CONFIRMED

MINUTES

OF THE

Special Meeting of Council

12 May 2022

|

These minutes were confirmed at a meeting held 26 May 2022 and signed below by the Presiding Person, at the meeting these minutes were confirmed.

|

CONFIRMED

MINUTES

OF THE

Special Meeting of Council

12 May 2022

|

These minutes were confirmed at a meeting held 26 May 2022 and signed below by the Presiding Person, at the meeting these minutes were confirmed.

|

Minutes – Special Meeting of Council 12 May 2022 Page 1 of 2

SHIRE OF BROOME

Special Meeting of Council

Thursday 12 May 2022

INDEX – Minutes

3. Declarations Of Financial Interest / Impartiality

5.3.1 NOTICE OF INTENTION TO IMPOSE 2022/23 DIFFERENTIAL RATES

MINUTES OF THE Special Meeting of Council OF THE SHIRE OF BROOME,

HELD IN THE Council Chambers, Corner Weld and Haas Streets, Broome, ON Thursday 12 May 2022, COMMENCING AT 4:30PM.

The Chairperson welcomed Councillors, Officers and members of the public and declared the meeting open at 4:39PM.

|

ATTENDANCE |

|

|

|

|

|

|

|

Councillors: |

Cr H Tracey |

Shire President (Via e-meeting) |

|

|

Cr D Male |

Deputy Shire President (Chair) |

|

|

Cr P Matsumoto |

|

|

|

Cr B Rudeforth |

|

|

|

Cr P Taylor |

|

|

|

Cr N Wevers |

|

|

|

||

|

Apologies: |

Cr E Foy |

|

|

|

Cr C Mitchell |

|

|

|

||

|

Leave of Absence: |

Nil |

|

|

|

|

|

|

|

||

|

Officers: |

Mr S Mastrolembo |

Chief Executive Officer |

|

|

Mr J Watt |

Director Corporate Services |

|

|

Ms Elizabeth French |

Manager Financial Services |

|

|

Miss K Cookson |

Senior Administration & Governance Officer |

|

|

|

|

|

|

|

|

|

|

||

|

Public Gallery: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nil.

Nil.

5.1 People

There are no reports in this section.

There are no reports in this section.

|

|

|

Minute No. C/0522/024 Moved: Cr N Wevers Seconded: Cr P Taylor That Meeting Procedures be suspended in accordance with Clause 16.1 of the Meeting Procedures Local Law at 4:41pm. |

|

Minute No. C/0522/025 Moved: Cr D Male Seconded: Cr N Wevers That Meeting Procedures be reinstated in accordance with Clause 16.1 of the Meeting Procedures Local Law at 5:12pm |

|

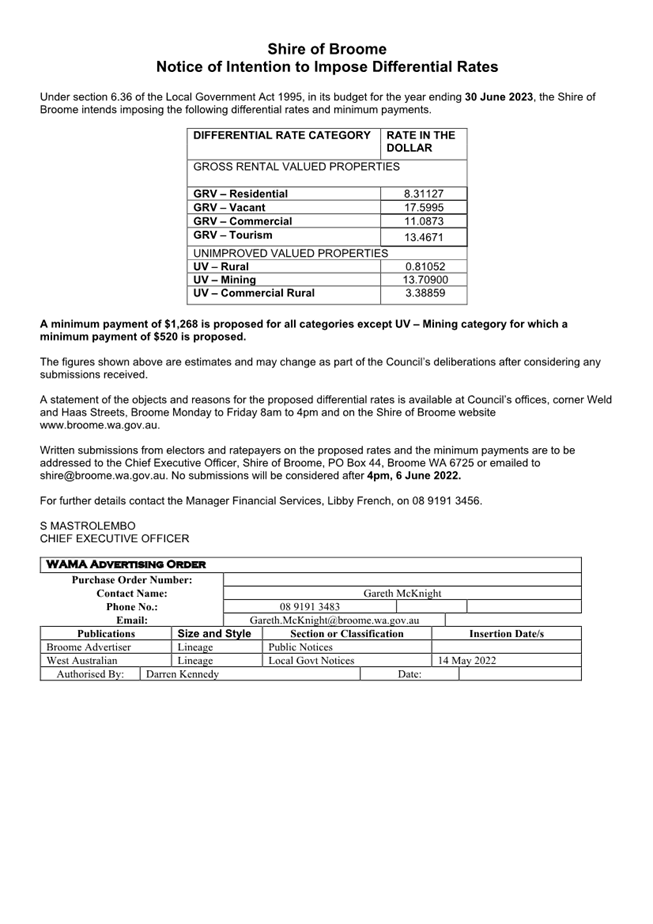

SUMMARY: As part of the 2022/23 budget process, Council is required to endorse the proposed differential rates for local public notice seeking public comment for not less than 21 days. The local public notice provides an opportunity to consider public submissions before the final adoption of rates. In summary, the proposed rates for the 2022/23 financial year required a general rate increase of 4% to balance the draft budget for 2022/23. Minimum rates for the UV Mining rating category is proposed to increase by $20 to $520 after remaining unchanged for several years. Likewise the Minimum payments on all other properties are proposed to increase by $48 to $1,268. |

BACKGROUND

Previous Considerations

The purpose of levying rates is to meet Council’s budget requirements to deliver services and community infrastructure in each financial year. The rates levied on properties is equal to the applicable property valuation multiplied by the relevant differential rating categories “rate in the dollar”. The Minister for Local Government (the Minister) determines the methods of land valuation with property valuations undertaken by the Valuer General’s Office (VGO).

