Our Vision

"Broome - a future for everyone."

AGENDA

FOR THE

Audit and Risk Committee Meeting

19 April 2021

Our Vision

"Broome - a future for everyone."

AGENDA

FOR THE

Audit and Risk Committee Meeting

19 April 2021

NOTICE OF MEETING

Dear Council Member,

The next Audit and Risk Committee of Council will be held on Monday, 19 April 2021 in the Committee Room, Corner Weld and Haas Streets, Broome, commencing at 2:00 PM.

Regards,

![]()

S MASTROLEMBO

Chief Executive Officer

16/04/2021

Our Mission

"To deliver affordable and quality Local Government services."

DISCLAIMER

The purpose of Council Meetings is to discuss, and where possible, make resolutions about items appearing on the agenda. Whilst Council has the power to resolve such items and may in fact, appear to have done so at the meeting, no person should rely on or act on the basis of such decision or on any advice or information provided by a Member or Officer, or on the content of any discussion occurring, during the course of the meeting.

Persons should be aware that the provisions in section 5.25 of the Local Government Act 1995 establish procedures for revocation or rescission of a Council decision. No person should rely on the decisions made by Council until formal advice of the Council decision is received by that person. The Shire of Broome expressly disclaims liability for any loss or damage suffered by any person as a result of relying on or acting on the basis of any resolution of Council, or any advice or information provided by a Member or Officer, or the content of any discussion occurring, during the course of the Council meeting.

Should you require this document in an alternative format please contact us.

Agenda – Audit and Risk Committee Meeting 19 April 2021 Page 1 of 2

SHIRE OF BROOME

Audit and Risk Committee Meeting

Monday 19 April 2021

INDEX – Agenda

3. Declarations Of Financial Interest / Impartiality

5.1 3RD QUARTER FINANCE AND COSTING REVIEW 2020-21

5.2 RISK MANAGEMENT POLICY REVIEW AND UPDATE

Agenda – Audit and Risk Committee Meeting 19 April 2021 Page 1 of 2

|

That the Minutes of the Audit and Risk Committee held on 10 February 2021, as published and circulated, be confirmed as a true and accurate record of that meeting.

