MINUTES

OF THE

Audit and Risk Committee Meeting

10 December 2024

|

These minutes were confirmed at a meeting held and signed below by the Presiding Person, at the meeting these minutes were confirmed.

|

MINUTES

OF THE

Audit and Risk Committee Meeting

10 December 2024

|

These minutes were confirmed at a meeting held and signed below by the Presiding Person, at the meeting these minutes were confirmed.

|

Minutes – Audit and Risk Committee Meeting 10 December 2024 Page 1 of 4

SHIRE OF BROOME

Audit and Risk Committee Meeting

Tuesday 10 December 2024

INDEX – Minutes

3. Declarations Of Financial Interest / Impartiality

5.1 Regulation 17 Internal Audit Review

5.2 ANNUAL FINANCIAL REPORT AND AUDIT REPORT 2023/24

6. Matters Behind Closed Doors

MINUTES OF THE Audit and Risk Committee Meeting OF THE SHIRE OF BROOME,

HELD IN THE Council Chambers, Corner Weld and Haas Streets, Broome, ON Tuesday 10 December 2024, COMMENCING AT 09.00AM.

The Chair welcomed Councillors and officers and declared the meeting open at 9:04am.

|

ATTENDANCE |

|

|

|

|

|

|

|

Members: |

Cr D Male |

Chair, Deputy Shire President |

|

|

C Mitchell |

Shire President |

|

|

Cr M Virgo |

|

|

|

|

|

|

Observers: |

Cr S Cooper |

|

|

|

Cr E Smith |

|

|

|

||

|

Apologies: |

Nil. |

|

|

|

||

|

Leave of Absence: |

Nil. |

|

|

|

||

|

Officers: |

Mr S Mastrolembo |

Chief Executive Officer |

|

|

Mr J Hall |

Director Infrastructure |

|

|

Ms R Doyle |

Manager Governance, Strategy and Risk |

|

|

Ms E French |

Manager Financial Services |

|

|

Ms E Kerr |

Creditors Officer |

|

Committee Member |

Item No |

Item |

Nature of Interest |

|

Nil. |

|||

|

Committee Resolution: Minute No. AR/1224/001 Moved: Cr D Male Seconded: Shire President C Mitchell That the Minutes of the Audit and Risk Committee held on 29 October 2024, as published and circulated, be confirmed as a true and accurate record of that meeting. |

|

LOCATION/ADDRESS: |

Nil |

|

APPLICANT: |

Nil |

|

FILE: |

COA01 |

|

AUTHOR: |

Manager Governance, Strategy And Risk |

|

CONTRIBUTOR/S: |

Nil |

|

RESPONSIBLE OFFICER: |

Director Corporate Services |

|

DISCLOSURE OF INTEREST: |

Nil |

|

SUMMARY: Regulation 17 of the Local Government (Audit) Regulations requires the Chief Executive Officer (CEO) to review the appropriateness and effectiveness of a local government’s systems and procedures in relation to risk management, internal control and legislative compliance. The Shire of Broome (Shire) engaged Paxon Group (Paxon) to undertake this review on behalf of the CEO. This report presents the findings of that review to the Audit and Risk Committee and subsequently to Council. |

Previous Considerations

ARC 14 May 2019 Item 5.1 Audit Regulation 17 Risk Biannual Progress

Report

OMC 30 May 2019 Item 10.3 Minutes Of The Audit And Risk Committee

Meeting Held 14 May 2019

ARC 13 December 2021 Item 5.1 Audit Regulation 17 – CEO Review of Certain

Systems and Procedures

OMC 16 December 2021 Item 13.1.1 Audit Regulation 17 - CEO Review Of Certain

Systems And Procedures

Regulation 17 of the Local Government (Audit) Regulations 1996 was introduced in early 2013. In June 2018, amendments to Regulation 17 changed the frequency of reviews from once every two financial years to at least once every three financial years. Both subsequent reviews were undertaken internally, with officers utilising tools such as the Department of Local Government’s Operational Guidelines to assess internal controls and legislative compliance.

In line with Regulation 17 requirements, the Shire’s last review was undertaken internally and was presented to the Audit and Risk Committee on 13 December 2021 and then subsequently endorsed by Council.

The risk management functions of the local government should manage the creation and protection of value within the Shire of Broome (Shire). Effective risk management improves performance, encourages innovation and supports the achievement of objectives.

Internal controls are the systematic measures (such as reviews, checks and balances, methods and procedures) instituted by an organisation to; conduct its business in an orderly and efficient manner, safeguard its assets and resources, deter and detect errors, fraud and theft, ensure accuracy and completeness of its accounting data, produce reliable and timely financial and management information, and ensure adherence to its policies and plans. Internal controls are a key component of a sound governance framework, which uses instruments such as policies, delegations, authorisations, audit practices, information systems and security, management and operation techniques and human resource practice to create a network of control mitigation to maintain appropriate levels of risk.

Legislative compliance involves monitoring compliance with legislation and regulations, reviewing the annual Compliance Annual Return, staying informed about how management is monitoring the effectiveness of its compliance, reviewing procedures that handle complaints, monitoring the local government’s compliance framework, obtaining assurances against adverse trends, reviewing statutory and financial returns and other evaluating, monitoring and problem solving against significant compliance issues.

The review may relate to any or all the matters in the regulation however, each of those matters is subject to review no less than once every three financial years. In accordance with Regulation 16(c) of the Local Government (Audit) Regulations 1996, the Audit Committee is required to review a report prepared by the CEO, and subsequently report to the Council the results of the Committee’s review.

COMMENT

The Shire engaged the external auditor, Paxon, on 12 September 2024 to conduct the Shire of Broome Regulation 17 Internal Audit Review. The review was conducted remotely via email, shared electronic folders and telephone correspondence during the period between 25 September 2024 and 25 November 2024. The findings and outcomes of the review are detailed in the attached report (Attachment 1).

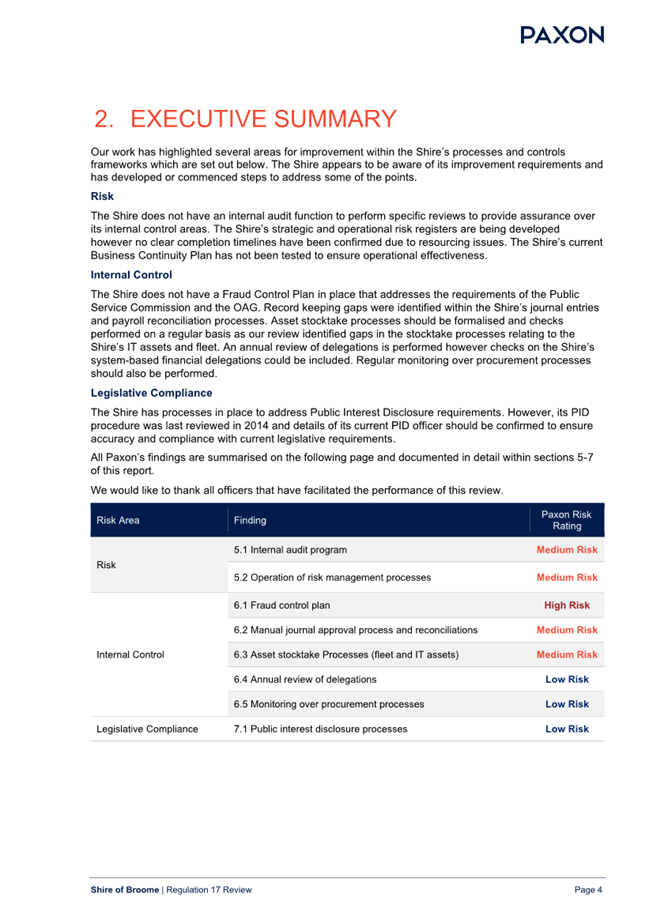

As per the Executive Summary of findings (section 2 of Attachment 1), Paxon found that, subject to eight recommendations, “The Shire appears to be aware of its improvement requirements and has developed or commenced steps to address some of the points”.

