AGENDA

FOR THE

Audit and Risk Committee Meeting

18 February 2025

NOTICE OF MEETING

Dear Council Member,

The next Audit and Risk Committee of Council will be held on Tuesday, 18 February 2025 in the Council Chambers, Corner Weld and Haas Streets, Broome, commencing at 2:30PM.

Regards,

![]()

S MASTROLEMBO

Chief Executive Officer

19/02/2025

Our Mission

"To deliver affordable and quality Local Government services."

DISCLAIMER

The purpose of Council Meetings is to discuss, and where possible, make resolutions about items appearing on the agenda. Whilst Council has the power to resolve such items and may in fact, appear to have done so at the meeting, no person should rely on or act on the basis of such decision or on any advice or information provided by a Member or Officer, or on the content of any discussion occurring, during the course of the meeting.

Persons should be aware that the provisions in section 5.25 of the Local Government Act 1995 establish procedures for revocation or rescission of a Council decision. No person should rely on the decisions made by Council until formal advice of the Council decision is received by that person. The Shire of Broome expressly disclaims liability for any loss or damage suffered by any person as a result of relying on or acting on the basis of any resolution of Council, or any advice or information provided by a Member or Officer, or the content of any discussion occurring, during the course of the Council meeting.

Should you require this document in an alternative format please contact us.

Agenda – Audit and Risk Committee Meeting 18 February 2025 Page 1 of 4

SHIRE OF BROOME

Audit and Risk Committee Meeting

Tuesday 18 February 2025

INDEX – Agenda

3. Declarations Of Financial Interest / Impartiality

5.1 COMPLIANCE AUDIT RETURN 2024

5.2 2ND QUARTER FINANCE AND COSTING REVIEW 2024-25

Agenda – Audit and Risk Committee Meeting 18 February 2025 Page 1 of 4

|

That the Minutes of the Audit and Risk Committee held on 10 December 2024, as published and circulated, be confirmed as a true and accurate record of that meeting.