The application of differential rates considers section 6.33 of the Local Government Act 1995 (the Act), enabling the rating of properties differentially, based on zoning and/or land use as determined by the local government.

Section 6.35 of the Act also provides the ability to impose a minimum payment higher than the general rate that would otherwise be payable on that land. The application of differential rating based on land use and/or zoning results in a rate in the dollar and minimum payment amounts for each rating category.

Under section 6.36 of the Act, a local government must give local public notice of its intention to impose general differential rates (including minimum payments).

The application of differential rates and minimum payments maintains equity in the rating of properties across the Shire of Broome (the Shire), enabling Council to provide facilities, infrastructure and services to the entire community and visitors.

This report has been developed to present to Council:

· The 2022/23 budget process to date including revenue required to be raised from rates as per the 2022/23 draft budget;

· The proposed rating categories and corresponding valuations;

· The proposed rate in the dollar for each rating category reflecting a 4% increase from the preceding year;

· The proposed minimum payments for each rating category;

· Details on the impact of 2019 UV Commercial Rural revaluation and subsequent objections affecting the yield in that rating category;

· An illustration of the proposed differential rates and minimum payments required to be raised to balance the 2022/23 budget;

· The statutory requirement to advertise certain rating information through public notice; and

· The statutory requirement to consider submissions received concerning the proposed rates.

Recommendations are also included in this report for Council’s consideration.

COMMENT

Summary of the Budget Process to Date and Revenue Required to be Raised from Rates

Several Council presentations and workshops have been held to date, including:

|

19 November 2021 |

Finalised Corporate Business Plan and Long Term Financial Plan; 4 Year Balanced Long Term Financial Plan |

|

23 March 2022 |

Draft Fees and Charges and Operating Budget (including Infrastructure Resource Budgets) |

|

5 April 2022 |

Capital Budget and Project Briefs, Plant Replacement |

|

9/11 May 2022 |

Rate Setting including analysis of impact of GRV Revaluations |

The Draft Operations Budget was discussed at the 23 March 2022 workshop and identified a deficit of a $18.4M operating deficit.

Capital and other special projects were discussed at the 5 April 2022 workshop. Council’s adopted Corporate Business Plan (CBP), Long Term Financial Plan (LTFP) and Asset Management Plans (AMP’s) were considered when developing the capital budget. Several project briefs submitted by staff and Councillors were also tabled with Council for consideration through the above workshops.

Following the Budget Workshop’s deliberations and feedback on 5 April 2022, minor amendments were made to the draft budget documents. As part of the budget workshops, which considered both the operating and capital requirements, it was identified that $24.95M of rate revenue was required to achieve a balanced budget in 2022/23, and this could be achieved through a general 4% rates increase.

Through Council’s quarterly budget review process (Finance and Costing Review) Quarter 3, the closing funding position for 2021/22 was identified as a budget deficit of $356,599, mainly attributable to the objections to valuations of 13 UV Commercial Rural properties being upheld, and backdated to 1 July 2020. Rates revenue lost from these objections totalled $288,362, equating to 1.2% of rates revenue for 2022/23.

Following Council workshops the March Quarter financial indicators were released and identified a March 2021 – March 20022 annual CPI increase of 7.6%.

Preparation of the 2022/23 budget was particularly challenging due to the following:

· Employee costs which account for $17M, are due to increase by 1.8% - 2.5% under relevant Enterprise Bargaining Agreements;

· Superannuation Guarantee Act mandatory super contributions to increase by a further 0.5%, after increasing by 0.5% in 2021-22;

· Continuing low interest rates which will keep return on cash investments at low levels;

· Increased costs of materials due to COVID and other global influences;

· Conservative growth in population and service usage, therefore, minimal growth in most user-paid services;

· Significant increases in Perth Consumer Price Index (CPI, 7.6%) with future forecasts indicating that CPI will remain high; and

· Increasing WA Local Government Cost Index (LGCI, 3%) with future forecasts indicating continuing increases in materials, fuel and other components.

Key achievements in this year’s budget include:

· Zero-based budgeting – all operational account budgets start at 0 not based on historical figures;

· Operational revenues, expenses and net results in line with the 2022/23 LTFP;

· A continued focus by officers to leverage Council funds to attract grant funding;

· $1.56M of revenue generated through commercial leases;

· Significantly reduced Waste Management Facility operating costs following internal review in 2021-22.

