AGENDA

FOR THE

Audit and Risk Committee Meeting

11 November 2021

NOTICE OF MEETING

Dear Council Member,

The next Audit and Risk Committee of Council will be held on Thursday, 11 November 2021 in the Council Chambers, Corner Weld and Haas Streets, Broome, commencing at 2:00pm.

Regards,

![]()

S MASTROLEMBO

Chief Executive Officer

04/11/2021

Our Mission

"To deliver affordable and quality Local Government services."

DISCLAIMER

The purpose of Council Meetings is to discuss, and where possible, make resolutions about items appearing on the agenda. Whilst Council has the power to resolve such items and may in fact, appear to have done so at the meeting, no person should rely on or act on the basis of such decision or on any advice or information provided by a Member or Officer, or on the content of any discussion occurring, during the course of the meeting.

Persons should be aware that the provisions in section 5.25 of the Local Government Act 1995 establish procedures for revocation or rescission of a Council decision. No person should rely on the decisions made by Council until formal advice of the Council decision is received by that person. The Shire of Broome expressly disclaims liability for any loss or damage suffered by any person as a result of relying on or acting on the basis of any resolution of Council, or any advice or information provided by a Member or Officer, or the content of any discussion occurring, during the course of the Council meeting.

Should you require this document in an alternative format please contact us.

Agenda – Audit and Risk Committee Meeting 11 November 2021 Page 1 of 2

SHIRE OF BROOME

Audit and Risk Committee Meeting

Thursday 11 November 2021

INDEX – Agenda

3. Declarations Of Financial Interest / Impartiality

5.1 1ST QUARTER FINANCE AND COSTING REVIEW 2021-22

Agenda – Audit and Risk Committee Meeting 11 November 2021 Page 1 of 2

|

That the Minutes of the Audit and Risk Committee held on 19 April 2021, as published and circulated, be confirmed as a true and accurate record of that meeting.

|

Agenda – Audit and Risk Committee Meeting 11 November 2021 Page 1 of 2

|

SUMMARY: The Audit and Risk Committee is requested to consider results of the 1st Quarter Finance and Costing Review (FACR) of the Shire’s budget for the period ended 30 September 2021, including forecast estimates and budget recommendations to 30 June 2022. |