|

Agenda – Audit and Risk Committee Meeting 18 February 2025 Page 1 of 4

|

LOCATION/ADDRESS: |

Nil |

|

APPLICANT: |

Nil |

|

FILE: |

LCR02 |

|

AUTHOR: |

Manager Governance, Strategy And Risk |

|

CONTRIBUTOR/S: |

Nil |

|

RESPONSIBLE OFFICER: |

Director Corporate Services |

|

DISCLOSURE OF INTEREST: |

Nil |

|

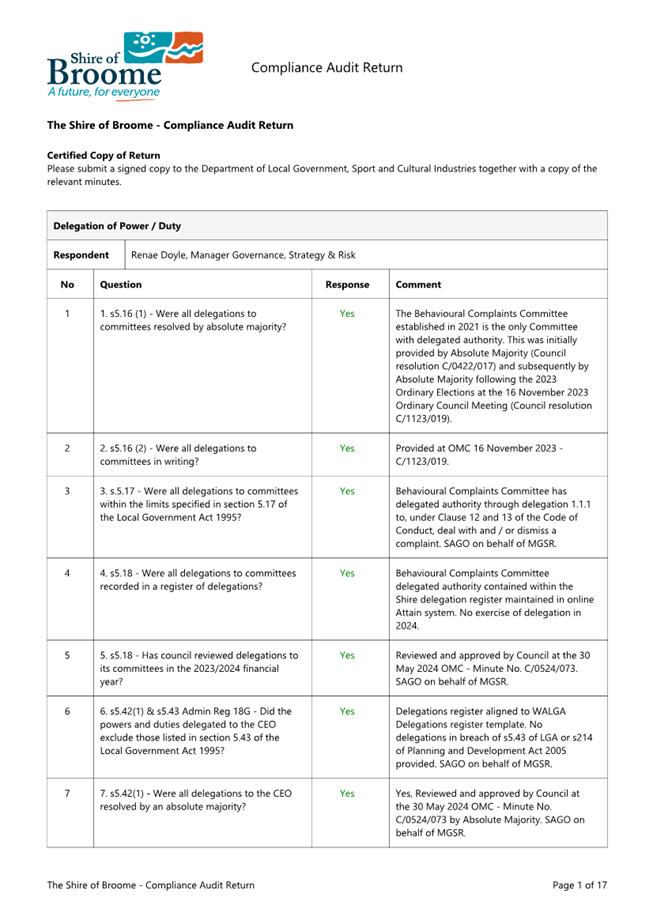

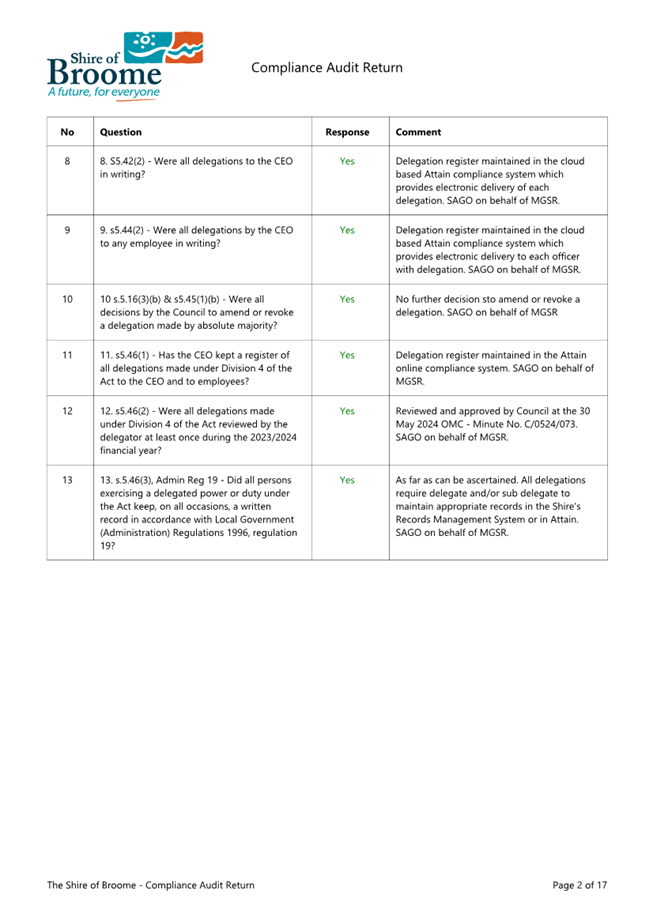

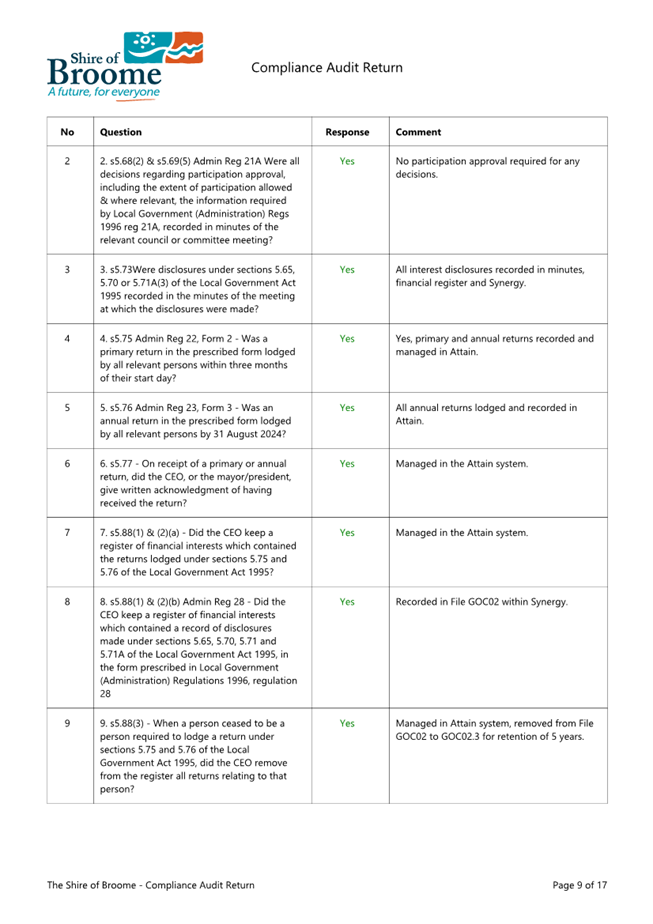

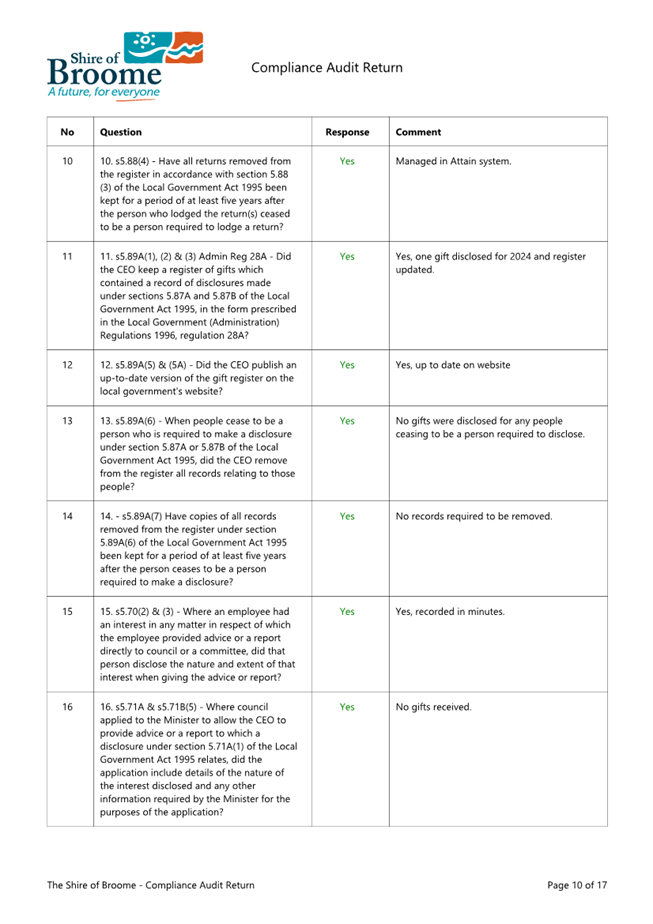

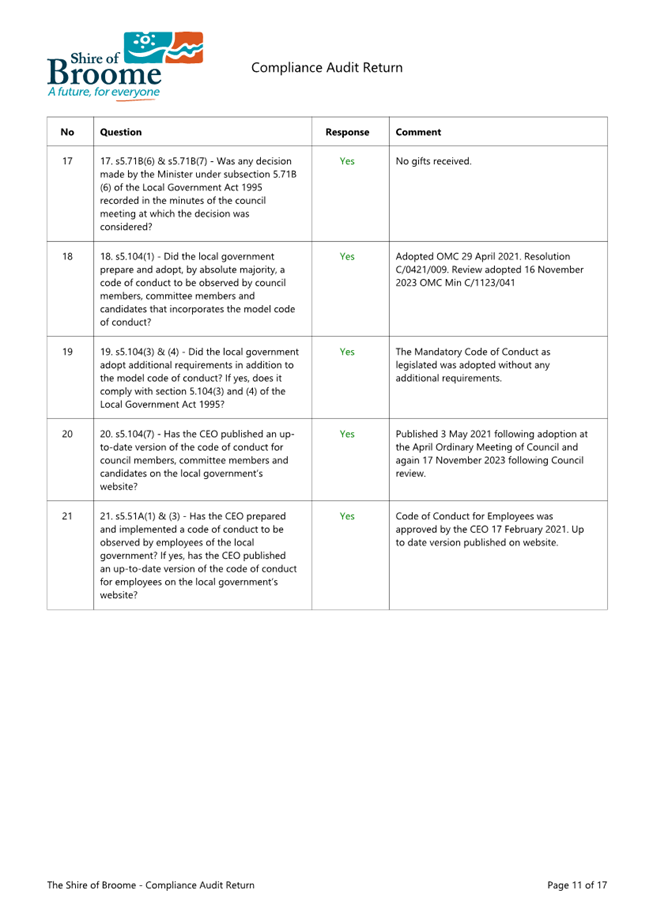

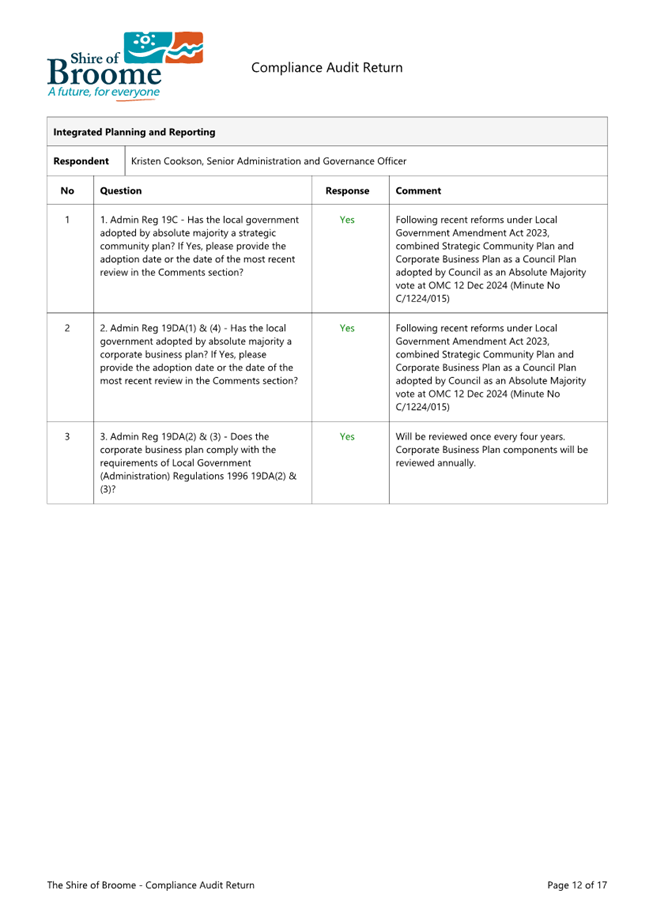

SUMMARY: The Department of Local Government, Sport and Cultural Industries (DLGSC) requires the Shire of Broome (Shire) to complete a Compliance Audit Return (CAR) annually. The Audit and Risk Committee (ARC) is requested to recommend that Council adopt the attached CAR for the period of 1 January 2024 to 31 December 2024 (Attachment 1) for submission to the Department of Local Government, Sport and Cultural Industries (DLGSC) by 31 March 2024. |

Previous Considerations

ARC 20 February 2024 Item 5.1

Local governments are required to complete an annual compliance audit for the previous calendar year by the 31 March. The DLGSC provides the questions each year with the compliance audit being an in-house self-audit that is undertaken by the appropriate responsible officer.

Section 7.13(i) of the Local Government Act 1995, and Regulations 13, 14 and 15 of the Local Government (Audit) Regulations 1996, outline the requirements for completion of the CAR.

Regulation 14 of the Local Government (Audit) Regulations 1996 requires the Audit and Risk Committee (ARC) to review the CAR and report to Council the results of that review. The CAR is to be:

1. presented to an Ordinary Meeting of Council;

2. adopted by Council; and

3. recorded in the minutes of the meeting at which it is adopted.

Following the adoption by Council of the CAR, a certified copy of the return, along with the relevant section of the minutes and any additional information detailing the contents of the return are to be submitted to the DLGSC by 31 March 2025.

The return requires the Shire President and the Chief Executive Officer to certify that the statutory obligations of the Shire of Broome have been complied with.

COMMENT

The DLGSC continues to focus on high risk areas of compliance and statutory reporting as prescribed in Regulation 13 of the Local Government (Audit) Regulations 1996.