These factors have resulted in rates being contained within the general 4% increase across differential rating categories. This 4% increase is higher than the indicative figure of 1.85% included within the Shire’s LTFP primarily due to the recognition of several years of lower than CPI rate increases, along with current CPI and LGCI increases.

A minimum rate increase of $48, to $1,268, is recommended for all rating categories except for the UV-Mining category, which is recommended to increase by $20 to $520, to ensure compliance with section 6.35 of the Act (where no more than half of the properties in a rating category pay the minimum rates).

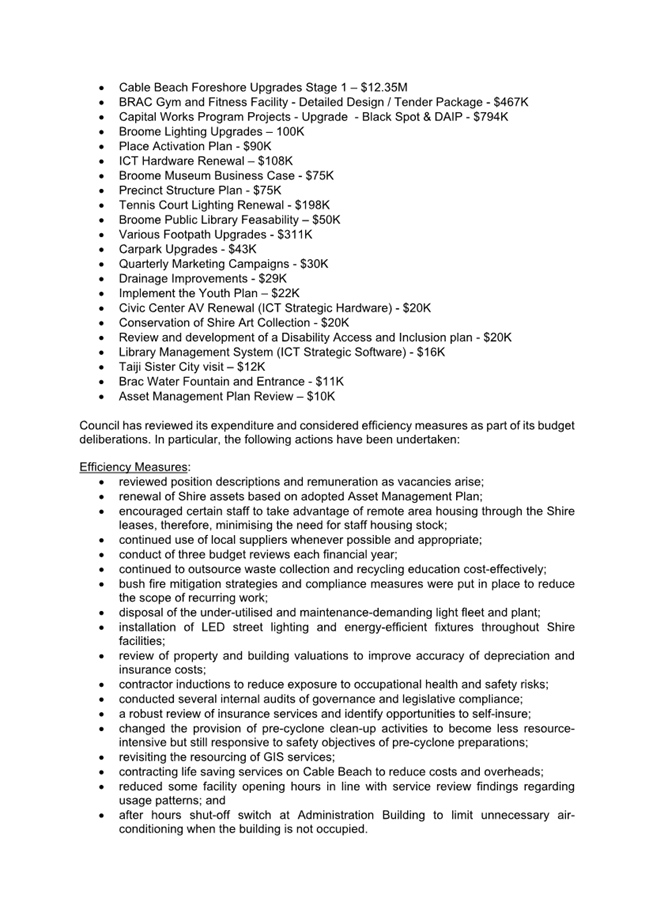

Despite the general 4% increase in rates, the Shire is aiming to deliver the following critical capital and special projects:

|

Projects |

Amount |

|

Cable Beach Foreshore Redevelopment |

$12.3M |

|

Regional Resource Recovery Park – Stage 1 Community Resource Centre |

$6.3M |

|

Asset Renewal Expenditure as per various Asset Management Plans |

$4.97M |

|

Capital Works Program Upgrades – Stewart Street |

$1.05M |

|

Port Drive – Guy Street Intersection Upgrades (Black Spot) |

$793K |

|

BRAC Dry Side Upgrade Business Case |

$467K |

|

Tennis Court Lighting Renewal |

$198K |

|

Bin Replacement |

$153K |

|

Information Communication and Technology Hardware Renewal |

$108K |

|

Streetlight Lighting Upgrades |

$100K |

|

Buckleys Road Waste Facility Rehabilitation and Capping |

$91K |

|

Broome Museum Business Case |

$75K |

|

Precinct Structure Plan |

$75K |

|

Vacuum Excavation Mobile Plant |

$58K |

|

Broome Library Business Case |

$50K |

|

Implement Cemetery Masterplan |

$50K |

|

Kimberley Regional Offices Window Security Screens (lessee co-contribution) |

$45K |

|

Council Chambers Live Streaming and Audio Upgrades |

$35K |

|

Sam Male Lugger restoration |

$30K |

|

Implement the Youth Plan |

$30K |

|

Quarterly Marketing Campaigns |

$30K |

|

Drainage Grate Improvements |

$25K |

|

Shoreline Monitoring |

$22.5K |

|

Home Composting Initiative |

$21K |

|

Conservation of Shire Art Collection |

$20K |

|

Civic Centre Audio Visual Renewal |

$20K |

|

Review of Disability Access and Inclusion Plan |

$20K |

|

Library Management System |

$16K |

|

Disability Access and Inclusion Upgrades |

$15K |

|

Frederick Street – Hamersley Street Intersection Lighting Upgrades (Black Spot) |

$14K |

|

BRAC Water Fountain and Entrance Upgrades |

$12K |

|

Asset Management Plan Review |

$10K |

The basis of the proposed rates modelling to achieve these capital projects and operational services are outlined below.

