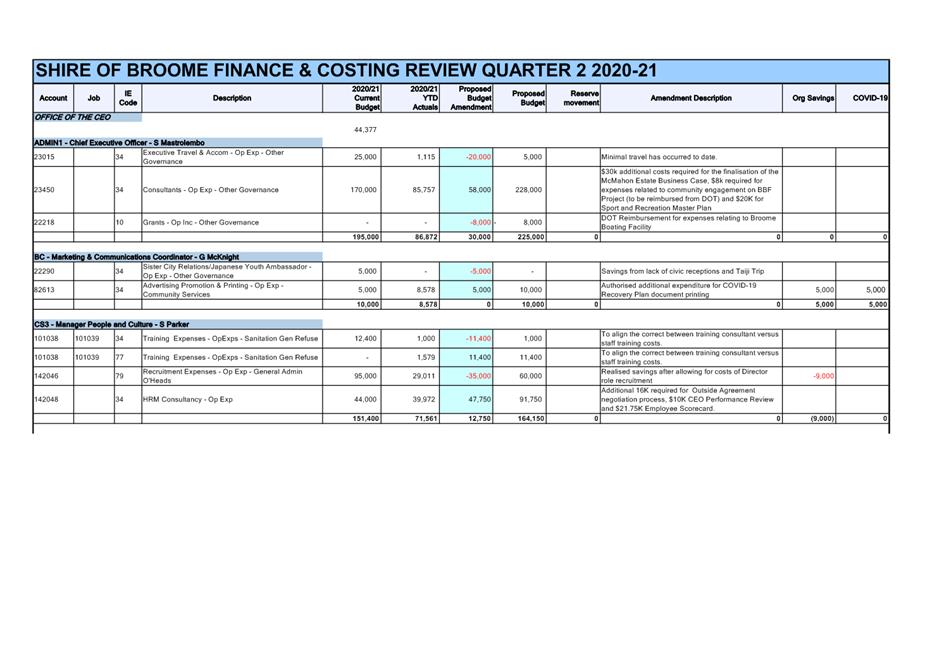

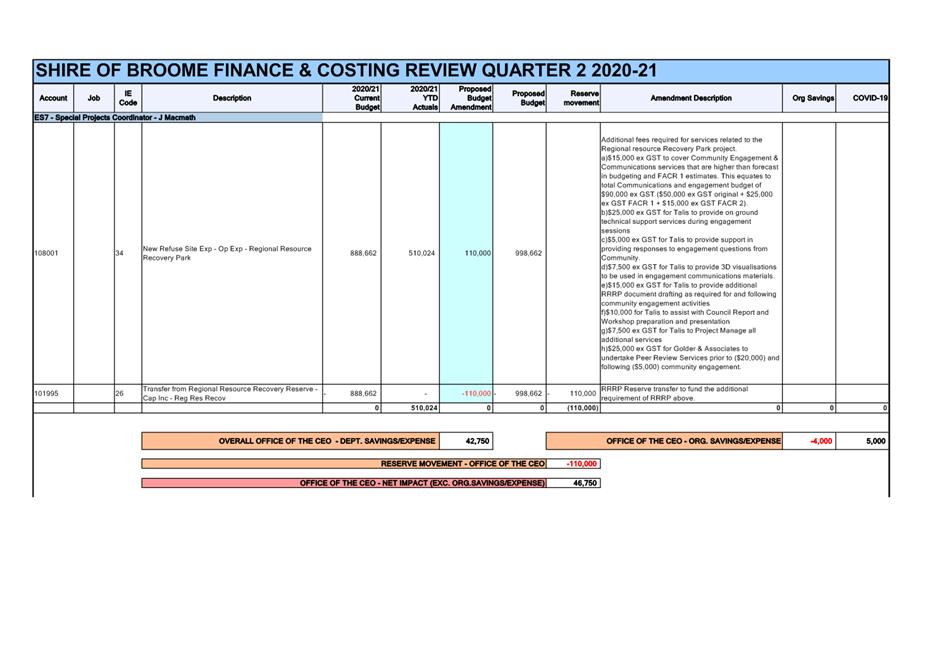

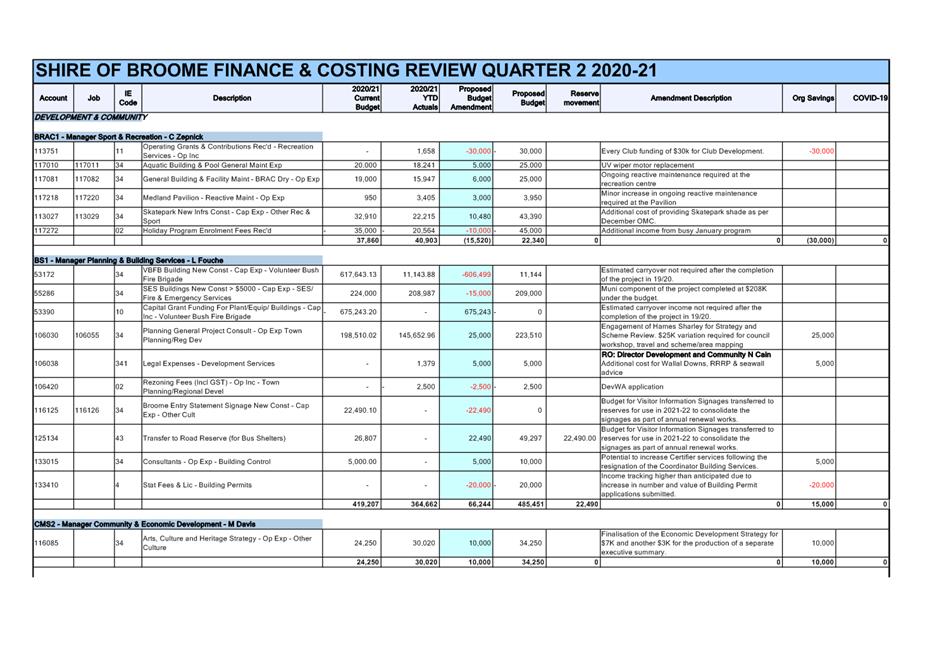

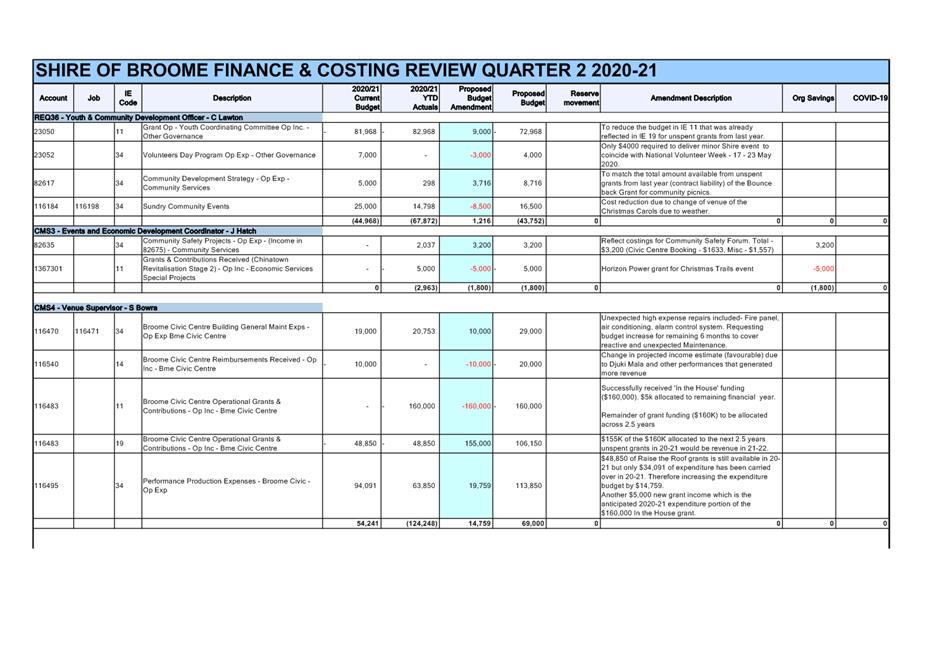

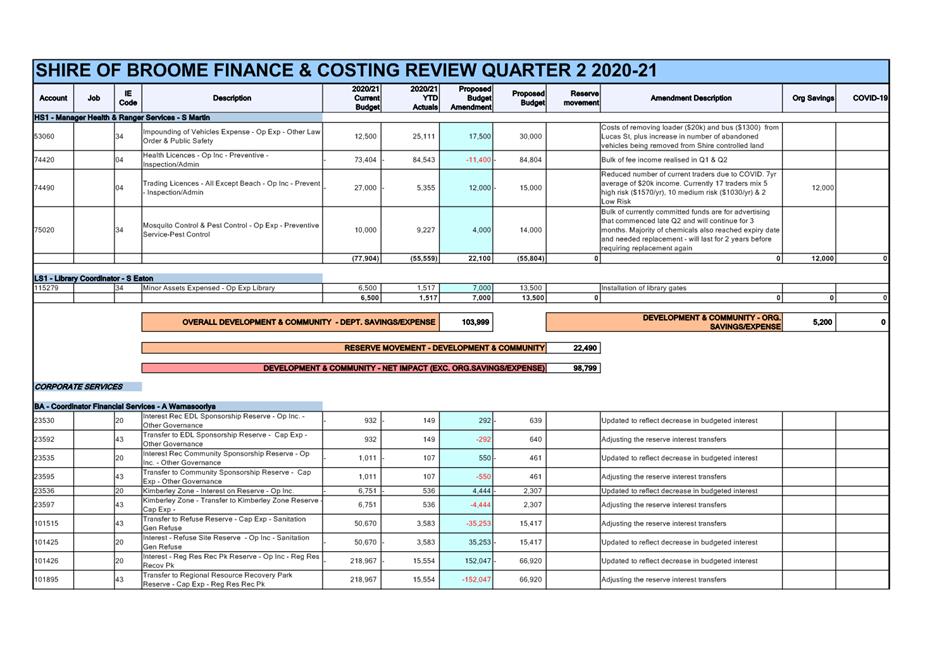

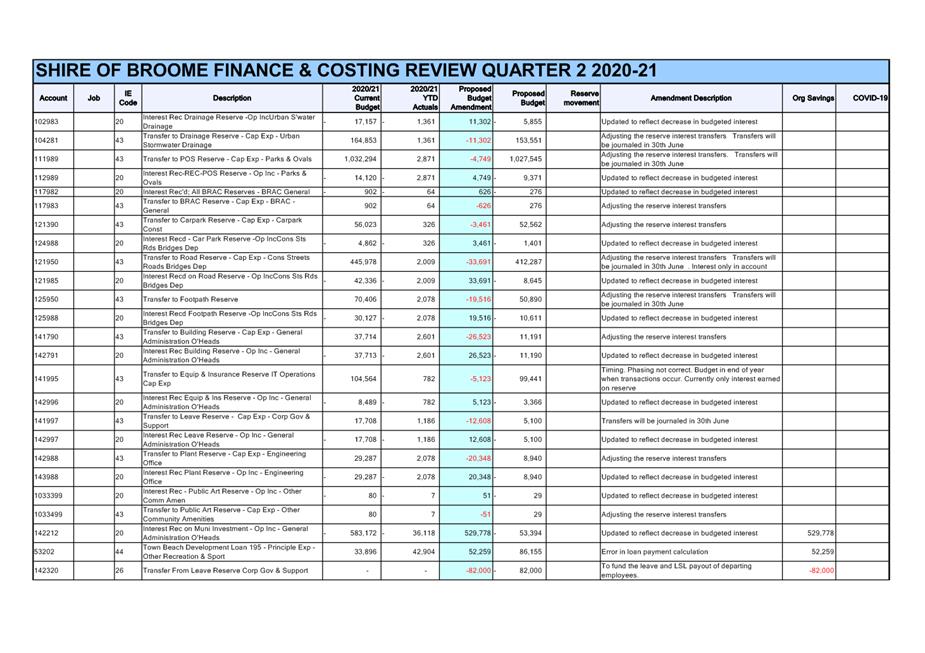