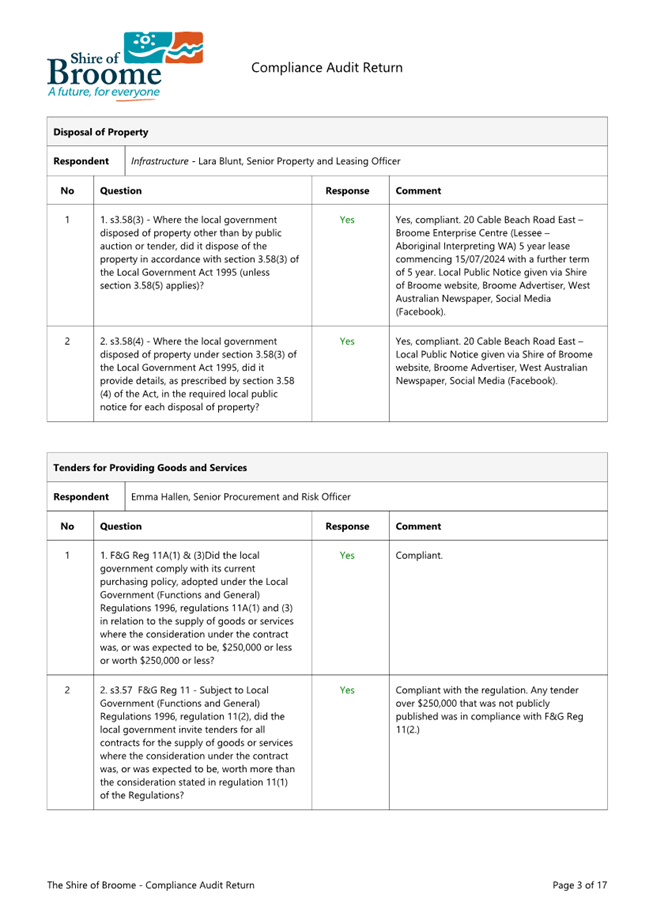

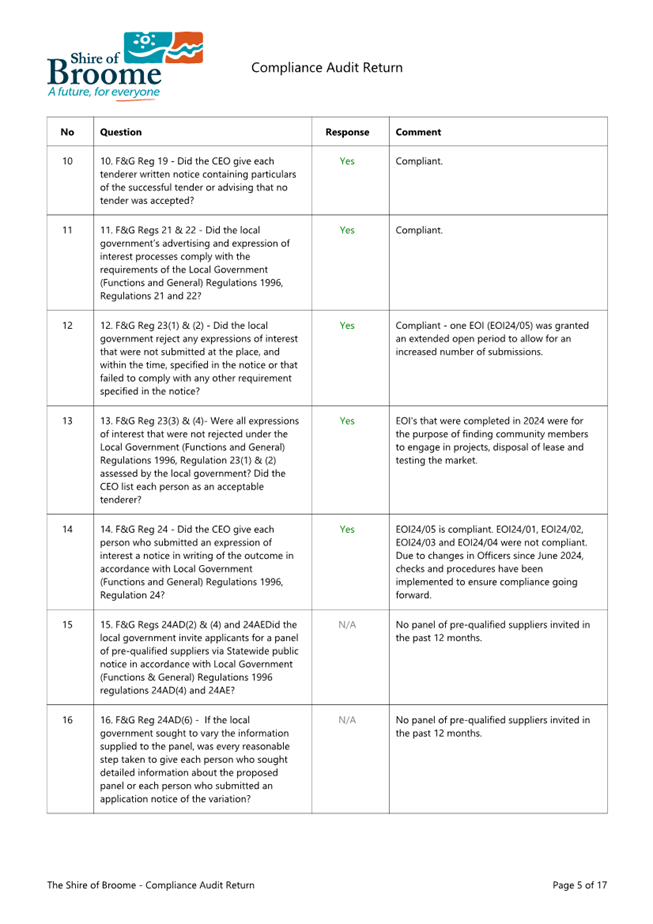

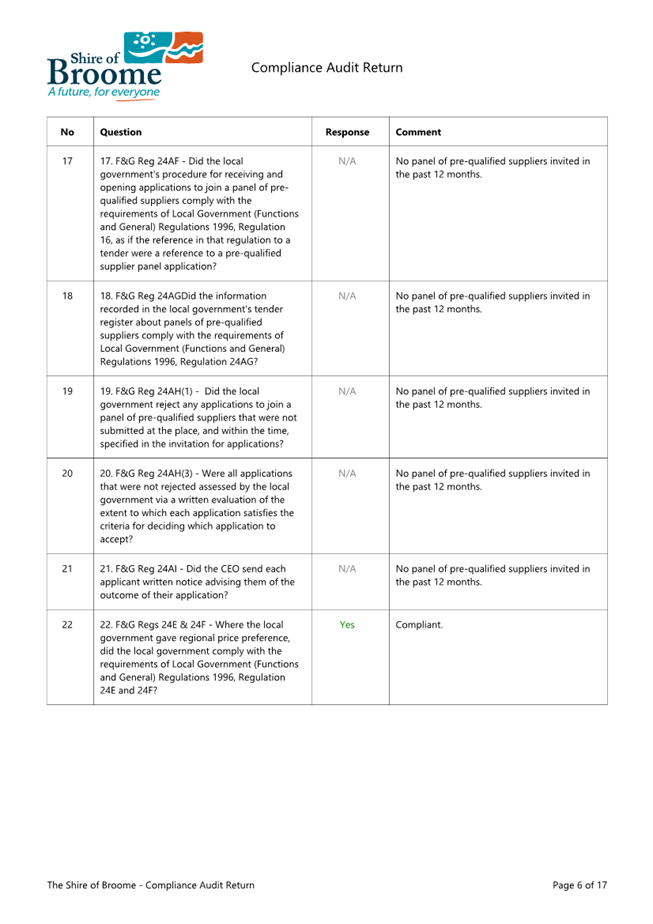

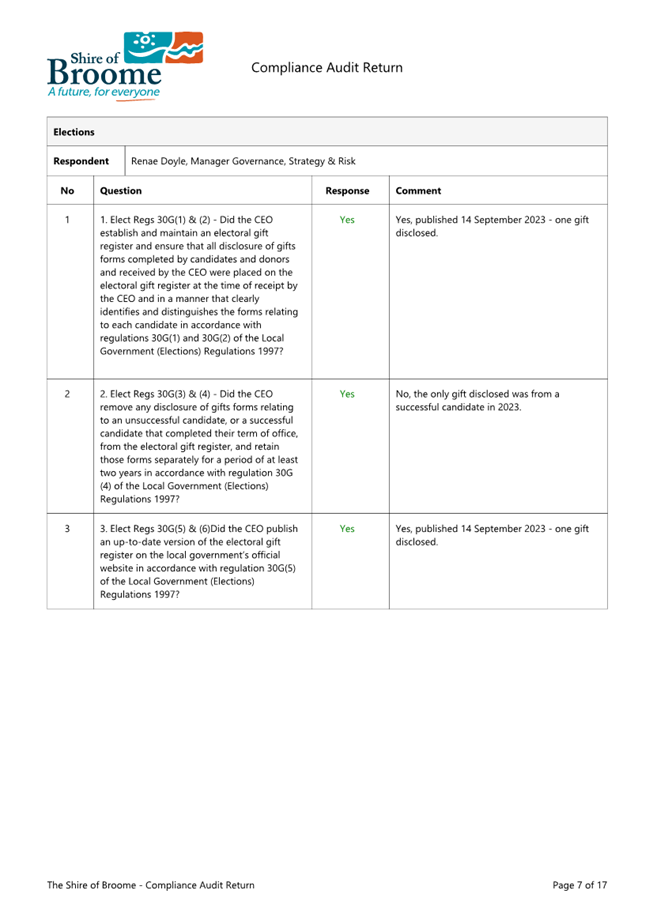

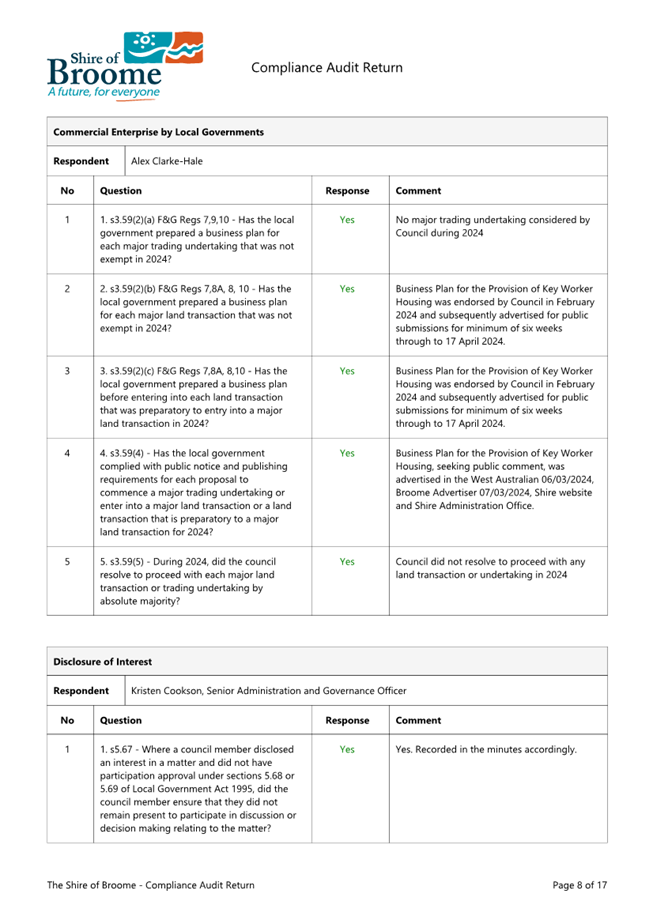

The CAR for the period 1 January to 31 December 2024 comprises a total of 94 questions. The questions are the same as the previous year. The key focus areas covered in the CAR are as follows:

|

Focus Area |

2024 Questions |

|

Commercial Enterprises by Local Governments |

5 |

|

Delegation of Power/Duty |

13 |

|

Disclosure of Interest |

25 |

|

Disposal of Property |

2 |

|

Elections |

3 |

|

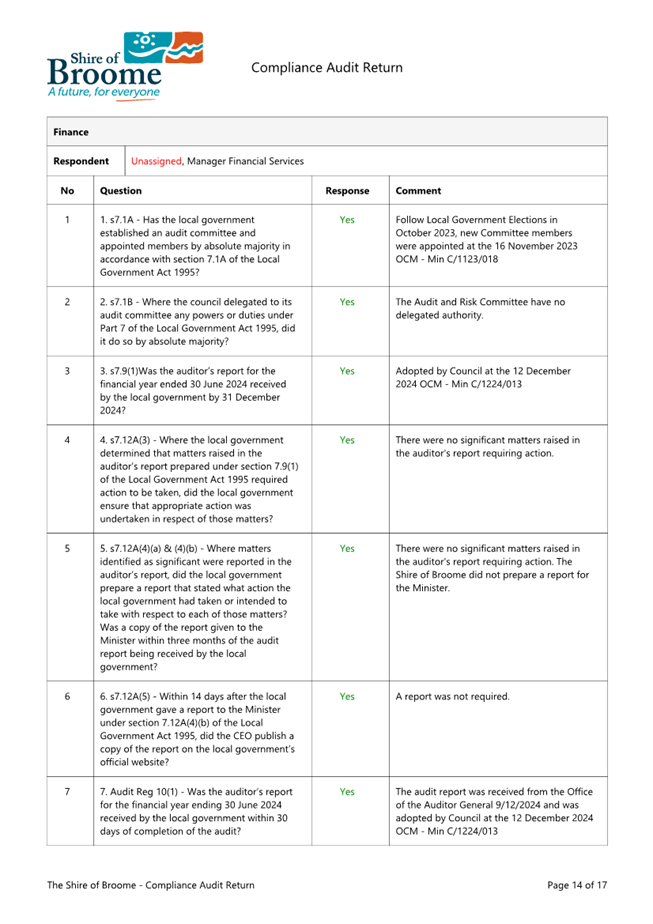

Finance |

7 |

|

Integrated Planning and Reporting |

3 |

|

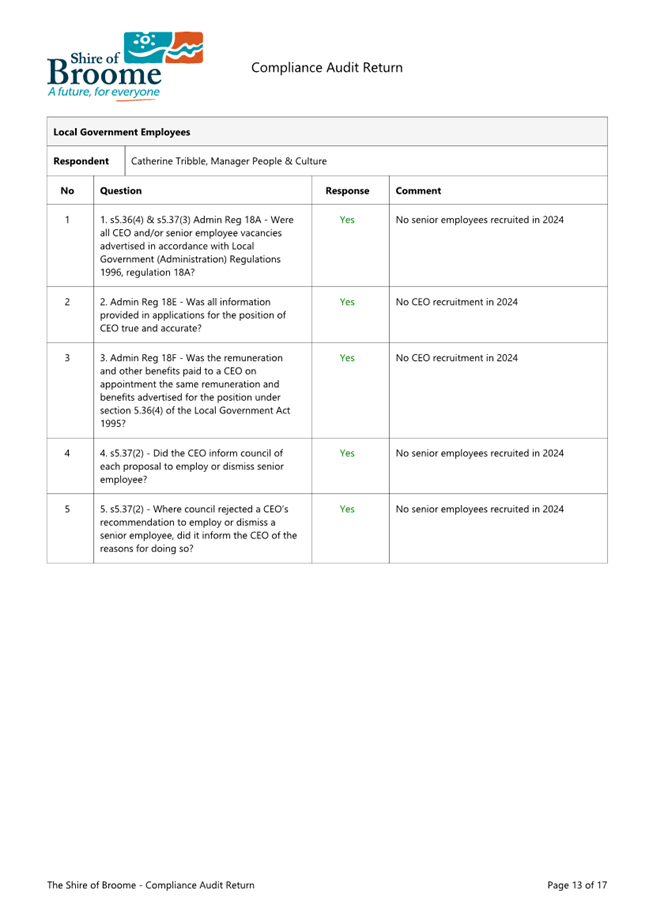

Local Government Employees |

5 |

|

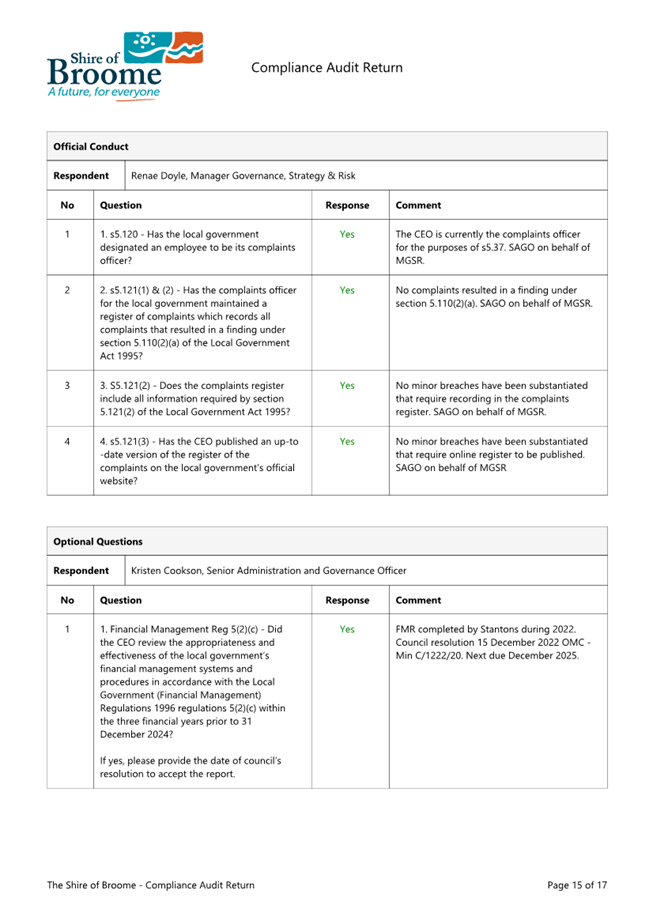

Official Conduct |

4 |

|

Optional Questions |

9 |

|

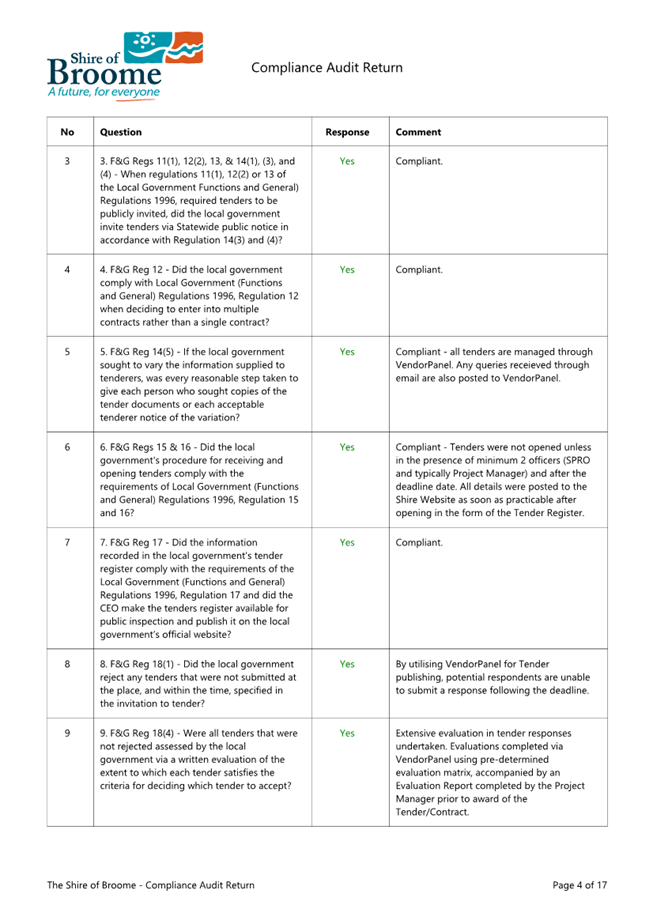

Tenders for Providing Goods and Services |

22 |

|

Total |

94 |

During 2024, responsible officers monitored compliance in each of the focus areas through the Shire’s cloud-based compliance system, Attain. This has continued an increased awareness of compliance obligations within the Shire and allowed the capture of compliance evidence in a central repository. This compliance system reduces the risk of non-compliance and streamlines compilation of the annual return.

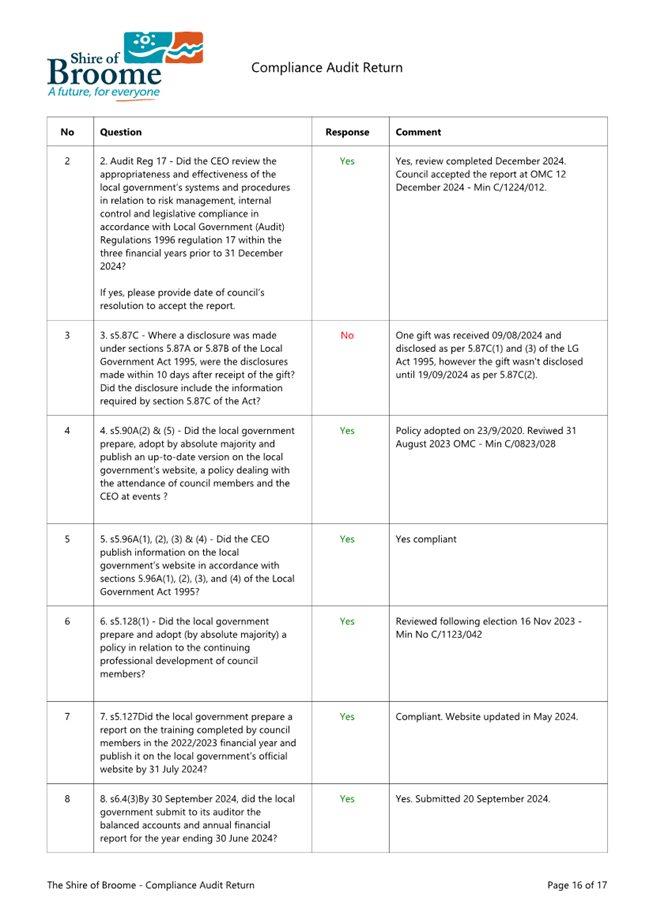

A compliance rating of 98% has been achieved for 2024 with one minor non-compliance identified in the optional questions area as follows:

|

Focus Area |

Question |

Comments |

|

Optional Questions |

Where a disclosure was made under sections 5.87A or 5.87B of the Local Government Act 1995, were the disclosures made within 10 days after receipt of the gift? Did the disclosure include their information required by section 5.87C of the Act? |

One gift was received 09/08/2024 and disclosed as per 5.87C(1) and (3) of the Local Government Act 1995, however the gift was not disclosed until 19/09/2024 as per 5.87C(2). |

The Shire will focus on the requirements pertaining to gift disclosures for both staff and elected members to ensure that these requirements are well understood going forward.

The CAR result continues the Shire’s strong history of compliance with the requirements of the Local Government Act (1995), with minimal non compliances reported over the last 5 years and none of a significant risk nature.

It is important to emphasise that the CAR is limited in scope.

Local Governments must also adhere to more than 200 additional legislative instruments, encompassing a broad range of areas such as governance, planning, environmental management, public health, and financial accountability. These laws collectively regulate various aspects of local government operations, ensuring compliance with state and federal requirements.

CONSULTATION

Department of Local Government, Sport and Cultural Industries.

STATUTORY ENVIRONMENT

Local Government Act 1995

7.13 Regulations as to audit

(1) Regulations may make provision as follows —

(i) – requiring local governments to carry out, in the prescribed manner and in a

form approved by the Minister, an audit of compliance with such statutory

requirements as are prescribed whether those requirements are —

(i) of a financial nature or not; or

(ii) under this Act or another written law.

Local Government (Audit) Regulations 1996

13. Prescribed statutory requirements for which compliance audit needed (Act s. 7.13(1)(i))

For the purposes of section 7.13(1)(i) the statutory requirements set forth in the Table to this regulation are prescribed.

14. Compliance audits by local governments

(1) A local government is to carry out a compliance audit for the period 1 January to 31 December in each year.