The table and breakdown below summarise the eight findings, with the review providing further detail and recommendations for each. As highlighted in the review, the findings are presented on an exception basis, reflecting identified issues while excluding areas tested where policies, procedures, and processes were found to be appropriate and in line with best practices. It is important to note that due to inherent limitations, the review was not designed to identify all weaknesses and does not assess the internal control structure in its entirety.

|

Risk Area |

Finding |

Paxon Risk Rating |

|

Risk |

5.1 Internal audit program |

Medium Risk |

|

5.2 Operation of risk management processes |

Medium Risk |

|

|

Internal Control |

6.1 Fraud control plan |

High Risk |

|

6.2 Manual journal approval process and reconciliations |

Medium Risk |

|

|

6.3 Asset stocktake Processes (fleet and IT assets) |

Medium Risk |

|

|

6.4 Annual review of delegations |

Low Risk |

|

|

6.5 Monitoring over procurement processes |

Low Risk |

|

|

Legislative Compliance |

7.1 Public interest disclosure processes |

Low Risk |

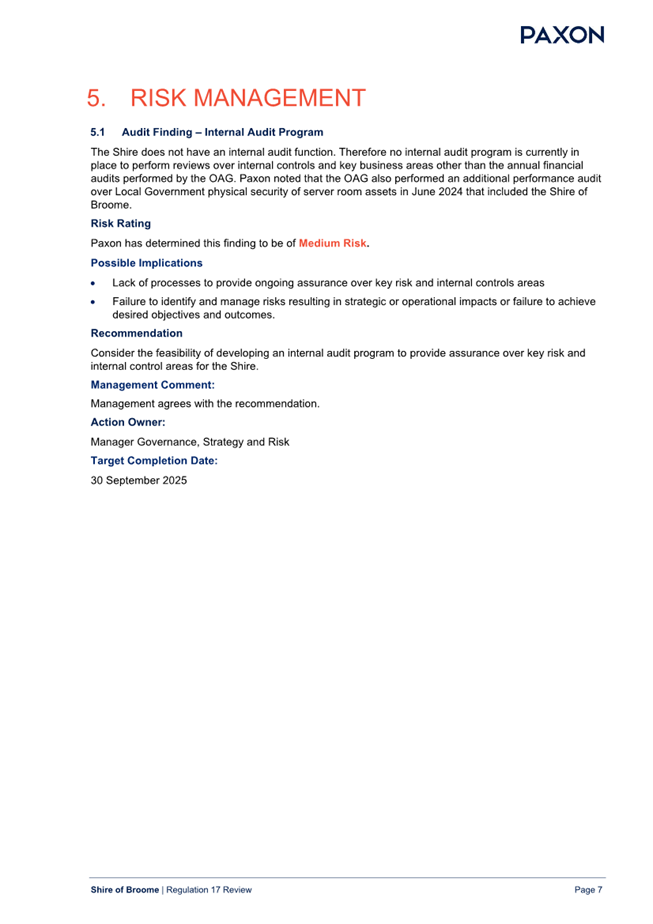

Audit Finding – Internal Audit Program

Finding Rating: Medium

During the audit, it was noted that the Shire of Broome does not have an internal audit function in place. As a result, there is currently no internal audit program to review internal controls and key business areas, aside from the annual financial audits conducted by the Office of the Auditor General (OAG). Additionally, it was highlighted that in June 2024, the OAG conducted a performance audit focused on local government physical security of server room assets, which included the Shire of Broome.

Management Comment:

Management acknowledges the finding and has agreed to establish an internal audit program to provide assurance over key risk and internal control areas for the Shire with completion by 30 September 2025.

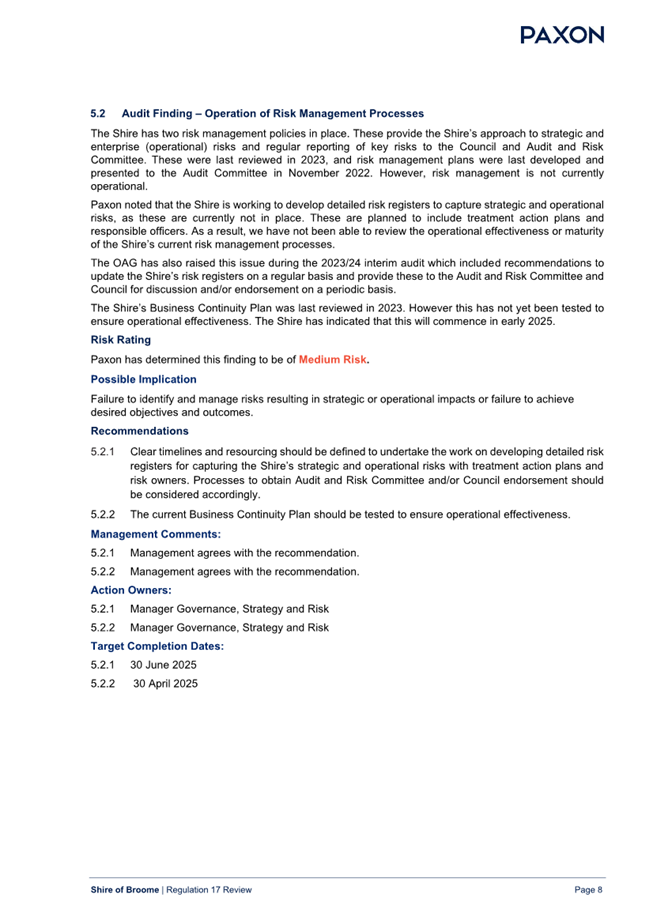

Audit Finding – Operation of Risk Management Processes

Finding Rating: Medium

The Shire has two risk management policies in place, addressing strategic and operational risks, with regular reporting to the Council and Audit and Risk Committee. These policies were last reviewed in 2023, and risk management plans were presented to the Audit and Risk Committee in November 2022. However, risk management is not yet fully operational, as the Shire is in the process of developing risk registers for both strategic and operational risks. These registers will include treatment action plans and responsible officers.

The Office of the Auditor General (OAG) identified this gap during the 2023 - 2024 interim audit, recommending that the Shire regularly update its risk registers and present them to the Audit and Risk Committee and Council for review.

The Shire’s Business Continuity Plan, last reviewed in 2023, has yet to be tested for effectiveness, but the Shire plans to begin testing in early 2025.

Management Comment:

The Shire is advised to establish clear timelines and allocate resources for developing detailed risk registers to capture both strategic and operational risks, including treatment action plans and risk owners. The processes for obtaining endorsement from the Audit and Risk Committee and/or Council should also be considered. Additionally, the current Business Continuity Plan is currently in planning and will be procured for in December 2024 with expected completion by 30 April 2025.

Audit Finding – Fraud Control Plan

Finding Rating: High

The Shire has a Code of Conduct for employees and Governance Framework in place which describe some requirements and processes related to misconduct, conflict of interests and fraud. The Shire does not currently have a Fraud Control Plan or related documents in place, The Public Sector Management Act requires a formal integrity framework to be in place. The Shire is in the process of developing the following documents however no clear timelines for completion have been identified:

• Integrity Framework

• Fraud and Corruption Policy

• Fraud and Corruption Control Plan

Management Comment:

Management agrees with this recommendation. The policy will be developed by the Manager of Governance, Strategy and Risk, and the Manager of Information Services, with a target completion date of 30 March 2025.

Audit Finding – Manual Journal Approval Process and Reconciliations

Finding Rating: Medium

The recommendation is to implement clear record-keeping requirements for manual journals and reconciliations, including capturing essential details such as the names of officers performing checks, their approvers, and the dates these tasks are completed.

Management Comment:

Management agrees with this observation and will review current processes to ensure proper approvals are consistently documented. The action has a target completion date of 31 January 2025.

Audit Finding – Asset Stocktake Processes (Fleet and IT Assets)

Paxon identified that the Shire lacks formal procedures for conducting stocktakes of assets, and there are gaps in the processes for It Assets and Fleet Management. Specifically, no evidence was provided that a formal stocktake of IT devices was performed, and it was unclear whether asset records were consistently updated. For the fleet, the last stocktake occurred in July 2023, but no verification evidence was recorded for the fleet items in the most recent listing.

Finding Rating: Medium

Management Comment:

Management acknowledges the need for formal stocktake procedures and plans to implement a policy that will define the requirements, frequency, and approval processes to ensure consistency and accountability. While staff vacancies and turnover in IT and the depot have impacted stocktake consistency, the Shire will reinforce organisational expectations to ensure regular and well-documented stocktakes in the future. The expected completion date of this policy is targeted for 30 June 2025.

Audit finding – Annual Review of Delegations

Finding Rating: Low

The Shire conducts annual reviews of its delegations as required by the Local Government Act 1995 (s5.46), with the latest review of its delegated authority register completed in May 2024.

Paxon conducted a high-level review of the Shire’s financial delegations, comparing them to the delegated authority register and performing sample testing to ensure alignment. No significant issues were identified. However, an opportunity for improvement was noted, suggesting that the Shire include a review of financial delegations within its system, such as purchase order and invoice approval delegations, during its annual review to ensure alignment with the delegated authority register.

Management Comment:

Management plans to consider the alignment the review of the Delegation Authority Register with the periodic review of the Expenditure Authorisation Policy to ensure consistent and efficient governance of financial delegations. This process will also involve reviewing the related system setup to identify and address any discrepancies or inefficiencies, with a target completion date of 30 June 2025.

Audit Finding – Monitoring Over Procurement Processes

Finding Rating: Low

The Shire has well-established procurement processes, including checklists, templates, and training for procurement officers, as well as support for business areas to ensure necessary documents and approvals are in place before finalising procurements. However, the Shire does not conduct periodic monitoring to ensure compliance with procurement requirements or to assess the effectiveness of its processes, such as identifying issues like split purchase orders or potential contravention of procurement principles.

The recommendation is for the Shire of Broome to implement periodic monitoring of procurement processes and ensure that supporting documentation is retained to verify the completion of such monitoring. Management acknowledges this finding and agrees with the need for periodic monitoring to reduce the risk of non-compliance, such as split purchase orders with a target completion date of 30 April 2025.