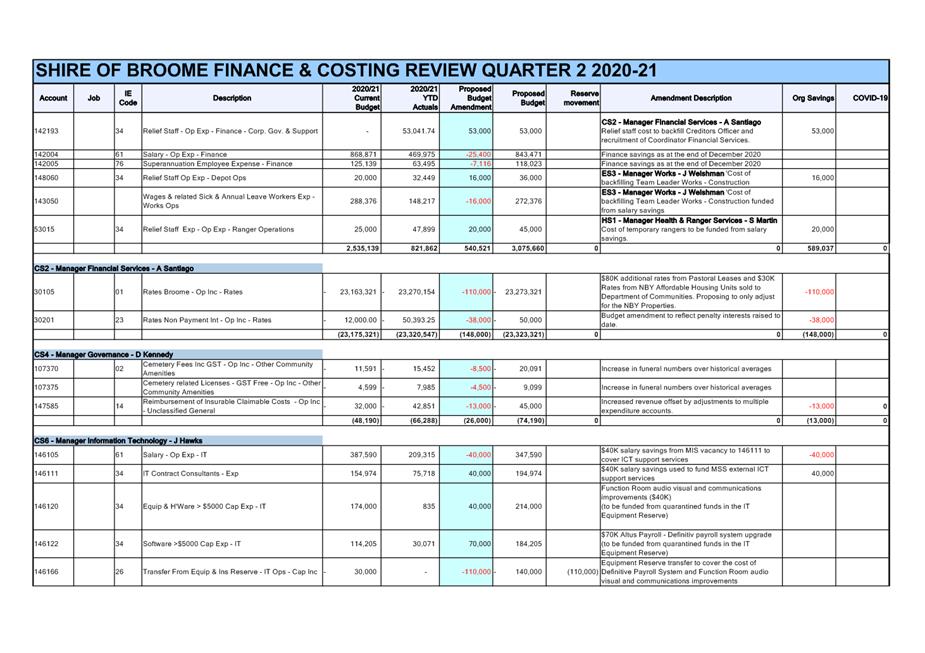

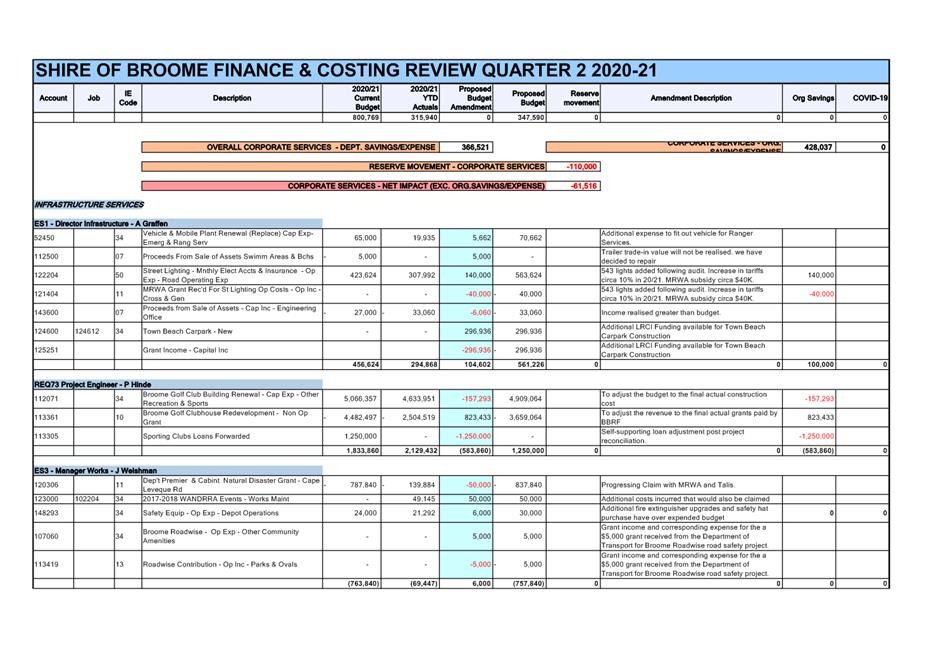

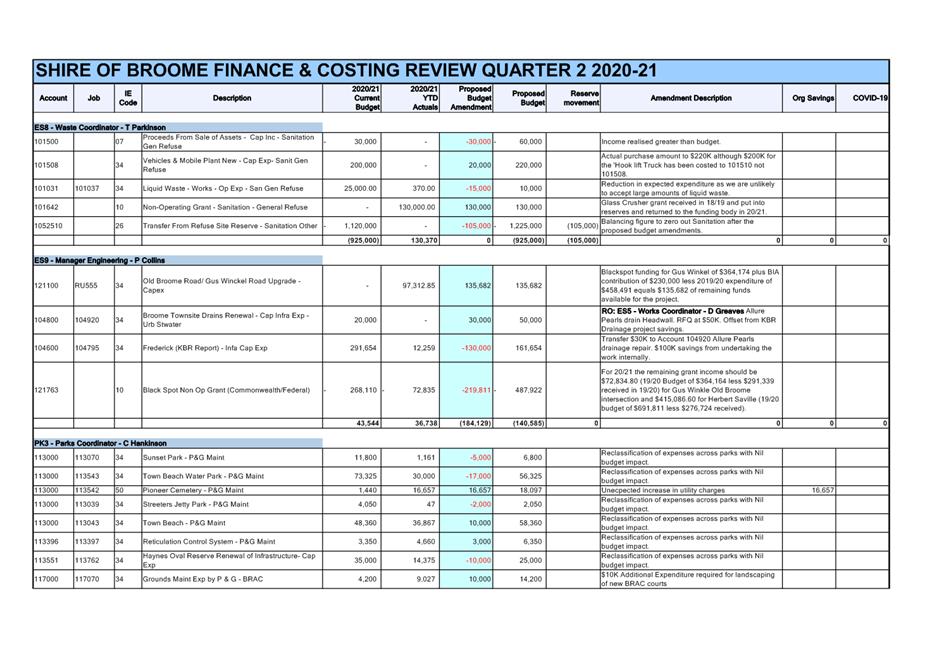

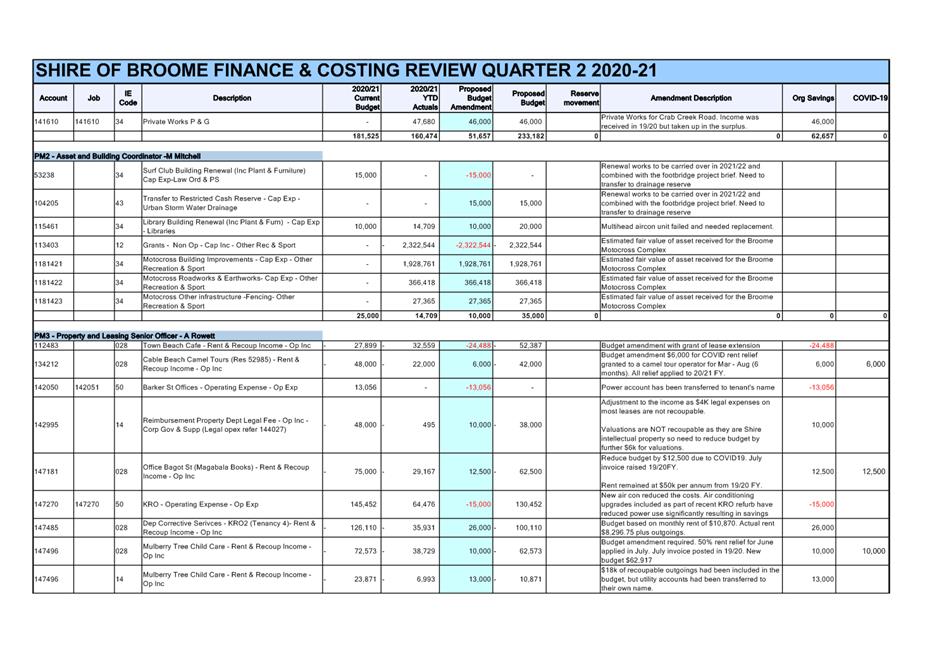

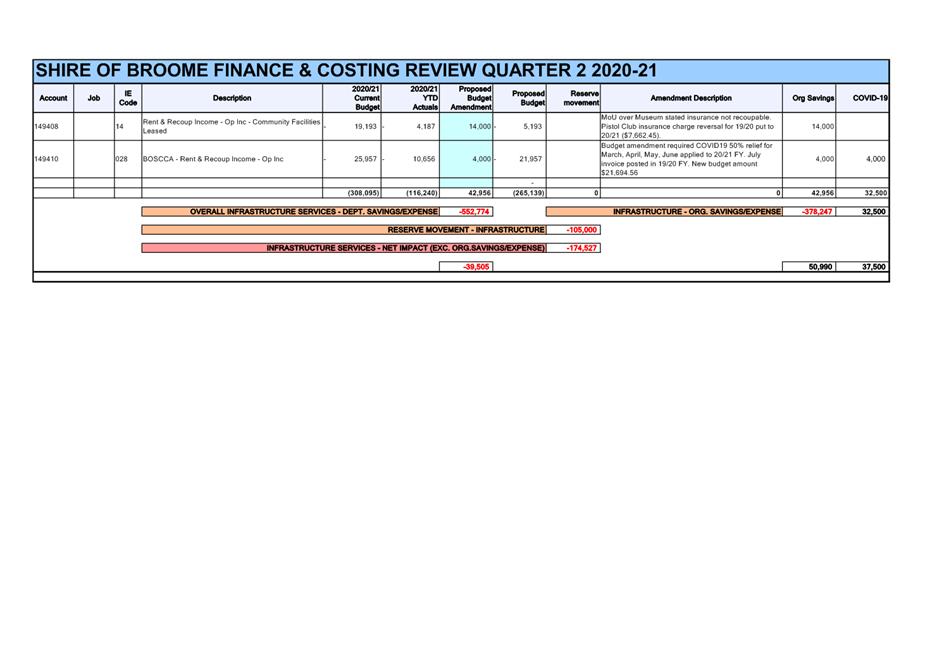

A comprehensive list of accounts

(refer to Attachment 1) has been included for perusal by the committee,

summarised by Directorate.

A summary of the results is as

follows:

|

|

|

SHIRE OF

BROOME SUMMARY REPORT

|

|

|

|

BUDGET IMPACT

|

|

|

|

2020/21 Adopted Budget

(Income) / Expense

|

YTD Adopted Budget

Amendments

(Income) / Expense

|

FACR Q2

Overall (Income) / Expense

|

YTD Impact

|

|

Executive

- Total

|

0

|

(12,920)

|

42,750

|

29,830

|

|

Corporate

Services - Total

|

0

|

0

|

366,521

|

366,521

|

|

Development

and Community- Total

|

0

|

332

|

103,999

|

104,331

|

|

Infrastructure

Services - Total

|

0

|

55,708

|

(552,774)

|

(497,066)

|

|

Impact

of Council approved budget amendments

|

0

|

307,478

|

0

|

307,478

|

|

|

|

|

0,000*

|

350,598

|

(39,505)

|

311,093

|

CONSULTATION

All amendments have been proposed

after consultation with Executive and responsible officers at the Shire.