|

Agenda – Audit and Risk Committee Meeting 19 April 2021 Page 1 of 2

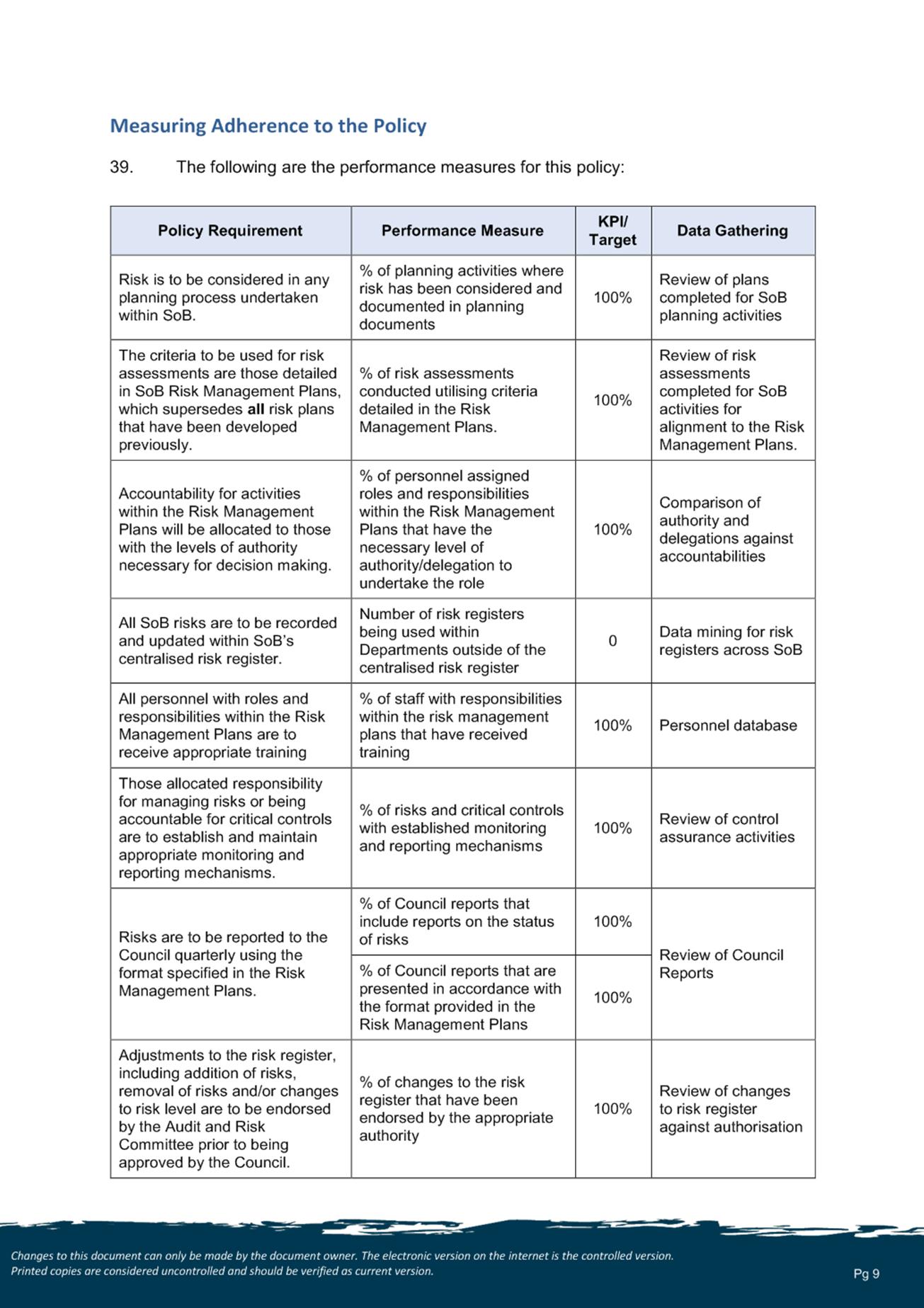

|

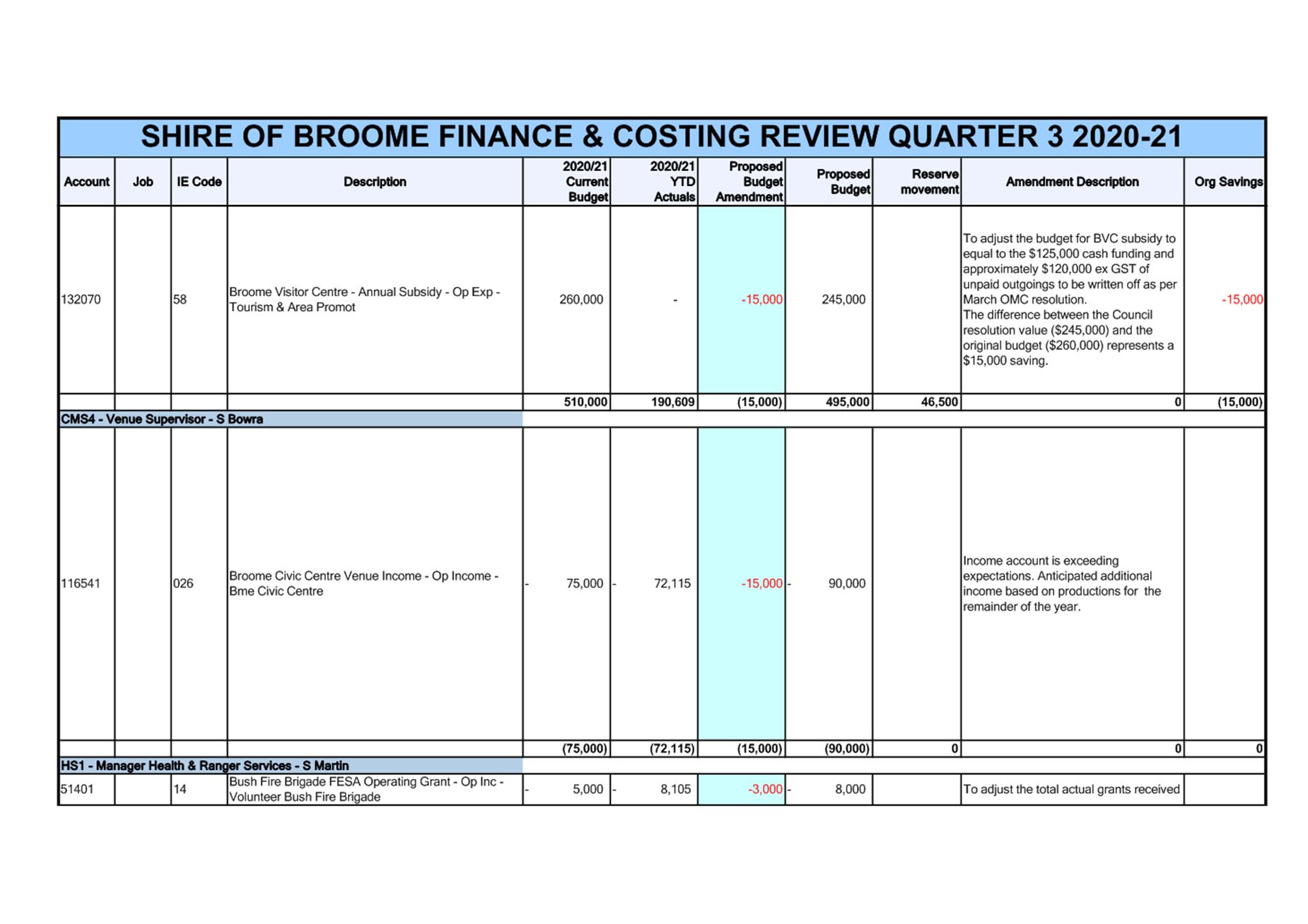

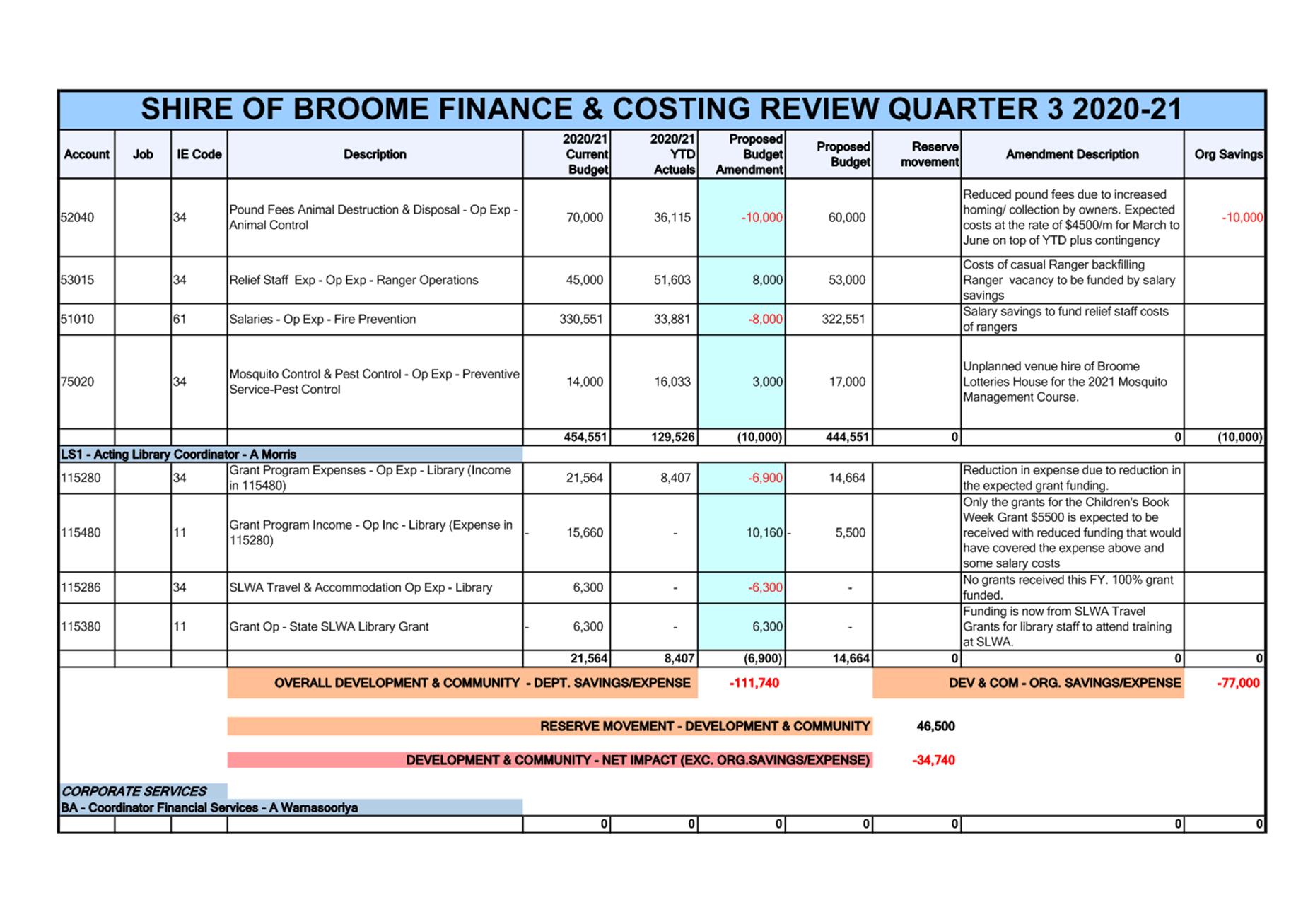

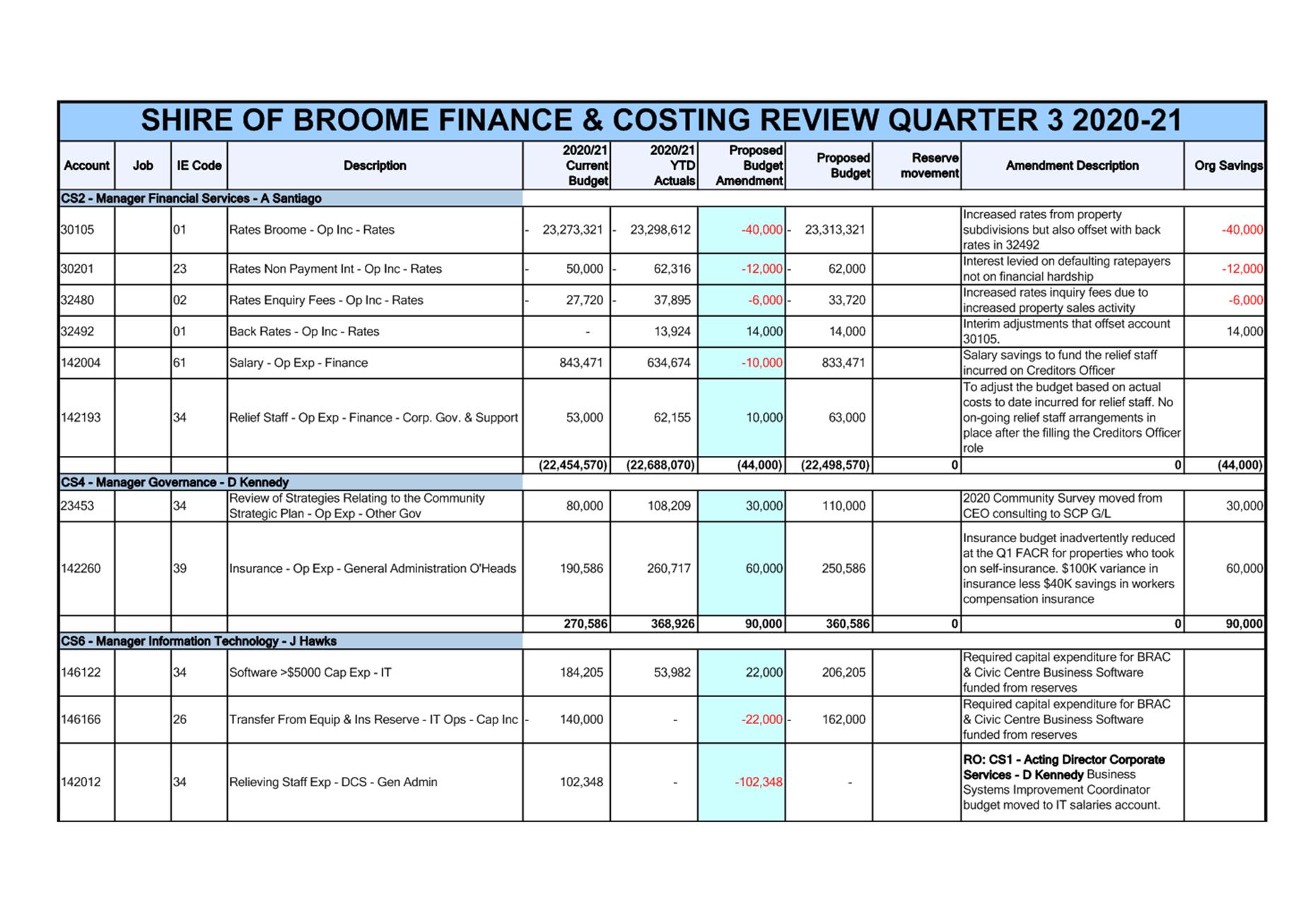

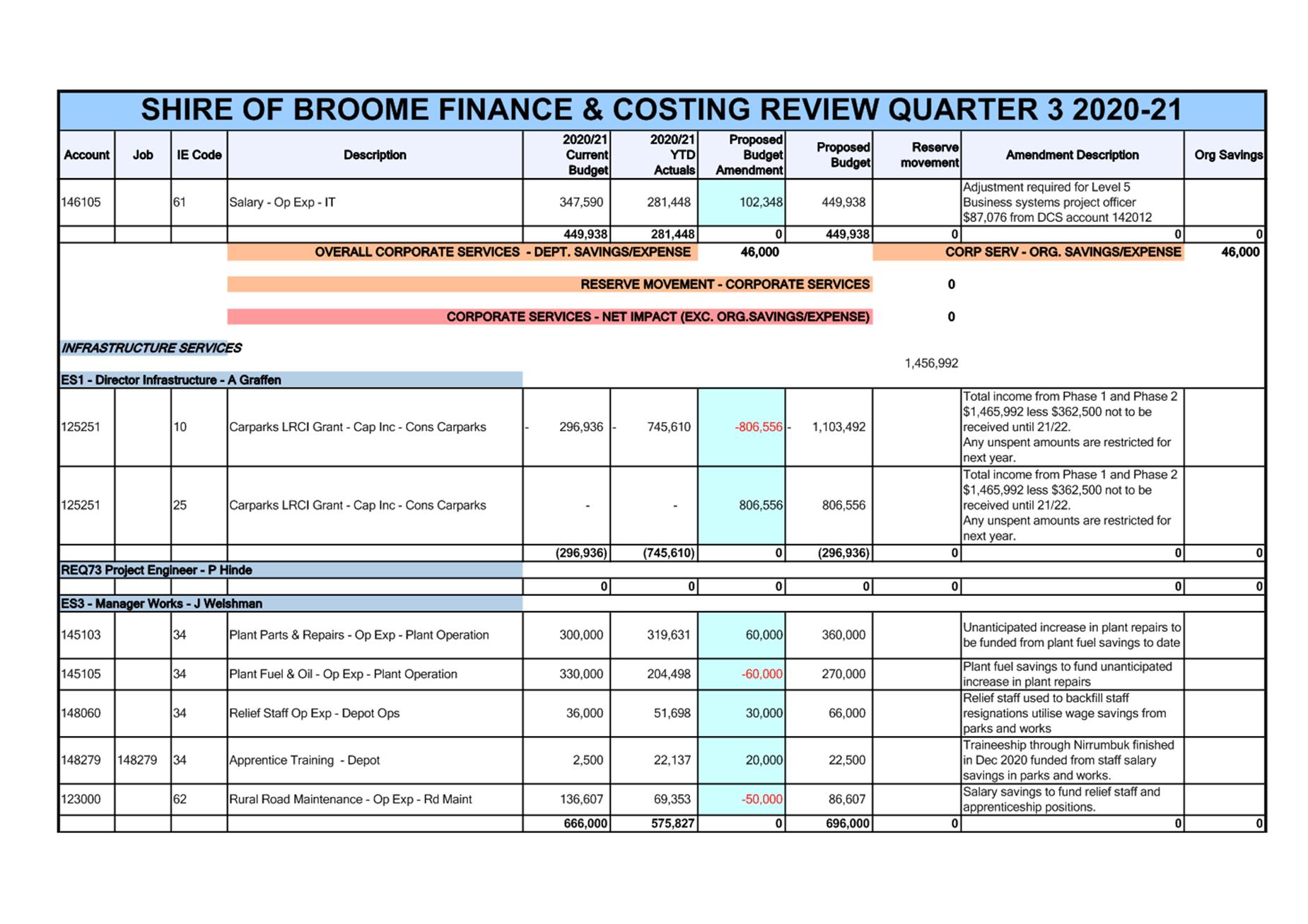