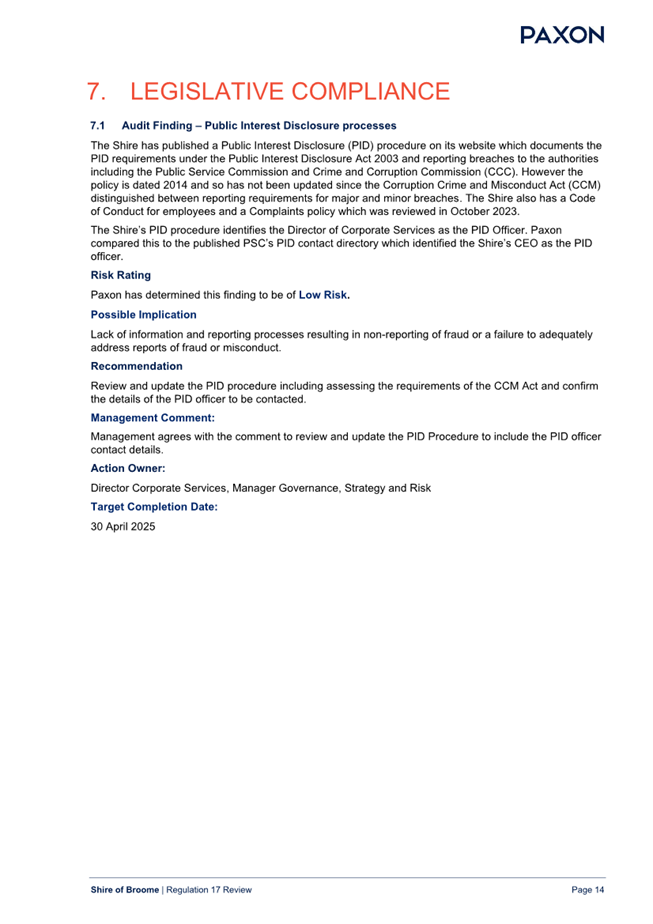

Audit Finding – Public Interest Disclosure Processes

Finding Rating: Low

Paxon identified gaps in information and reporting processes, leading to potential non-reporting of fraud or inadequate responses to fraud or misconduct reports.

Management Comment:

Management agrees with the comment to review and update the PID Procedure to include the PID officer contact details and has set a target completion date of 30 April 2025.

Overall, the review undertaken by Paxon concludes that the Shire has appropriate and effective systems and procedures in place to manage and mitigate risk; but identifies the areas for further improvement.

An update on the findings will be presented to the Audit and Risk Committee on a quarterly basis, starting in the first quarter of 2025.

CONSULTATION

Paxon Group for the purpose of undertaking the Regulation 17 Audit process.

STATUTORY ENVIRONMENT

Local Government (Audit) Regulations 1996

17. CEO to review certain systems and procedures

(1) The CEO is to review the appropriateness and effectiveness of a local government’s systems and procedure in relation to-

(a) Risk management; and

(b) Internal control; and

(c) Legislative compliance.

(2) The review may relate to any or all of the matters referred to in subregulation (1)(a), (b) and (c), but each of those matters is to be the subject of a review not less than once in every 3 financial years.

(3) The CEO is to report to the audit committee the results of that review.

POLICY IMPLICATIONS

Shire of Broome Code of Conduct for Council Members, Committee Members and Candidates.

Shire of Broome Council Policy Risk Management.

FINANCIAL IMPLICATIONS

The cost of conducting the Regulation 17 Audit was included in the 2023 / 2024 Budget.

RISK

There is reputational risk from non-compliance with the legislative requirement to complete an audit regulation 17 review triennially. The external Regulation 17 Audit being conducted mitigates this risk.

STRATEGIC ASPIRATIONS

Performance - We will deliver excellent governance, service & value for everyone.

Outcome 11 - Effective leadership, advocacy and governance

Objective 11.2 Deliver best practice governance and risk management.

VOTING REQUIREMENTS

|

(Report Recommendation) Minute No. AR/1224/002 Moved: Cr M Virgo Seconded: Shire President C Mitchell That the Audit and Risk Committee recommends that Council: 1. Accept the findings of the Chief Executive Officer’s review of the Shire of Broome’s systems and procedures concerning risk management, internal control, and legislative compliance in Attachment 1. 2. Requests the Chief Executive Officer provide quarterly progress reports to the Audit and Risk Committee on the implementation of the improvement recommendations identified in the review in Attachment 1 until all issues have been resolved. |

|

Regulation 17 Report - Shire of Broome |

Minutes – Audit and Risk Committee Meeting 10 December 2024 Page 1 of 4

|

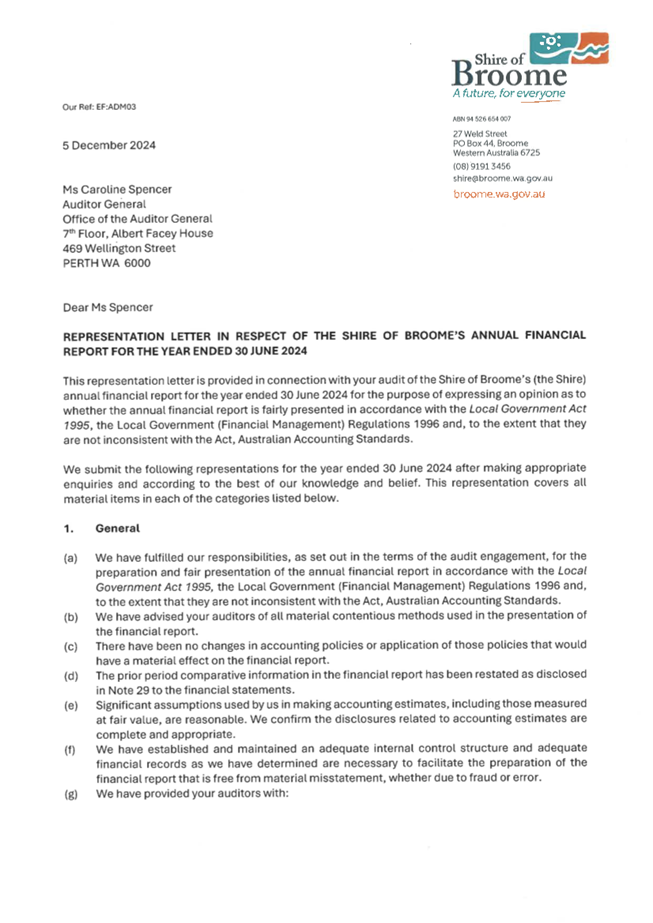

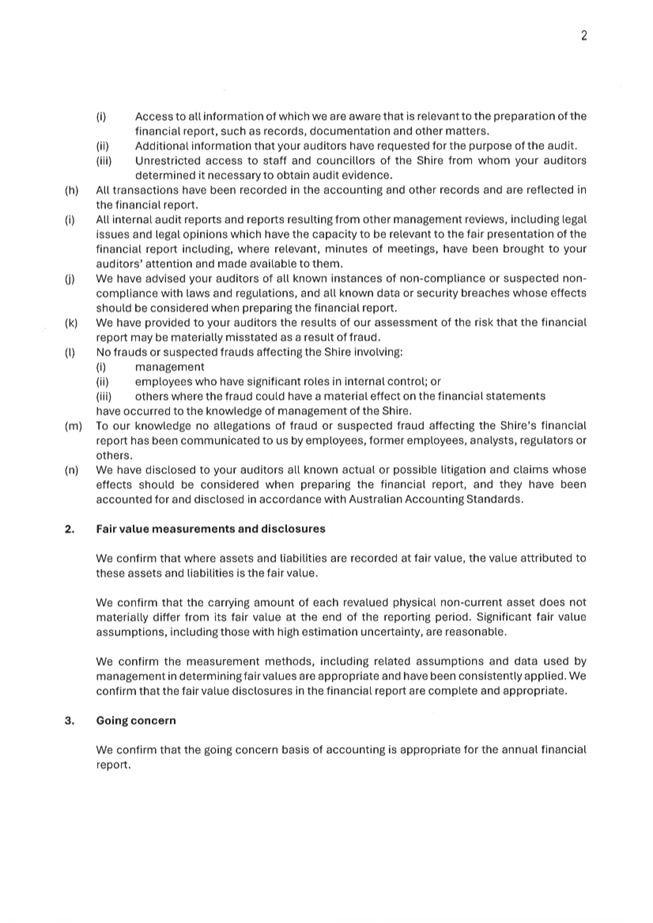

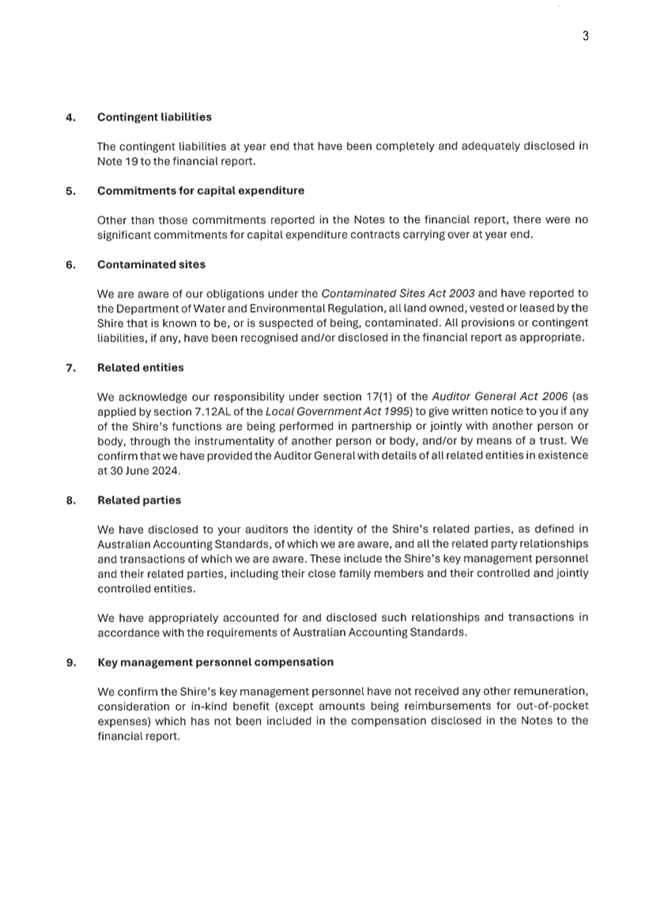

SUMMARY: The Audit and Risk Committee is requested to review and recommend to Council the adoption of the 2024 Annual Financial Report, Audit Management Letter and applicable budget amendments. |

In accordance with section 7.9 of the Local Government Act 1995 (the Act), an auditor is required to examine the accounts and annual financial report of a local government. Upon completion of the audit, the auditor must prepare a report and submit it by 31 December following the end of the financial year to:

(a) The Mayor or President,

(b) The Chief Executive Officer (CEO), and

(c) The Minister.