STATUTORY ENVIRONMENT

Local Government (Financial Management) Regulation 1996

r33A. Review of Budget

(1) Between

1 January and 31 March in each financial year a local government is to carry

out a review of its annual budget for that year.

(2A) The review of an annual budget for a

financial year must —

(a) consider the local

government’s financial performance in the period beginning on 1 July and

ending no earlier than 31 December in that financial year; and

(b) consider the local

government’s financial position as at the date of the review; and

(c) review the outcomes for the end

of that financial year that are forecast in the budget.

(2) Within

30 days after a review of the annual budget of a local government is carried

out it is to be submitted to the council.

(3) A

council is to consider a review submitted to it and is to determine* whether or

not to adopt the review, any parts of the review or any recommendations made in

the review.

*Absolute majority required.

(4) Within

30 days after a council has made a determination, a copy of the review and

determination is to be provided to the Department.

Local Government Act 1995

6.8. Expenditure from municipal fund not included in annual budget

1) A local government

is not to incur expenditure from its municipal fund for an additional purpose

except where the expenditure —

(a) is incurred in a financial year

before the adoption of the annual budget by the local government;

(b) is authorised in advance by

resolution*; or

(c) is authorised in advance by the

mayor or president in an emergency.

(1a) In subsection (1) —

“additional purpose”

means a purpose for which no expenditure estimate is included in the local

government’s annual budget.

POLICY IMPLICATIONS

Nil.

It should be noted that according to

the materiality threshold set at the budget adoption, should a deficit achieve

1% of Shire’s operating revenue ($394,804) the Shire must formulate an

action plan to remedy the over expenditure.

FINANCIAL IMPLICATIONS

The net result of the Quarter

2 FACR estimates is a budget deficit position of $311,093 to 30 June

2021.

RISK

The Finance and Costing Review (FACR)

seeks to provide a best estimate of the end-of-year position for the Shire of

Broome at 30 June 2021. Contained within the report are recommendations of

amendments to budgets which have financial implications on the estimate of the

end-of-year position.

The review does not, however, seek to

make amendments below the materiality threshold unless strictly necessary. The

materiality thresholds are set at $10,000 for operating budgets and $20,000 for

capital budgets. Should a number of accounts exceed their budget within these

thresholds, it poses a risk that the predicted final end-of-year position may

be understated.

In order to mitigate this risk, the

CEO enacted the FACRs to run quarterly and Executive examine each job and

account to ensure compliance. In addition, the monthly report provides variance

reporting highlighting any discrepancies against budget.

It should also be noted that should

Council decide not to adopt the recommendations, it could lead to some initiatives

being delayed or cancelled in order to offset the additional expenditure

associated with running the Shire’s operations.

STRATEGIC

IMPLICATIONS

Our

Organisation Goal – Continually enhance the Shire’s organisational

capacity to service the needs of a growing community:

Responsible resource allocation

Improved systems, processes and

compliance

VOTING REQUIREMENTS

Absolute Majority

|

REPORT RECOMMENDATION:

That the Audit and Risk Committee recommends that

Council:

1. Receives the Quarter

2 Finance and Costing Review Report for the period ended 31 December 2020;

2. Adopts the

operating and capital budget amendment recommendations for the year ended 30

June 2021 as attached; and

3. Notes a

forecast end-of-year position to 30 June 2021 of $311,093 deficit

position.

|

Attachments

|

1.

|

2020-2021 Quarter 2

Finance and Costing Review

|