CONFIRMED

MINUTES

OF THE

Audit and Risk Committee Meeting

17 February 2022

|

These minutes were confirmed at a meeting held 27 April 2022 and signed below by the Presiding Person, at the meeting these minutes were confirmed.

|

CONFIRMED

MINUTES

OF THE

Audit and Risk Committee Meeting

17 February 2022

|

These minutes were confirmed at a meeting held 27 April 2022 and signed below by the Presiding Person, at the meeting these minutes were confirmed.

|

Minutes – Audit and Risk Committee Meeting 17 February 2022 Page 1 of 4

SHIRE OF BROOME

Audit and Risk Committee Meeting

Thursday 17 February 2022

INDEX – Minutes

3. Declarations Of Financial Interest / Impartiality

5.2 2ND QUARTER FINANCE AND COSTING REVIEW 2021-22

5.1 COMPLIANCE AUDIT RETURN 2021

5.3 REPORT ON SIGNIFICANT AUDIT MATTERS 2020-2021.

6. Matters Behind Closed Doors

MINUTES OF THE Audit and Risk Committee Meeting OF THE SHIRE OF BROOME,

HELD IN THE Council Chambers, Corner Weld and Haas Streets, Broome, ON Thursday 17 February 2022, COMMENCING AT 12:00PM.

The Chair welcomed Councillors and Officers and declared the meeting open at 12:04 PM

|

ATTENDANCE |

|

|

|

|

|

|

|

Members: |

Cr D Male |

Deputy Shire President |

|

|

Cr C Mitchell |

|

|

|

Cr B Rudeforth |

|

|

|

Cr P Taylor |

Proxy |

|

|

|

|

|

|

||

|

Apologies: |

Nil |

|

|

|

|

|

|

|

||

|

Leave of Absence: |

Nil |

|

|

|

|

|

|

|

||

|

Officers: |

Mr S Mastrolembo |

Chief Executive Officer (left 12:51PM) |

|

|

Mr J Hall |

Director Infrastructure (from 12:38PM) |

|

|

Mr J Watt |

Director Corporate Services |

|

|

Mr K Williams |

Director Development (left 12:48PM) |

|

|

Mr D Kennedy |

Manager Governance Strategy and Risk |

|

|

|

|

|

Committee Member |

Item No |

Item |

Nature of Interest |

|

Cr D Male |

5.3 |

2nd Quarter Finance and Costing Review |

Financial - Budget amendments referred to in the item relate to a client of my business. |

|

Committee Resolution: Minute No. AR/0222/001 Moved: Cr D Male Seconded: Cr C Mitchell That the Minutes of the Audit and Risk Committee held on 15 February 2022, as published and circulated, be confirmed as a true and accurate record of that meeting. |

|

Move Item of Business: Minute No. AR/0222/002 Moved: Cr D Male Seconded: Cr B Rudeforth That Council move item 5.2 – 2nd Quarter Finance and Costing Review in the order of business in front of item 5.1 Compliance Audit Return. |

Cr D Male declared a financial interest in Item 5.2 being “budget amendments referred to in the item relate to a client of my business.” Cr Male did not participate in the decision making process relating to item 5.2

|

SUMMARY: The Audit and Risk Committee is requested to consider results of the 2nd Quarter Finance and Costing Review (FACR) of the Shire’s budget for the period ended 31 December 2021, including forecast estimates and budget recommendations to 30 June 2022. |

Previous Considerations

OMC 24 June 2021 Item 9.3.1

OMC 18 November 2021 Item 9.4.7

Quarter 1 Finance and Costing Review

The Shire of Broome has carried out its 2nd Quarter Finance and Costing Review (FACR) for the 2021-22 financial year. This review of the 2021-22 Annual Budget is based on actuals and commitments for the first 6 months of the year from 1 July 2021 to 31 December 2021, and forecasts for the remainder of the financial year.

This process aims to highlight over and under expenditure of funds and over and under achievement of income targets for the benefit of Executive and Responsible Officers to ensure good fiscal management of their projects and programs.

Once this process is completed, a report is compiled identifying budgets requiring amendments to be adopted by Council. Additionally, a summary provides the financial impact of all proposed budget amendments to the Shire of Broome’s adopted end-of-year forecast, to assist Council to make an informed decision.

It should be noted that the 2021-22 annual budget was adopted at the Ordinary Meeting of Council on 24 June 2021 as a balanced budget.

COMMENT

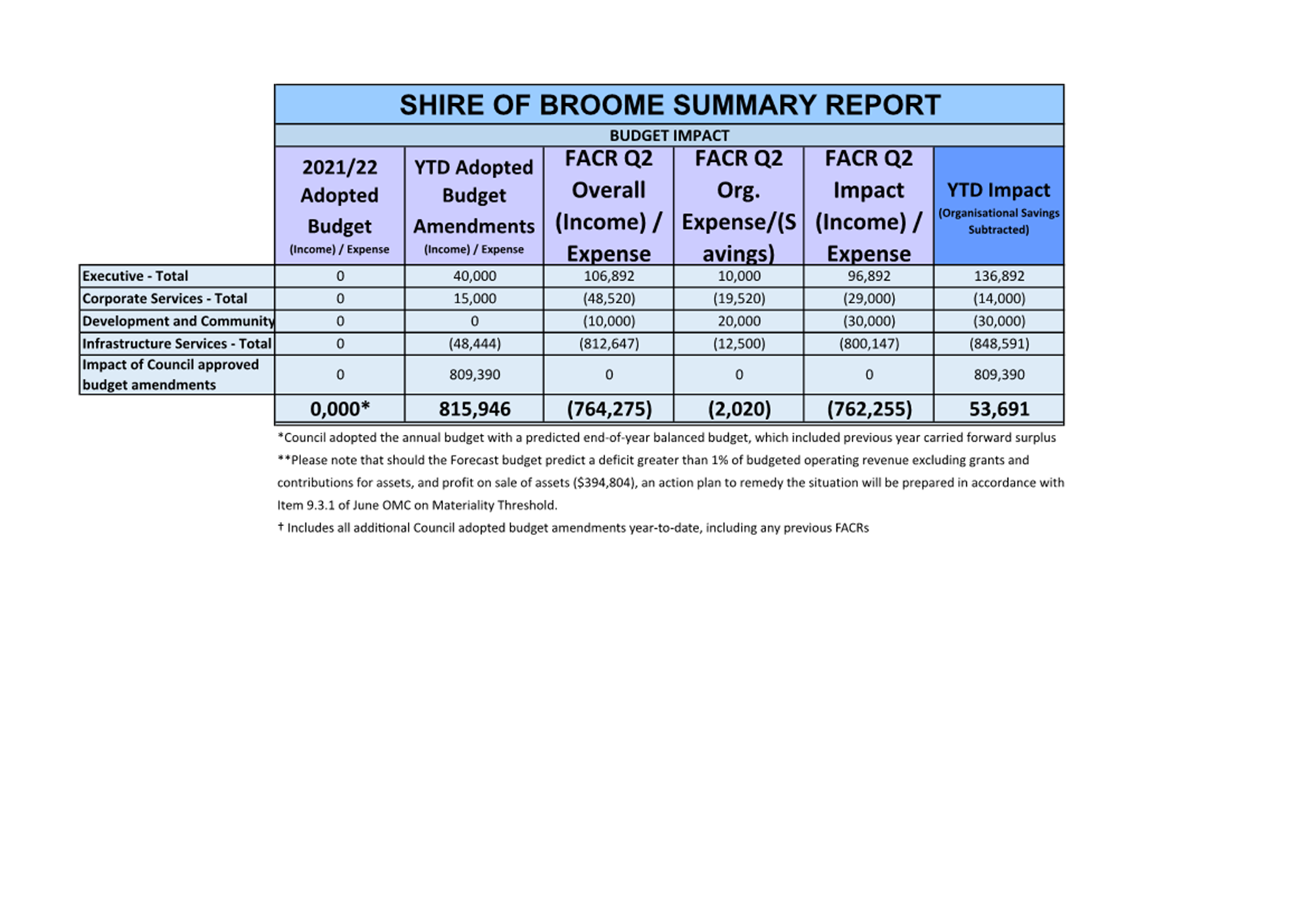

The Quarter 2 FACR commenced on 2 February 2022. At the start of the Q2 FACR, a net deficit of $815,946 was forecast arising from past budget amendments adopted by Council, including Q1 FACR. The Q2 FACR identifies net savings of $764,275 resulting in a cumulative net deficit forecast of $53,691.

The overall Q2 FACR result indicates a deficit forecast financial position of $53,691 should Council approve the proposed budget amendments.