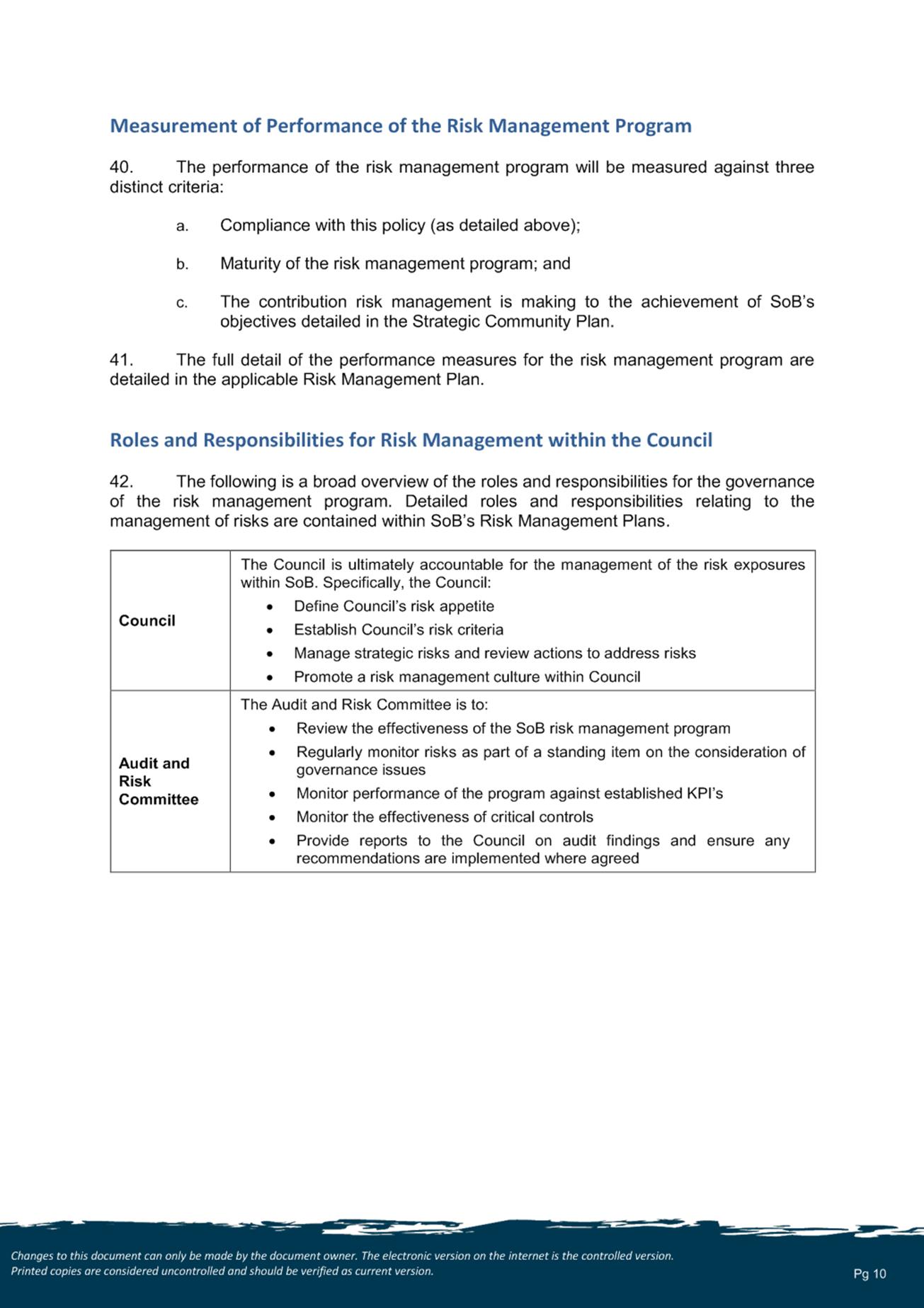

SUMMARY: The Audit and Risk Committee is requested to consider results of the 3rd Quarter Finance and Costing Review (FACR) of the Shire’s budget for the period ended 31 March 2021, including forecast estimates and budget recommendations to 30 June 2021. |