(2) After carrying out a compliance audit the local government is to prepare a compliance audit return in a form approved by the Minister.

(3A) The local government’s audit committee is to review the compliance audit return and is to report to the council the results of that review.

(3) After the audit committee has reported to the council under subregulation (3A), the compliance audit return is to be —

(a) presented to the council at a meeting of the council; and

(b) adopted by the council; and

(c) recorded in the minutes of the meeting at which it is adopted.

15. Compliance audit return, certified copy of etc. to be given to Departmental CEO

(1) After the compliance audit return has been presented to the council in accordance with regulation 14(3) a certified copy of the return together with —

(a) a copy of the relevant section of the minutes referred to in regulation 14(3)(c); and

(b) any additional information explaining or qualifying the compliance audit,

is to be submitted to the Departmental CEO by 31 March next following the period to which the return relates.

POLICY IMPLICATIONS

Nil.

FINANCIAL IMPLICATIONS

Nil.

RISK

There is a reputational risk with the DLGSC should the CAR not be completed on time or if significant non compliances are reported.

The likelihood of this occurring is rare.

STRATEGIC ASPIRATIONS

Performance - We will deliver excellent governance, service & value for everyone.

Outcome 11 - Effective leadership, advocacy and governance

Objective 11.2 Deliver best practice governance and risk management.

VOTING REQUIREMENTS

|

That the Audit and Risk Committee recommends that Council: 1. Accepts the attached 2024 Compliance Audit Return as contained in Attachment 1. 2. Authorises the Shire President and the Chief Executive Officer to certify the 2024 Compliance Audit Return in Attachment 1 and provide to the Department of Local Government Sport and Cultural Industries by 31 March 2025. |

|

2024 Compliance Audit Return |

Agenda – Audit and Risk Committee Meeting 18 February 2025 Page 1 of 4

|

SUMMARY: The Audit and Risk Committee is requested to consider results of the 2nd Quarter Finance and Costing Review (FACR) of the Shire’s budget for the period ended 31 December 2024, including forecast estimates and budget recommendations to 30 June 2025. |

Previous Considerations

SMC 22 August 2024 Item 5.4.1

ARC 29 October 2024 Item 5.1

OMC 31 October 2024 Item 13.1

1st Quarter Finance and Costing Review

The 1st Quarter Finance and Costing Review (the Q1 Review) was approved by Council at the OMC 31 October 2024. The Q1 Review contained a comprehensive list of budget amendments with the following proposed amendments of note:

· BRAC Importance Level 4 Upgrades Project (expense)

1. An additional $100,000 in municipal funds is required due to an increased scope of work identified during project preparations. The original project budget consists of $110,000 in grant funding and $110,000 in municipal funding. No further funding is confirmed at this stage. If the additional municipal funds are not provided, the grant funding will need to be returned, and the project will not proceed.

· Accounting Support (expense)

2. An additional $81,600 is requested to engage contractors for the preparation of the 2025/26 annual budget and to review Council’s Long Term Financial Plan. Contractor support is required due to the long term vacancy in the Accountant position necessitating external support to ensure these statutory projects are completed.