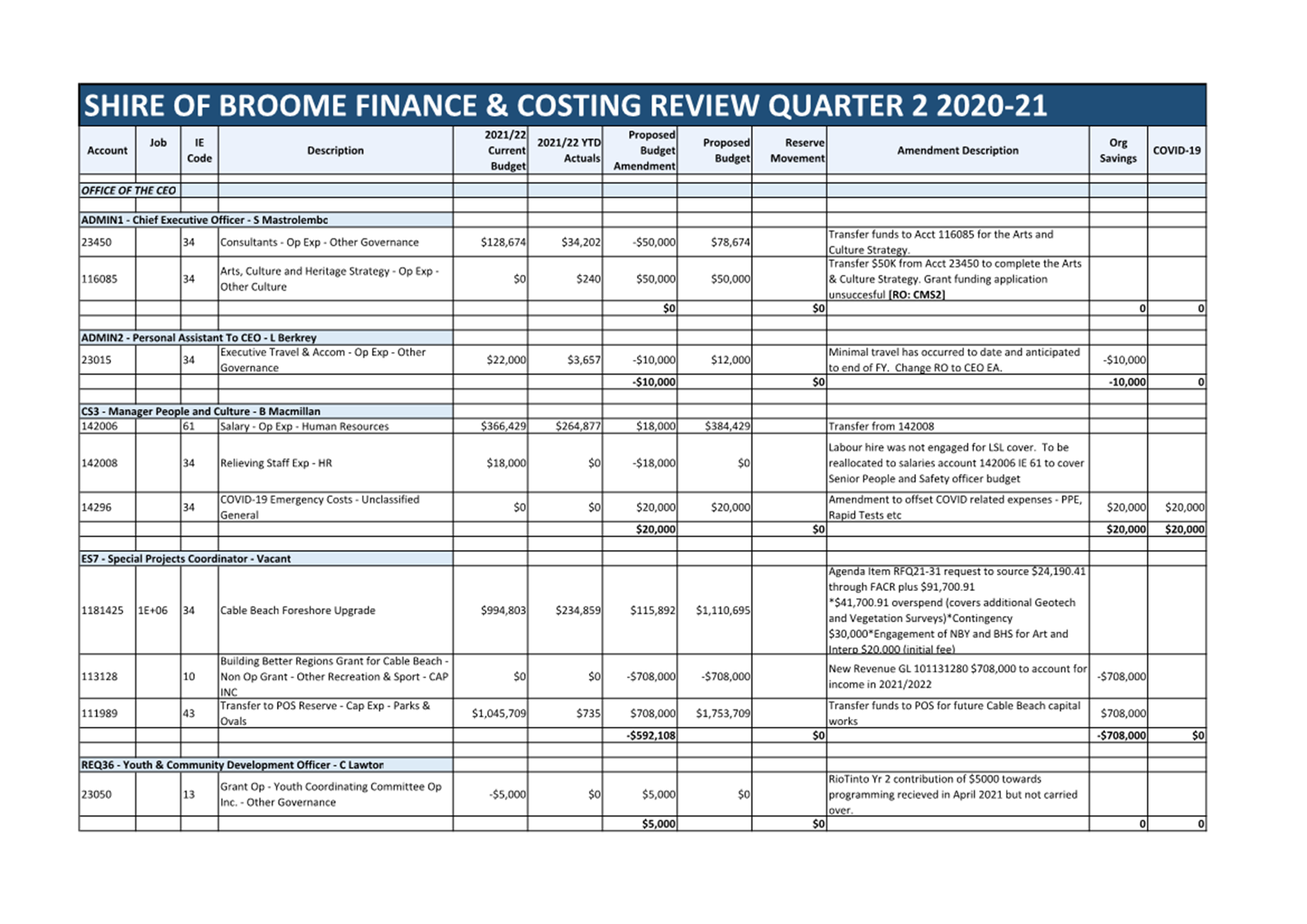

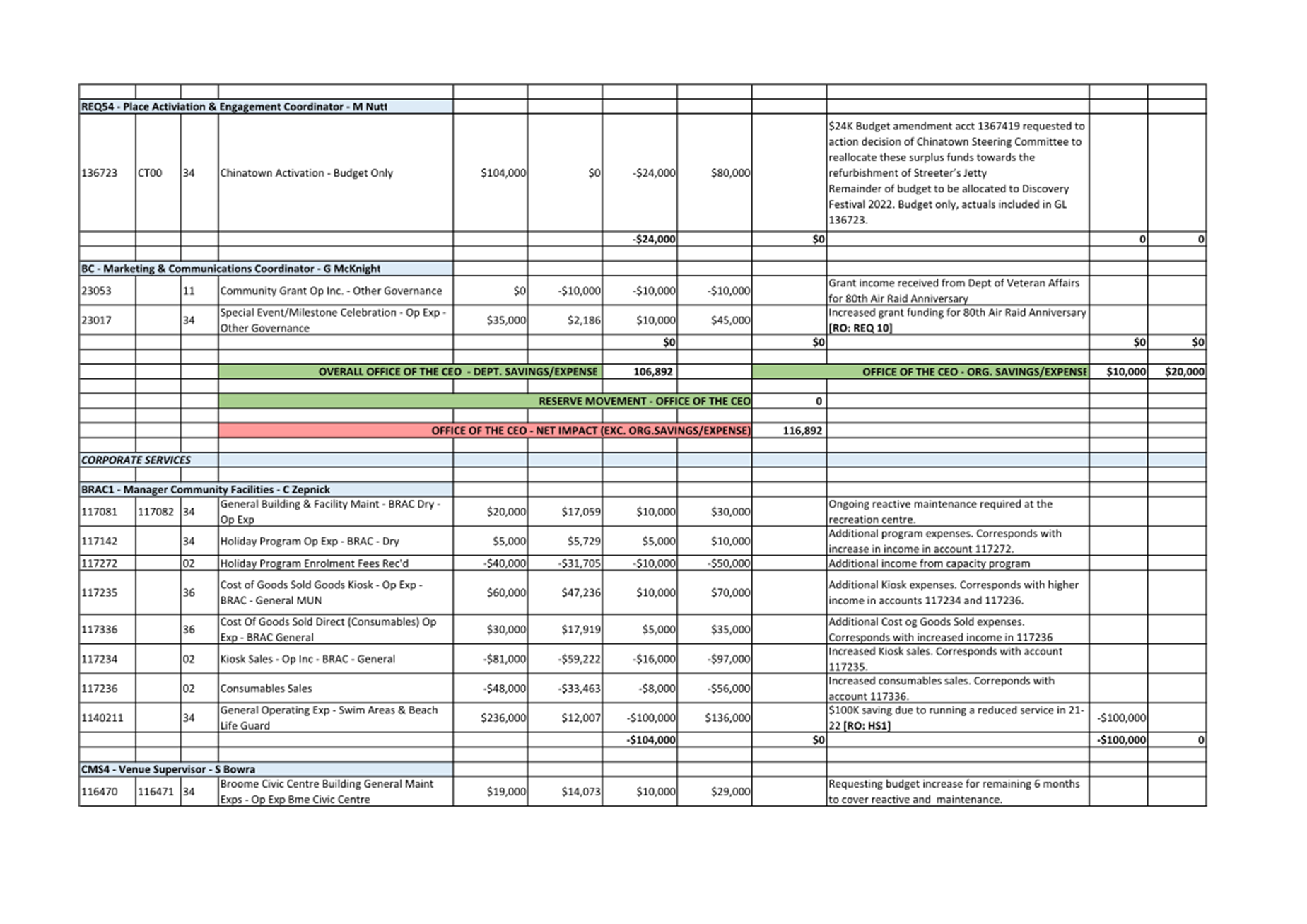

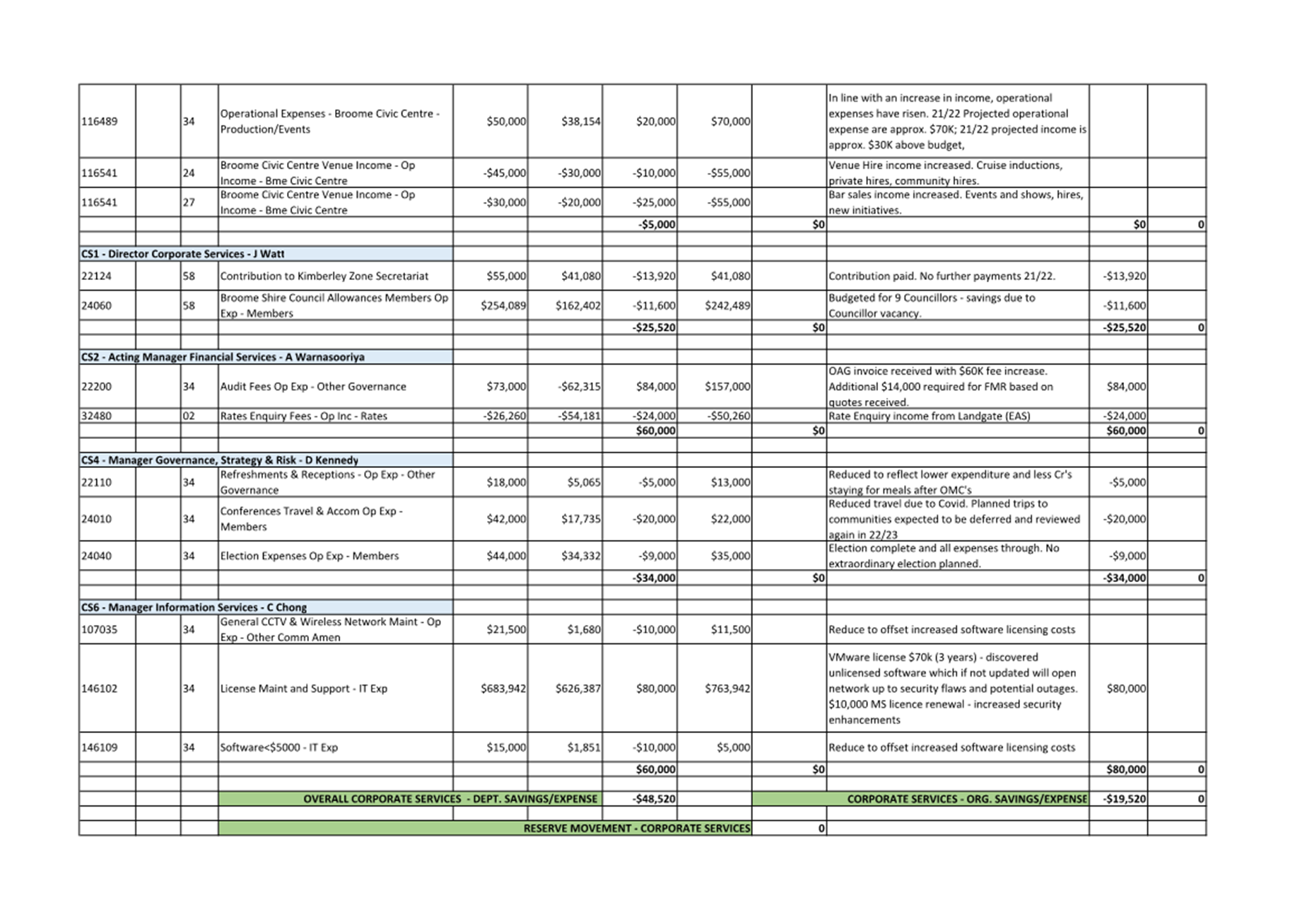

There were a total of 71 budget amendments proposed at the Q2 FACR which made up the $764,275 net surplus for the quarter. There is no single transaction to which this net surplus is attributed. While officers make every effort to ensure the net impact of each FACR is minimal, the net deficit forecast mainly relates to the following proposed amendments:

· $708,000 Building Better Regions Funding received for the Cable Beach project

· $390,000 recognition of the increased Self-Supporting Loan for the Broome Surf Life Saving Club

· $350,000 recognition of the increased Lotterywest contribution towards the Broome Surf Life Saving Club

· $84,000 amendment for increased 2020-21 Audit Fees

The significant amendments from Q1 FACR included:

· a $185,000 increase in revenue from anticipated Rates interest and admin fees

· a $227,000 reduction in budgeted Western Australian Local Government Grant Commission Road Grants (Local Roads component of FAGS)

· a $172,000 increase in commercial lease rental income

· a $238,000 amendment required to address budget upload errors identified through the process.

The above figure represents a budget forecast should all expenditure and income occur as expected. It does not represent the actual end-of-year position which can only be determined as part of the normal annual financial processes at the end of the financial year.