Previous Considerations

OMC 24 June 2021 Item 9.3.1

Quarter 1 Finance and Costing Review

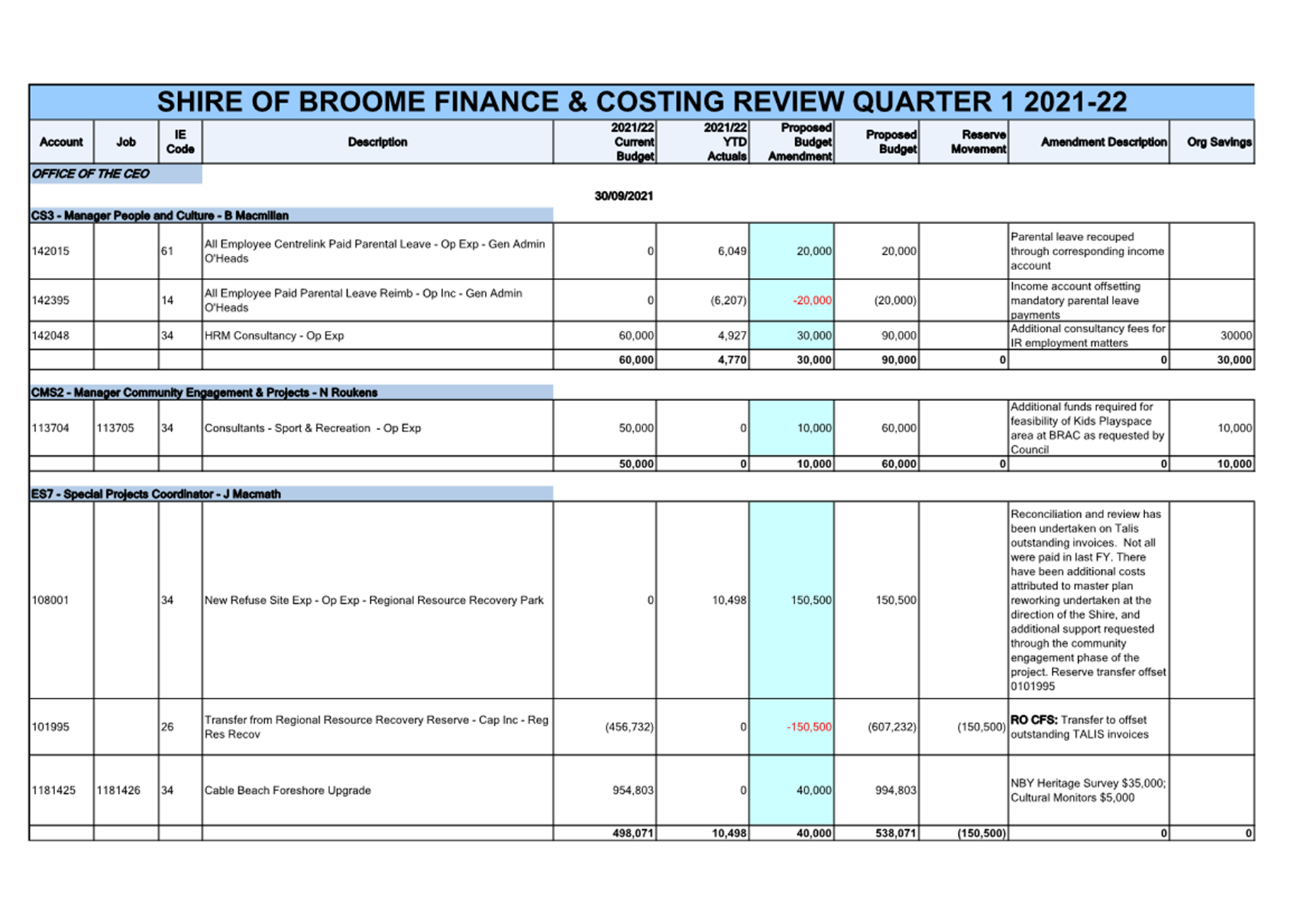

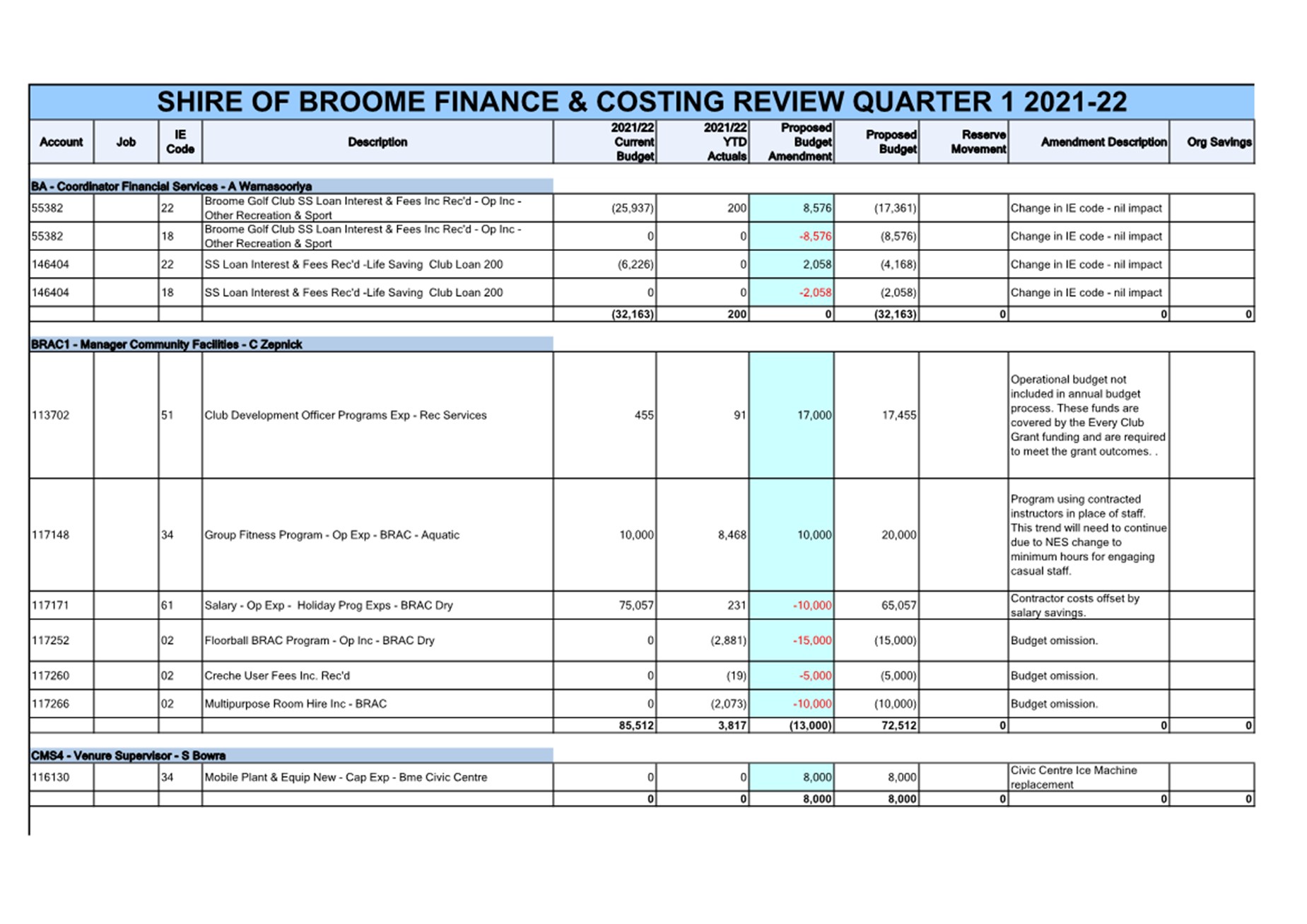