BACKGROUND

Previous Considerations

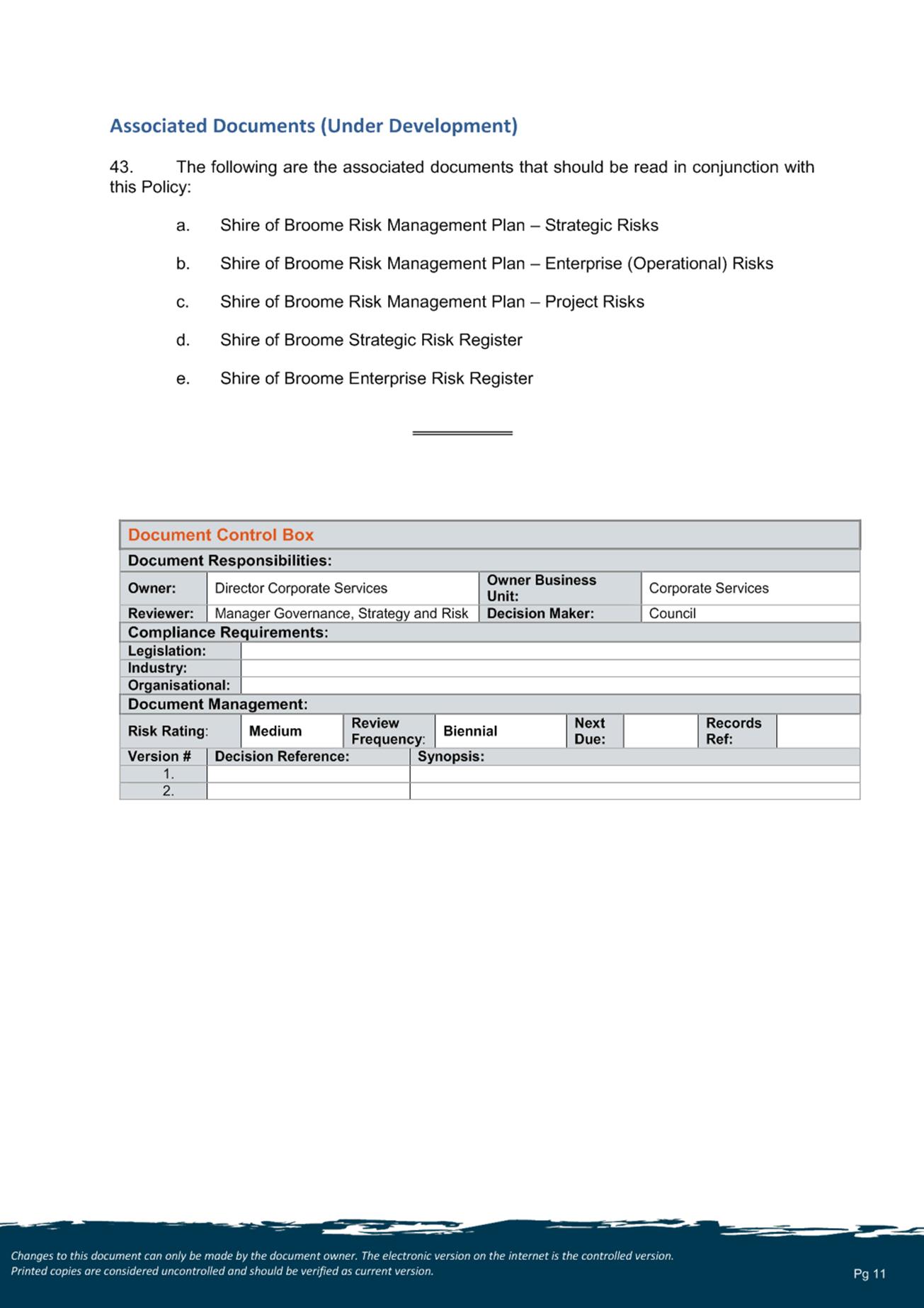

OMC 25 June 2020 Item 9.3.2

OMC 19 November 2020 Item 10.1

OMC 25 February 2021 Item 9.4.8

Quarter 3 Finance and Costing Review

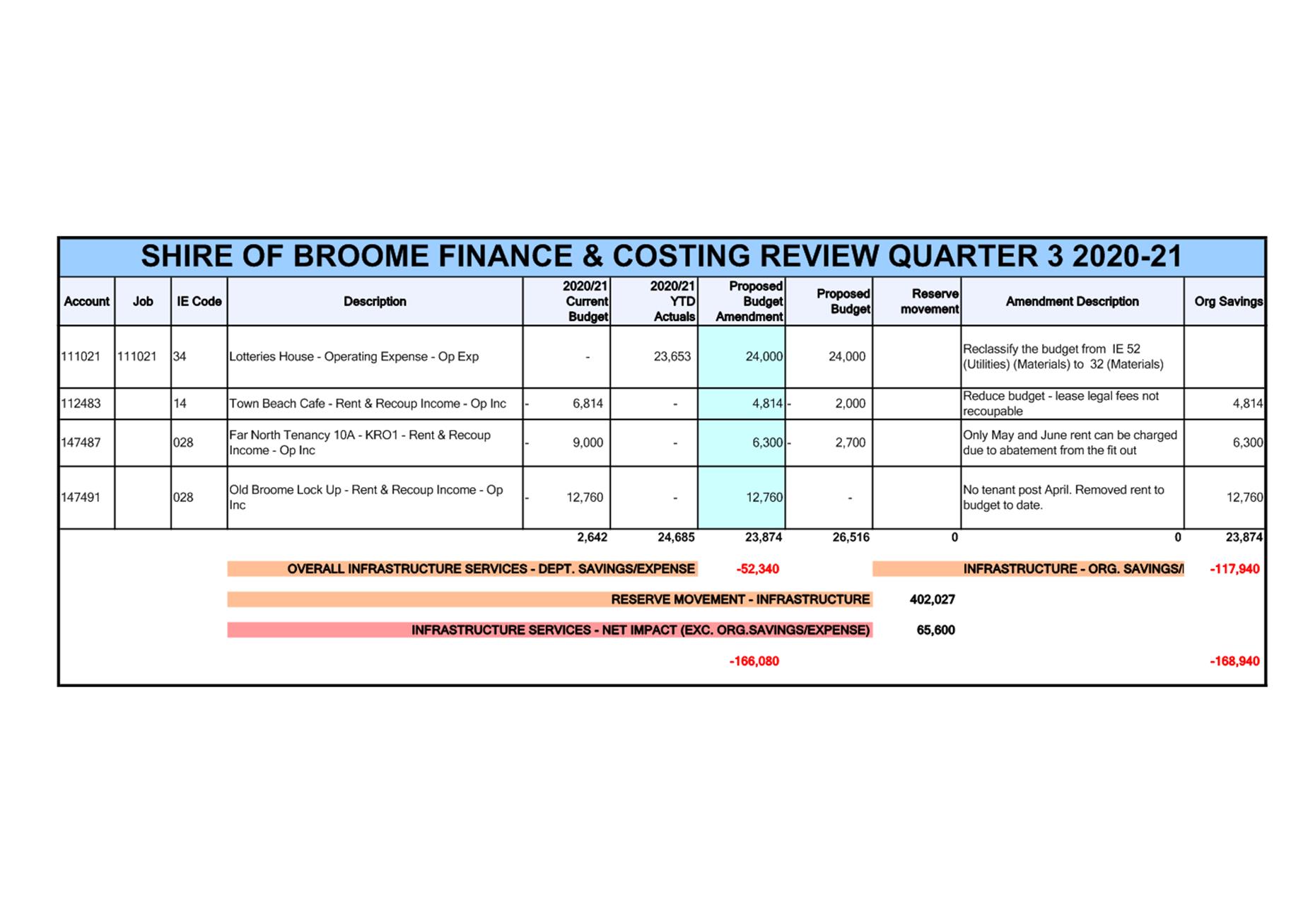

The Shire of Broome has carried out its 3rd Quarter FACR for the 2020-21 financial year. This review of the 2020-21 Annual Budget is based on actuals and commitments for the nine months ending 31 March 2021, and forecasts for the remainder of the financial year.

The FACR aims to highlight over and under expenditure of funds and over and under achievement of income targets for the benefit of Executive and Responsible Officers to ensure good fiscal management of their projects and programs.

Once this process is completed, a report is compiled identifying budgets requiring amendments to be adopted by Council. Additionally, a summary provides the financial impact of all proposed budget amendments to the Shire of Broome’s adopted end-of-year forecast, to assist Council to make an informed decision.

It should be noted that the 2020-21 annual budget was adopted at the Ordinary Meeting of Council on 25 June 2020 as a balanced budget.