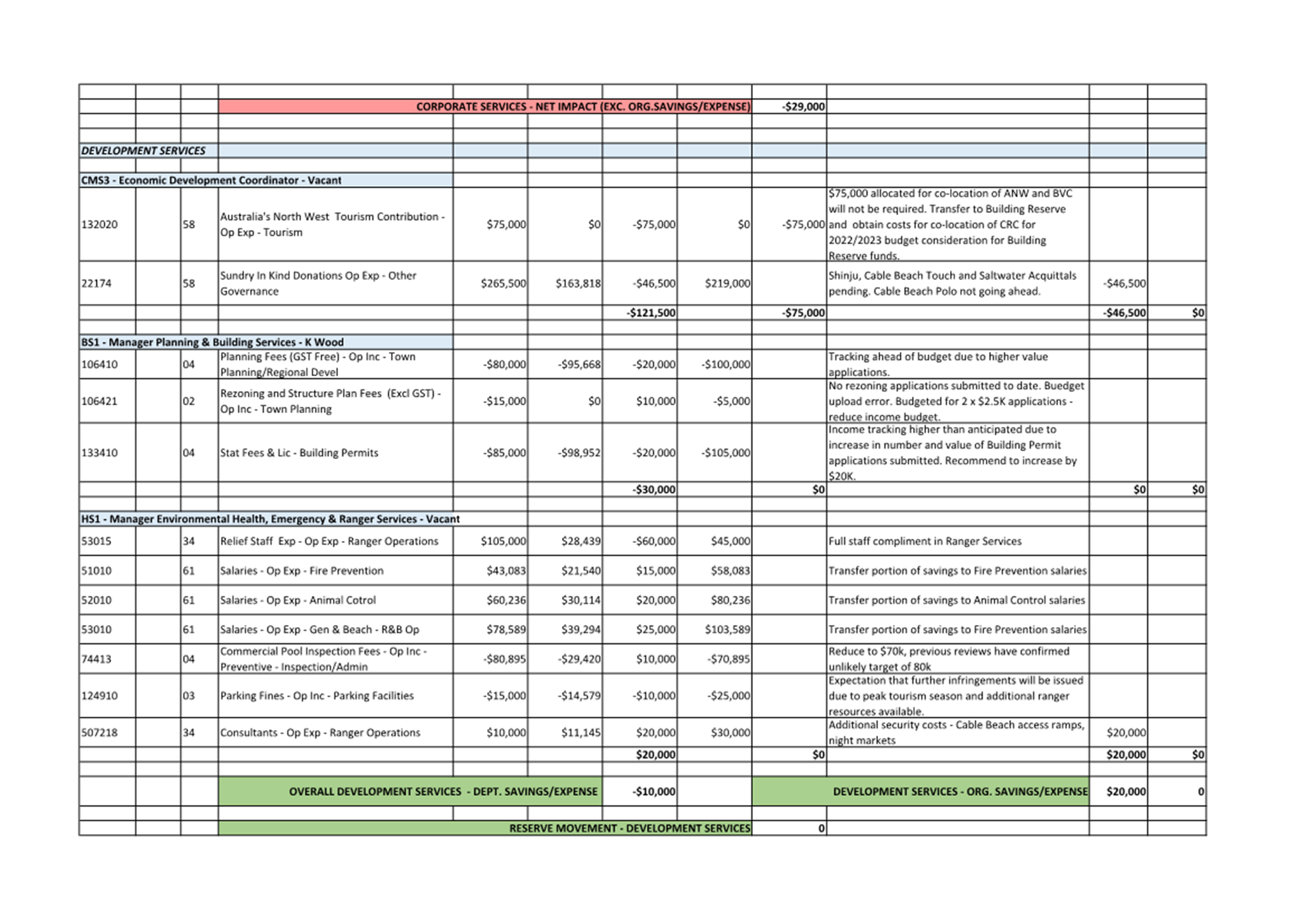

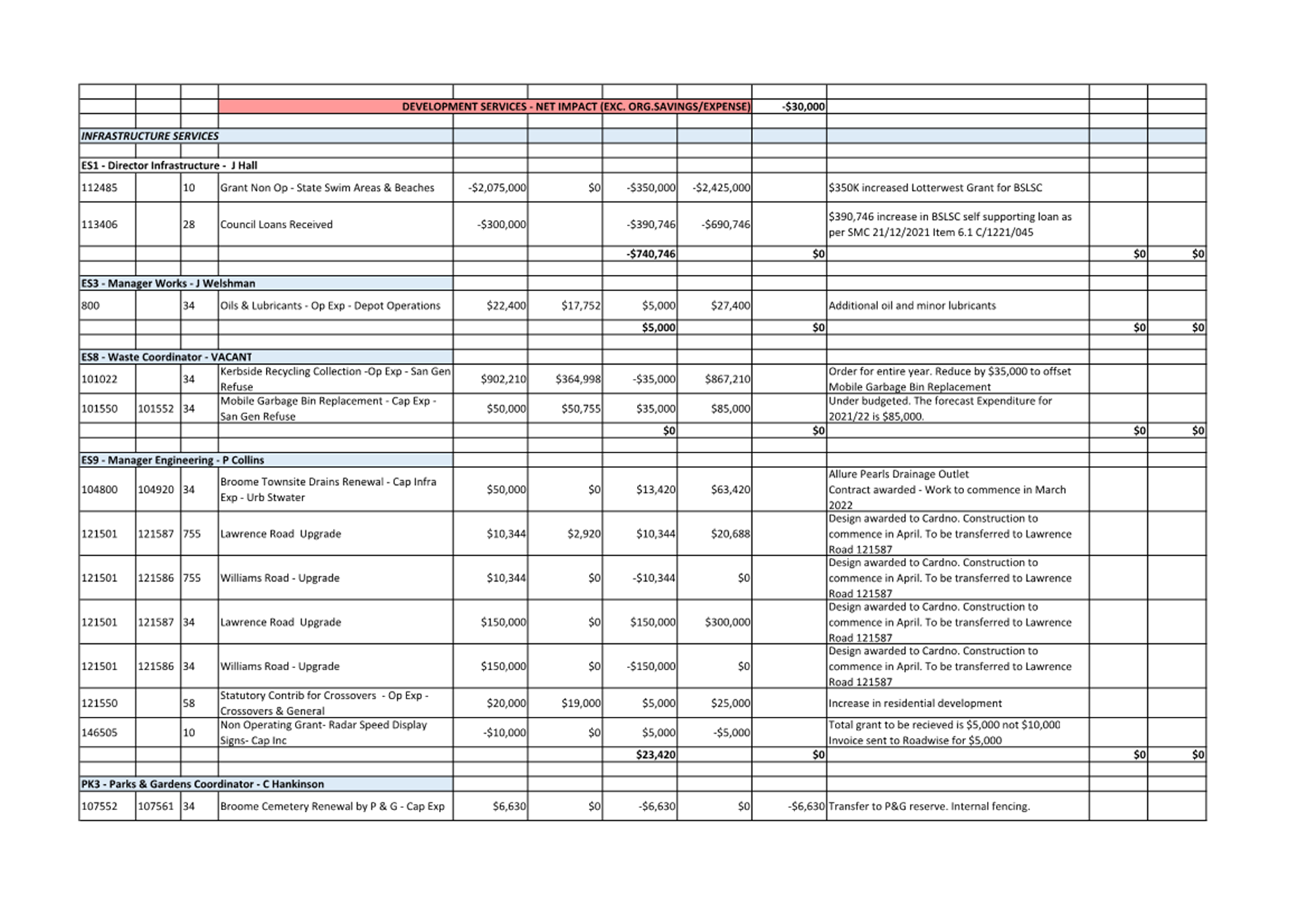

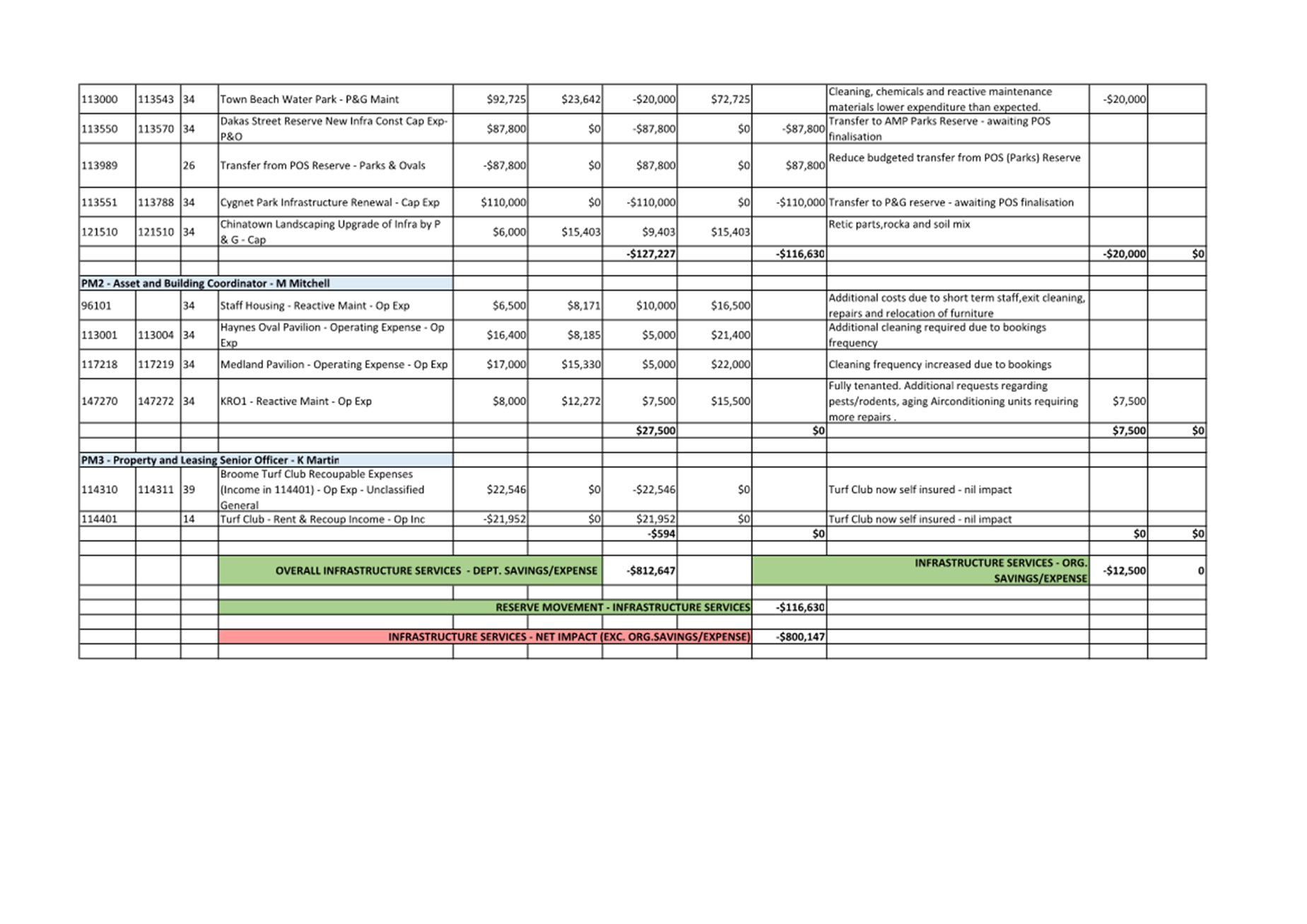

A comprehensive list of accounts (refer to Attachment 1) has been included for perusal by the committee, summarised by Directorate.

A summary of the results is as follows:

|

|

SHIRE OF BROOME SUMMARY REPORT |

|||||||

|

BUDGET IMPACT |

||||||||

|

2021/22

Adopted Budget |

YTD

Adopted Budget Amendments |

FACR Q2 |

FACR Q2 |

FACR Q2 |

YTD

Impact |

|||

|

Executive |

0 |

40,000 |

106,892 |

10,000 |

96,892 |

136,892 |

||

|

Corporate |

0 |

15,000 |

(48,520) |

(19,520) |

(29,000) |

(14,000) |

||

|

Development |

0 |

0 |

(10,000) |

20,000 |

(30,000) |

(30,000) |

||

|

Infrastructure |

0 |

(48,444) |

(812,647) |

(12,500) |

(800,147) |

(848,591) |

||

|

Impact of Council approved budget amendments |

0 |

809,390 |

0 |

0 |

0 |

809,390 |

||

|

|

|

|

0,000* |

815,946 |

(764,275) |

(2,020) |

(762,255) |

53,691 |

CONSULTATION

All amendments have been proposed after consultation with Executive and responsible officers at the Shire.

STATUTORY ENVIRONMENT

Local Government (Financial Management) Regulation 1996

r33A. Review of Budget

(1) Between 1 January and 31 March in each financial year a local government is to carry out a review of its annual budget for that year.

(2A) The review of an annual budget for a financial year must —

(a) consider the local government’s financial performance in the period beginning on 1 July and ending no earlier than 31 December in that financial year; and

(b) consider the local government’s financial position as at the date of the review; and

(c) review the outcomes for the end of that financial year that are forecast in the budget.

(2) Within 30 days after a review of the annual budget of a local government is carried out it is to be submitted to the council.

(3) A council is to consider a review submitted to it and is to determine* whether or not to adopt the review, any parts of the review or any recommendations made in the review.

*Absolute majority required.

(4) Within 30 days after a council has made a determination, a copy of the review and determination is to be provided to the Department.

Local Government Act 1995

6.8. Expenditure from municipal fund not included in annual budget

1) A local government is not to incur expenditure from its municipal fund for an additional purpose except where the expenditure —

(a) is incurred in a financial year before the adoption of the annual budget by the local government;

(b) is authorised in advance by resolution*; or

(c) is authorised in advance by the mayor or president in an emergency.

(1a) In subsection (1) —

“additional purpose” means a purpose for which no expenditure estimate is included in the local government’s annual budget.

POLICY IMPLICATIONS

Nil.

It should be noted that according to the materiality threshold set at the budget adoption, should a deficit achieve 1% of Shire’s operating revenue ($395,334) the Shire must formulate an action plan to remedy the over expenditure.

FINANCIAL IMPLICATIONS

The net result of the Quarter 2 FACR estimates is a budget deficit position of $53,691 to 30 June 2022.

RISK

The Finance and Costing Review (FACR) seeks to provide a best estimate of the end-of-year position for the Shire of Broome at 30 June 2022. Contained within the report are recommendations of amendments to budgets which have financial implications on the estimate of the end-of-year position.

The review does not, however, seek to make amendments below the materiality threshold unless strictly necessary. The materiality thresholds are set at $10,000 for operating budgets and $20,000 for capital budgets. Should a number of accounts exceed their budget within these thresholds, it poses a risk that the predicted final end-of-year position may be understated.

In order to mitigate this risk, the CEO enacted the FACRs to run quarterly and Executive examine each job and account to ensure compliance. In addition, the monthly report provides variance reporting highlighting any discrepancies against budget.

It should also be noted that should Council decide not to adopt the recommendations, it could lead to some initiatives being delayed or cancelled in order to offset the additional expenditure associated with running the Shire’s operations.

STRATEGIC ASPIRATIONS

Performance – We will deliver excellent governance, service and value, for everyone.

Outcome Eleven – Effective leadership, advocacy and governance:

11.2 Deliver best practice governance and risk management.

Outcome Thirteen - Value for money from rates and long term financial sustainability:

13.1 Plan effectively for short and long term financial sustainability.

VOTING REQUIREMENTS

|

(Report Recommendation) Minute No. AR/0222/003 Moved: Cr C Mitchell Seconded: Cr B Rudeforth That the Audit and Risk Committee recommends that Council: 1. Receives the Quarter 2 Finance and Costing Review Report for the period ended 31 December 2021; 2. Adopts the operating and capital budget amendment recommendations for the year ended 30 June 2022 as attached; 3. Notes a forecast net end-of-year deficit position to 30 June 2022 of $53,691.