Under Regulation 10(4) of the Local Government (Audit) Regulations 1996, the auditor may also prepare a Management Letter, which provides additional commentary on the audit process, internal control issues, or any other matters deemed relevant. While generally not material in relation to the overall audit of the financial report, are nonetheless considered relevant to the day-to-day operations of the Shire. This Management Letter accompanies the auditor’s report and is similarly forwarded to the individuals specified under section 7.9 of the Act.

The Office of the Auditor General (OAG), with RSM Australia as its contracted auditor for the second consecutive year, conducted the Shire's 2023/24 financial year audit. An Audit Entrance Meeting which outlined the audit process and timeline was held on 22 April 2024, attended by the Audit and Risk Committee, CEO, Shire Executive and officers.

The final audit occurred between 14 October 2024 and 1 November 2024, with follow-up discussions continuing into early December.

The Final Audit Exit Meeting was held on 27 November 2024, attended by the Audit and Risk Committee, CEO, Executive and Shire officers. This satisfies the requirement of section 7.12A(2) of the Act requiring a local government to meet with its auditor at least once every year. During the meeting, the auditors presented an overview of the audit, including:

1. Areas of focus

2. Prior year restatements

3. Management letter points

On 9 December 2024, the OAG issued the signed audit report, including their Opinion and Management Letter, which are attached to this report.

The Audit and Risk Committee (ARC), under its terms of reference, is required to:

1. Review the auditor’s reports after considering a report from the CEO on the matters raised.

2. Assess whether any matters raised require action by the local government.

3. Ensure appropriate responses and remedial actions are implemented.

In the instance that the auditor raises findings considered significant in the audit report, the ARC must consider a report prepared by the CEO addressing those significant findings, and state what action the local government has taken or intends to take with respect to each of those findings. As per section 7.12A(4) of the Act:

- within three months of receiving the auditor’s report it must be provided to the Minister, and

- a copy of the report published on the local government’s official website within 14 days after a local government gives a report to the Minister.

This agenda item ensures compliance with the legislative requirements of the Local Government Act 1995, the Local Government (Audit) Regulations 1996, and the Local Government (Financial Management) Regulations 1996, while facilitating the necessary review and recommendation process for the adoption of the Annual Financial Report.

COMMENT

The 2024 financial statements were submitted to the OAG on 20 September 2024. The statutory requirement is to submit by 30 September 2024.

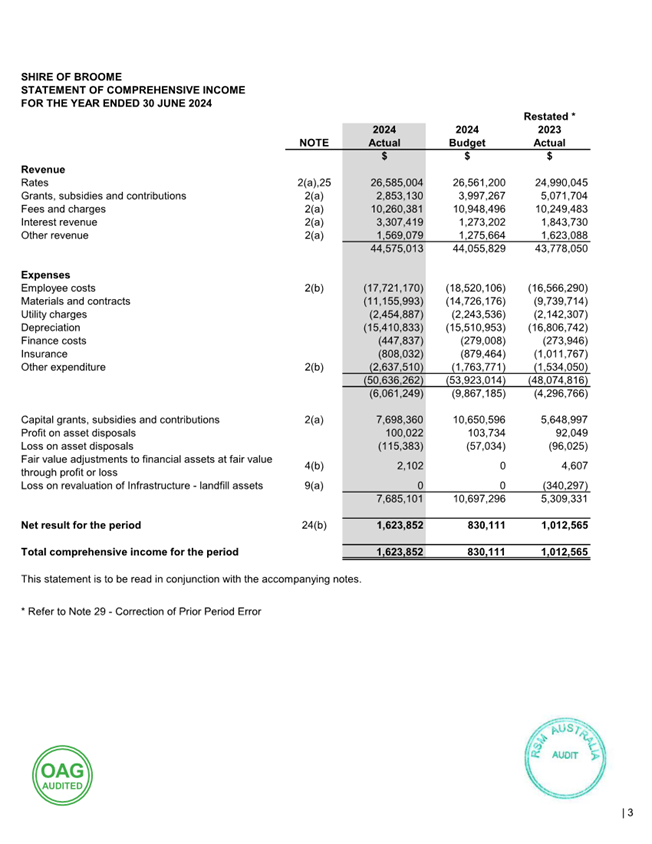

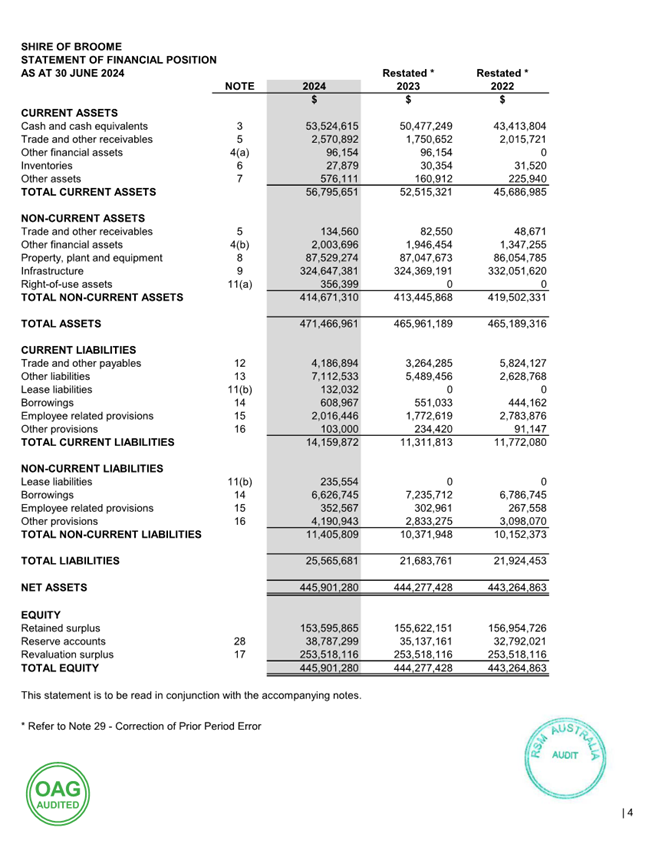

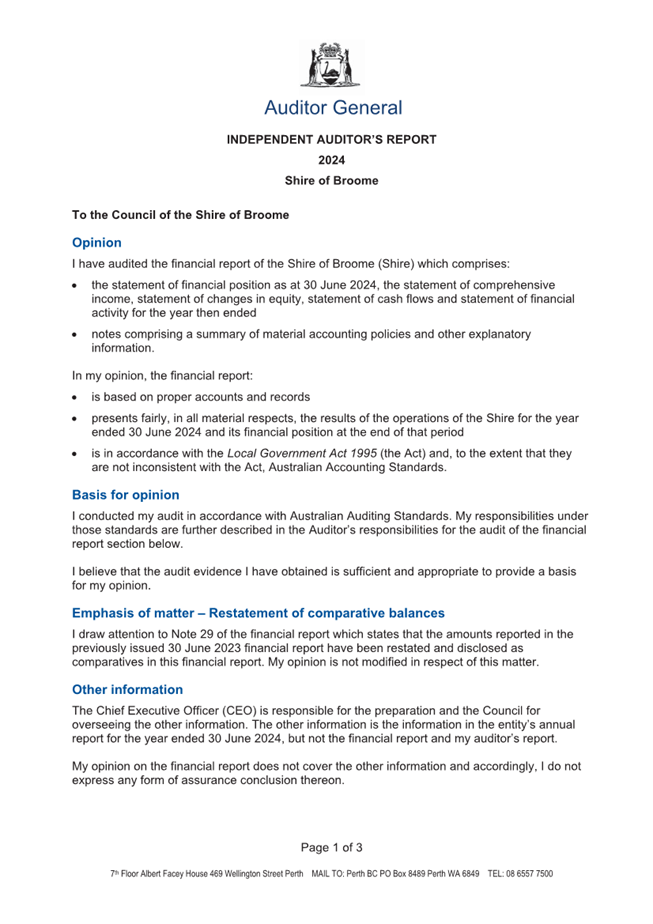

The Shire of Broome has received a clear (unmodified) audit opinion from the OAG, with an emphasis of matter highlighted.