COMMENT

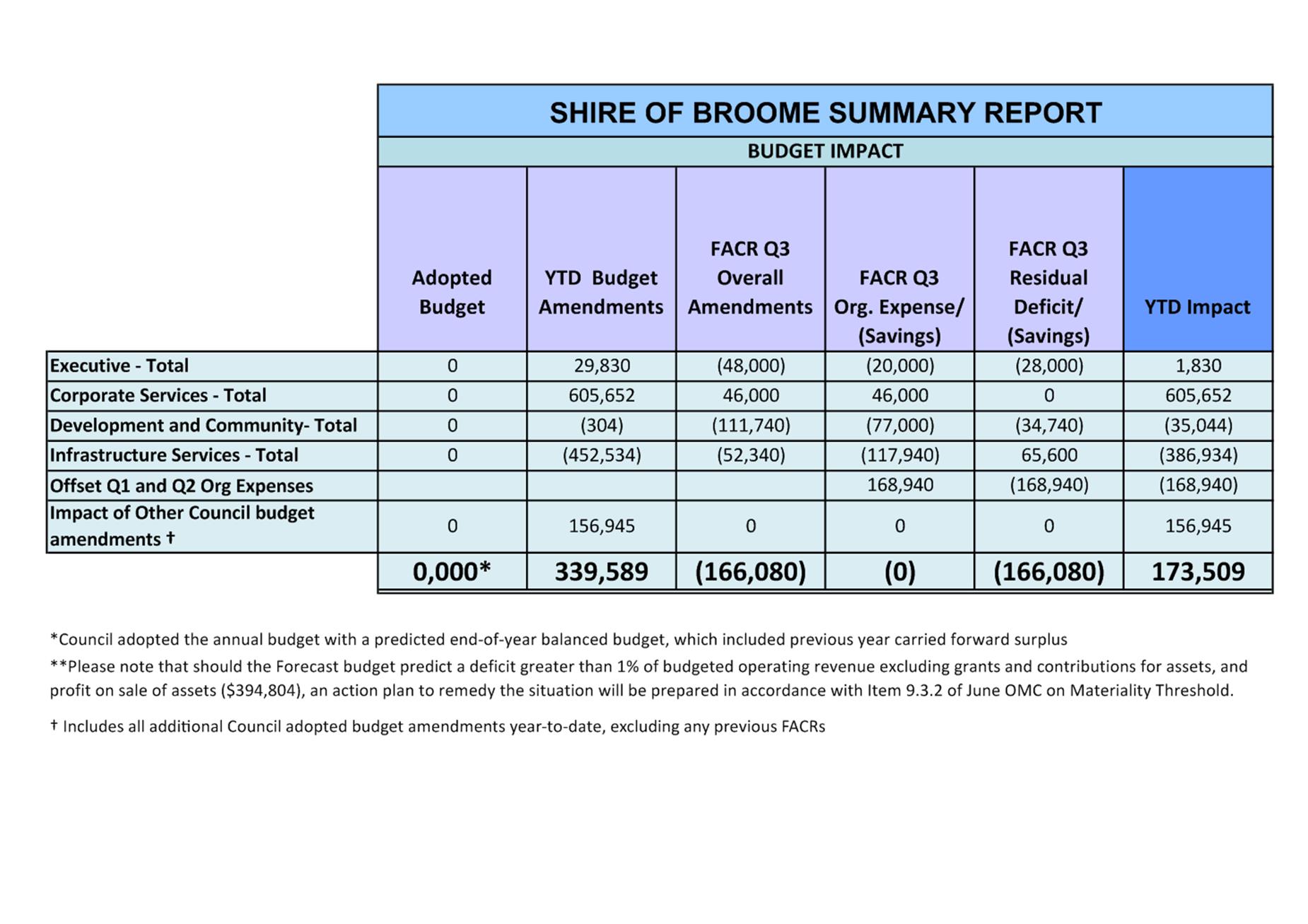

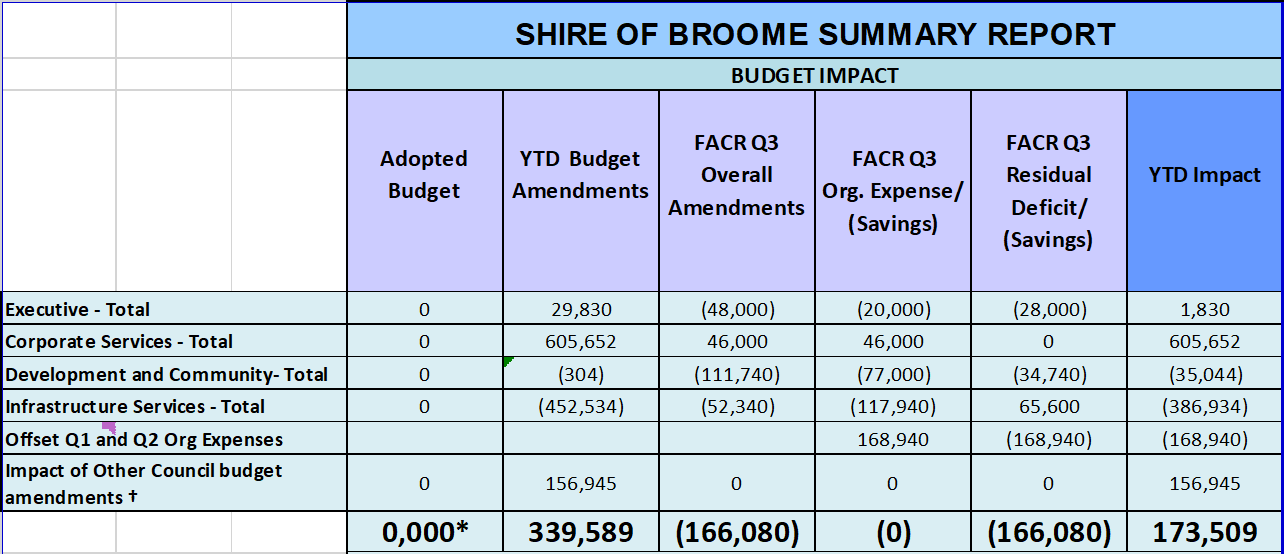

The Quarter 3 FACR occurred on 8 April 2021. The results from this process indicated a forecast deficit financial position to 30 June 2021 of $173,509 should Council approve the proposed budget amendments. This is down $166,080 from the Q2 FACR forecast net deficit of $339,589.

The above figure represents a budget forecast should all expenditure and income occur as expected. It does not represent the actual end-of-year position, which can only be determined as part of the financial year’s normal annual financial processes.

Management will focus on controlling the forecast deficit and is confident that through strong financial management and controls the deficit can be addressed by June 30.