|

|

2021-22 Q2 FACR Review |

Minutes – Audit and Risk Committee Meeting 17 February 2022 Page 1 of 4

|

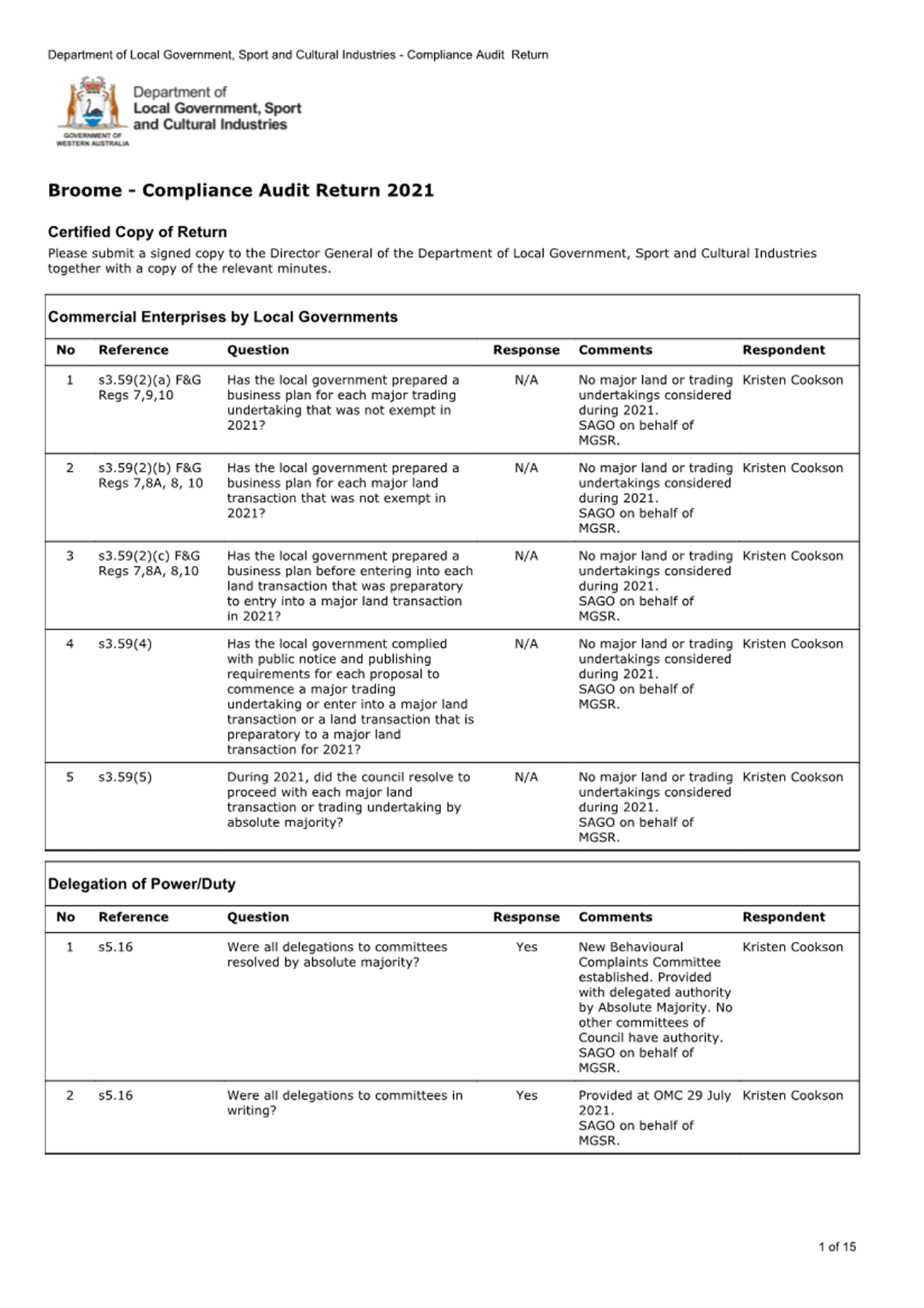

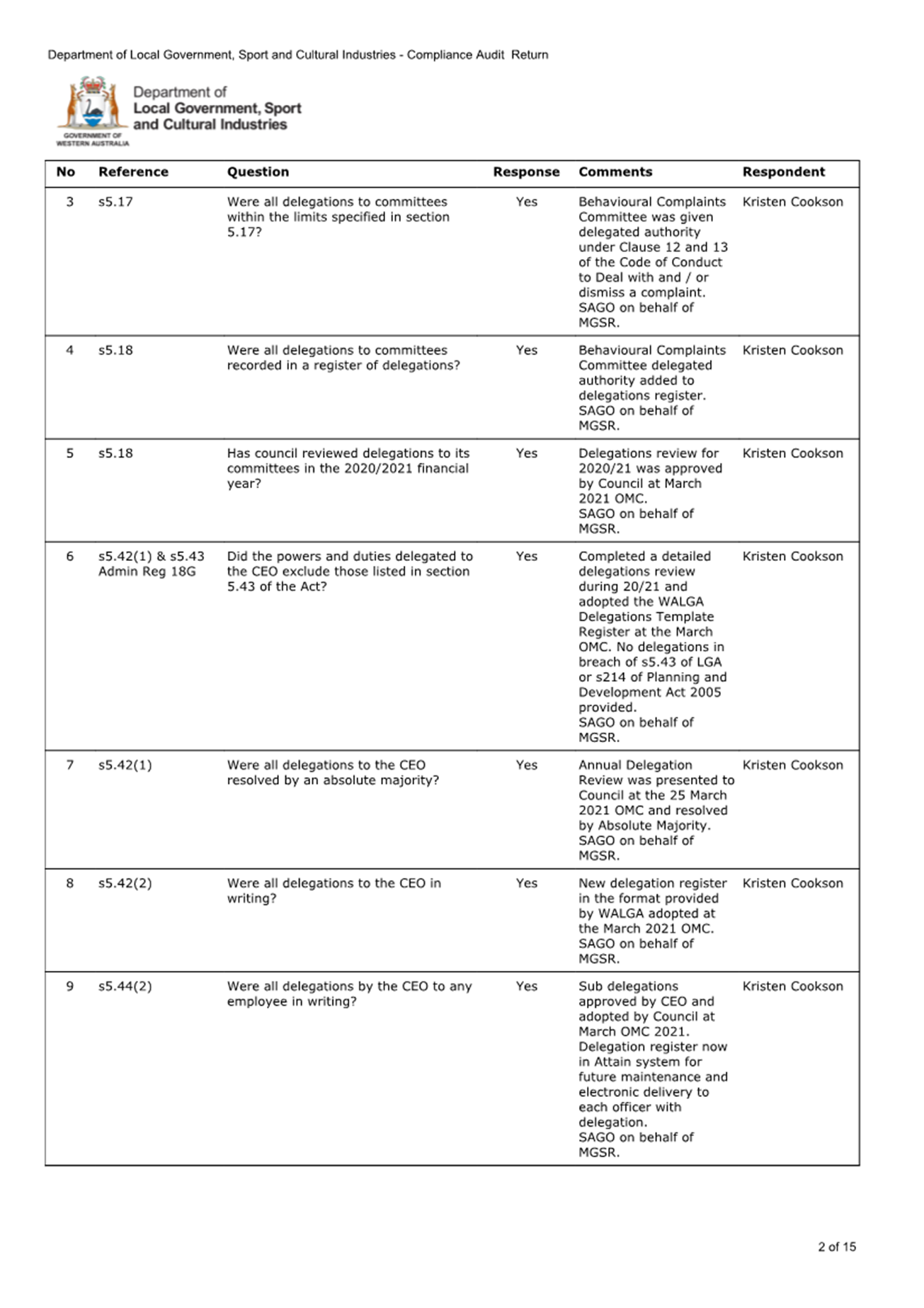

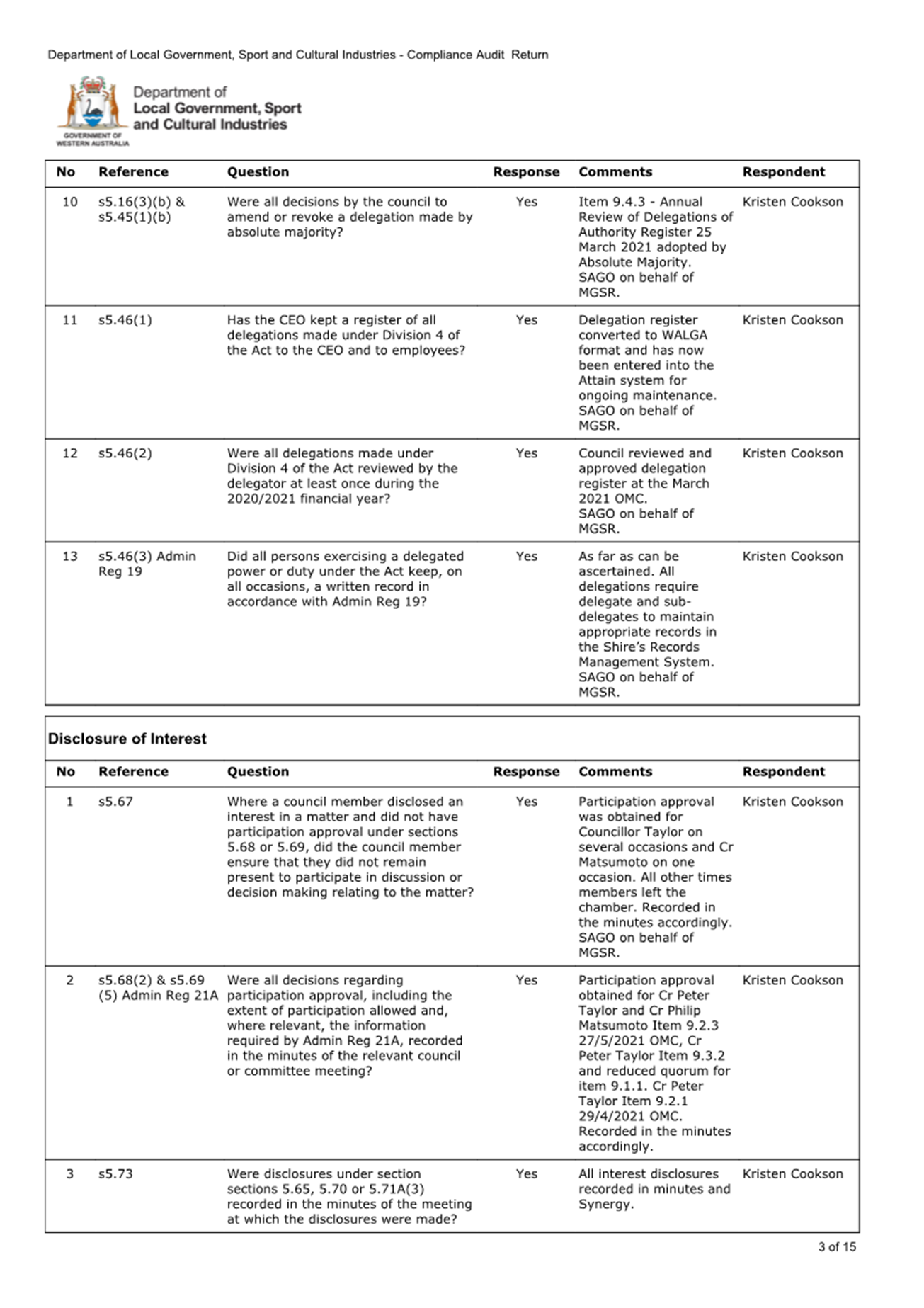

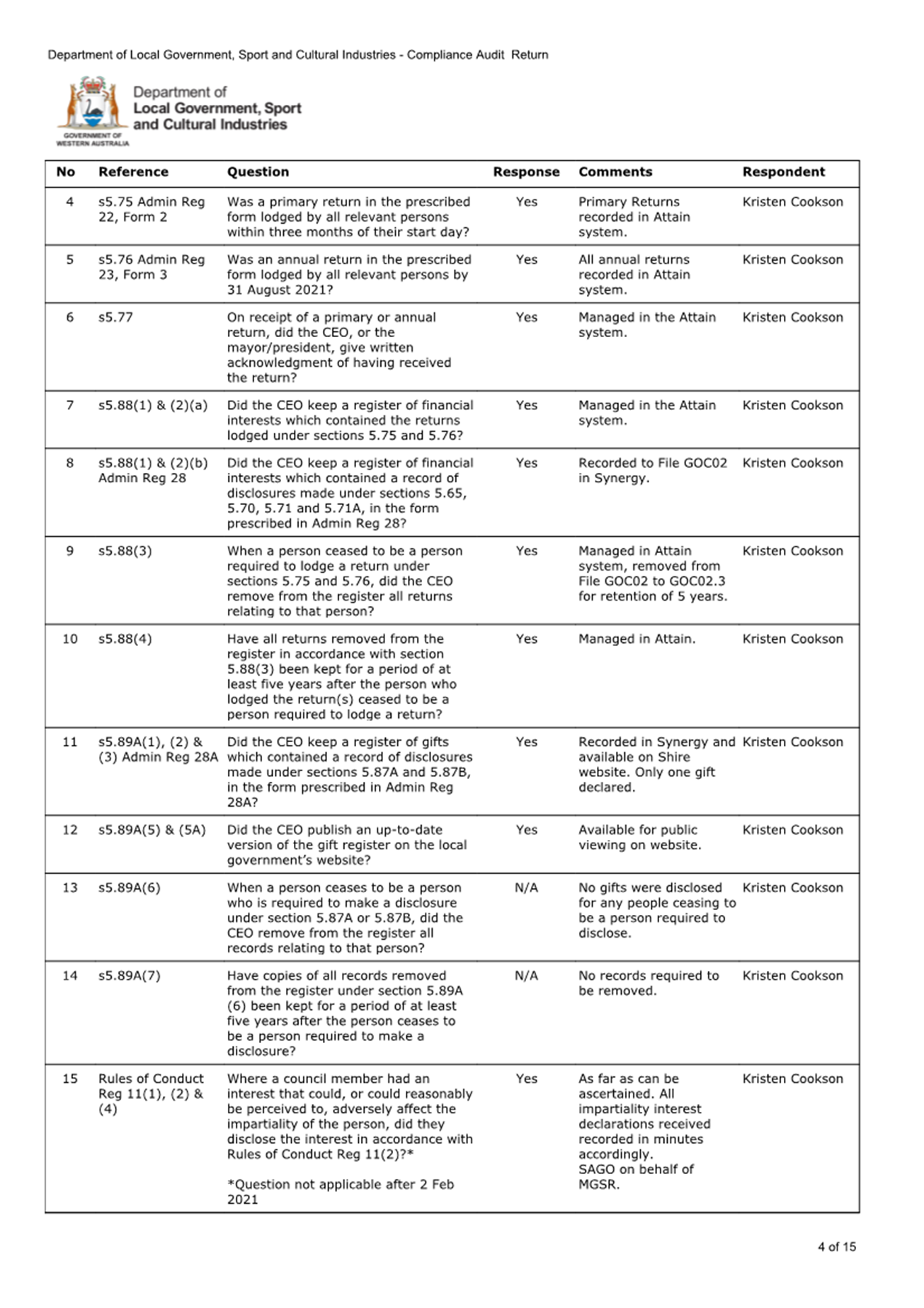

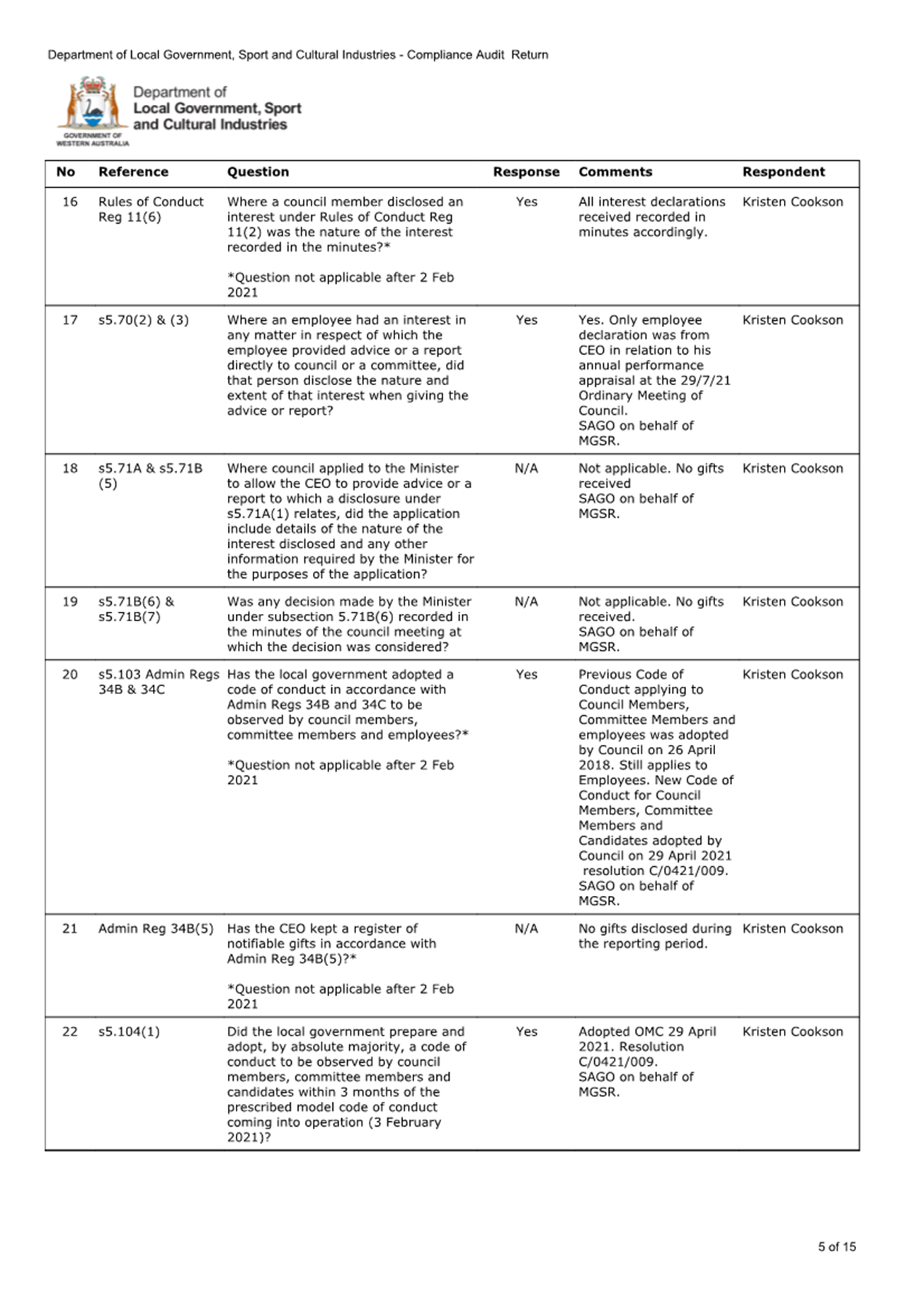

SUMMARY: The purpose of this report is to present to the Audit and Risk Committee (ARC) the 2021 Compliance Audit Return (CAR) for review, and to request that the ARC recommend that Council adopt the 2021 CAR for submission to the Department of Local Government, Sport and Cultural Industries (DLGSC) by 31 March 2022. |

Previous Considerations

Local governments are required to complete a compliance audit for the previous calendar year by the 31 March. The DLGSC provides the questions each year with the compliance audit being an in-house self audit that is undertaken by the appropriate responsible officer.