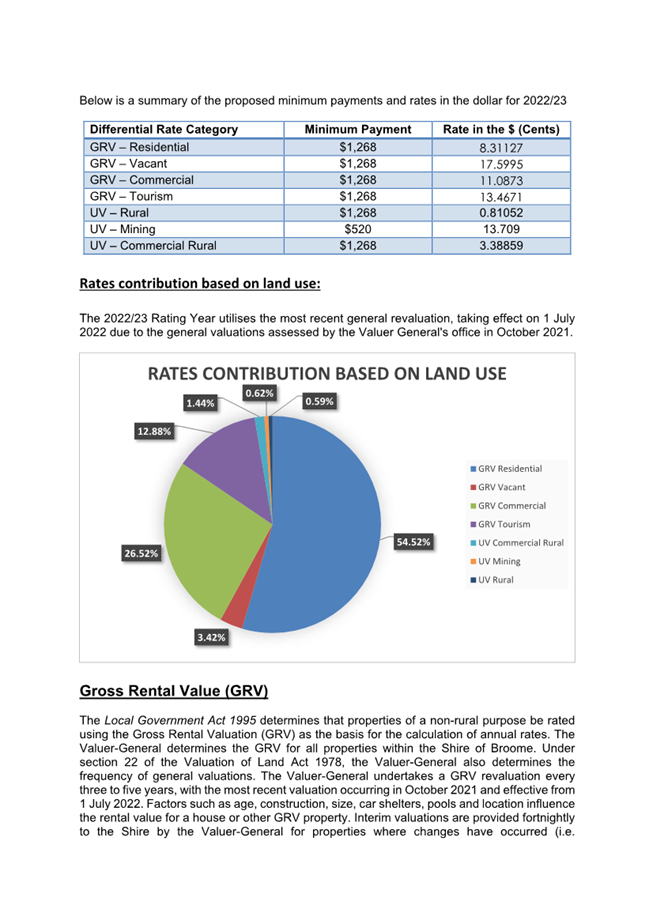

2022/23 Rating Categories and Corresponding Valuation Amounts

Gross Rental Value (GRV)

The Act prescribes that properties with a non-rural purpose be rated using GRV as the basis of calculation of annual rates. The Valuer General’s Office (VGO) determines the GRV for all properties within the Shire. As per section 22 of the Valuation of Land Act 1978, the VGO determines the frequency of general valuations, although historically, a GRV revaluation has occurred every three to five years. The previous valuation was undertaken in October 2018, effective from 1 July 2019.

In October 2021, the VGO commenced reviewing all GRV properties within the Shire, with revised valuations becoming effective from 1 July 2022.

Given the relationship between GRV and rental potential, property owners and the Shire can be exposed to large variations in property values from one valuation cycle to the next. For example, as can be seen in the tables below, there is an average increase of 25.86% in total rateable land value between 2019/20 and 2022-23. It is important for both ratepayers and Council to recognise that changes in land values do not automatically drive changes to overall rates.

The 25.86% average increase in GRV is also not uniform for all properties. As can be observed from the tables below, the average change in GRV of residential properties differed from that of commercial, tourism and vacant properties. Additionally, the average change in GRV also varied from one suburb to another.

In seeking to achieve a balanced budget and a single rate in the dollar for each rating category, the Shire amended its rate in the dollar and reviewed the relative rates burden placed on each category. This provided a fair and equitable methodology in achieving a required general rate increase of 4%.