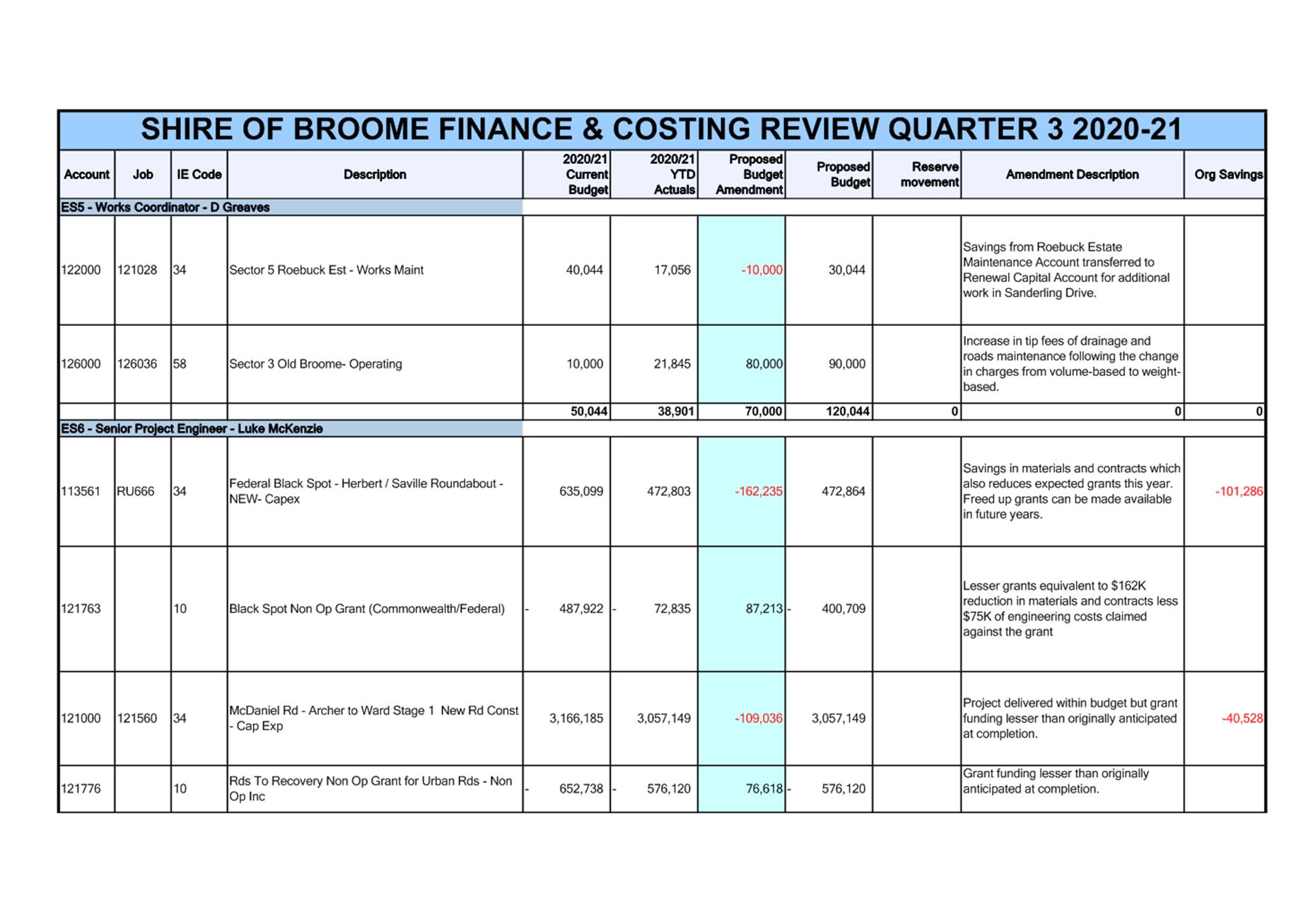

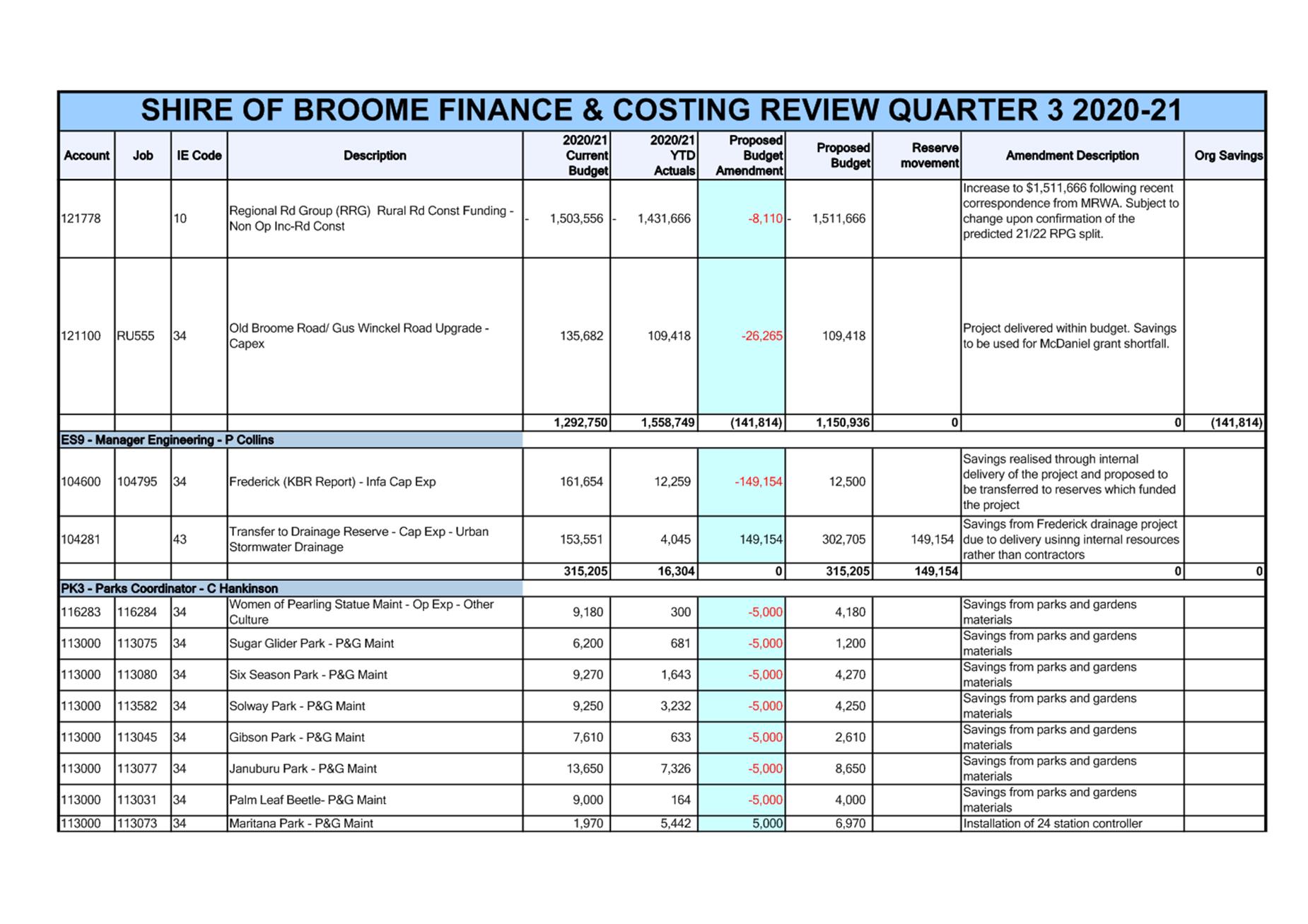

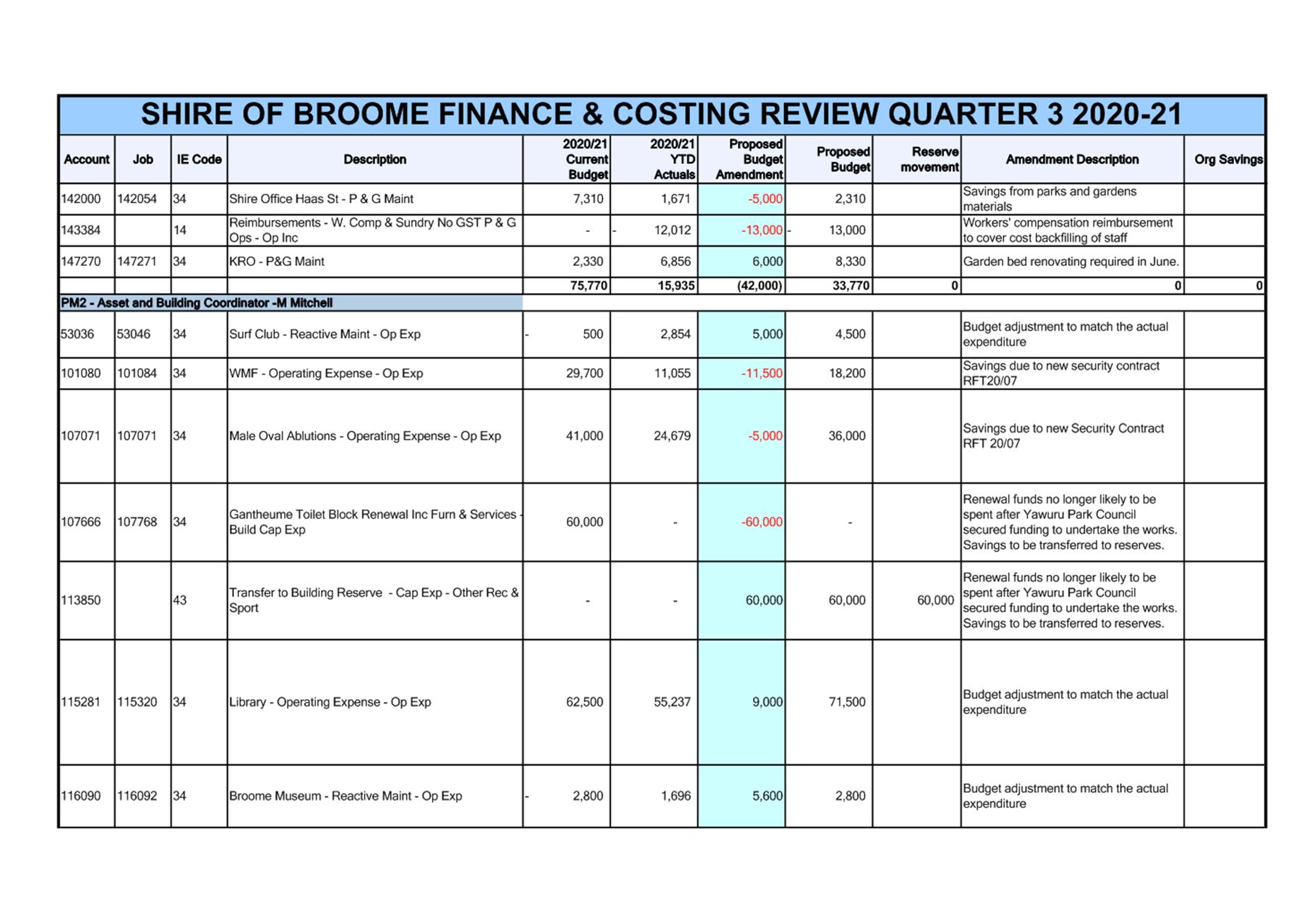

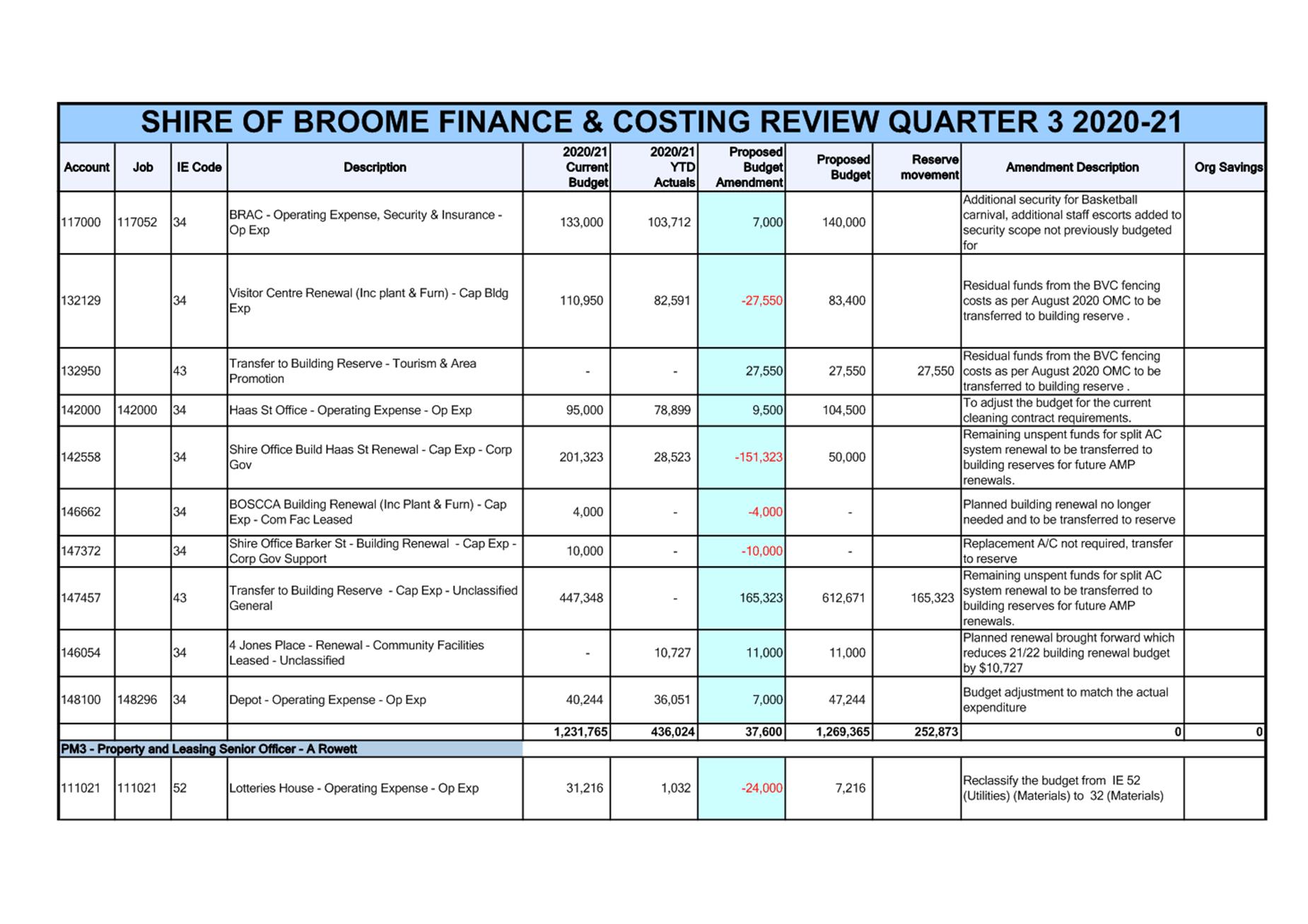

A comprehensive list of accounts (refer to Attachment 1) has been included for perusal by the committee, summarised by Directorate.

A summary of the results is as follows:

|

Income Items |

Deficit/(Surplus) |

|

Fees & Charges Levied Rec'd |

(165,940) |

|

Other Revenue Rec'd |

(26,186) |

|

Transfer From Reserves (Cap Accts) |

(22,000) |

|

Interest Rec'd From All Sources |

(12,000) |

|

Operating Grants, Subsidies, Contributions, & Reimb Rec'd |

16,460 |

|

Non Operating Grants & Subsidies Rec'd |

155,721 |

|

|

|

|

Expense Items |

|

|

Materials & Contracts |

(684,510) |

|

Utilities Expenses |

(24,000) |

|

Other Expenses |

13,500 |

|

Insurance Exps (Not Workers Comp) |

60,000 |

|

Employee Exps (Inc Workers Comp, Excl. Overheads) |

74,348 |

|

Transfer to Reserve (Cap Accts) |

448,527 |

|

Net Deficit/(Surplus) |

(166,080) |

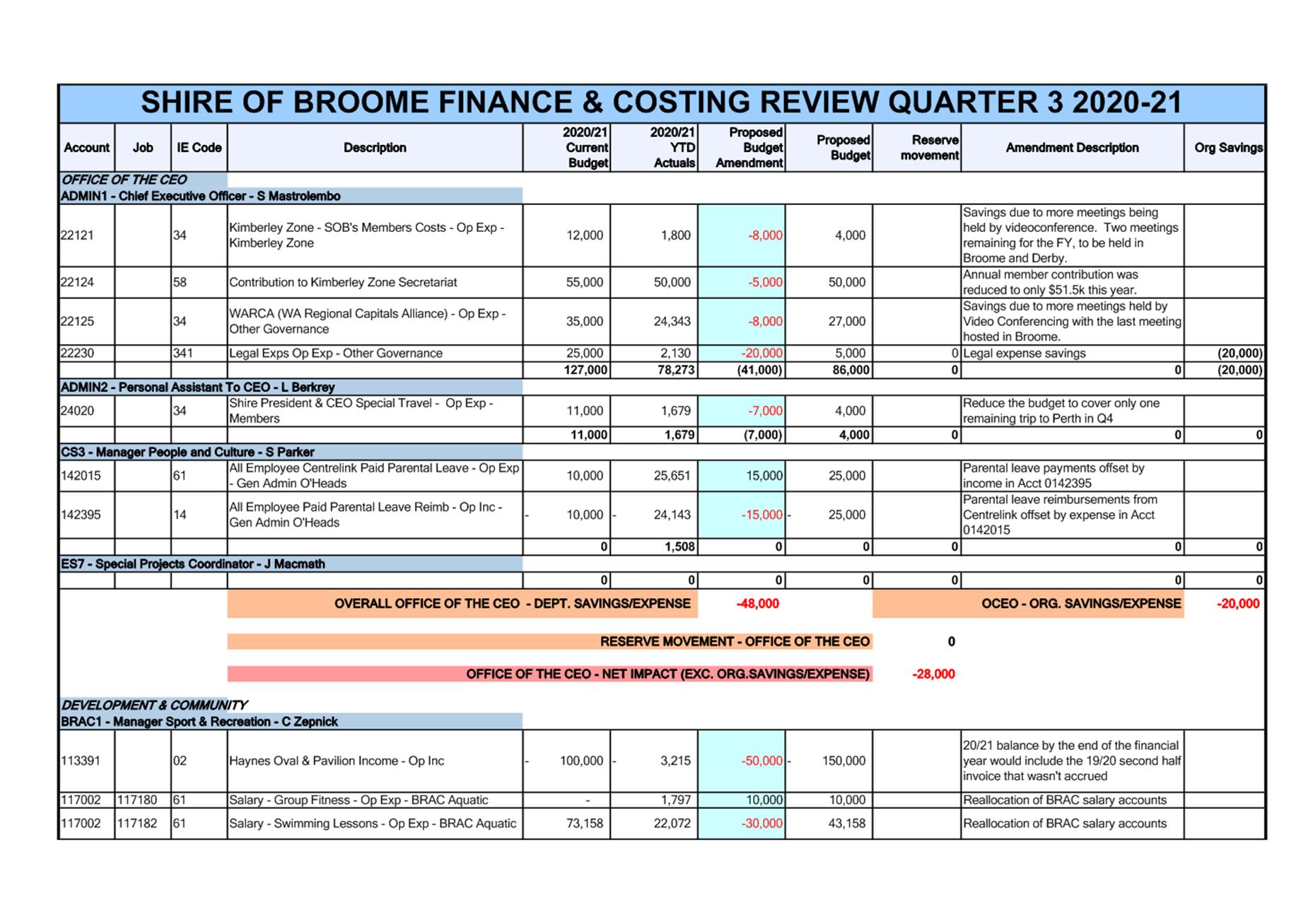

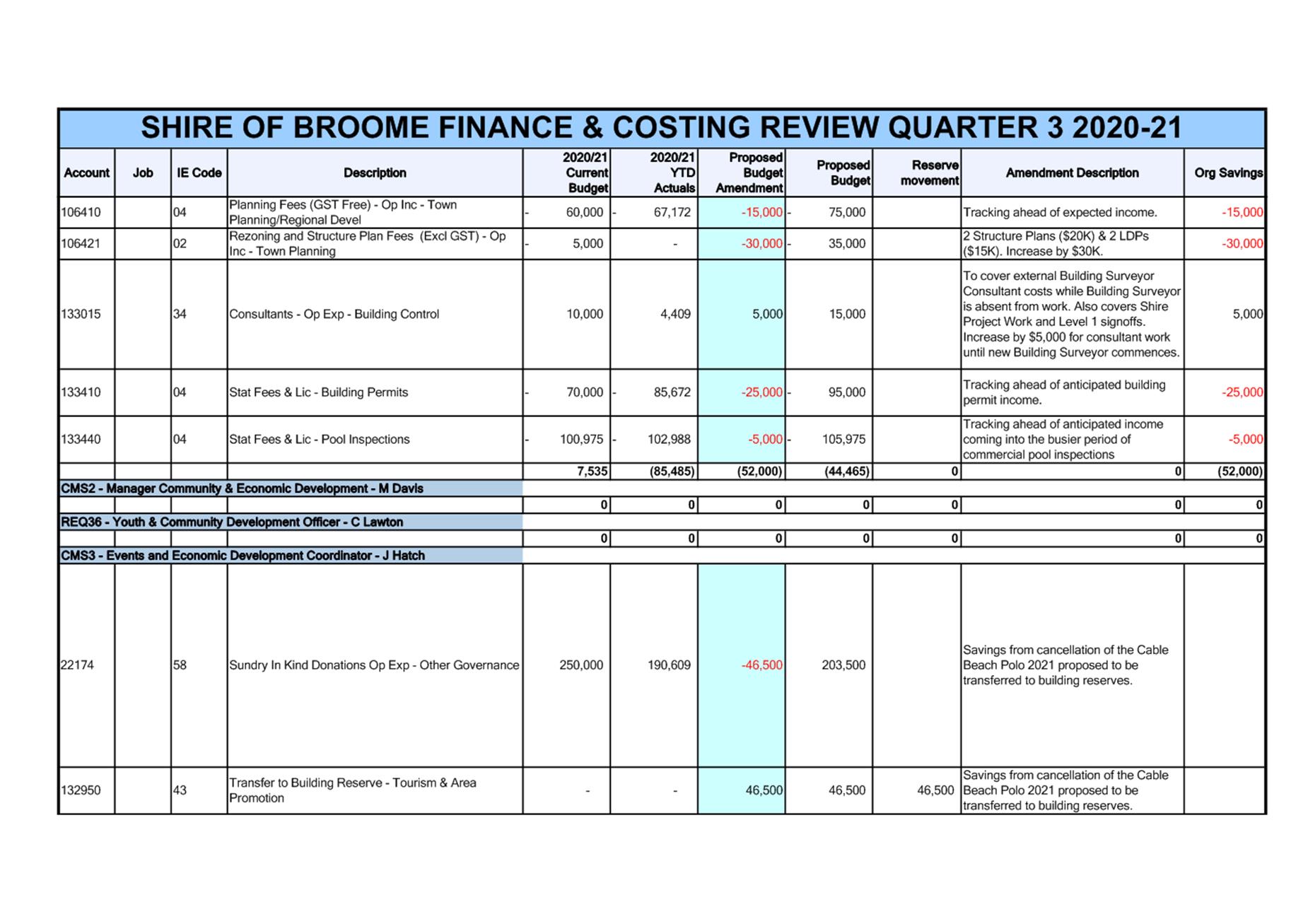

A total of 107 budget amendments were proposed at Q3 FACR, which made up the $166,080 net surplus for the quarter. There is no single transaction to which this net surplus is attributed. However, the most significant amendments among these are as follows:

Income Items

· $165K net increase in fees and charges revenue due to additional interim rates, building and planning fees from increased subdivisions and residential property improvements. Sport and recreation fees are also expected to increase, leading to the sporting season.

· $26K increase in other revenue due to workers’ compensation and government parental leave reimbursements

· $22K reserve transferred in to fund the BRAC and Civic Centre improved business systems

· $12K reduction in operating grants expected to be received from the State Library due to change in the funding structure

· $155K reduction in capital grants for McDaniel and Herbert-Saville roundabout projects upon completing the projects at a lower total cost