In accordance with Regulation 14 of the Local Government (Audit) Regulations 1996 the ARC is to review the CAR and is to report to Council the results of that review. The CAR is to be:

1. presented to an Ordinary Meeting of Council

2. adopted by Council; and

3. recorded in the minutes of the meeting at which it is adopted.

Following the adoption by Council of the CAR, a certified copy of the return, along with the relevant section of the minutes and any additional information detailing the contents of the return are to be submitted to the DLGSC by 31 March 2022.

The return requires the Shire President and the Chief Executive Officer to certify that the statutory obligations of the Shire of Broome have been complied with.

COMMENT

The DLGSC continues to focus on high risk areas of compliance and statutory reporting as prescribed in Regulation 13 of the Local Government (Audit) Regulations 1996.

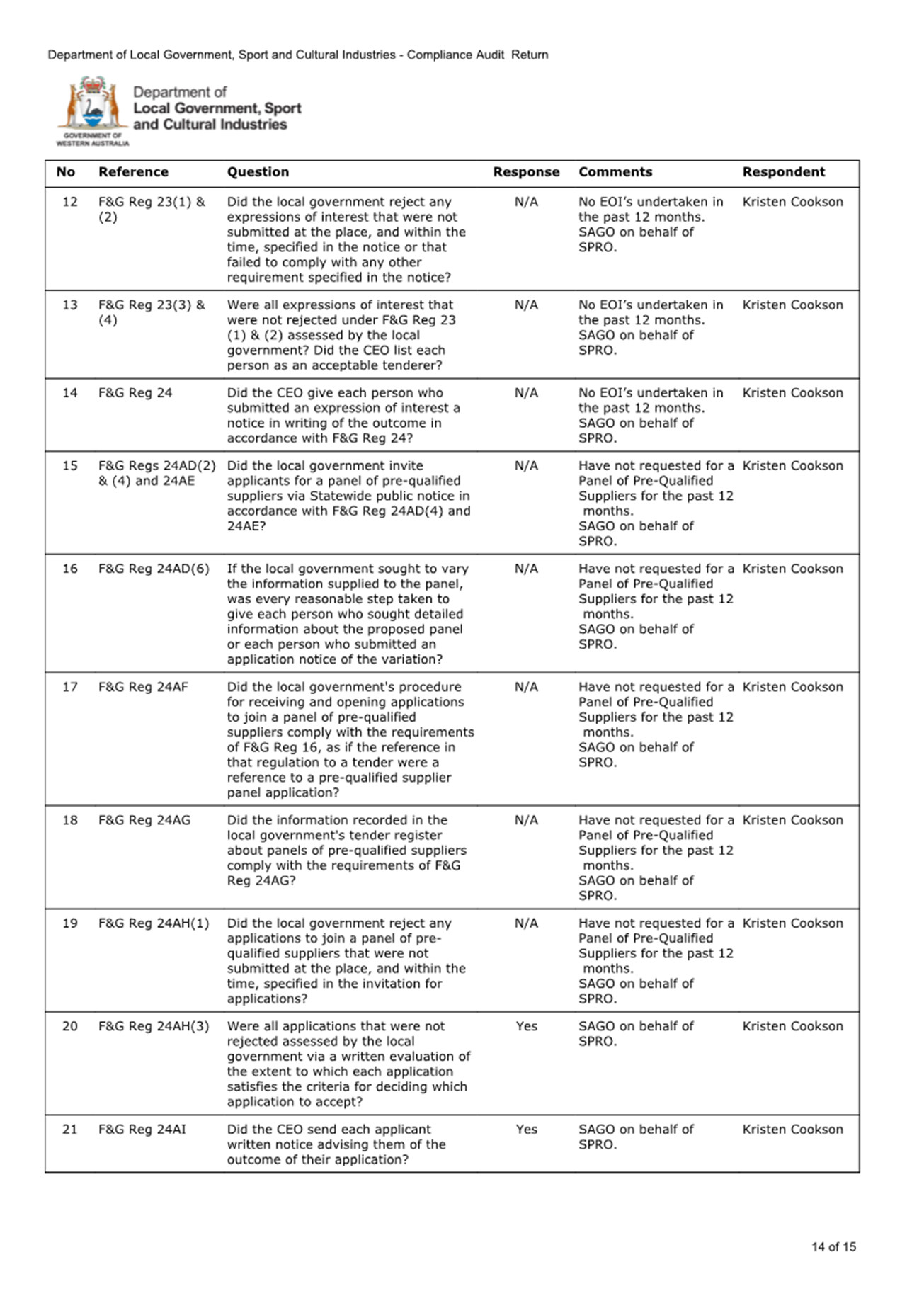

The CAR for the period 1 January to 31 December 2021 comprises a total of 98 questions, down from 102 questions the previous year. Whilst the number of questions is similar, the DLGSC has combined questions of a similar nature. New questions have appeared for the first time to reflect the legislative changes that are occurring, and this trend is expected to continue.

The key focus areas covered in the CAR are as follows:

|

Focus Area |

2020 Q’s |

2021 Q’s |

Comments |

|

Commercial Enterprises by Local Governments |

5 |

5 |

No change. |

|

Delegation of Power/Duty |

13 |

13 |

No change. |

|

Disclosure of Interest |

21 |

25 |

Several questions only applicable up until 2 Feb 2021 prior to mandatory code of conduct for council members, committee members and candidates being implemented.

New questions relating to the provisions of the adopted code of conduct for council members, committee members and candidates and separate code of conduct for employees. |

|

Disposal of Property |

2 |

2 |

No change. |

|

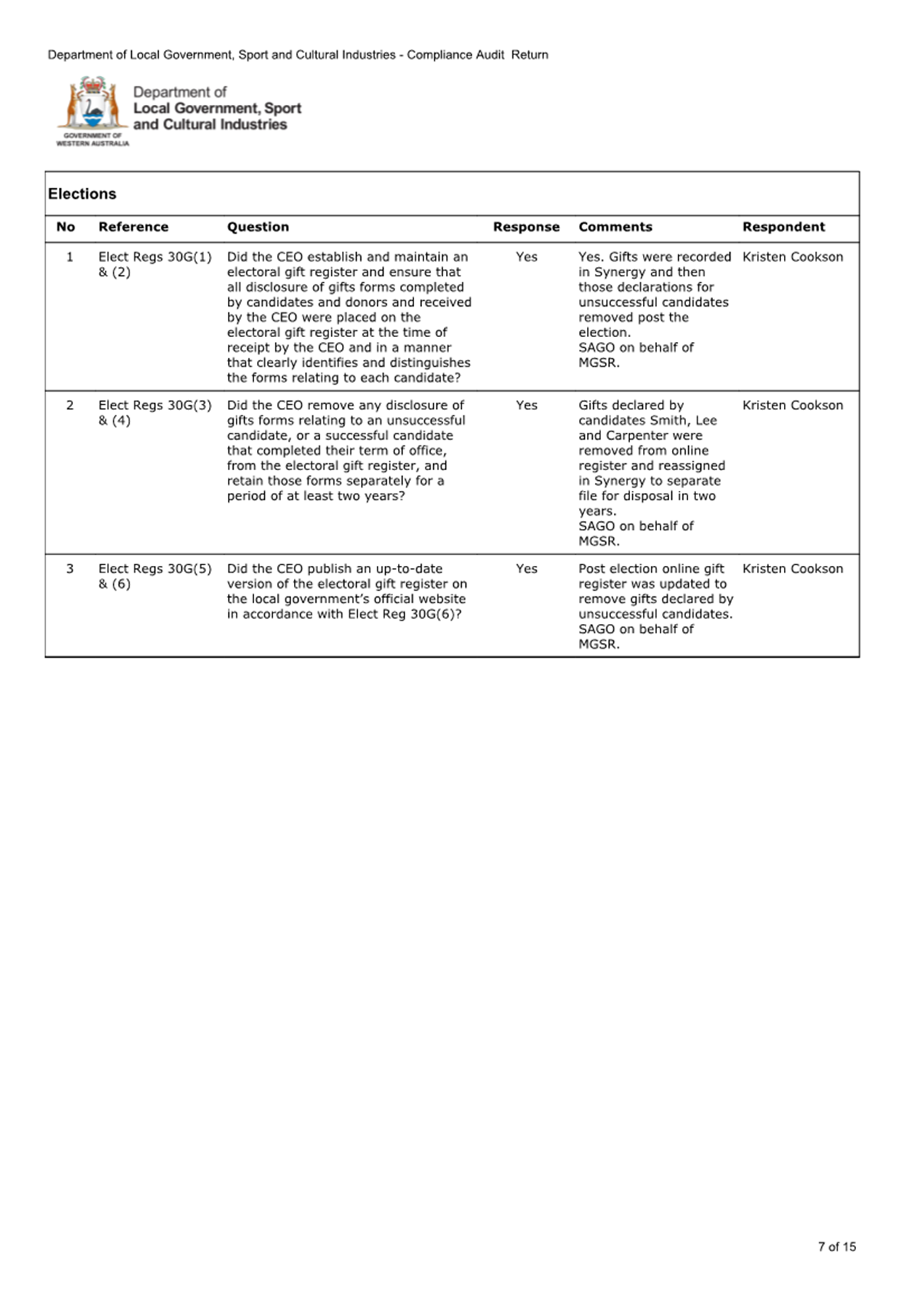

Elections |

3 |

3 |

No change. |

|

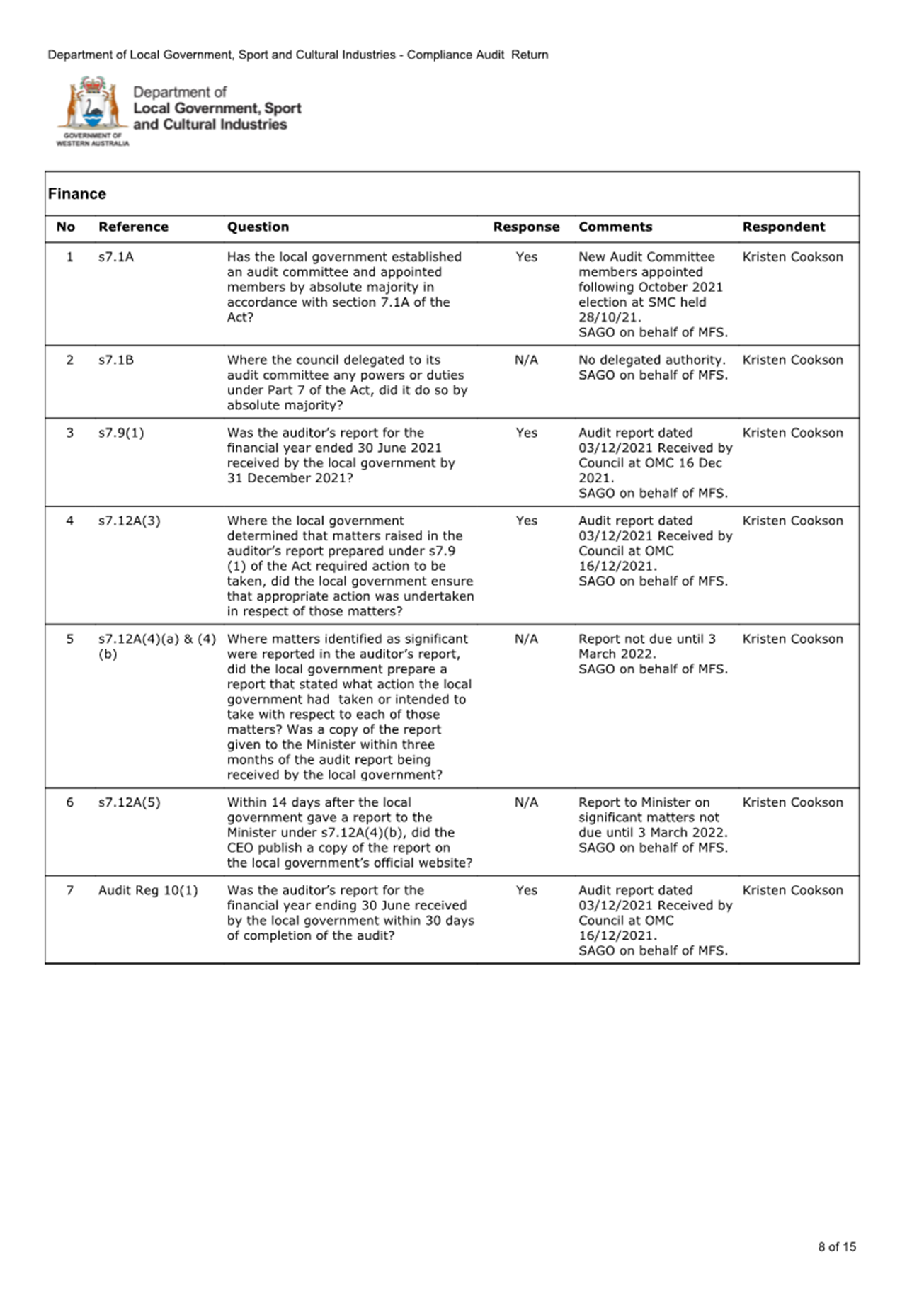

Finance |

11 |

7 |

Questions relating to the appointment of the auditor removed as Office of the Auditor General has taken on this role.