· Insurance (saving)

3. Actual annual insurance costs are $93,984 lower than budgeted. Additionally, there is a $27,000 insurance reimbursement for LGIS wage adjustments for 2023/24.

· Planning and Building Fee Income (saving)

4. Additional income of $70,000 is projected above budget, with income tracking ahead across both areas. This increase stems largely from increased solar applications.

· Main Roads Direct Grant (saving)

5. Actual grant was confirmed to be $34,110 more than the budget estimate.

· Property Reactive Maintenance (expense)

6. An amount of $40,000 is required for unplanned maintenance across the Administration building and two commercial properties.

· Implementation of the Animal Management Plan (expense)

7. The Animal Management Plan was adopted at the Ordinary Council Meeting on 19 September 2024. Council Resolution Point 3 requested the allocation of $50,000 through Quarter 1 FACR to cover costs for implementing actions in the plan.

Since the adoption of the 2024/25 annual budget, Council has approved the following budget amendments independent of the FACR process:

OMC 29 August 2024 Item 9.2.1 – Broome Housing Affordability Strategy And Master Planning

The net impact on municipal funds for 2024/25 is $0, as the budget amendments offset each other ($98,428 in income and $98,428 in expenditure). An agenda item was presented to the full Council, outside of the FACR process, to facilitate the proposed project. Council resolved the following:

|

Council Resolution: (Report Recommendation) Minute No. C/0824/001 Moved: Cr E Smith Seconded: Cr S Cooper That Council: 1. Notes the successful outcome of application – Housing Support Program Stream 1 (Attachment 1); 2. Endorses the proposed scope of works to develop a Broome Housing Affordability Strategy, in addition to offering concept master planning to help stimulate the development of undeveloped and underdeveloped land across the townsite of Broome; and a) Increase expenditure account 1367460 to $98,428; and b) Increase budget account 1367304 by $98,428.

For: Shire President C Mitchell, Cr. D Male, Cr. S Cooper, Cr. J Lewis, Cr. P Matsumoto, Cr. M Virgo, Cr. P Taylor, Cr. E Smith, Cr. J Mamid.

CARRIED UNANIMOUSLY BY ABSOLUTE MAJORITY 9/0 |

OMC 29 August 2024 Item 9.2.3 – Walmanyjun Cable Beach Foreshore Redevelopment - Waterpark Design Services (Stage3)

The net impact on municipal funds for 2024/25 is $0, as the budget amendments offset each other ($350,000 in income and $350,000 in expenditure). An agenda item was presented to the full Council, outside of the FACR process, to facilitate the proposed project. Council resolved the following:

|

Council Resolution: (Report Recommendation) Minute No. C/0824/002 Moved: Cr D Male Seconded: Cr P Taylor That Council adopt the following budget amendments to the 2024/25 Annual Budget for the detailed design of Stage 3 (Waterpark) of the Walmanyjun Cable Beach Foreshore redevelopment Project, noting a nil impact on municipal funds: 1. Increase expenditure account WD02 to $350,000: and 2. Increase grant income account WD01 of $350,000. For: Shire President C Mitchell, Cr. D Male, Cr. S Cooper, Cr. J Lewis, Cr. P Matsumoto, Cr. M Virgo, Cr. P Taylor, Cr. J Mamid. CARRIED UNANIMOUSLY BY ABSOLUTE MAJORITY 9/0 |

OMC 19 September 2024 Item 9.4.3 – Monthly Financial Report - August 2024

The net impact on municipal funds in 2024/25 is $0, as the budget amendments offset each other ($26,500 income and $26,500 expenditure). An agenda item was presented to full Council, outside of the FACR process, given the critical timing of the Community Development Fund program. Council resolved the following:

|

Council Resolution: (Report Recommendation) Minute No. C/0924/003 Moved: Cr J Lewis Seconded: Cr E Smith That Council: 1. Receives the Monthly Financial Report for the period ended 31 August 2024 as attached; and 2. Approves the following 2024/25 budget amendments to implement Council's previous resolution, Minute No. C/0624/066, regarding the allocation of the 2024/25 Community Development Fund program and Energy Development Limited grant funding: a. Budget increase of $26,500 for Account 100235930 Transfer from EDL Sponsorship Reserve; b. Budget increase of $26,500 for Account 100221730 EDL Sponsorship Programme; c. Budget increase of $19,500 for Account 100221720 Community Development Fund Stream 1 and Quick Response Grants; and d. Budget decrease of $19,500 for Account 100221740 Community Development Fund Stream 2 and 3. For: Shire President C Mitchell, Cr. D Male, Cr. S Cooper, Cr. J Lewis, Cr. P Matsumoto, Cr. M Virgo, Cr. P Taylor, Cr. E Smith, Cr. J Mamid. CARRIED UNANIMOUSLY BY ABSOLUTE MAJORITY 9/0 |

The net result of the Quarter 1 FACR estimates is a budget deficit position of $122,617 to 30 June 2025. Budget amendments previously endorsed by Council have had no municipal impact.

This net result includes $84,560 of additional expenditure requirements across directorates, and $38,057 of additional organisational expenditure.

Quarter 2 Finance and Costing Review

The Shire of Broome has carried out its 2nd Quarter Finance and Costing Review (FACR) for the 2023/24 financial year. This review of the 2023/24 adopted Annual Budget is based on actuals and commitments for the first six months of the year from 1 July 2023 to 31 December 2023, and forecasts for the remainder of the financial year.

This process aims to highlight over and under expenditure of funds and over and under achievement of income targets for the benefit of Executive and Responsible Officers to ensure good fiscal management of their projects and programs.

Once this process is completed, a report is compiled identifying budgets requiring amendments to be adopted by Council. Additionally, a summary provides the financial impact of all proposed budget amendments to the Shire of Broome’s adopted end-of-year forecast, to assist Council to make an informed decision.

It should be noted that the 2023/24 Annual Budget was adopted at the Special Meeting of Council (SMC) on 11 July 2023 as a balanced budget.

COMMENT

Council Approved budget amendments

The following budget amendments have been approved by Council since the 1st Quarter FACR:

OMC December 12 2024 Item 14.1 Request for Tender RFT24-09 Frederick Street Intersection

The net impact on municipal funds in 2024/25 is $0, as the budget amendments offset each other ($112,500 income and $112,500 expenditure). An agenda item was presented to full Council, outside of the FACR process, given the critical timing of the tender. Council resolved the following:

OMC December 12 2024 Item 14.2 Request for Tender RFT24-08 Contaminated Site Remediation – Reserve 42502

The net impact on municipal funds in 2024/25 is $0, as the budget amendments offset each other ($1,800,000 income, $1,046,000 expenditure and $754,000 transfer to reserve). An agenda item was presented to full Council, outside of the FACR process, given the critical timing of the tender. Council resolved the following:

|

Council Resolution: (Report Recommendation) Minute No. C/1224/024 Moved: Cr J Mamid Seconded: Cr P Matsumoto That Council: 1. Note the recommendation outlined in the Evaluation Report for RFT 24/08 Contaminated Site Remediation Reserve 42502 as presented in Attachment 2; 2. Accepts the Tender from Site Environmental and Remediation Services Pty Ltd as the most advantageous Respondent from which to form a Contract, subject to final contract negotiations for RFT 24/08, with a maximum value of $1,196,000 Ex GST. 3. Authorises the Chief Executive Officer to finalise and sign the contract following negotiations and financial due diligence, and to negotiate contract variations during the project; 4. If a Contract cannot be executed, authorises negotiations to commence with the second preferred Respondent. 5. Approve a budget amendment of $1,046,000 Ex GST to Expense Account 101010500 for the delivery of RFT 24/08 Contaminated Site Remediation Reserve 42502. 6. Approve a budget amendment of $1,800,000 Ex GST to Income Account 101014200 WMF Op Income – Sanitation Gen Refuse Mun. 7. Approve a budget amendment to transfer $754,000 Ex GST to Account 101018950 Transfer to Regional Resource Recovery Park Reserve. 8. Requests the Chief Executive Officer to update the Landfill Closure Management Plan and provide an update on the costings for inclusion in the financial modelling for the Refuse Reserve and Regional Resource Recovery Park Reserve. For: Shire President C Mitchell, Cr D Male, Cr S Cooper, Cr J Mamid, Cr P Matsumoto, Cr E Smith, Cr M Virgo. CARRIED UNANIMOUSLY BY ABSOLUTE MAJORITY 7/0 |

Quarter 2 Finance and Costing Review

Responsible officers completed the second quarter review in January 2025. The executive team thoroughly reviewed and considered the budget requests, carefully weighing the impacts on service levels and potential delays to projects, against the overall annual budget.