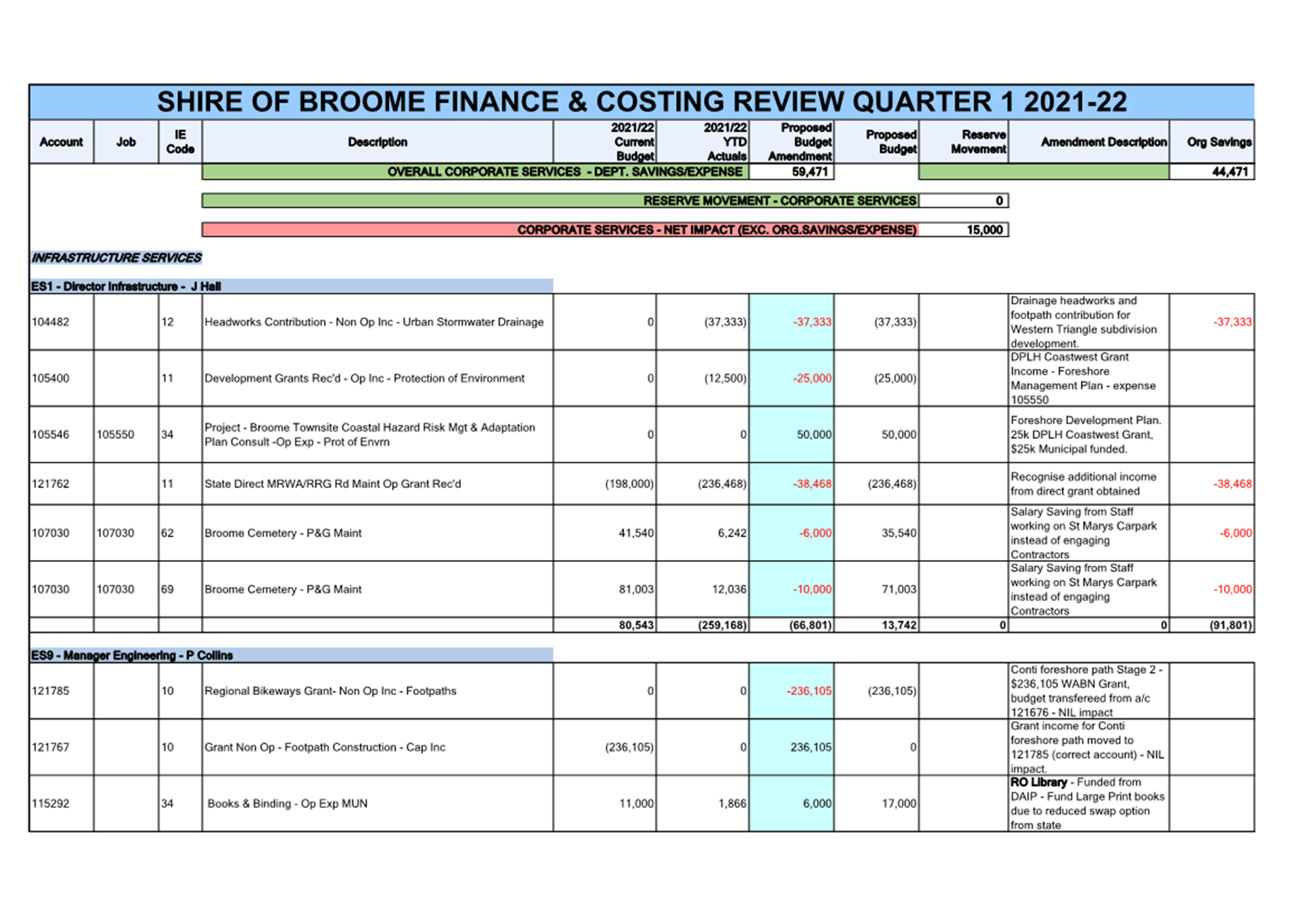

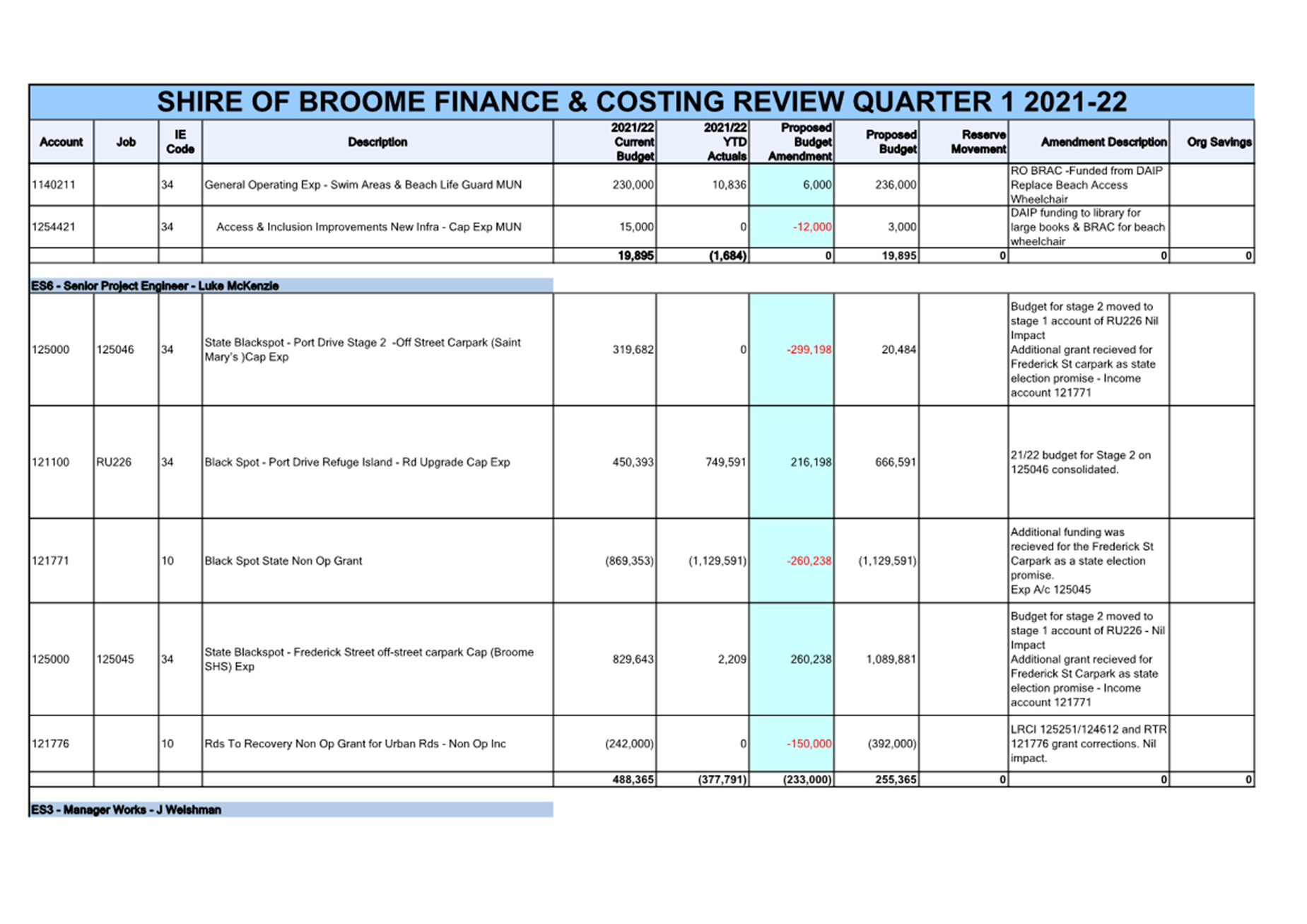

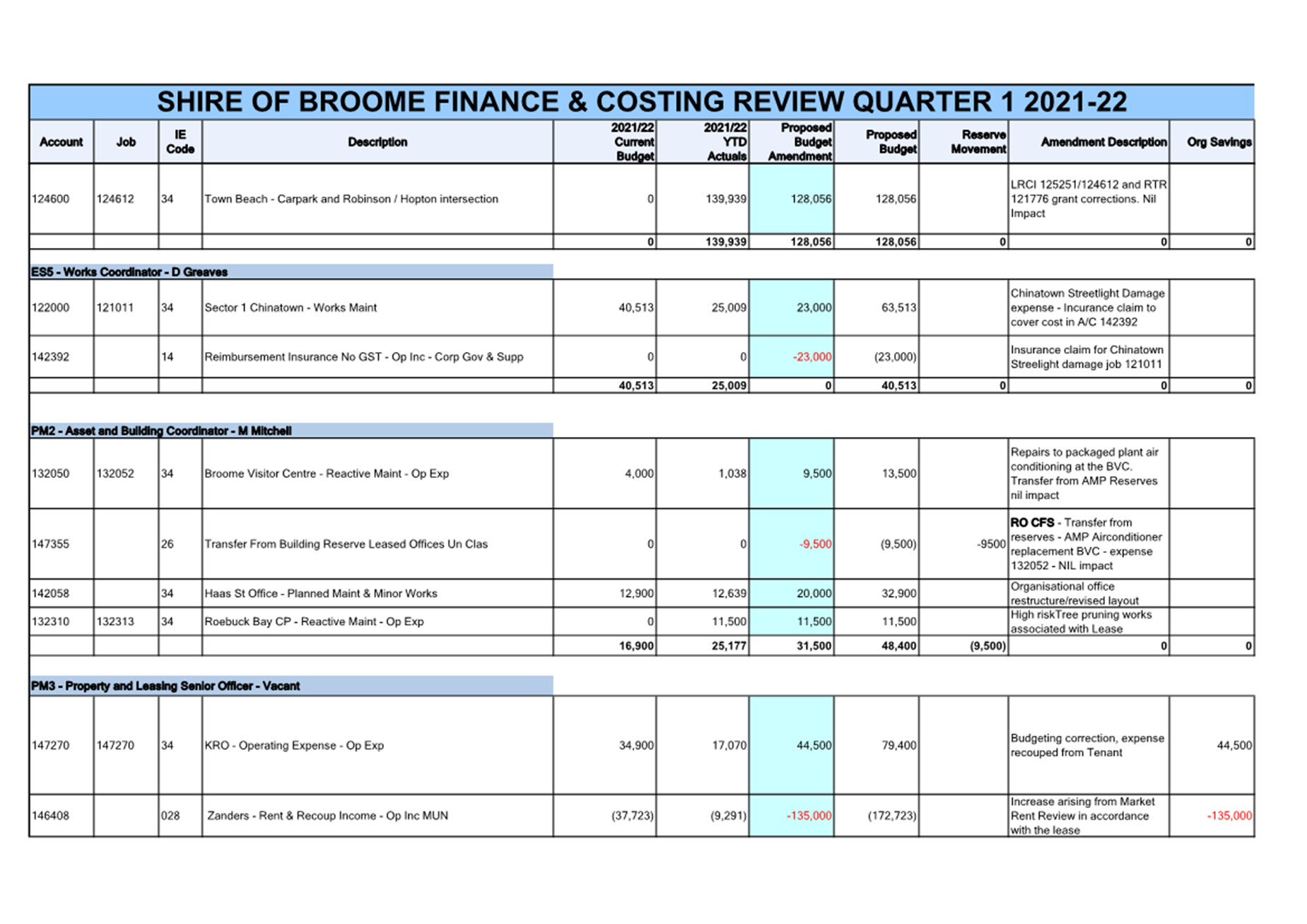

The Shire of Broome has carried out its 1st Quarter Finance and Costing Review (FACR) for the 2021-22 financial year. This review of the 2021-22 Annual Budget is based on actuals and commitments for the first three months of the year from 1 July 2021 to 30 September 2021, and forecasts for the remainder of the financial year.