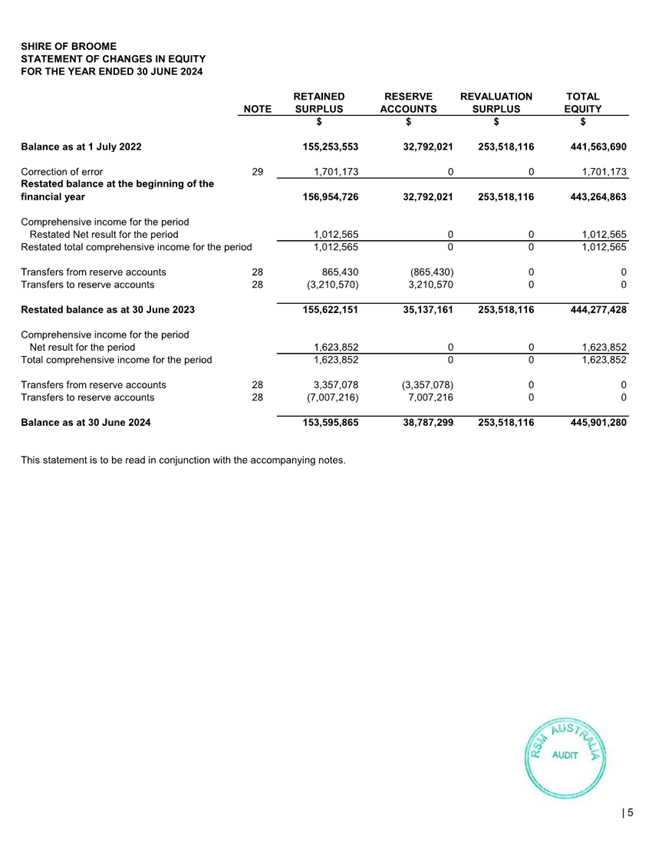

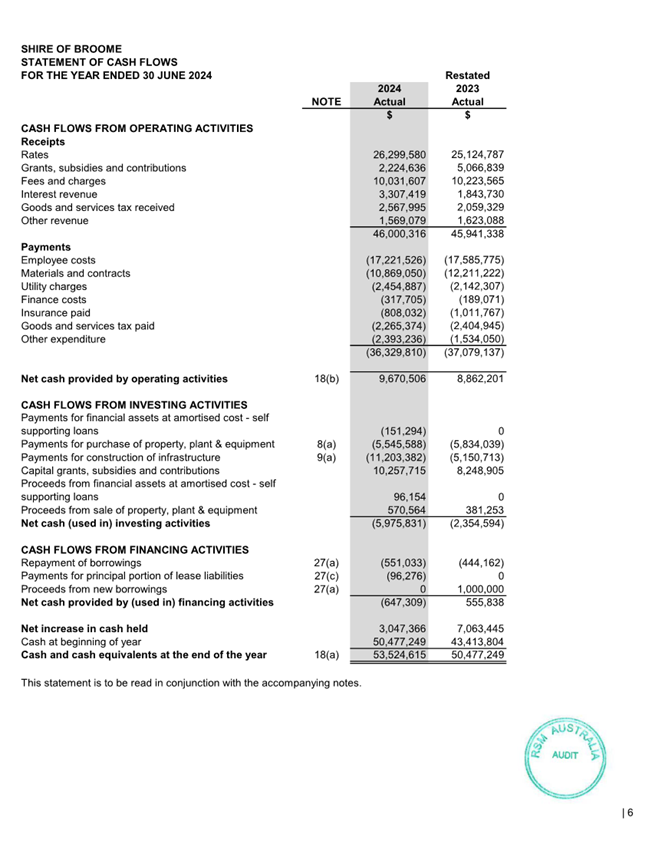

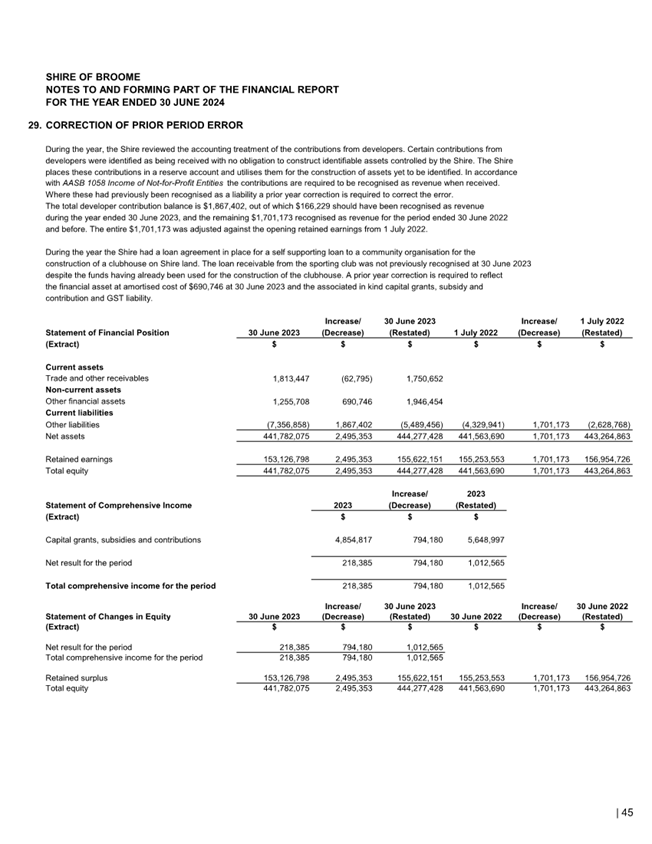

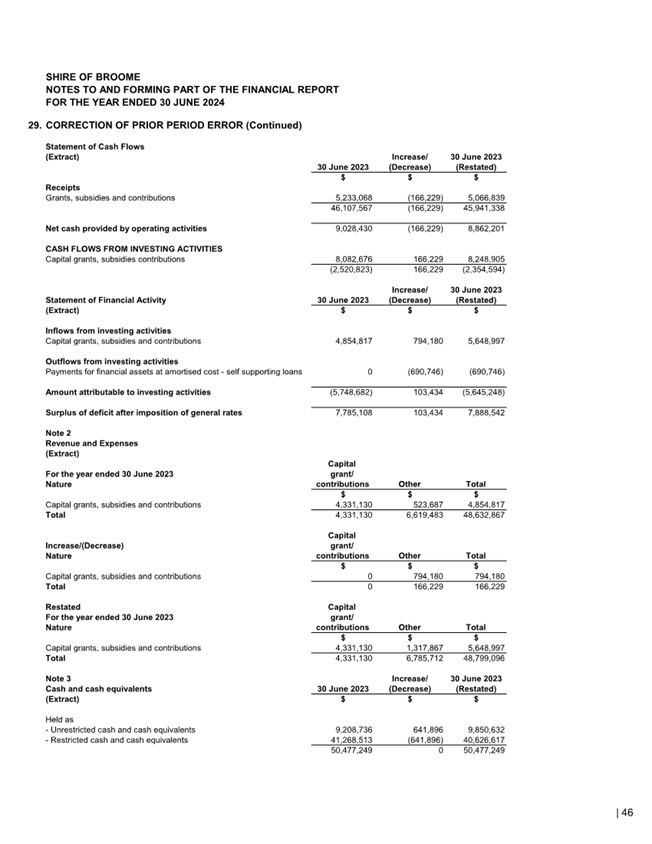

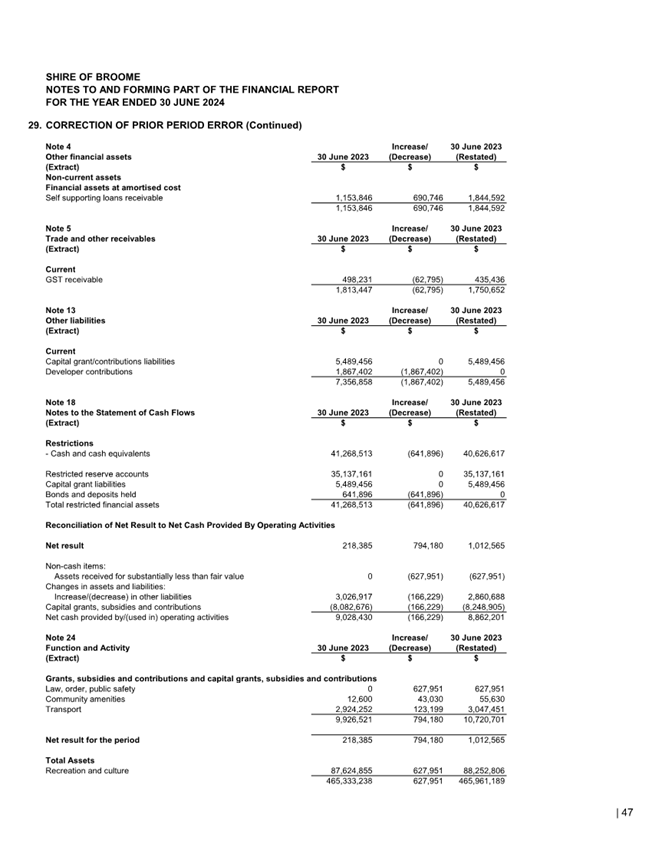

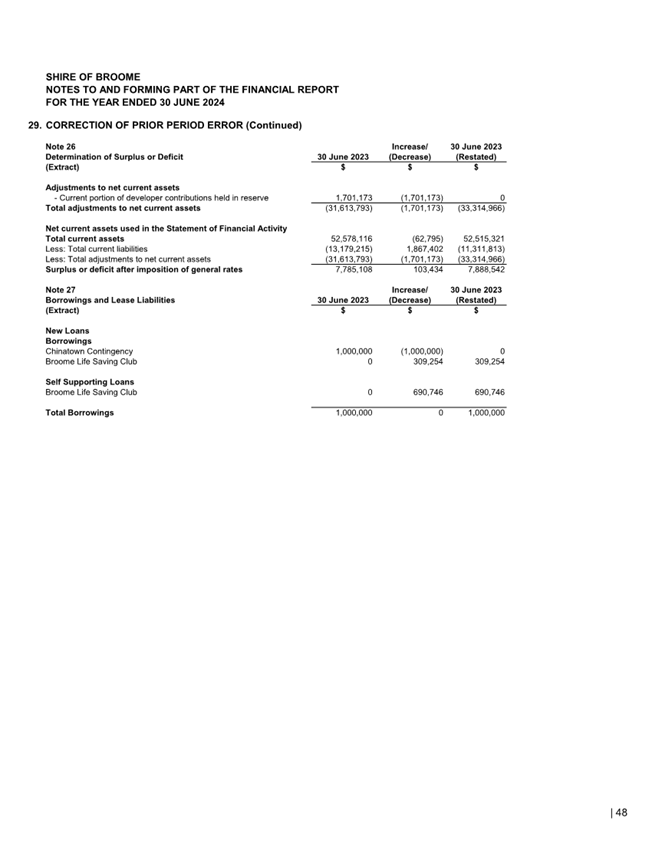

The emphasis of matter pertains to the Restatement of Comparative Balances. Specifically, attention is drawn to Note 29 of the financial report, which outlines that amounts reported in the previously issued 30 June 2023 financial report have been restated and disclosed as comparatives in this financial report. The audit opinion remains unmodified regarding this matter. The two restatements are the result of a review of accounting treatment, summarised below:

1. Developer Contributions: During the year, the Shire reviewed its accounting for developer contributions and determined that they did not meet the statutory definition of a "developer contribution." Instead, these are Standard Infrastructure Contributions under AASB 1058 and should be recognised as revenue upon receipt.

As a result, prior year contributions were corrected by removing the liability balance from the Balance Sheet and adjusting the Retained Surplus – Equity account. This is considered a material prior year error, corrected in the 2023/24 financial year with comparatives restated for 2022/23. The funds will continue to be transferred to the Shire’s Reserve Fund as per Council policy.

A prior year correction recognised $166,229 as revenue for the year ended 30 June 2023 and $1,701,173 for the year ended 30 June 2022, with the latter adjustment reflected in opening retained earnings as of 1 July 2022. The collection and use of the funds remain unchanged, but the accounting treatment now accurately reflects their nature.

2. Self- Supporting Loan (BSLSC): The Shire revised the recognition of a loan receivable for the construction of a clubhouse on Shire land. A $1,000,000 loan was drawn in 2022/23 to part-fund the project. However, the self-supporting loan agreement was not signed by both parties, and the 2023 financial report recognised the loan liability but not the receivable.

As the agreement remains unsigned and there was uncertainty about the correct accounting treatment, external accounting advice, audit teams from RSM and OAG, and Shire management agreed to recognise part of the receivable in the 2024 financial report. $690,746 of the loan has been recognised as self-supporting as a prior year adjustment, with an additional $151,294 recognised in 2024, and the remaining $157,960 to be recognised in the 2025 financials once the agreement is signed.