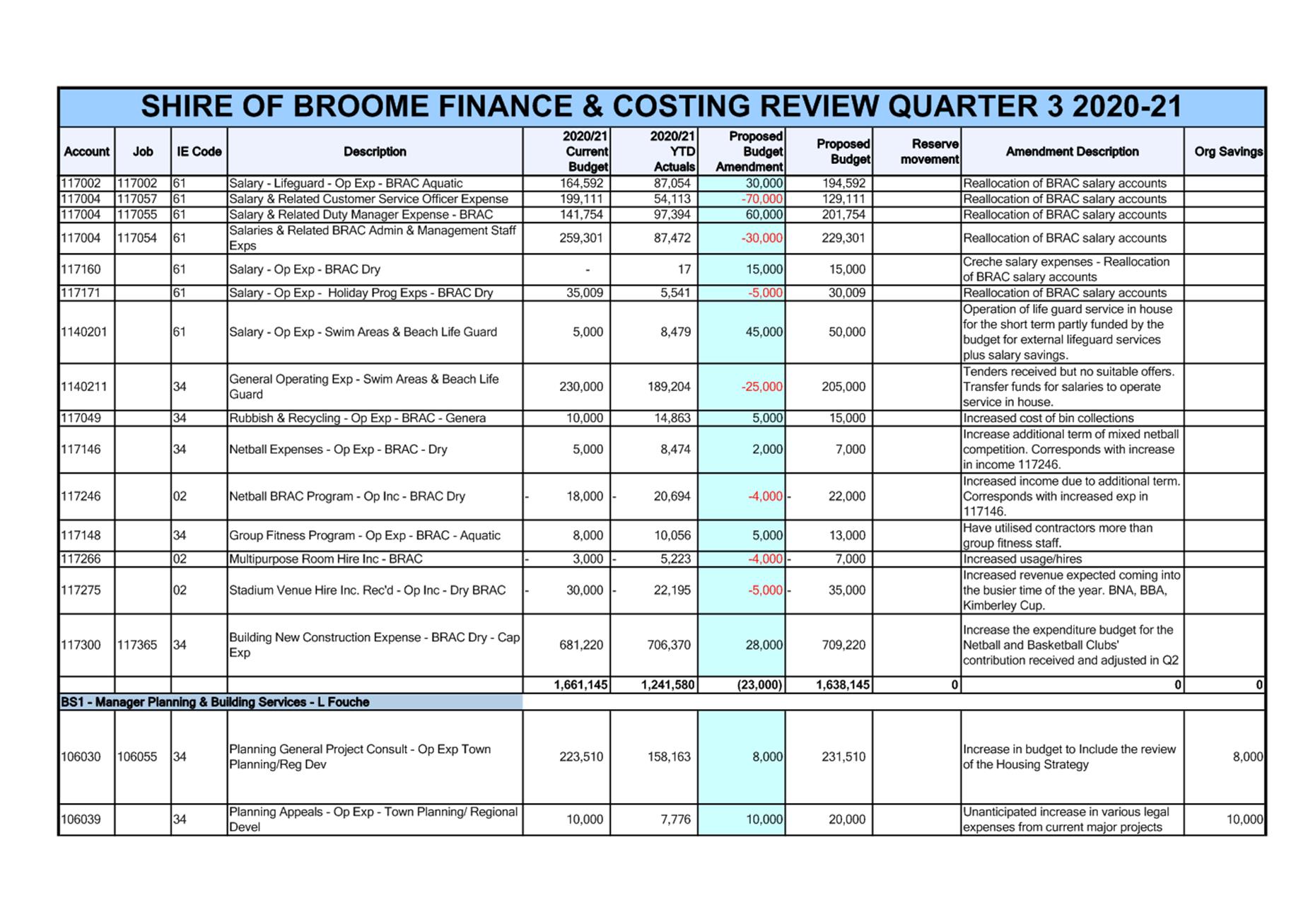

Expense Items

· $155K reduction in capital grants for Herbert-Saville and McDaniel projects

· $685K net savings in materials and contracts

o $271K savings from Herbert-Saville and McDaniel

o $165K Air Conditioner renewals transferred to reserves

o $150K Frederick Street drainage savings transferred to reserves

· $24K savings to date in power and water charges

· $13K net increase in other expenses due to $80K increase in tip fees despite $66K savings in various community sponsorship expenditure for Cable Beach Polo and Broome Visitor Centre

· $60K increase in insurance due to increase in reinsurance rates of assets above the 26th parallel, insurance for new infrastructure and property together with increased declared values of the Shire’s fleet

· $74K increase in employment costs (funded from relief staff budget).

· $449K additional transfer to reserves from savings from Air Conditioner Renewals and Frederick Street drainage work.

CONSULTATION

All amendments have been proposed after consultation with Executive and responsible officers at the Shire.

STATUTORY ENVIRONMENT

Local Government (Financial Management) Regulation 1996

r33A. Review of Budget

(1) Between 1 January and 31 March in each financial year a local government is to carry out a review of its annual budget for that year.

(2A) The review of an annual budget for a financial year must —

(a) consider the local government’s financial performance in the period beginning on 1 July and ending no earlier than 31 December in that financial year; and

(b) consider the local government’s financial position as at the date of the review; and

(c) review the outcomes for the end of that financial year that are forecast in the budget.

(2) Within 30 days after a review of the annual budget of a local government is carried out it is to be submitted to the Council.

(3) A council is to consider a review submitted to it and is to determine* whether or not to adopt the review, any parts of the review or any recommendations made in the review.

*Absolute majority required.

(4) Within 30 days after a council has made a determination, a copy of the review and determination is to be provided to the Department.

Local Government Act 1995

6.8. Expenditure from municipal fund not included in annual budget

1) A local government is not to incur expenditure from its municipal fund for an additional purpose except where the expenditure —

(a) is incurred in a financial year before the adoption of the annual budget by the local government;

(b) is authorised in advance by resolution*; or

(c) is authorised in advance by the mayor or president in an emergency.

(1a) In subsection (1) —

“additional purpose” means a purpose for which no expenditure estimate is included in the local government’s annual budget.

POLICY IMPLICATIONS

Nil.

It should be noted that according to the materiality threshold set at the budget adoption, should a deficit achieve 1% of Shire’s operating revenue ($394,804) the Shire must formulate an action plan to remedy the over expenditure.

FINANCIAL IMPLICATIONS

The Quarter 3 FACR estimated net result is a budget deficit position of $173,509 to 30 June 2021.

RISK

The Finance and Costing Review (FACR) seeks to provide the best estimate of the end-of-year position for the Shire of Broome at 30 June 2021. The report contains recommendations of amendments to budgets that have financial implications on the estimate of the end-of-year position.

The review does not, however, seek to make amendments below the materiality threshold unless strictly necessary. The materiality thresholds are set at $10,000 for operating budgets and $20,000 for capital budgets. Should several accounts exceed their budget within these thresholds, it poses a risk that the predicted final end-of-year position may be understated.

To mitigate this risk, the CEO enacted the FACRs to run quarterly, and the Executive Management Group examine each job and account to ensure compliance. Also, the monthly report provides variance reporting highlighting any discrepancies against budget.

It should also be noted that should Council decide not to adopt the recommendations. It could lead to some initiatives being delayed or cancelled to offset the additional expenditure associated with running the Shire’s operations.

STRATEGIC CORPORATE PLAN OBJECTIVES

Performance – We will deliver excellent governance, service and value, for everyone.

Outcome Thirteen - Value for money from rates and long term financial sustainability:

Outcome Fourteen – Excellence in organisational performance and service delivery:

VOTING REQUIREMENTS

|

That the Audit and Risk Committee recommends that Council: 1. Receives the Quarter 3 Finance and Costing Review Report for the period ended 31 March 2021; 2. Adopts the operating and capital budget amendment recommendations for the year ended 30 June 2021 as attached; and 3. Notes a forecast end-of-year deficit position to 30 June 2021 of $173,509.

|

|

2020-2021 Quarter 3 Finance and Costing Review |

Agenda – Audit and Risk Committee Meeting 19 April 2021 Page 1 of 2

|

SUMMARY: A new risk management policy has been developed to meet the requirements of AS/NZS Risk Management Standard; 31000:2018 and to assist the Shire improve its Risk Management Framework. The report recommends that the Audit and Risk Committee endorse the policy for Council approval. |

BACKGROUND

Previous Considerations

The Shire first adopted a risk management policy in October 2010. The policy has largely remained the same since this time. The Policy was supported by a Risk Management Strategy that described the detailed process of implementing a Risk Management Framework and associated systems and processes across the Shire.

The Risk Management Policy and Strategy were based on the principles, framework and guidelines as detailed in the AS/NZS Risk Management Standard; 31000:2009. This Standard was updated in 2018.

COMMENT

Many organisations including the Shire of Broome, have found the implementation of a risk management framework a challenging process, and one that has not developed into a business as usual process that can be clearly linked to a reduction in risk events and more importantly being used as a integral tool in the assessment of shire priorities.

With that in mind, a change of approach was required and to that end during 2020 the Shire commenced working remotely with a Risk Management consultant based in Canberra, to refresh the Shire approach to risk management.

Unfortunately, the Corona virus pandemic has prevented the consultant from visiting Broome to complete staff and elected member risk management training, but it is hoped that this will be possible in June of this year.

In the meantime, the Risk Management Policy has been completely rewritten, with a view to providing a concise snap shot of what risk management is, why it is important to the Shire of Broome, the commitment required, an explanation of the approach that will be taken, how the policy will be measured, and the roles and responsibilities for risk management within Council.

Approach

Not all risks are the same and for that reason the Policy breaks risks into three distinct focus groups:

Strategic Risks: defined in the context of Shire of Broome as risks where the causes/contributing factors are outside the control of Council, but, if they were to occur, they may be serious enough to require a revision of the Shire’s Strategic Community Plan.

Enterprise (Operational) Risks: are those where the causes are either inside or outside the control of the Shire of Broome, but, if they occur, they will impact on the achievement of the current Strategic Community Plan and Corporate Business Plan strategies.

Project Risks: requires a unique approach, given the significant difference in context. The assessment of project risk requires consideration of schedule, cost and performance within the context of the project. Therefore, the use of a typical risk reference table based on likelihood and consequence is not appropriate.

Rather than one Risk Management Strategy to support the implementation of the Risk Management Policy separate Risk Management Plans for Strategic, Enterprise and Project Risks will be developed. These are currently being drafted and will be presented to the Audit and Risk Committee for endorsement at the next opportunity. The separate Risk Management Plans identify that likelihood needs to be assessed differently between strategic, enterprise and project risk when determining a suitable risk assessment matrix.

Finally, a Strategic Risk Register and Enterprise Risk Register will be established. This is aimed at ensuring that the risk context is set at the correct level and that the focus of control assurance and investment in risk management improvements is aligned to the highest level of risk areas identified.

CONSULTATION

Paladin Risk Management

STATUTORY ENVIRONMENT

Local Government (Audit) Regulations 1996

Regulation 17. CEO to review certain systems and procedures

The CEO is to review the appropriateness and effectiveness of risk management, internal controls and legislative compliance once in every 3 financial years and report results to the audit committee.

POLICY IMPLICATIONS

Nil. Updates existing policy of Council.

FINANCIAL IMPLICATIONS

Nil

RISK

Nil

STRATEGIC CORPORATE PLAN OBJECTIVES

Performance – We will deliver excellent governance, service and value, for everyone.

Outcome Eleven – Effective leadership, advocacy and governance:

11.2 Deliver best practice governance and risk management

VOTING REQUIREMENTS

|

That the Audit and Risk Committee recommends that Council adopts the updated Risk Management Policy as attached.

|

|

Risk Management Policy (updated) |

|

|

Risk Management Policy (Existing to be retired) |

Agenda – Audit and Risk Committee Meeting 19 April 2021 Page 1 of 2

|

These minutes were confirmed at a meeting held (DD Month Year), and signed below by the Presiding Person, at the meeting these minutes were confirmed.

Signed: ……………………………

|