Question relating to Audit Reg 7 – Agreements with auditors removed.

Amalgamation of questions relating to significant audit matters, s7.12A(4)(a) & (4)(b) into one question. |

|

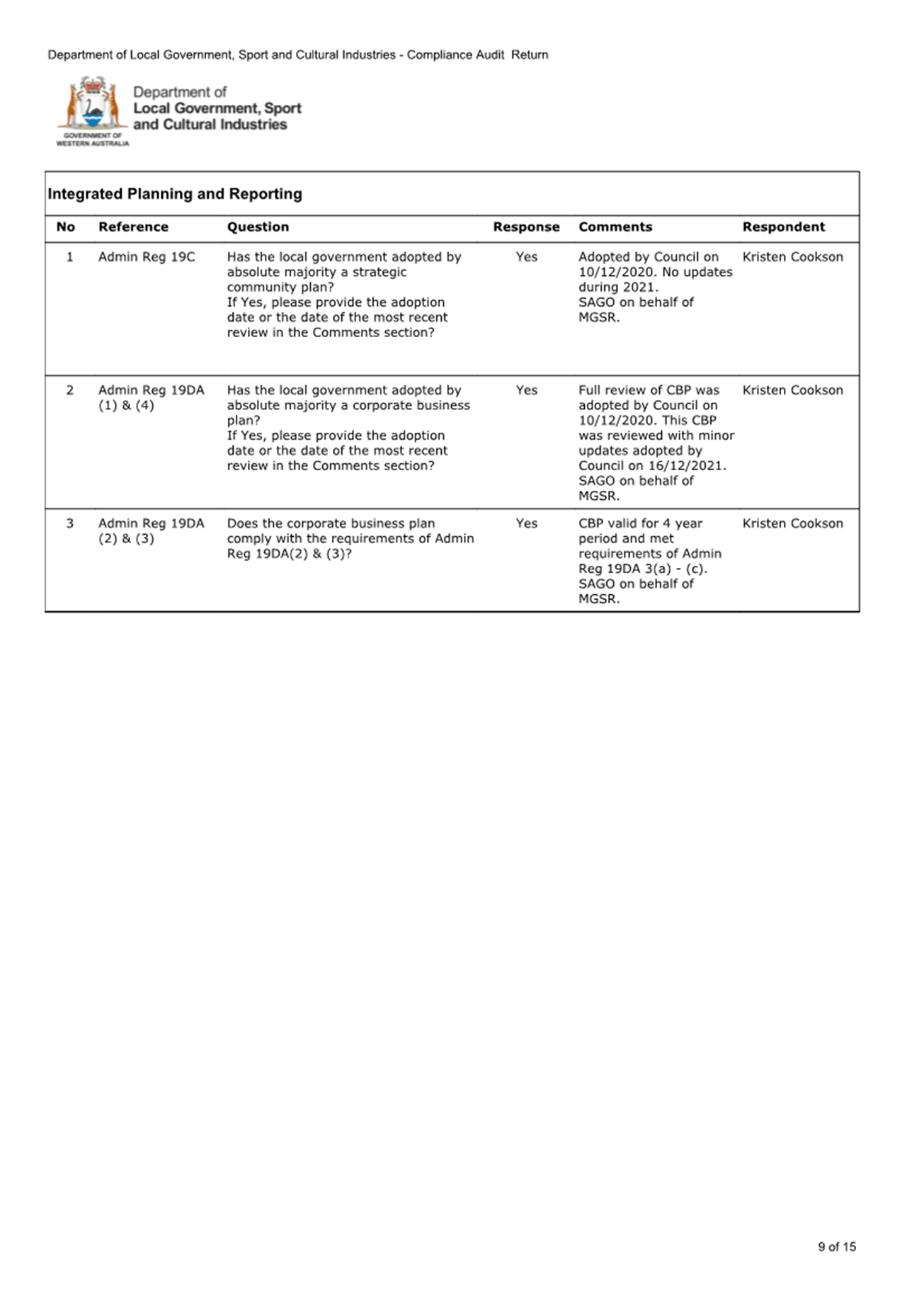

Integrated Planning and Reporting |

7 |

3 |

No change. |

|

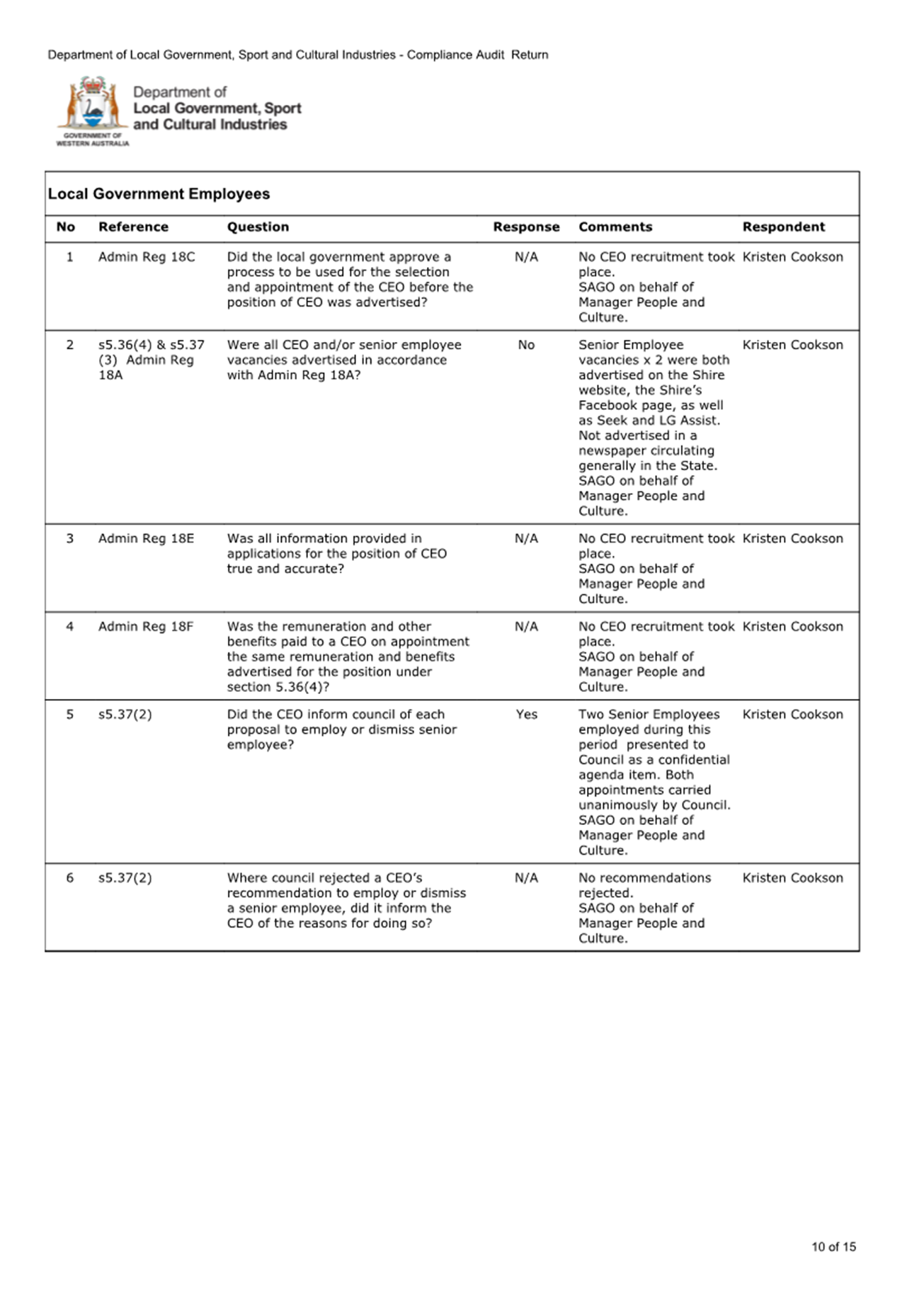

Local Government Employees |

5 |

6 |

No change. |

|

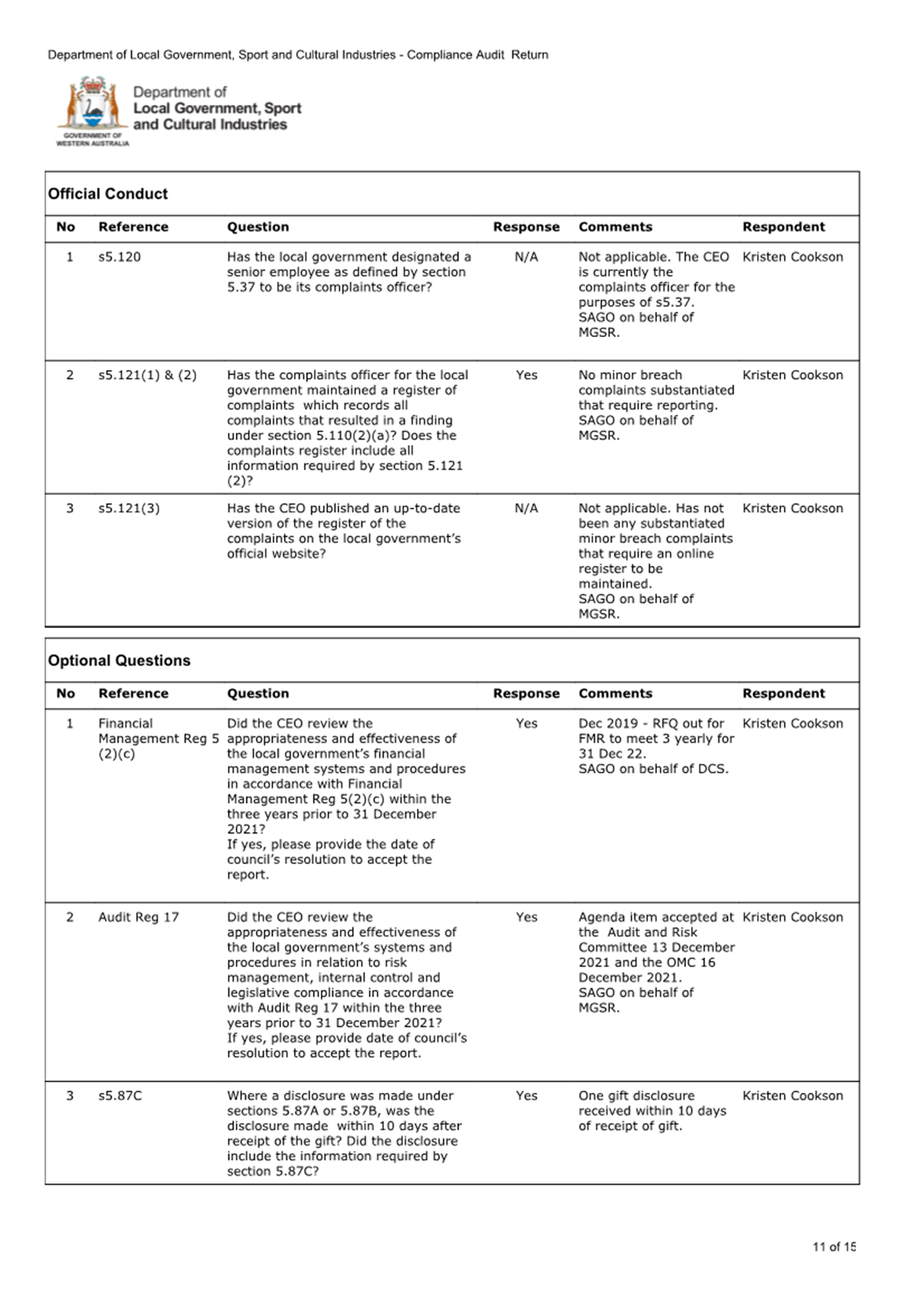

Official Conduct |

4 |

3 |

Amalgamation of questions relating to the complaints register into one question. |