No significant issues were raised requiring a report to the Minister.

Audit Findings

The 2024 final audit raised eight internal control improvement recommendations, identified in the table below. The Management Letter (Confidential Attachment 3) provides further detail on each finding, including an audit recommendation and Management comment. No findings identified were determined to be significant. The contents of the report are deemed confidential due to the potential risk of increased vulnerability to fraudulent or illegal activities if released publicly.

|

Findings |

Prior year finding |

Rating |

Target completion date |

|

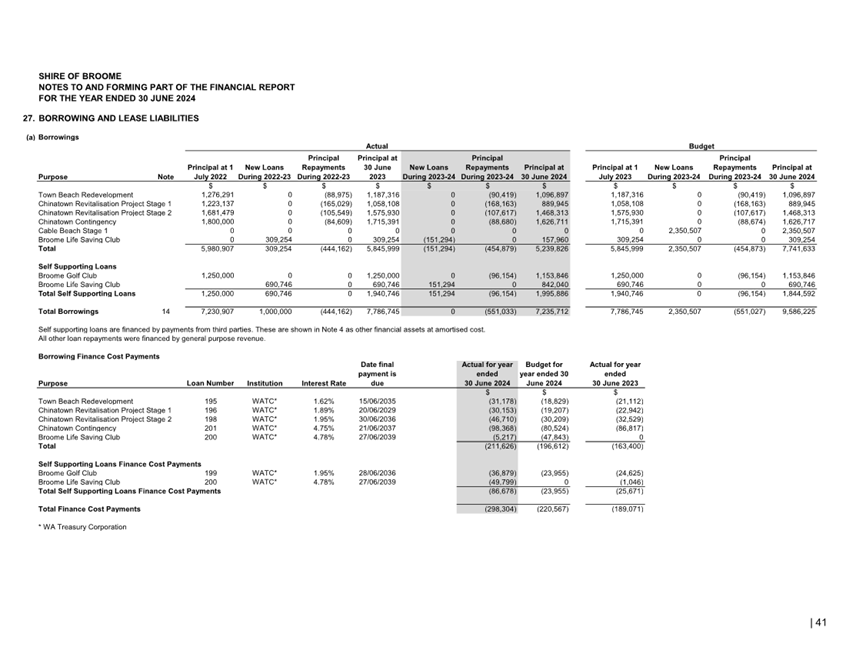

1. Incorrect recognition of Loan Receivable from the Broome Surf Life Saving Club |

Moderate |

30-Jun-25 |

|

|

2. Timeliness and evidence of review of general journals |

Moderate |

31-Jan-25 |

|

|

3. Non-timely reconciliation of key account balances |

Yes |

Moderate |

30-Jun-25 |

|

4. Non-confirmation of goods received or services transferred |

Minor |

30-Jun-25 |

|

|

5. No testing of business continuity (BCP) and disaster recovery plan (DRP) |

Minor |

DRP:

31-Jan-25 |

|

|

6. Portable and attractive assets register not maintained |

Yes |

Minor |

30-Jun-25 |

|

7. Bonds and deposits register not maintained |

Yes |

Minor |

28-Feb-25 |

|

8. No policies and procedures for Inventory management |

Yes |

Minor |

31-Dec-25 |

Audit findings are rated as either significant, moderate or minor. Four of the findings are new (two moderate and two minor), and four have been identified in a prior audit, which are being progressed by Officers (one moderate, three minor). Officers have proposed completion dates for each item.

Outstanding items will be addressed and presented at each subsequent ARC meeting until appropriately resolved.

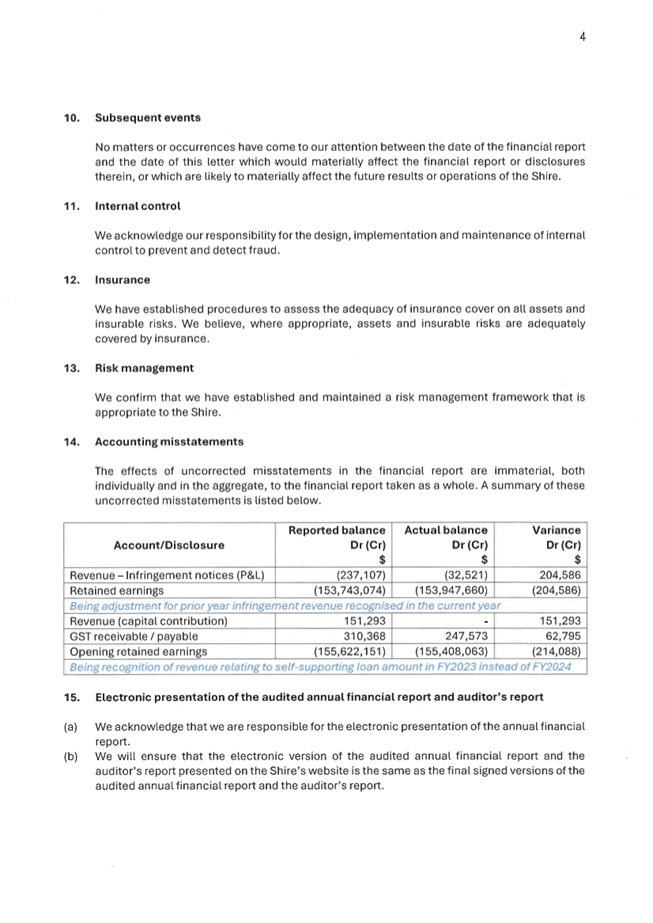

Identified Accounting Misstatements

The auditors identified two minor misstatements in the financial report that remain unadjusted. These items, detailed below, are included in the Management Representation Letter (Attachment 1) as required under Auditing Standard ASA 320, Materiality and Audit Adjustments:

1. $204,586 – Infringement notice revenue recognised in the current financial year but relating to the prior year.

2. $214,088 – Self-supporting loan contribution recognised in the current financial year but relating to the prior year.