Change in GRV summarised by rating category

|

Rating Category |

Old GRV |

Proposed GRV |

Change in |

Change in GRV % |

|

GRV $ |

||||

|

GRV – Commercial |

55,332,932 |

59,726,556 |

4,393,624 |

7.94% |

|

GRV – Residential |

119,382,495 |

162,777,808 |

43,740,913 |

36.64% |

|

GRV – Tourism |

19,164,916 |

22,380,599 |

3,215,683 |

16.78% |

|

GRV – Vacant |

3,817,322 |

4,404,188 |

207,666 |

5.44% |

|

Total |

197,697,665 |

249,289,151 |

51,557,886 |

26.08% |

Change in GRV summarised by suburb

|

Rating Category |

Old GRV |

Proposed GRV |

Change in GRV $ |

Change in GRV % |

|

Bilingurr |

19,189,262 |

24,487,849 |

5,298,587 |

27.61% |

|

Broome |

61,332,867 |

75,445,304 |

14,112,437 |

23.01% |

|

Cable Beach |

63,668,944 |

83,337,325 |

19,668,381 |

30.89% |

|

Dampier Peninsula |

384,847 |

384,847 |

0 |

0.00% |

|

Djugun |

39,954,484 |

50,800,585 |

10,846,101 |

27.15% |

|

Eighty Mile Beach |

417,490 |

422,570 |

5,080 |

1.22% |

|

La Grange |

107,900 |

113,520 |

5,620 |

5.21% |

|

Minyirr |

9,565,580 |

10,387,336 |

821,756 |

8.59% |

|

Roebuck |

2,234,463 |

2,817,664 |

583,201 |

26.10% |

|

Waterbank |

841,828 |

1,092,151 |

250,323 |

29.74% |

|

Total |

197,697,665 |

249,289,151 |

51,591,486 |

26.10% |

Pastoral Property Revaluations

2019 revaluations of the UV Commercial Rural rating category the average pastoral property valuation increased by 327%. Following the revaluation, total property valuations in the category increased by $12.66M from $6.65M to $19.3M. This change translated to an increased rates yield of $403K. Council adopted a 5 year concession strategy aimed at reducing the impact on pastoral properties, with an 80% concession applied in year 1, a 60% concession in year two and so on.

Objections were lodged by all pastoral property owners and in late 2021 the Valuer General upheld those objections, consequently reducing the valuations applied to those properties from $19.3M to $10.5M (still significantly higher than the original $6.65M).

Following the revaluation and subsequent reduction in the category, pastoral properties will be required to pay higher rates than in 2019-20, however the impact of this increase will be tempered by the increased “concessional” rates paid in 2020-21 and 2021-22.

Differential Rating Categories

Properties rated based on GRV are categorised as follows:

· GRV Residential: This rating category consists of properties located within the townsite boundaries with predominant residential use. This category is the base rate by which all other GRV rated properties are assessed. The reason is that the different GRV rating categories have a higher demand for Shire resources, and vacant land is encouraged to be developed.

The GRV Residential rating category contains 73% of all properties within the Shire and accounts for 58% of total property value.

· GRV Vacant: This rating category consists of vacant properties located within the townsite boundaries, including land zoned as Tourist, Commercial or Industrial. The object of the rate for this category is designed to encourage landowners to develop vacant land, discourage land banking and reflect the different methods used for the valuation of vacant land compared to the GRV Residential rate category. The reasons behind the increased rate include:

o Desire to increase residential property development to address aspects of the current housing shortage;

o excessive vacant land leaves subdivisions and various parts of the Shire appearing barren and unsightly to the detriment of the aesthetics of the area.

The GRV Vacant rating category contains 5% of all properties within the Shire and accounts for 2% of total property value.

The rate in the dollar for this category is 112% higher than the GRV-Residential base rate.

· GRV Commercial: This rating category consists of properties used for Commercial, Town Centre or Industrial purposes, excluding properties with tourism use. The object of the rate for this category is to raise additional revenue to fund the costs associated with the higher level of service provided to properties in this category. The reason is that the Shire incurs higher costs to service these areas, including car park infrastructure, landscaping, and other amenities. Also, extra charges are associated with economic development activities that have a benefit to these ratepayers.

The GRV Commercial rating category contains 8% of all properties within the Shire and accounts for 21% of total property value.

The rate in the dollar for this category is 33% higher than the GRV–Residential base rate.

· GRV Tourism: This rating category consists of properties with tourism use. The object of the rate for this category is to raise additional revenue to fund the costs associated with the higher reliance on Shire resources and the higher level of service provided to properties in this category. This category is rated higher than the base rate for GRV to fund costs associated with the more significant use of infrastructure and other Council assets and services and contribution towards tourism promotion activities.

The GRV Tourism rating category contains 12% of all properties within the Shire and accounts for 8% of total property value.

The rate in the dollar for this category is 62% higher than the GRV–Residential base rate.

Unimproved Value (UV) Revaluations

Properties that are predominantly used for rural purposes are assigned a UV valuation. The rate in the dollar set for the UV-Rural category forms the basis for calculating all other UV differential rates.

UV properties are updated and re-valued by the VGO on an annual basis, with the most recent valuations taking effect from 1 July 2021. UV-Rural revaluations have yet to be received from the VGO at the date of this report. However, historically, UV properties did not change significantly, and therefore the rateable value of UV properties in 2022/23 is expected to remain the same as 2021/22.

UV-Mining revaluations had not been received as of the date of this report and expected to be available in late May. Council will be consulted should these valuations affect the rate model as presented. Should the adopted differential rates vary from the advertised due to significant changes in valuations, certain disclosures would be made to comply with the requirements of the Local Government (Financial Management) Regulations, Reg 23(b).

· UV Rural: This rating category consists of properties that are exclusively for rural use. This category is the base rate by which all other UV rated properties are assessed. The reason is that the different UV rating categories have a higher demand for Shire resources.

· UV Commercial Rural: This rating category consists of properties with commercial use outside of the townsite and inclusive of:

i. Pearling Leases;

ii. Pastoral leases or Pastoral use;

This category raises revenue to fund the additional costs of servicing these properties. The reason is that the Shire incurs higher costs in infrastructure maintenance due to extra vehicle movements on the Shire’s road network due to the activities associated with these properties.