|

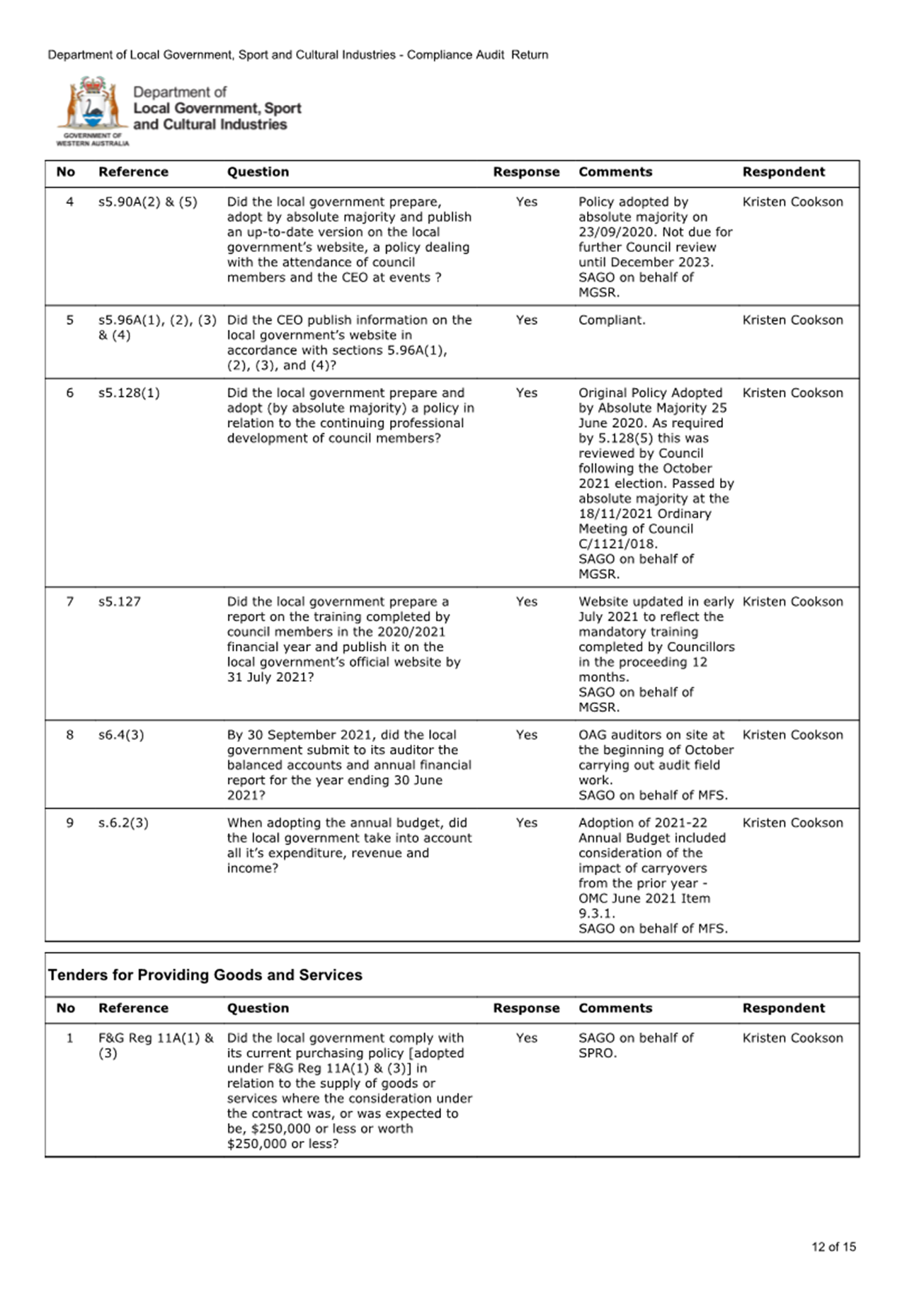

Optional Questions |

10 |

9 |

Amalgamation of questions relating to gift disclosures into one question.,

Amalgamation of questions relating to the attendance of elected members and the CEO at events policy into one question.

New question relating to adopting the budget. |

|

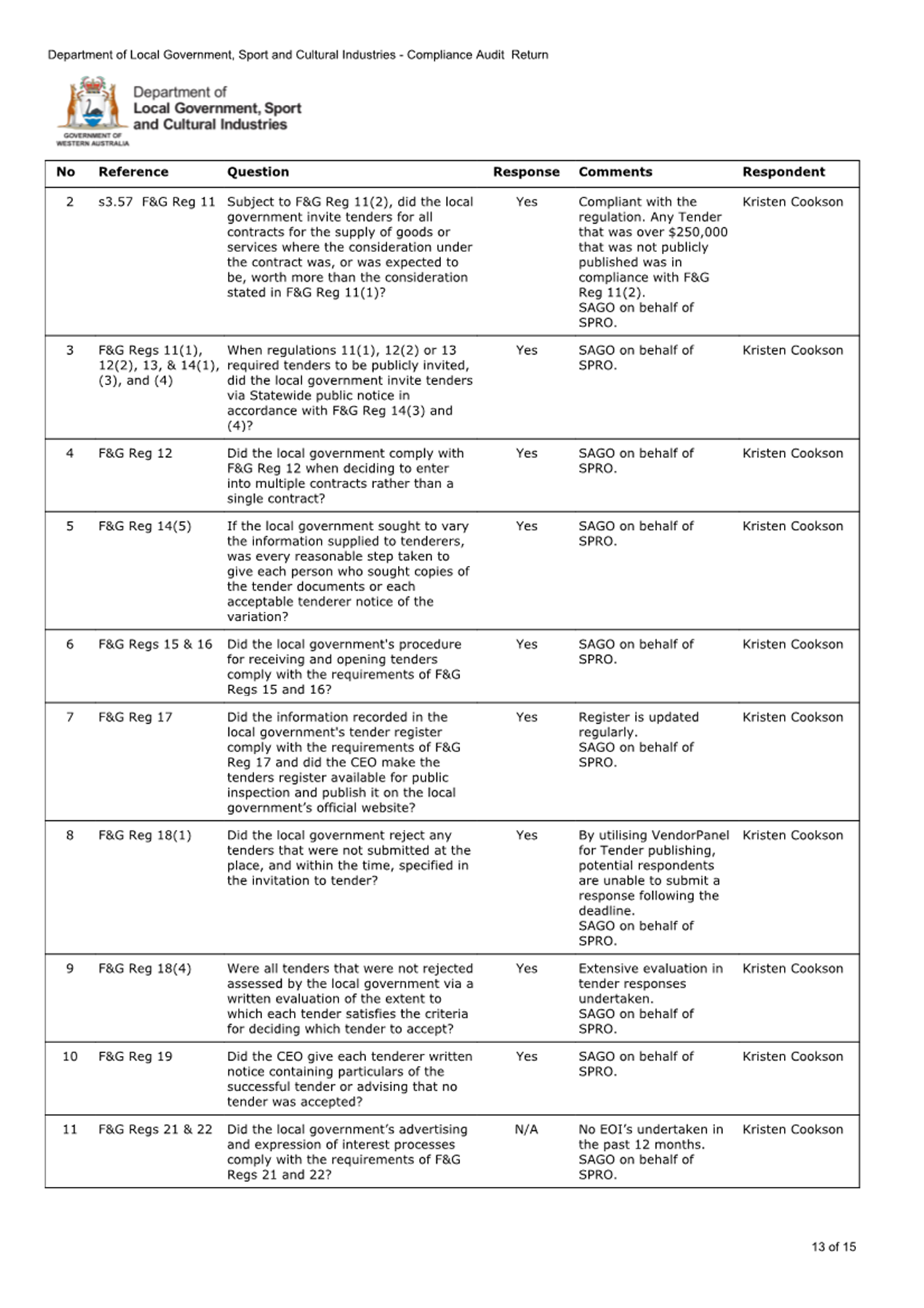

Tenders for Providing Goods and Services |

24 |

22 |

Amalgamation of questions relating to purchases for $250,000 or less into one question.

Amalgamation of questions relating to expression of interests F&G Reg 23(3) & (4) into one question. |

|

Total |

102 |

98 |

|

During 2021, responsible officers monitored compliance in each of the focus areas through the Shire’s cloud-based compliance system, RelianSys. This has continued to increase the awareness of compliance obligations and allowed the capture of compliance evidence in one central repository throughout the year. This compliance system reduces the risk of noncompliance and streamlines compilation of the annual return.

A compliance rating of 98% has been achieved for 2021 with 2 minor non compliances identified as follows:

|

Focus Area |

Question |

Comments |

|

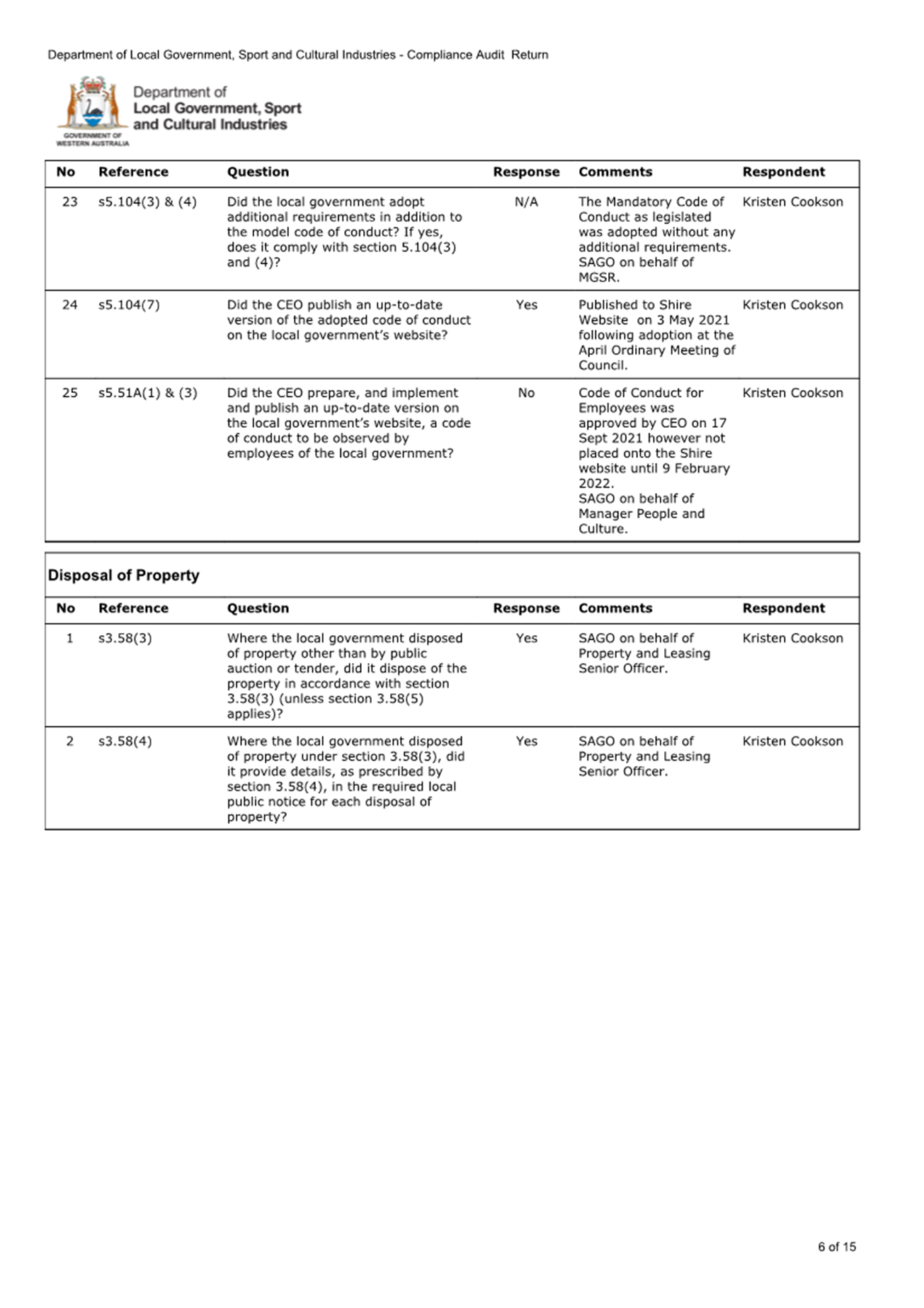

Disclosure of Interest |

(25) – Did the CEO prepare, and implement and publish an up-to-date version on the local government’s website, a code of conduct to be observed by employees of the local government?

|

Code of Conduct for Employees was approved by the CEO on 17 September 2021 however not placed on the Shire website until 9 February 2022.

|

|

Local Government Employees |

(2) - Were all CEO and/or senior employee vacancies advertised in accordance with Admin Reg 18A? |

There were 2 senior employee vacancies filled during 2021. These were extensively advertised on the Shire’s website, Facebook page, as well as Seek and LG Assist.

Under Admin Regulation 18A, CEO or senior employee vacancies require Statewide public notice.

One of the requirements for Statewide public notice is publication in a newspaper circulating generally in the State (The West Australian), that was not completed for these appointments. |

The CAR result continues the Shire’s strong history of compliance with the requirements of the Local Government Act (1995), with minimal non compliances reported over the last 5 years and none of a significant risk nature.

It is important to emphasise that the CAR is limited in scope.

Local Governments are also required to comply with upwards of 200 other pieces of legislation. The use of the RelianSys Compliance system during 2021 provided the ability to continually improve the monitoring and assurance of other significant pieces of legislation on a prioritised basis.

CONSULTATION

Department of Local Government, Sport and Cultural Industries

STATUTORY ENVIRONMENT

Local Government (Audit) Regulations 1996

14. Compliance audits by local governments

(1) A local government is to carry out a compliance audit for the period 1 January to 31 December in each year.

(2) After carrying out a compliance audit the local government is to prepare a compliance audit return in a form approved by the Minister.

(3A) The local government’s audit committee is to review the compliance audit return and is to report to the council the results of that review.

(3) After the audit committee has reported to the council under subregulation (3A), the compliance audit return is to be —

(a) presented to the council at a meeting of the council; and

(b) adopted by the council; and

(c) recorded in the minutes of the meeting at which it is adopted.