Both items were thoroughly reviewed and discussed between the Shire, RSM, and OAG, with agreement reached on the presentation of these unadjusted items.

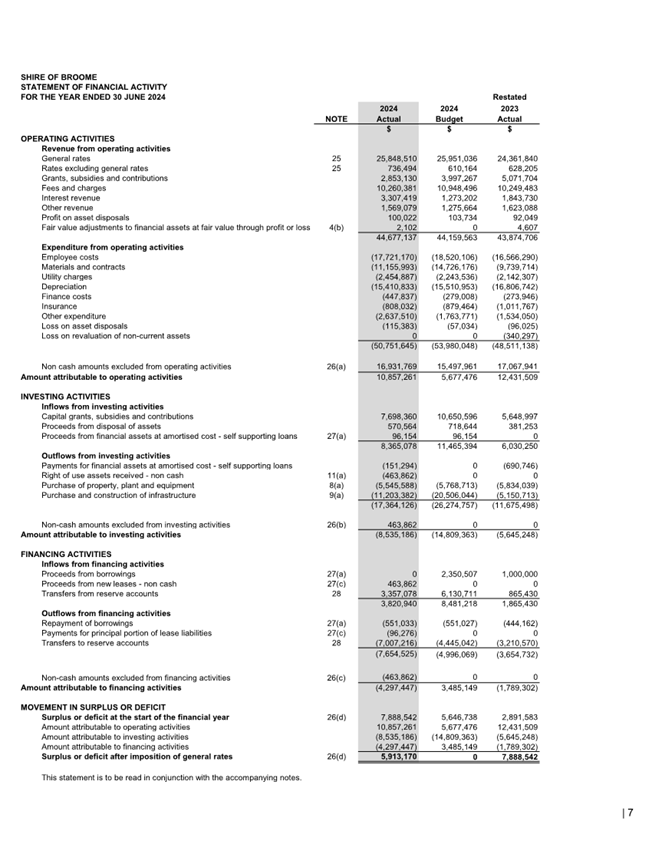

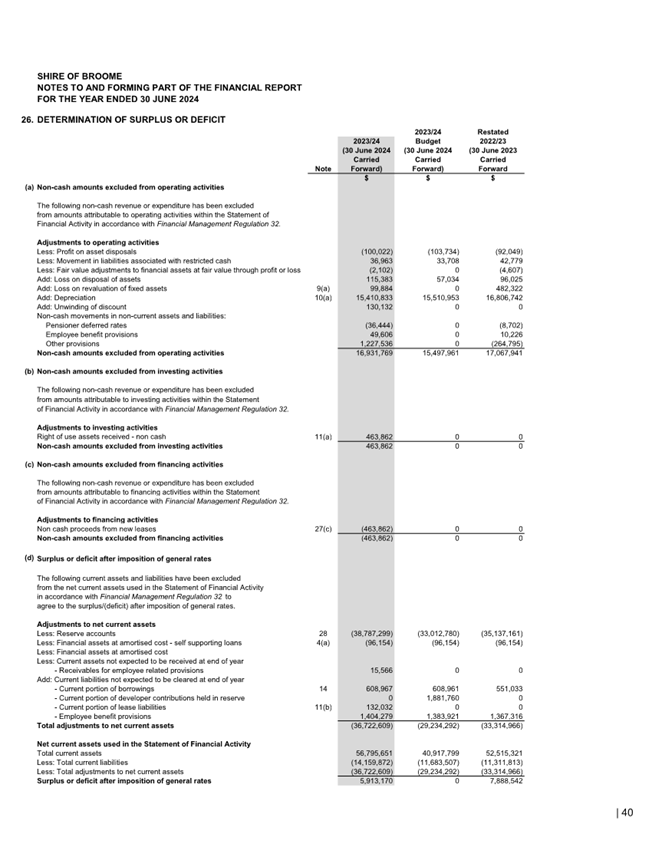

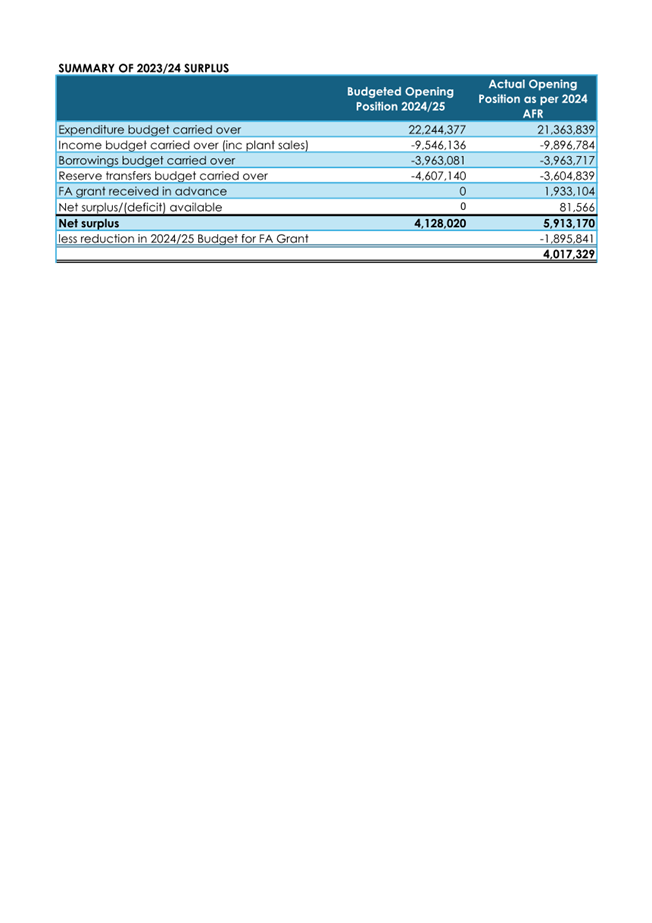

2023/24 Operating Result

The Audited Financial Report for the year ended 30 June 2024 received audit signoff on 9 December 2024, and resulted in a $5,913,170 carried forward operating surplus, which is summarised below:

|

Budgeted Opening Position 2024/25 |

Actual Opening Position as per 2024 AFR |

|

|

Expenditure budget carried over |

22,244,377 |

21,237,420 |

|

Income budget carried over (inc plant sales) |

-9,546,136 |

-9,770,364 |

|

Borrowings budget carried over |

-3,963,081 |

-3,963,717 |

|

Reserve transfers budget carried over |

-4,607,140 |

-3,604,839 |

|

FA grant received in advance |

0 |

1,933,104 |

|

Net surplus/(deficit) available |

0 |

81,566 |

|

Net surplus |

4,128,020 |

5,913,170 |

|

less reduction in 2024/25 Budget for FA Grant |

-1,895,841 |

|

|

4,017,329 |

The actual surplus amount stated excludes non-cash transactions such as depreciation, gains or losses from asset revaluations, profit or loss from plant disposal, and provisions for credit losses.

Budget Overview: The 2024/25 Annual Budget, adopted at the Special Council Meeting on 22 August 2024, included an estimated carried-forward operating surplus of $4,128,020 from the 2023/24 financial year. This surplus comprised:

· $22,244,377 for ongoing or externally funded projects.

· $14,153,276 from cashflows linked to reserves, asset sales, and external grants.

· $3,963,081 from proposed borrowings for Cable Beach Stage 1 and the Staff Housing project.

These figures were preliminary and calculated before the finalisation of the 2023/24 financial year.

Final Financial Position: After completing year-end processes, the confirmed carried-forward surplus is $5,913,170, broken down as follows:

· $1,933,104 from advance Financial Assistance Grant funding.

· $3,017,638 net surplus from capital projects.

· $880,862 net surplus from operating projects.

· $81,566 untied surplus.

Advance Financial Assistance Grant Impact: The Federal Government provides an annual Financial Assistance Grant (covering general purpose and road funding) through the WA Local Government Grants Commission. The 2024/25 allocation was partially paid in advance on 26 June 2024, inflating the 2023/24 closing position. This requires an amendment to the 2024/25 budget to account for the advance payment ($1,895,841 decrease in income). Additional grant funds are expected later in 2024/25 to complete the annual allocation.

Budget Compliance and Monitoring: The Shire of Broome is required to budget for an end-of-year closing position of $0, or within 10% of the rates raised, as per statutory principles. The Shire adopts a $0 closing balance position.

To ensure compliance, internal controls including quarterly budget reviews are in place. Responsible officers review expenditures and forecast potential variances. All budget amendments must be approved by an Absolute Majority of Council.

During the 3rd quarter budget review for 2023/24, a closing deficit of $213,342 was forecast for 30 June 2024, assuming all budgets were met. This forecast considered the cash needed to maintain services and projects and was detailed in quarterly reviews and monthly financial statements.

Following end-of-year reconciliations and audit, the final untied surplus is confirmed at $81,566.