· UV Mining: This rating category consists of properties used for mining, exploration or prospecting purposes. This category raises additional revenue to fund the other cost impacts to the Shire. This category is rated higher than UV-Commercial to reflect the higher road infrastructure maintenance costs to Council as a result of frequent heavy vehicle use over extensive lengths of Shire roads throughout the year.

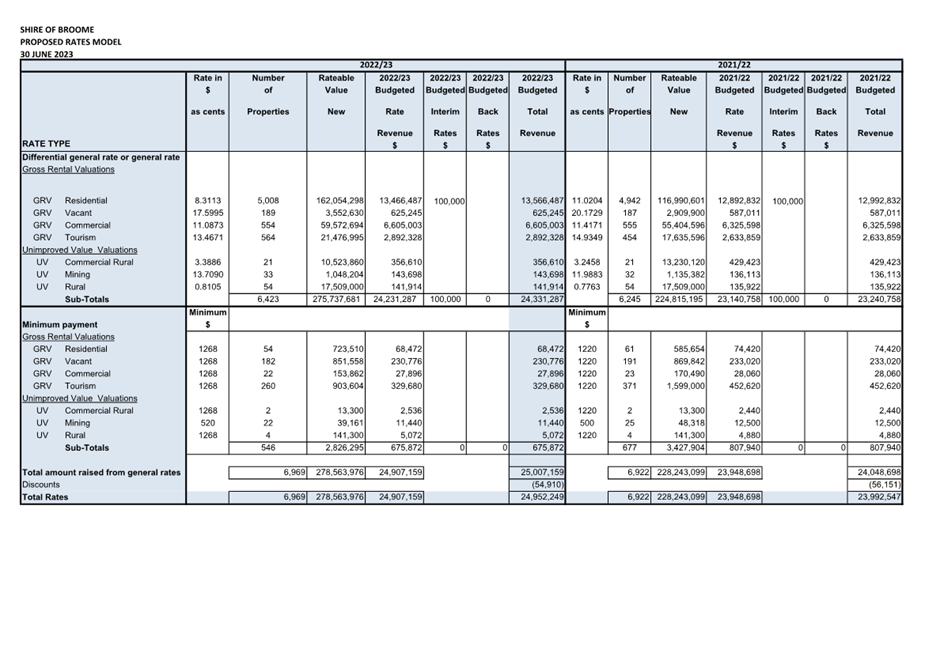

The Proposed Rate in the Dollar

The draft budget documents reflect a 4% general rate rise for all differential rating categories. Rates modelling has been undertaken, and adjustments in the proposed general rates in the dollar and minimum payments have been made with consideration to achieving a minimal rate increase given the current economic climate.

|

Differential Rate Category |

Minimum Payment Proposed |

Rate in the $ (Cents) Proposed |

|

GRV – Residential |

$1,268 |

8.3113 |

|

GRV – Vacant |

$1,268 |

17.5995 |

|

GRV – Commercial/Industrial |

$1,268 |

11.0873 |

|

GRV – Tourism |

$1,268 |

13.4671 |

|

UV – Rural |

$1,268 |

0.8105 |

|

UV – Mining |

$520 |

13.7090 |

|

UV – Commercial Rural |

$1,268 |

3.3886 |

The proposed rate in the dollar for each rating category is summarised in the table above and reflects a general 4% change from the preceding year.

Proposed Minimum Payments

As part of the annual budget process, the Council must determine the minimum payment for differential rating categories in the 2022/23 financial year.

The setting of minimum rates within rating categories recognises that every property receives some minimum level of benefit from the Shire’s works and services, which is shared by all properties regardless of size, value, and use. A proposed minimum rate of $1,268 has been applied to all rating categories except for the UV-Mining category, set at $520. This represents an increase of $48 and $20 respectively which has been applied in recognition of minimum rates having no increase for several years.

UV of the 57 mining tenements ranges from $200 to $453,000 with an average UV of $19,936.32. The minimum rate for the UV-Mining category is set at a lower level than the other rating categories to ensure that the rate burden is distributed equitably between all other property owners paying the minimum amount. A lower minimum payment will also ensure that less than 50% of the properties in this category are on the minimum rate and comply with section 6.35 of the Act.

Rates from Proposed Differential Rates and Minimum Payments Making up the 2022/23 Budget Deficiency

Applying the rate in the dollar to the rateable value of the various properties within each rating category, plus a conservative estimate of interim rates of $100,000, results in an estimated total rate of $24.95M, which is 100% of the $24.95M budget deficiency. This percentage satisfies the requirements of section 6.34 of the Act.

Detailed calculations illustrating the resulting rates for all differential rating categories and associated minimum payments are summarised in Attachment 3 of this report.

The proposed objects and reasons for Differential Rating for 2022/23 are found in Attachment 2.

From a statutory perspective, it is important to note that section 6.35 of the Act requires a local government to ensure that the general rate is imposed on not less than 50% of the number of separately rated properties, or 50% of the number of properties in a differential general rate category. This requirement has been achieved in all categories.