This process aims to highlight over and under expenditure of funds and over and under achievement of income targets for the benefit of Executive and Responsible Officers to ensure good fiscal management of their projects and programs.

Once this process is completed, a report is compiled identifying budgets requiring amendments to be adopted by Council. Additionally, a summary provides the financial impact of all proposed budget amendments to the Shire of Broome’s adopted end-of-year forecast, to assist Council to make an informed decision.

It should be noted that the 2021-22 annual budget was adopted at the Ordinary Meeting of Council on 24 June 2021 as a balanced budget.

COMMENT

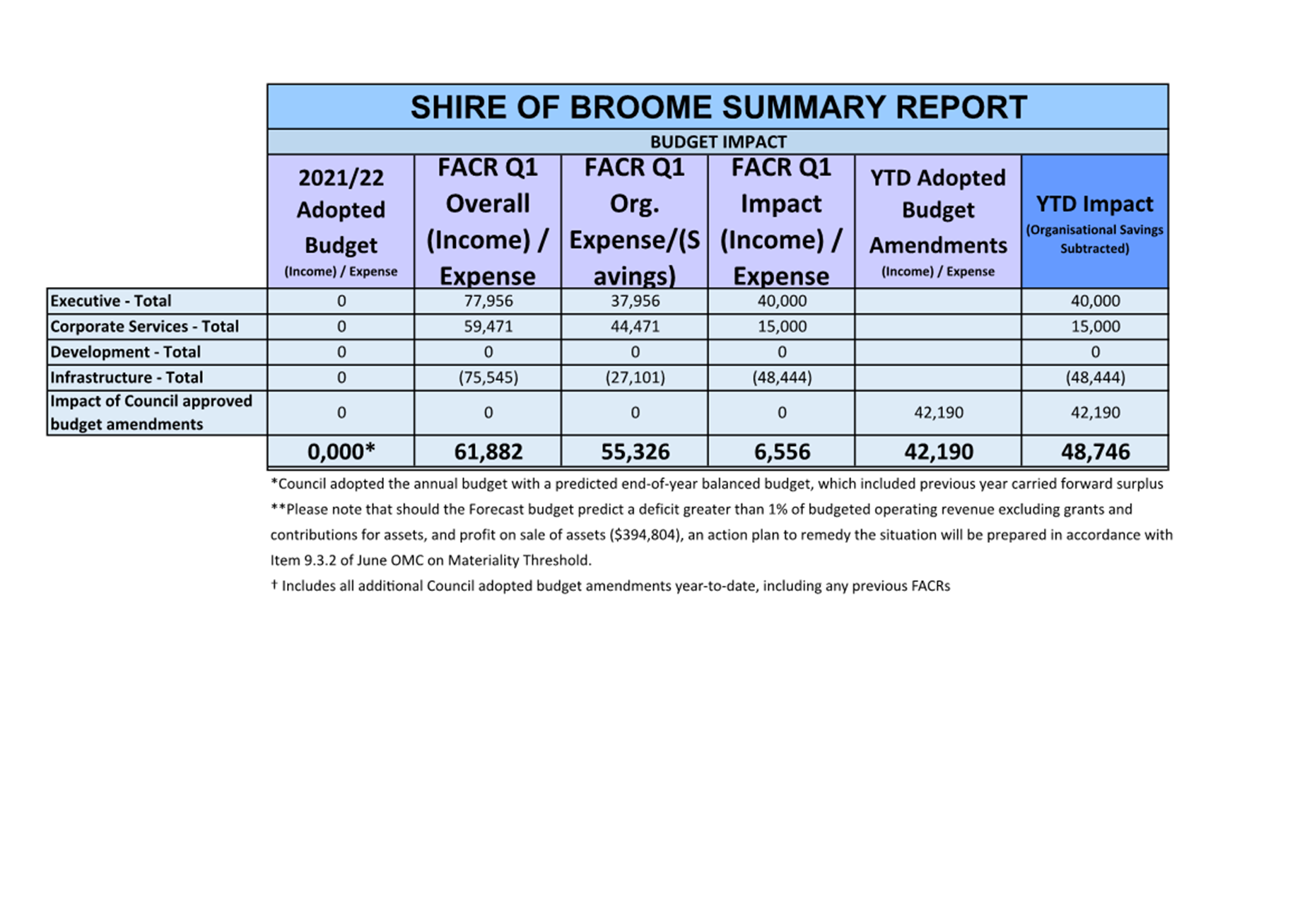

The Quarter 1 FACR commenced on 18 October 2021. The results from this process indicate a deficit forecast financial position of $48,746 should Council approve the proposed budget amendments. Council should note this net result excludes an organisational expense (deficit) of $55,326. The overall result indicates a total deficit position to 30 June 2022 of $104,073.