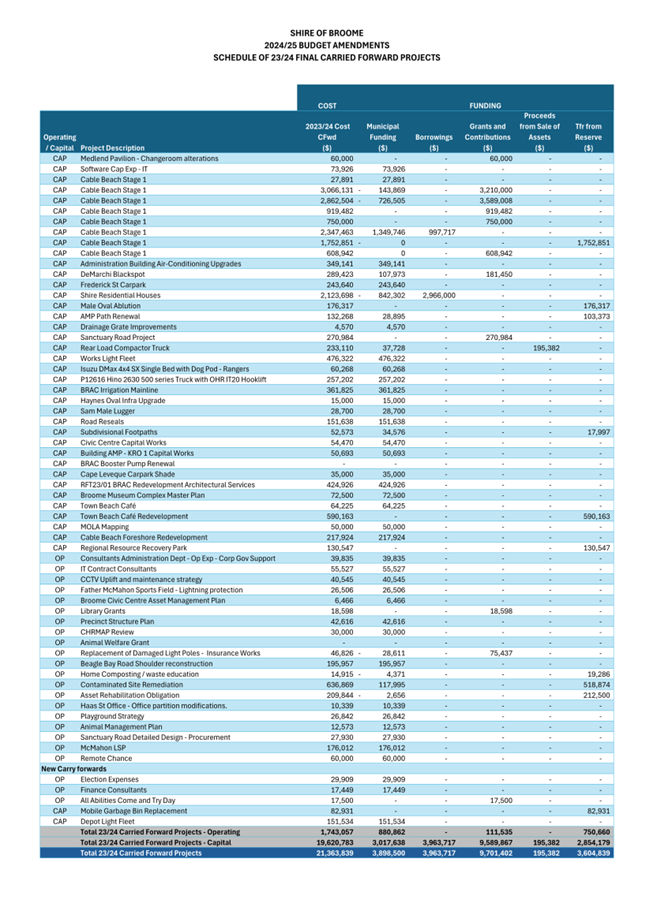

Carry-Over Projects: The Executive Management Group has reviewed the carry-over project list to ensure all retained projects are essential. These include:

· Grant or reserve-funded projects,

· Committed projects,

· Asset Management Plan (AMP) renewals, where funds are allocated to appropriate reserves for future use.

CONSULTATION

The preparation of the Annual Financial Report involved collaboration with key stakeholders to ensure compliance with statutory requirements and alignment with financial management best practices. This included:

· The Office of the Auditor General (OAG) and its contracted auditing firm, RSM Australia (RSM), to oversee the audit process and address audit requirements.

· Moore Australia, which provided technical local government accounting advice and preparation of the statutory financial report.

· Source Business Partners, who prepared the financial workpapers and provided specialist advice on local government financial reporting.

· The Department of Local Government, Sport and Cultural Industries, for guidance on regulatory compliance.

These partnerships ensured a thorough and transparent process in the preparation and review of the Annual Financial Report.

STATUTORY ENVIRONMENT

Local Government Act 1995

6.4. Financial report

(1) A local government is to prepare an annual financial report for the preceding financial year and such other financial reports as are prescribed.

(2) The financial report is to —

(a) be prepared and presented in the manner and form prescribed; and

(b) contain the prescribed information.

(3) By 30 September following each financial year or such extended time as the Minister allows, a local government is to submit to its auditor —

(a) the accounts of the local government, balanced up to the last day of the preceding financial year; and

(b) the annual financial report of the local government for the preceding financial year.

s7.9 Audit to be conducted

(1) An auditor is required to examine the accounts and annual financial report submitted for audit and, by the 31 December next following the financial year to which the accounts and report relate or such later date as may be prescribed, to prepare a report thereon and forward a copy of that report to —

(a) the mayor or president; and

(b) the CEO of the local government; and

(c) the Minister.

(2) Without limiting the generality of subsection (1), where the auditor considers that —

(a) there is any error or deficiency in an account or financial report submitted for audit; or

(b) any money paid from, or due to, any fund or account of a local government has been or may have been misapplied to purposes not authorised by law; or

(c) there is a matter arising from the examination of the accounts and annual financial report that needs to be addressed by the local government, details of that error, deficiency, misapplication or matter, are to be included in the report by the auditor.

(3) The Minister may direct the auditor of a local government to examine a particular aspect of the accounts and the annual financial report submitted for audit by that local government and to —

(a) prepare a report thereon; and

(b) forward a copy of that report to the Minister, and that direction has effect according to its terms.

(4) If the Minister considers it appropriate to do so, the Minister is to forward a copy of the report referred to in subsection (3), or part of that report, to the CEO of the local government

7.12A. Duties of local government with respect to audits

(1) A local government is to do everything in its power to —

(a) assist the auditor of the local government to conduct an audit and carry out the auditor’s other duties under this Act in respect of the local government; and

(b) ensure that audits are conducted successfully and expeditiously.

(2) Without limiting the generality of subsection (1), a local government is to meet with the auditor of the local government at least once in every year.

(3) A local government must —

(aa) examine an audit report received by the local government; and

(a) determine if any matters raised by the audit report, require action to be taken by the local government; and

(b) ensure that appropriate action is taken in respect of those matters

(4) A local government must —

(a) prepare a report addressing any matters identified as significant by the auditor in the audit report, and stating what action the local government has taken or intends to take with respect to each of those matters; and

(b) give a copy of that report to the Minister within 3 months after the audit report is received by the local government.

(5) Within 14 days after a local government gives a report to the Minister under subsection (4)(b), the CEO must publish a copy of the report on the local government’s official website.

Local Government (Audit) Regulations 1996

Local Government (Financial Management) Regulations 1996

Local governments are required to present to Council an audited annual financial report for the preceding financial year, within specified timeframes as prescribed.

POLICY IMPLICATIONS

Nil.

FINANCIAL IMPLICATIONS

Adopting the Annual Financial Report ensures compliance with statutory financial reporting obligations and promotes transparency for both Council and the community.

The committed expenditure and corresponding income sources detailed in Attachment 5 will require an absolute majority vote to approve any budget amendments for the 2024/25 financial year. Furthermore, reconciling the final financial position with proposed carryover projects will also necessitate an absolute majority decision to allocate the untied portion of the net surplus.

Officers recommend $81,566 of the untied surplus funds are transferred to the Public Open Space (POS) Reserve to support the Walmanyjun Cable Beach Foreshore Redevelopment Stage 2.

RISK

The audited Annual Financial Report is a critical control tool, ensuring transparency and accountability in the Shire’s financial management. It communicates to Council and stakeholders that the financial position, operational outcomes, cash flows, equity changes, and financial activities are free from material misstatements due to fraud or error.

The audit findings highlight areas where improvements are necessary, prompting management to either implement corrective measures or recommend reviews of existing processes. These actions support the Shire’s ongoing efforts to maintain robust internal controls and sound financial governance.

The report also evaluates Council’s financial capacity to meet its strategic and operational objectives. Identified variances or findings may highlight the need to reassess budget assumptions, workforce allocation, or overall resource capacity to achieve strategic goals effectively.

A recommendation from the Committee for Council to adopt the Annual Financial Report, Audit and Management Reports, and the CEO’s Report is crucial to ensure compliance with statutory requirements. Failure to adopt these documents could delay the approval of the 2023/24 Annual Report, which would, in turn, impact the timely scheduling of the Annual Electors’ Meeting (AEM). This represents a significant risk, as it could disrupt compliance with statutory obligations related to the AEM. Furthermore, such delays could have a substantial reputational impact, as the AEM attracts considerable attention from ratepayers and the community.

Should the Committee recommend alternative allocations for the 2023/24 surplus, aligned with Council’s risk appetite, the associated risk is considered moderate. This risk can be effectively mitigated through adherence to the report recommendations, ensuring clarity and alignment with strategic priorities.

STRATEGIC ASPIRATIONS

Performance - We will deliver excellent governance, service & value for everyone.

Outcome 13 - Value for money from rates and long term financial sustainability

Objective 13.1 Plan effectively for short- and long-term financial sustainability

Outcome 14 - Excellence in organisational performance and service delivery

Objective 14.3 Monitor and continuously improve performance levels.

VOTING REQUIREMENTS

|

(Report Recommendation) Minute No. AR/1224/003 Moved: Shire President C Mitchell Seconded: Cr M Virgo That the Audit and Risk Committee recommends that Council: 1. Receive the Chief Executive Officer’s report relating to the audit. 2. Receive the: (a) Management Representation Letter as per Attachment 1; (b) Audited Annual Financial Report including the Independent Auditor’s Report as per Attachment 2; and (c) Audit Management Letter as per Confidential Attachment 3. 3. Adopt the Audited Annual Financial Report dated 9 December 2024 and the Audit Management Letter for the year ended 30 June 2024 as per Attachment 2 and 3 respectively. 4. Confirms the allocation of the net surplus from the 2023/24 financial year as per Attachment 4 with the balance of $81,566. 5. Acknowledging the advance payment of the Financial Assistance Grant in June 2024, approves budget amendments to decrease GL 100303010 General Purpose Grant by $1,429,836 and GL 101203050 Untied Roads Grant by $466,005. 6. Approves an allocation of $81,566 of net 2023/24 surplus to GL 101119890 Transfer to POS Reserve for Walmanyjun Cable Beach Foreshore Redevelopment Stage 2. |

|

Management Representation Letter |

|

|

2024 Audited Annual Financial Report including Independent Auditor's Report |

|

|

Audit Management Letter (Confidential to Councillors and Directors Only) This attachment is confidential in accordance with section 5.23(2) of the Local Government Act 1995 section 5.23(2)((f)(ii)) as it contains “a matter that if disclosed, could be reasonably expected to endanger the security of the local governments property”. |

|

|

2023/24 Final Carried Forward Projects |

Minutes – Audit and Risk Committee Meeting 10 December 2024 Page 1 of 4

Nil.

There being no further business the Chair declared the meeting closed at 10:03 AM.