In line with previous years, Ministerial approval must be sought under section 6.33 of the Act for the proposed UV Mining and UV Commercial differential general rates as these are more than twice the lowest UV general rate.

It is acknowledged that the UV Mining revaluations will require analysis upon receipt. However, it is intended to ensure a comparable rate yield from each UV category, thus not impacting the proposed total revenue.

Council will need to consider these valuations before formally adopting differential rates and adjust the UV rates accordingly. To progress the timely adoption of the budget, it is proposed to seek public comments on the proposed UV differential rates indicating a general 4% rate increase subject to review upon receipt of UV Mining valuations.

The Required Public Notice of Certain Rates

Section 6.36 of the Act requires Council to give local public notice of its intention to impose general differential rates or a minimum payment applying to a differential rate category. This allows the ratepayers to see how properties are rated across the district.

As per section 1.7 and 6.36 of the Act, the local public notice of differential rates must:

· be published at least once in a newspaper circulating generally in the district;

· be displayed on a notice board at the local government’s offices;

· be displayed on a notice board at each local government library;

· contain details of each rate or minimum payment the Council proposes to impose;

· advise where a document can be inspected that provides the objects of and reasons for each proposed rate and minimum payment;

· contain an invitation for electors or ratepayers to lodge submissions on any of the proposals within 21 days from the date of the notice (i.e. the 21-day submission period excludes the first day of publishing); and

· be published within two months before 1 July 2022 (i.e. not earlier than 1 May).

Council must then consider any submissions received before seeking the Minister’s approval (should this be required) before formally adopting the differential rates and minimum payments as part of the annual budget process.

CONSULTATION

Department of Local Government, Sport and Cultural Industries

Moore Australia

STATUTORY ENVIRONMENT

Local Government Act 1995

1.7 Local public notice

(1) Where under this Act local public notice of a matter is required to be given, a notice of the matter is to be —

(a) published in a newspaper circulating generally throughout the district; and

(b) exhibited to the public on a notice board at the local government’s offices; and

(c) exhibited to the public on a notice board at every local government library in the district.

(2) Unless expressly stated otherwise it is sufficient if the notice is —

(a) published under subsection (1)(a) on at least one occasion; and

(b) exhibited under subsection (1)(b) and (c) for a reasonable time, being not less than —

(i) the time prescribed for this paragraph; or

(ii) if no time is prescribed, 7 days.

6.28 Basis of Rates

1). The Minister is to -

(a) determine the method of valuation of land to be used by a local government as the basis for a rate; and

(b) publish a notice of the determination in the government gazette.

2). In determining the method of valuation of land to be used by a local government the Minister is to have regard to the general principle that the basis for a rate on any land is to be –

(a) where the land is used predominantly for rural purposes, the unimproved value of the land, and

(b) where the land is used predominantly for non-rural purposes, the gross rental value of the land.

6.32 Rates and service charges

(1) When adopting the annual budget, a local government —

(a) to make up the budget deficiency, is to impose* a general rate on rateable land within its district, which rate may be imposed either —

(i) uniformly; or

(ii) differentially; and

(b) may impose* on rateable land within its district —

(i) a specified area rate; or

(ii) a minimum payment; and

(c) may impose* a service charge on land within its district.

* Absolute majority required.

(2) Where a local government resolves to impose a rate it is required to —

(a) set a rate which is expressed as a rate in the dollar of the gross rental value of rateable land within its district to be rated on gross rental value; and

(b) set a rate which is expressed as a rate in the dollar of the unimproved value of rateable land within its district to be rated on unimproved value.

6.33 Differential general rates

(1) A local government may impose differential general rates according to any or a combination, of the following characteristics -

(a) the purpose for which the land is zoned under a local planning scheme in force under the Planning and Development Act 2005;

(b) the predominant purpose for which the land is held or used as determined by the local government;

(c) whether or not the land is vacant land; or

(d) any other characteristic or combination of characteristics prescribed.

6.34 Limit on revenue or income from general rates

Unless the Minister otherwise approves, the amount shown in the annual budget as being the amount it is estimated will be yielded by the general rate is not to —

(a) be more than 110% of the amount of the budget deficiency; or

(b) be less than 90% of the amount of the budget deficiency.

6.35. Minimum payment

(1) Subject to this section, a local government may impose on any rateable land in its district a minimum payment which is greater than the general rate which would otherwise be payable on that land.

(2) A minimum payment is to be a general minimum but, subject to subsection (3), a lesser minimum may be imposed in respect of any portion of the district.

(3) In applying subsection (2) the local government is to ensure the general minimum is imposed on not less than —

(a) 50% of the total number of separately rated properties in the district; or

(b) 50% of the number of properties in each category referred to in subsection (6),

on which a minimum payment is imposed.