While officers make every effort to ensure the net impact of each FACR is minimal, the net deficit forecast mainly relates to the following proposed amendments:

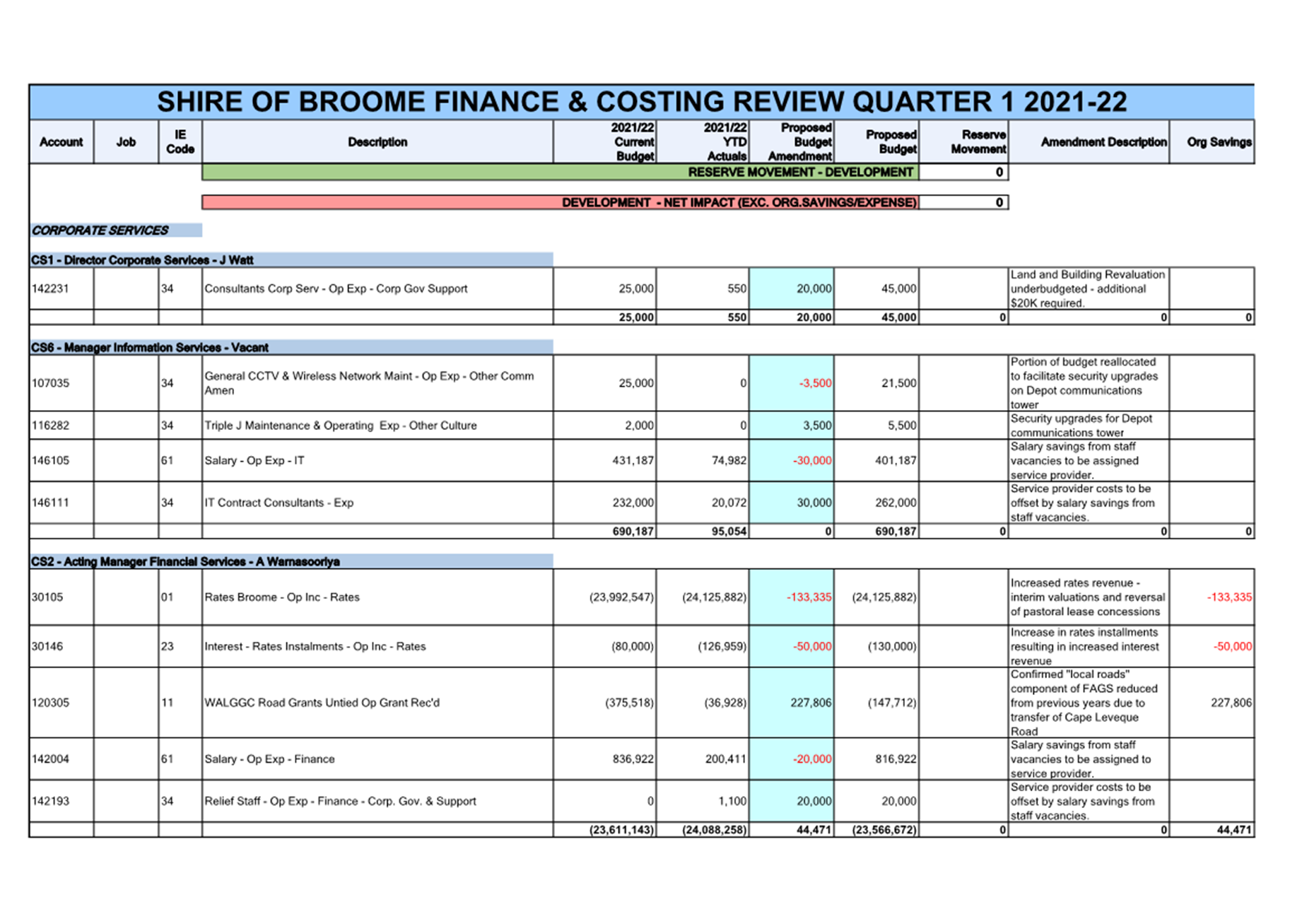

· a $185,000 increase in revenue from anticipated Rates interest and admin fees

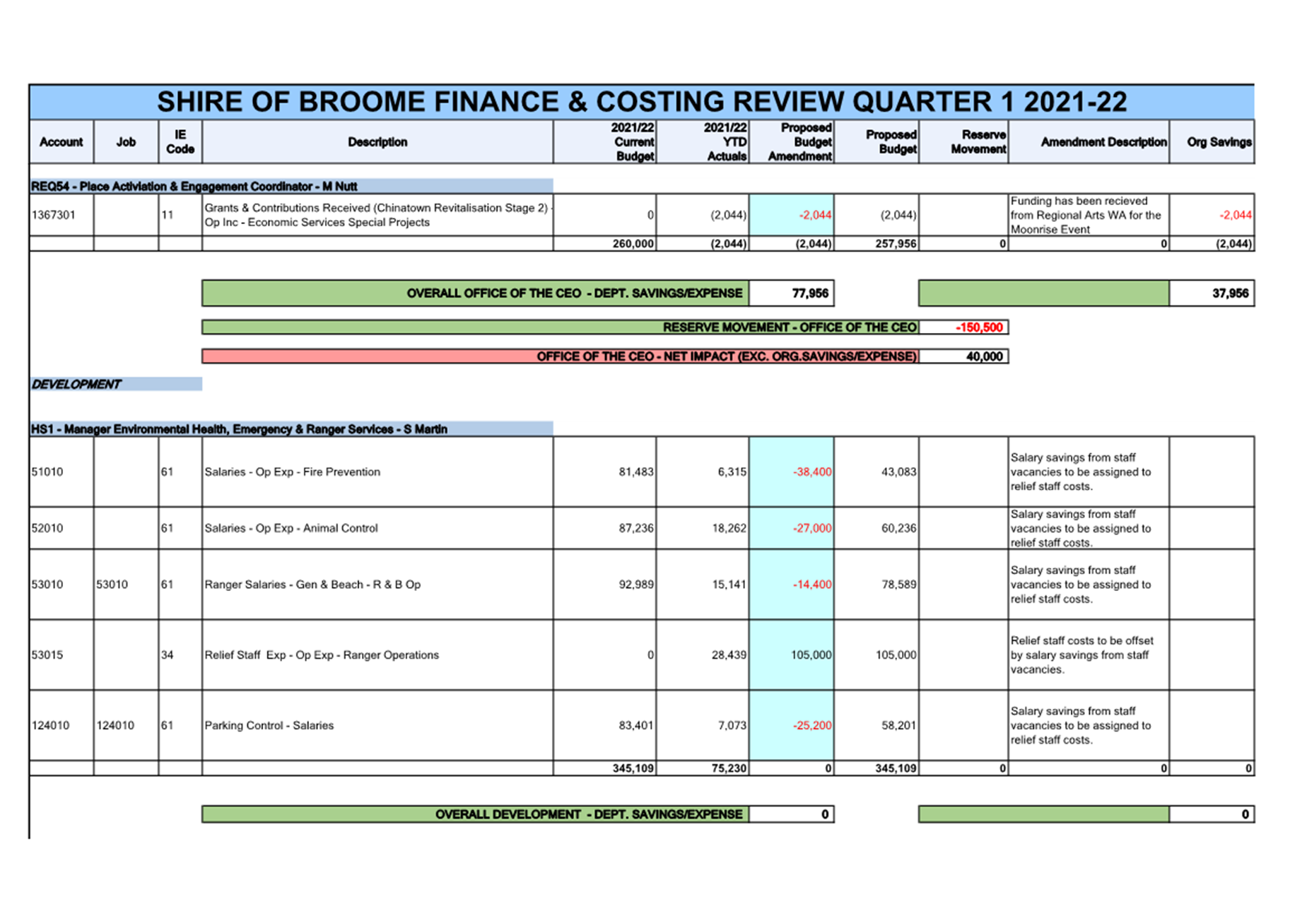

· a $227,000 reduction in budgeted Western Australian Local Government Grant Commission Road Grants (Local Roads component of FAGS)

· a $172,000 increase in commercial lease rental income

· a $238,000 amendment required to address budget upload errors identified through the process.

The above figure represents a budget forecast should all expenditure and income occur as expected. It does not represent the actual end-of-year position which can only be determined as part of the normal annual financial processes at the end of the financial year.

A comprehensive list of accounts (refer to Attachment 1) has been included for perusal by the committee, summarised by Directorate.

A summary of the results is as follows:

|

|

SHIRE OF BROOME SUMMARY REPORT |

|||||||

|

BUDGET IMPACT |

||||||||

|

2021/22

Adopted Budget |

FACR Q1 (Inc) /

Exp |

FACR Q1 |

FACR Q1 |

YTD

Adopted Budget Amendments |

YTD

Impact |

|||

|

Executive - Total |

0 |

77,956 |

37,956 |

40,000 |

|

40,000 |

||

|

Corporate Services - Total |

0 |

44,471 |

44,471 |

15,000 |

|

15,000 |

||

|

Development - Total |

0 |

0 |

0 |

0 |

|

0 |

||

|

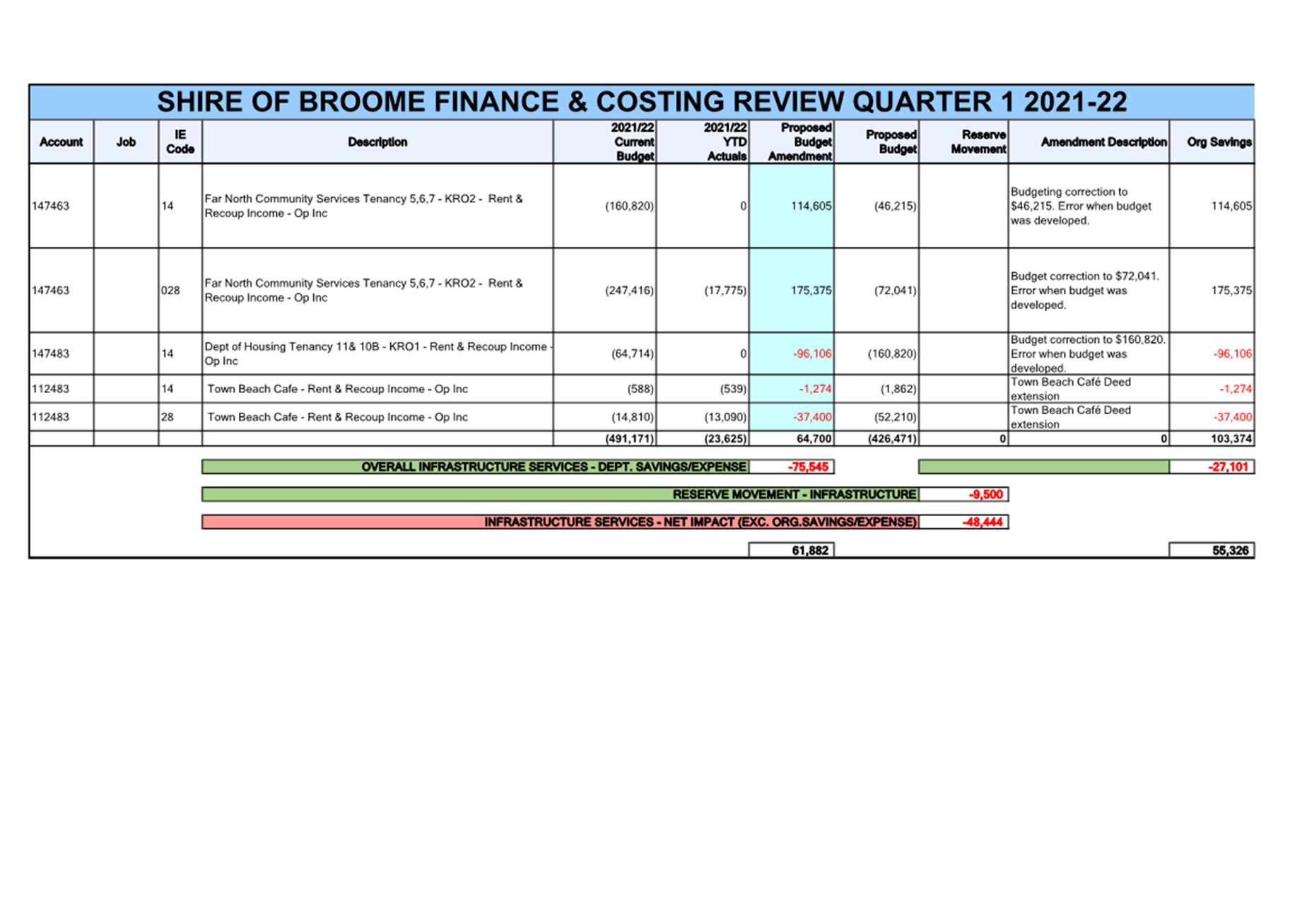

Infrastructure - Total |

0 |

(75,545) |

(27,101) |

(48,444) |

|

(48,444) |

||

|

Council approved budget amendments |

0 |

0 |

0 |

0 |

42,190 |

42,190 |

||

|

|

|

|

0,000* |

61,882 |

55,326 |

6,556 |

42,190 |

48,746 |

CONSULTATION

All amendments have been proposed after consultation with Executive and responsible officers at the Shire.

STATUTORY ENVIRONMENT

Local Government (Financial Management) Regulation 1996

r33A. Review of Budget

(1) Between 1 January and 31 March in each financial year a local government is to carry out a review of its annual budget for that year.

(2A) The review of an annual budget for a financial year must —

(a) consider the local government’s financial performance in the period beginning on 1 July and ending no earlier than 31 December in that financial year; and

(b) consider the local government’s financial position as at the date of the review; and

(c) review the outcomes for the end of that financial year that are forecast in the budget.

(2) Within 30 days after a review of the annual budget of a local government is carried out it is to be submitted to the council.

(3) A council is to consider a review submitted to it and is to determine* whether or not to adopt the review, any parts of the review or any recommendations made in the review.

*Absolute majority required.

(4) Within 30 days after a council has made a determination, a copy of the review and determination is to be provided to the Department.

Local Government Act 1995

6.8. Expenditure from municipal fund not included in annual budget

1) A local government is not to incur expenditure from its municipal fund for an additional purpose except where the expenditure —

(a) is incurred in a financial year before the adoption of the annual budget by the local government;

(b) is authorised in advance by resolution*; or

(c) is authorised in advance by the mayor or president in an emergency.

(1a) In subsection (1) —

“additional purpose” means a purpose for which no expenditure estimate is included in the local government’s annual budget.

POLICY IMPLICATIONS

Nil.

It should be noted that according to the materiality threshold set at the budget adoption, should a deficit achieve 1% of Shire’s operating revenue ($395,334) the Shire must formulate an action plan to remedy the over expenditure.

FINANCIAL IMPLICATIONS

The net result of the Quarter 1 FACR estimates is a budget deficit position of $48,746 to 30 June 2022.

This net result excludes an organisational expense (deficit) of $55,326.

The overall result indicates a total deficit position to 30 June 2022 of $104,073.

RISK

The Finance and Costing Review (FACR) seeks to provide a best estimate of the end-of-year position for the Shire of Broome at 30 June 2022. Contained within the report are recommendations of amendments to budgets which have financial implications on the estimate of the end-of-year position.

The review does not, however, seek to make amendments below the materiality threshold unless strictly necessary. The materiality thresholds are set at $10,000 for operating budgets and $20,000 for capital budgets. Should a number of accounts exceed their budget within these thresholds, it poses a risk that the predicted final end-of-year position may be understated.

In order to mitigate this risk, the CEO enacted the FACRs to run quarterly and Executive examine each job and account to ensure compliance. In addition, the monthly report provides variance reporting highlighting any discrepancies against budget.

It should also be noted that should Council decide not to adopt the recommendations, it could lead to some initiatives being delayed or cancelled in order to offset the additional expenditure associated with running the Shire’s operations.

STRATEGIC ASPIRATIONS

Performance – We will deliver excellent governance, service and value, for everyone.

Outcome Eleven – Effective leadership, advocacy and governance:

11.2 Deliver best practice governance and risk management.

Outcome Thirteen - Value for money from rates and long term financial sustainability:

13.1 Plan effectively for short and long term financial sustainability.

VOTING REQUIREMENTS

|

That the Audit and Risk Committee recommends that Council: 1. Receives the Quarter 1 Finance and Costing Review Report for the period ended 30 September 2021; 2. Adopts the operating and capital budget amendment recommendations for the year ended 30 June 2022 as attached; 3. Notes a forecast net end-of-year deficit position to 30 June 2022 of $48,746, noting an organisational expense (deficit) of $55,326, resulting in an overall deficit position of $104,073.

|

|

2021-22 Quarter 1 Finance and Costing Review |

Agenda – Audit and Risk Committee Meeting 11 November 2021 Page 1 of 2

|

These minutes were confirmed at a meeting held (DD Month Year), and signed below by the Presiding Person, at the meeting these minutes were confirmed.

Signed: ……………………………

|