15. Compliance audit return, certified copy of etc. to be given to Departmental CEO

(1) After the compliance audit return has been presented to the council in accordance with regulation 14(3) a certified copy of the return together with —

(a) a copy of the relevant section of the minutes referred to in regulation 14(3)(c); and

(b) any additional information explaining or qualifying the compliance audit,

is to be submitted to the Departmental CEO by 31 March next following the period to which the return relates.

POLICY IMPLICATIONS

Nil.

FINANCIAL IMPLICATIONS

Nil.

RISK

There is a reputational risk with the DLGSC should the CAR not be completed on time or if significant non compliances are reported.

The likelihood of this occurring is rare.

STRATEGIC ASPIRATIONS

Performance – We will deliver excellent governance, service and value, for everyone.

Outcome Eleven – Effective leadership, advocacy and governance:

11.2 Deliver best practice governance and risk management.

VOTING REQUIREMENTS

|

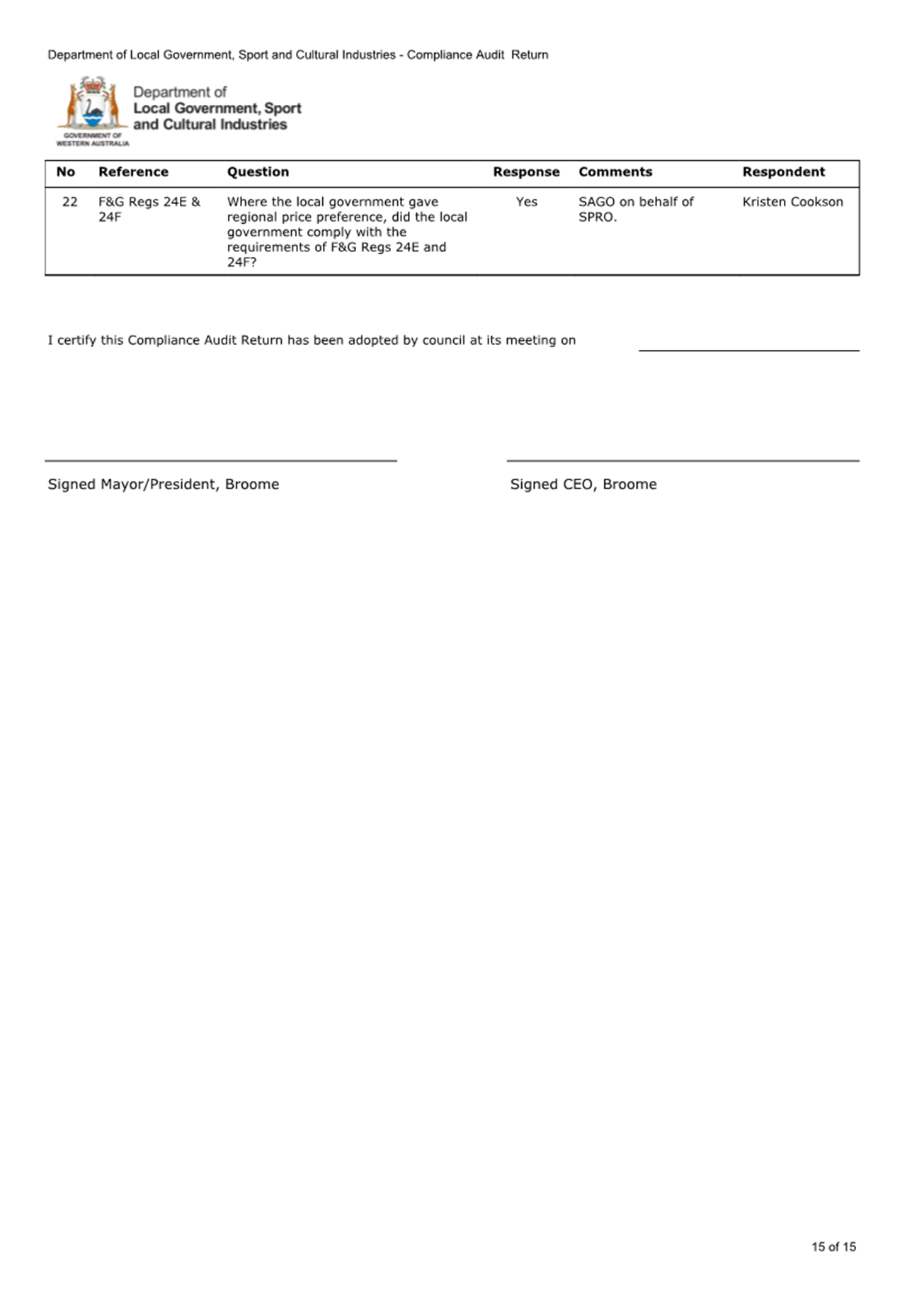

(Report Recommendation) Minute No. AR/0222/004 Moved: Cr D Male Seconded: Cr B Rudeforth That the Audit and Risk Committee recommends that Council: 1. Adopt the attached 2021 Compliance Audit Return as the official return for the Shire of Broome; and 2. Requests the Chief Executive Officer to submit the certified return and a copy of the minutes relative to this report to the Department of Local Government, Sport and Cultural Industries prior to 31 March 2022.

|

|

Compliance Audit Return 2021 |

Minutes – Audit and Risk Committee Meeting 17 February 2022 Page 1 of 4

|

SUMMARY: Section 7.12A(4)(a) of the Local Government Act 1995 (the Act) requires that a local government must prepare a report addressing any matters identified as significant by the auditor in the audit report, and stating what action the local government has taken or intends to take with respect to each of those matters. The report is required to be provided to the Minister within 3 months after the audit report is received by the local government. The purpose of this item is to seek the Audit and Risk Committee’s endorsement of the attached report addressing the Significant Matters raised in the Office of the Auditor General’s (OAG) 2020-21 Audit Report. |

Previous Considerations

OMC 16 December 2021 Item 13.1

Under section 7.9 of the Local Government Act 1995 (the Act), an Auditor is required to examine the accounts and annual financial report submitted by a local government for audit. The Auditor is required to prepare a report thereon by 31 December following the financial year to which the accounts and report relate and forward a copy of that report to:

(a) The Mayor or President;

(b) The Chief Executive Officer (CEO); and

(c) The Minister.

Furthermore, under Regulation 10(4) of the Local Government (Audit) Regulations 1996 (Audit Regulations), where it is considered appropriate to do so, the Auditor may prepare a Management Report to accompany the Auditor’s Report, which is also to be forwarded to the persons specified in section 7.9 of the Act.

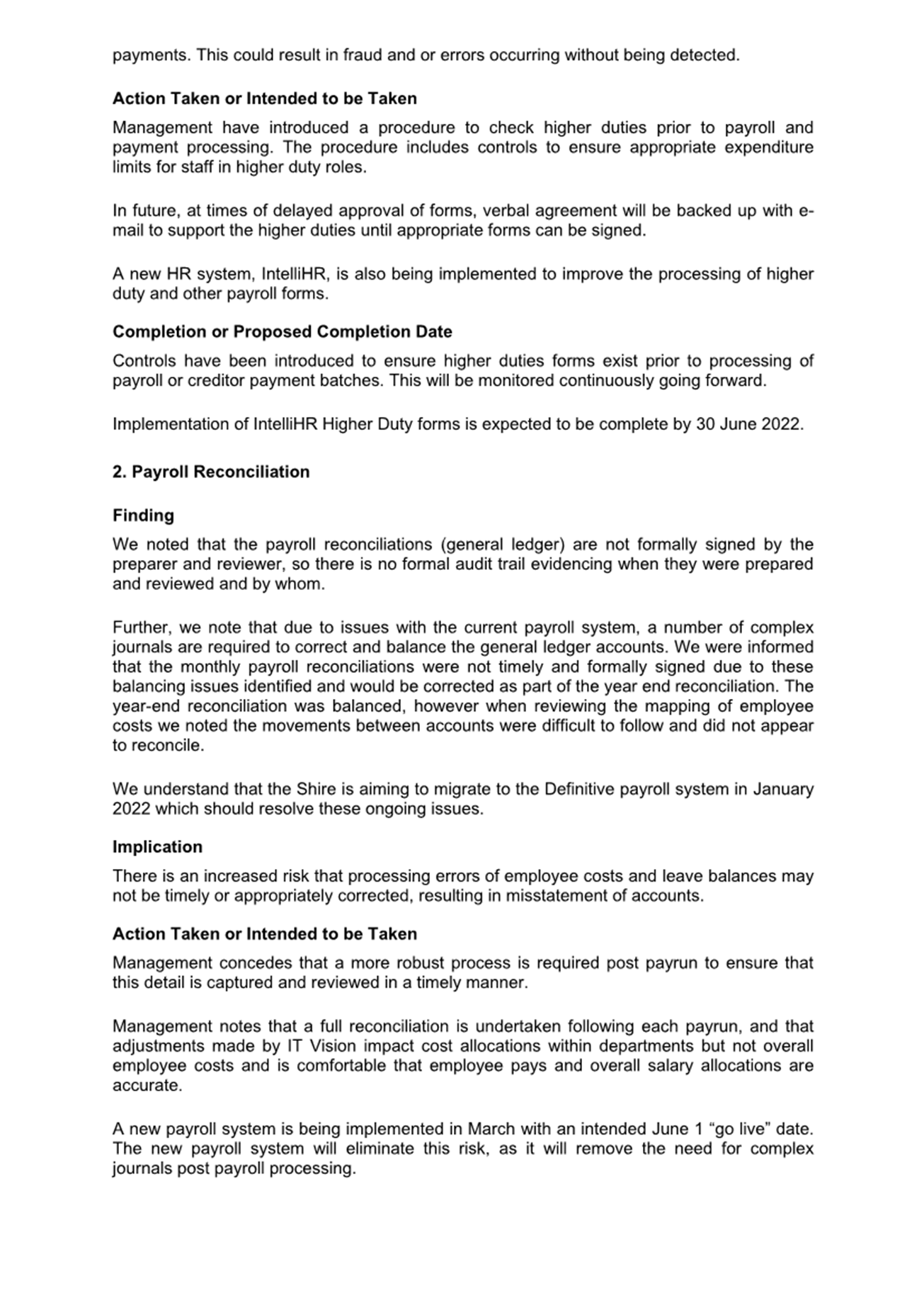

The Audit Report’s were presented to the Audit and Risk Committee (the Committee) on 13 December 2021. The Auditor’s Management Report provided an overview of the approach undertaken in respect of the annual Audit process and the associated outcomes of the audit. The Management Report identified 10 Significant Matters that, whilst generally not material in relation to the overall audit of the financial report, are considered relevant to the day-to-day operations of the Shire. Of the 10 Significant Matters, 3 were identified as new issues during the 2020-21 Audit, and 7 minor or moderate matters previously identified in the 2019-20 audit were escalated to significant.

The Committee recommended that Council receive the Auditor’s reports along with the Chief Executive Officer’s (CEO) report relating to the Audit. The Audit Report’s were subsequently received and adopted by Council at its Ordinary Meeting held 16 December 2021.

Under section 7.12A of the Act, Council must prepare a report addressing any matters identified as significant by the auditor in the Audit Report, and state what action Council has taken or intends to take with respect to each of those matters. The report is to be provided to the Audit and Risk Committee and Council for endorsement, with a copy provided to the Minister within 3 months of the audit report being received by Council.

A report is required to be tabled with the Minister for Local Government by 16 March 2021.

COMMENT

Following the December OMC officer’s have drafted a report addressing the Significant Matters identified during the OAG 2020-21 Audit (Attachment 1). The report outlines the actions undertaken, or planned to be undertaken, in response to the issues identified and includes comment on the timing of any proposed actions.

It is noted that due to the Audit Report being received by Council in December 2021 that there have been limited improvements enacted due to the impact of the Christmas leave period.

CONSULTATION

Office of the Auditor General

STATUTORY ENVIRONMENT

Local Government Act 1995

s5.53 Annual reports

s5.54 Acceptance of Annual Reports

s6.4 Financial Report

s7.9 Audit to be conducted

s7.12A Duties of a local government with respect to audits

POLICY IMPLICATIONS

Nil.

FINANCIAL IMPLICATIONS

Nil, noting there may be minor operational cost implications relating the implementation of procedures and controls required to address the matters raised.

RISK

The audited Annual Financial Report is a key control measure used to report to Council and its stakeholders that Council’s financial position, result of operations, cash flows, changes in equity and rate setting statement are free from any material misstatement caused by fraud or error. The audit findings have identified areas requiring improvement and this item presents a report detailing the actions proposed to address these issues. Should the Committee or Council not support the item recommendation, there is a risk that the 3 month deadline for submission of the report to the Minister will not be met, resulting in a compliance risk.

STRATEGIC ASPIRATIONS

Performance – We will deliver excellent governance, service and value, for everyone.

Outcome Eleven – Effective leadership, advocacy and governance:

11.2 Deliver best practice governance and risk management.

Outcome Fourteen – Excellence in organisational performance and service delivery:

14.3 Monitor and continuously improve performance levels.

VOTING REQUIREMENTS

|

(Report Recommendation) Minute No. AR/0222/005 Moved: Cr C Mitchell Seconded: Cr B Rudeforth That the Audit and Risk Committee recommends that Council: 1. Receive and endorse the report addressing the Significant Matters identified by the Office of the Auditor General during the 2020-21 Audit as attached; and 2. Authorises the report to be forwarded to the Minister for Local Government and be published on the Shire website. |

|

REPORT ON SIGNIFICANT AUDIT MATTERS 2020-2021 |

Minutes – Audit and Risk Committee Meeting 17 February 2022 Page 1 of 4

Nil

There being no further business the Chair declared the meeting closed at 1:13 PM.