(4) A minimum payment is not to be imposed on more than the prescribed percentage of —

(a) the number of separately rated properties in the district; or

(b) the number of properties in each category referred to in subsection (6),

unless the general minimum does not exceed the prescribed amount.

(5) If a local government imposes a differential general rate on any land on the basis that the land is vacant land it may, with the approval of the Minister, impose a minimum payment in a manner that does not comply with subsections (2), (3) and (4) for that land.

(6) For the purposes of this section a minimum payment is to be applied separately, in accordance with the principles set forth in subsections (2), (3) and (4) in respect of each of the following categories —

(a) to land rated on gross rental value; and

(b) to land rated on unimproved value; and

(c) to each differential rating category where a differential general rate is imposed.

[Section 6.35 amended by No. 49 of 2004 s. 61.]

6.36 Local government to give notice of certain rates

(1) Before imposing any differential general rates or a minimum payment applying to a differential rate category under section 6.35(6)(c) a local government is to give local public notice of its intention to do so.

(2) A local government is required to ensure that a notice referred to in subsection (1) is published in sufficient time to allow compliance with the requirements specified in this section and section 6.2(1).

(3) A notice referred to in subsection (1) —

(a) may be published within the period of 2 months preceding the commencement of the financial year to which the proposed rates are to apply on the basis of the local government’s estimate of the budget deficiency; and

(b) is to contain —

(i) details of each rate or minimum payment the local government intends to impose; and

(ii) an invitation for submissions to be made by an elector or a ratepayer in respect of the proposed rate or minimum payment and any related matters within 21 days (or such longer period as is specified in the notice) of the notice; and

(iii) any further information in relation to the matters specified in subparagraphs (i) and (ii) which may be prescribed; and

(c) is to advise electors and ratepayers of the time and place where a document describing the objects of, and reasons for, each proposed rate and minimum payment may be inspected.

(4) The local government is required to consider any submissions received before imposing the proposed rate or minimum payment with or without modification.

(5) Where a local government —

(a) in an emergency, proposes to impose a supplementary general rate or specified area rate under section 6.32(3)(a); or

(b) proposes to modify the proposed rates or minimum payments after considering any submissions under subsection (4),

it is not required to give local public notice of that proposed supplementary general rate, specified area rate, modified rate or minimum payment.

6.47 Concessions

Subject to the Rates and Charges (Rebates and Deferments) Act 1992, a local government may at the time of imposing a rate or service charge or at a later date resolve to waive* a rate or service charge or resolve to grant other concessions in relation to a rate or service charge.

* Absolute majority required

POLICY IMPLICATIONS

Rating Policy

Tourism Administration Policy

FINANCIAL IMPLICATIONS

The proposed differential rates and minimum payments for the 2022/23 financial year will raise estimated rates revenue of $24.95M. A detailed rates model is in Attachment 3.

RISK

Decisions on this matter impact the rates levied on the ratepayers of the district.

There is a possible moderate risk of non-compliance with the Act, potential moderate level public embarrassment and almost certain significant financial implications to Council. It is advised that the Council support the recommendations of this report to mitigate these risks.

STRATEGIC IMPLICATIONS

People – We will continue to enjoy Broome-time, our special way of life. It’s laid-back but bursting with energy, inclusive, safe and healthy, for everyone:

Affordable services and initiatives to satisfy community need

Place – We will grow and develop responsibly, caring for our natural, cultural and built heritage, for everyone:

Core asset management to optimise the Shire’s infrastructure whilst minimising life cycle costs.

Prosperity – Together, we will build a strong, diversified and growing economy with work opportunities for everyone:

Affordable and equitable services and infrastructure

Affordable land for residential, industrial, commercial and community use

Performance - We will deliver excellent governance, service and value, for everyone.:

Sustainable and integrated strategic and operational plans

Responsible resource allocation

VOTING REQUIREMENTS

|

(Report Recommendation) Minute No. C/0522/026 Moved: Cr N Wevers Seconded: Cr P Taylor That Council: 1. Publishes a local public notice proposing the 2022/23 differential general rates and minimum payments set out in the table below and invites electors or ratepayers to lodge submissions about this proposal within 21 days from the date of notice:

2. Adopts the Objects and Reasons presented in Attachment 2 for each of the proposed differential general rates and minimum payments in point 1 above; and 3. Following the close of the public submission period, requests the Chief Executive Officer to report back to Council, presenting any submissions for formal consideration before seeking Minister’s Approval under section 6.33(3) of the Local Government Act 1995 to impose differential rates which are more than twice the lowest differential rate. |

|

Attachment 1 - 2022-23 Advert - Intention to Impose Differential Rates |

|

|

Attachment 2 - 2022-23 Objects and Reasons |

|

|

Attachment 3 - 2022-23 Rates Model for Budget Adoption |

There are no reports in this section.

Nil

There being no further business the Chairperson declared the meeting closed at 5:27pm.