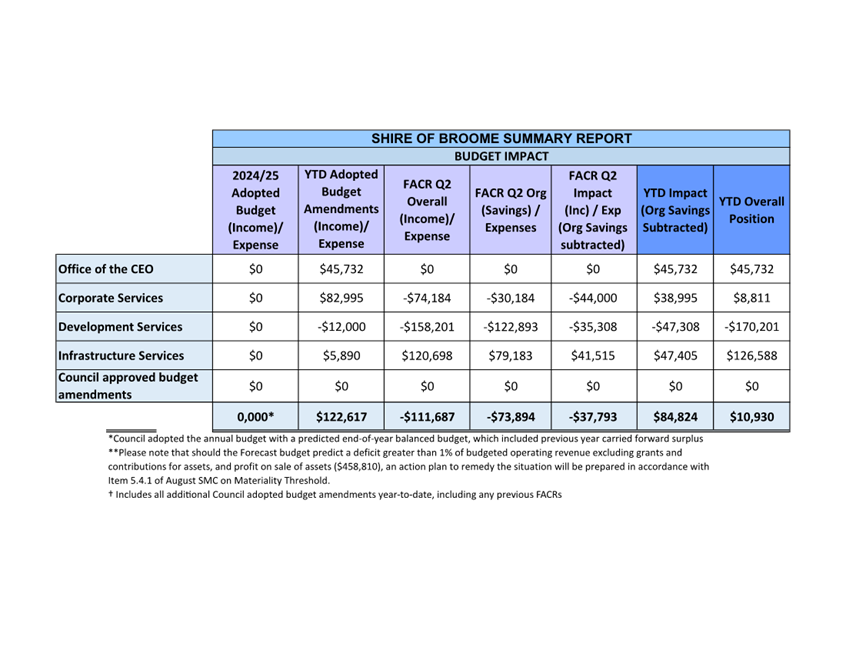

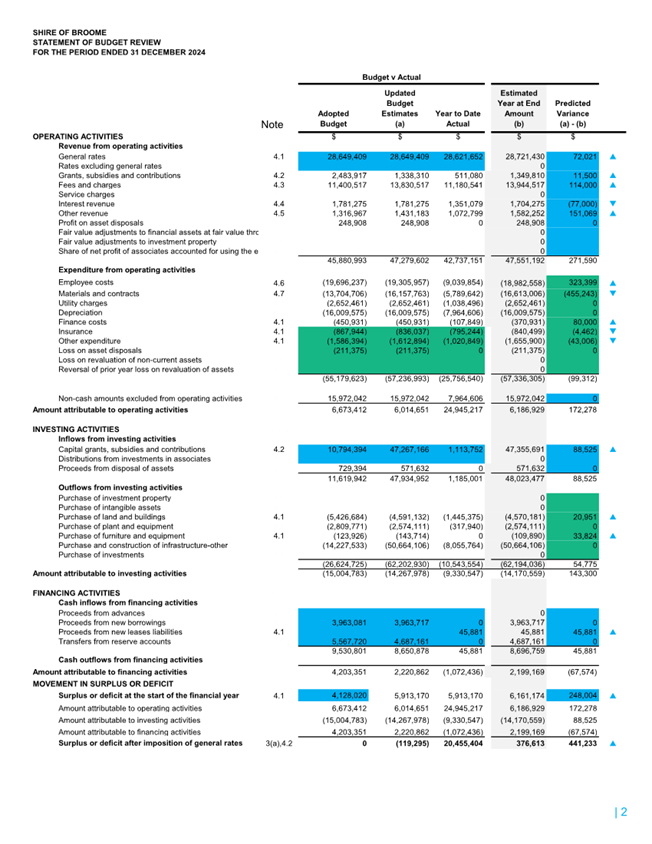

The Quarter 2 FACR results indicate a deficit forecast financial position of $10,930 should Council approve the Quarter 2 proposed budget amendments. This figure represents a budget forecast should all expenditure and income occur as expected.

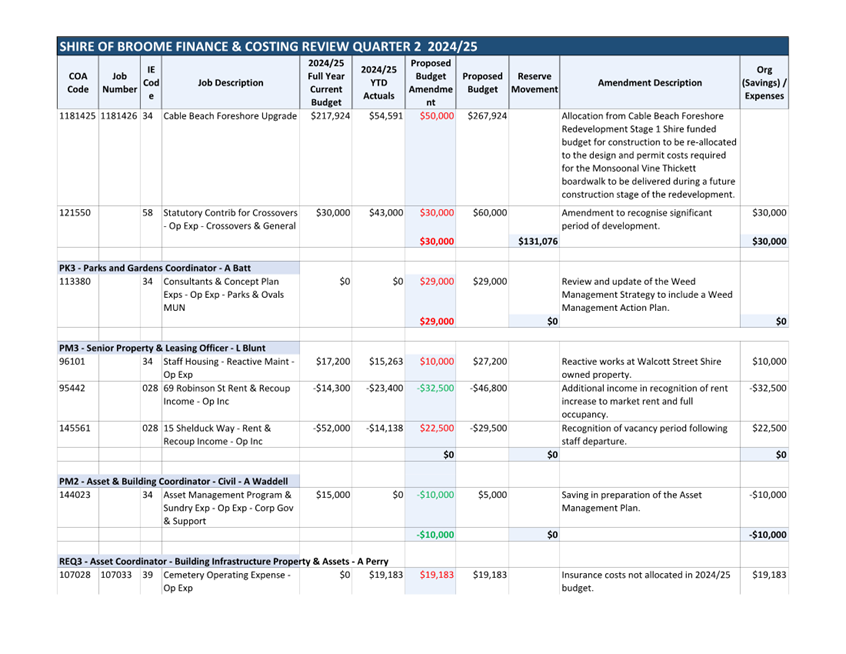

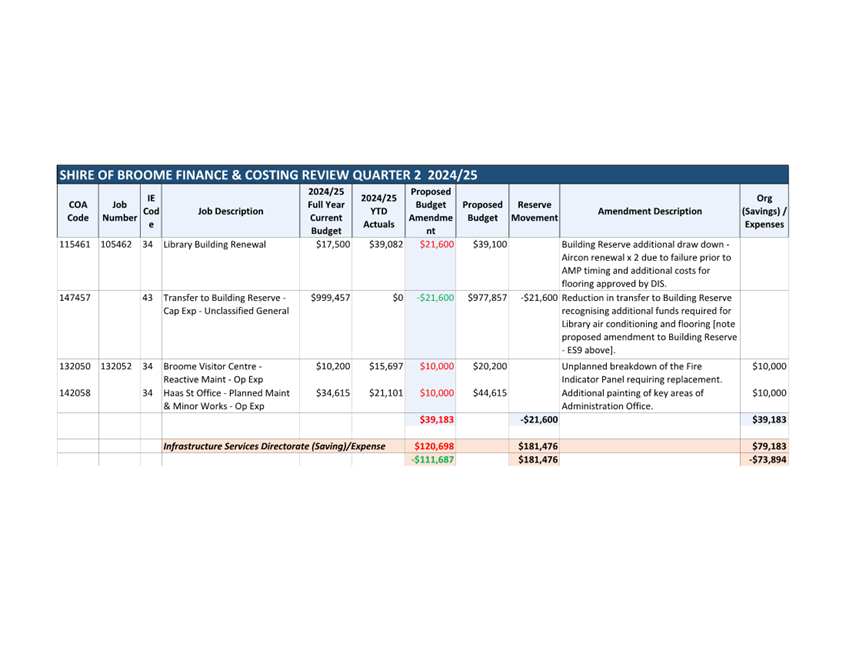

While officers make every effort to ensure the net impact of each FACR is minimal, and offset savings and expenditure within their assigned budgets and directorates, this is not always achievable. The second quarter review has balanced the impact of the proposed variances within the full budget, including the following proposed amendments:

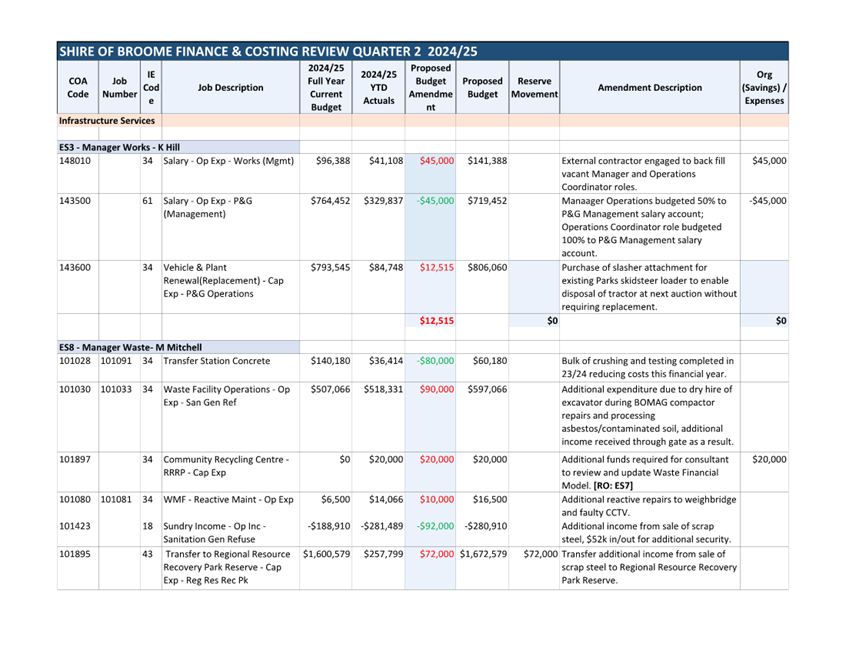

· $172,000 additional income at the Waste Management Facility offset by a $100,000 increase in costs (primarily related to dry hire excavator costs required due to BOMAG repairs) resulting in a $72,000 transfer to the Regional Resource Recovery Park Reserve.

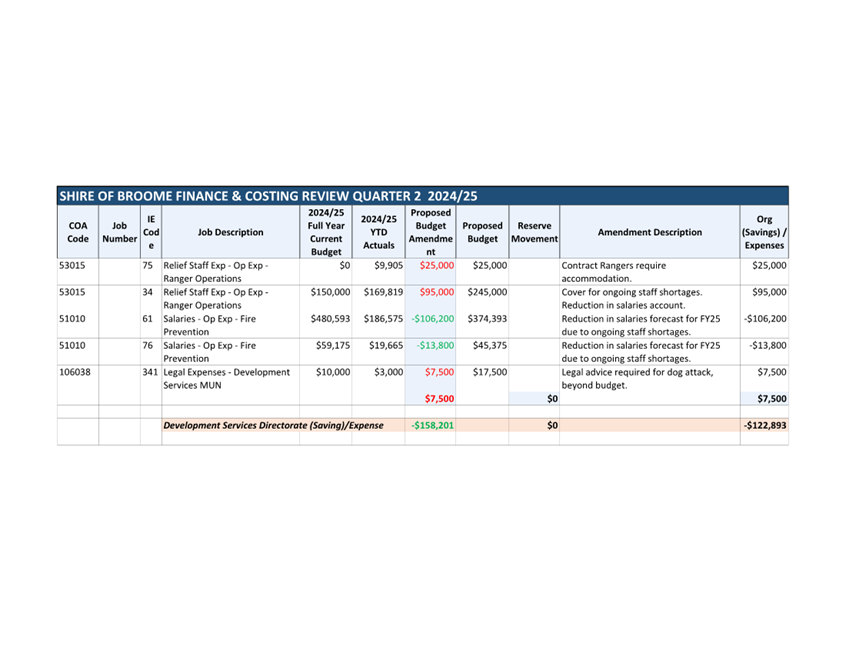

· $120,000 decrease to salary accounts in the Ranger Operations business unit with a corresponding $120,000 increase to fund relief staff required due to vacancies.

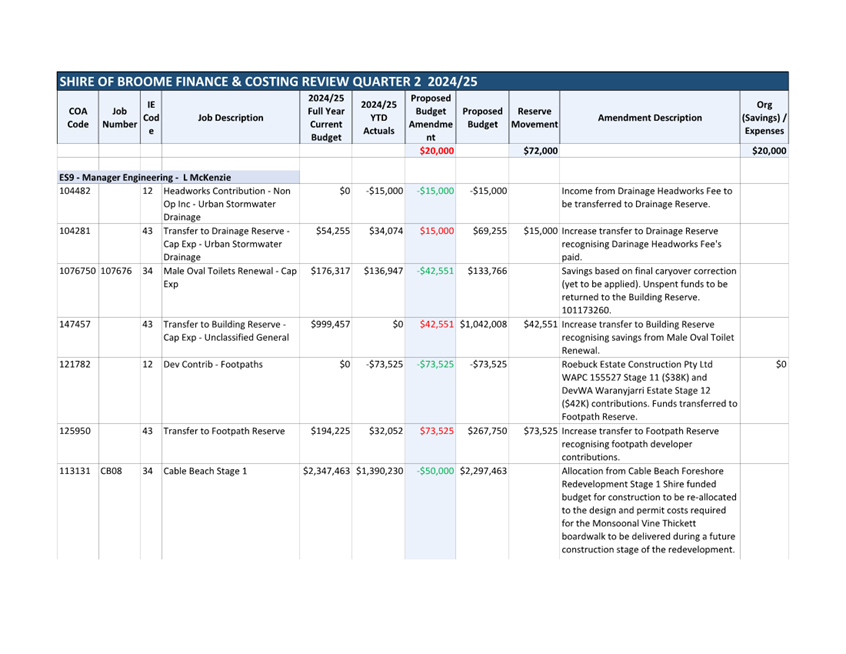

· $88,525 increased income via developer contributions which have been quarantined in reserve for future footpath and drainage works.

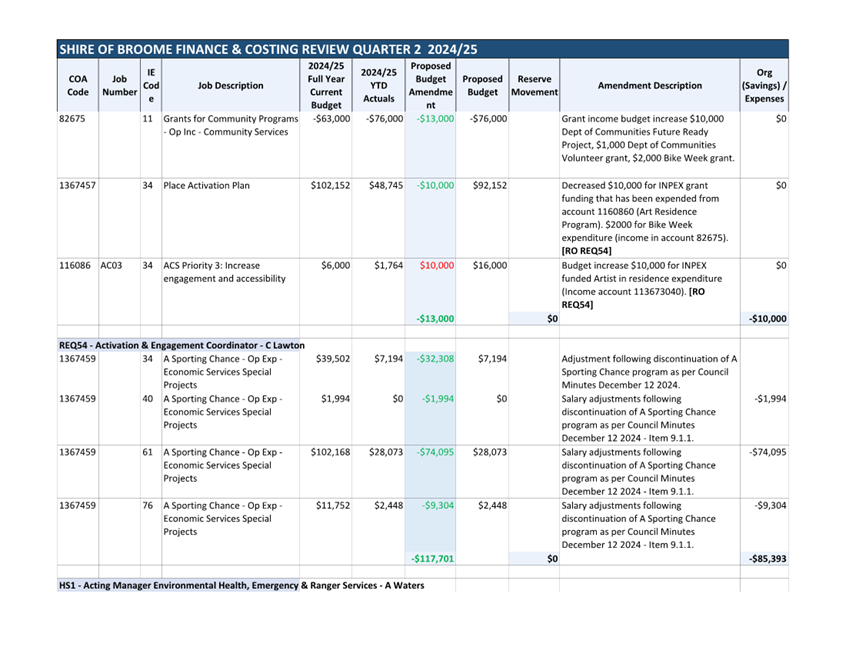

· $85,393 savings in salary allocations for A Sporting Chance due to the program being wound up (refer December 12 2024 OMC Item 9.1.1).

· $80,000 reduction in loan fees and adjustments due to the delayed draw down of the Key Worker Housing Loan.

· $77,000 loss of interest income due to the delayed issue of rates notices following late budget adoption coupled with less grant funding being held in the municipal bank account.

· $60,000 decrease to salary accounts in the Finance business unit with a corresponding $77,021 increase to fund relief staff and external financial support due to vacancies in key positions. Pleasingly the Manager Finance position has recently been filled with recruitment continuing for the Accountant role.

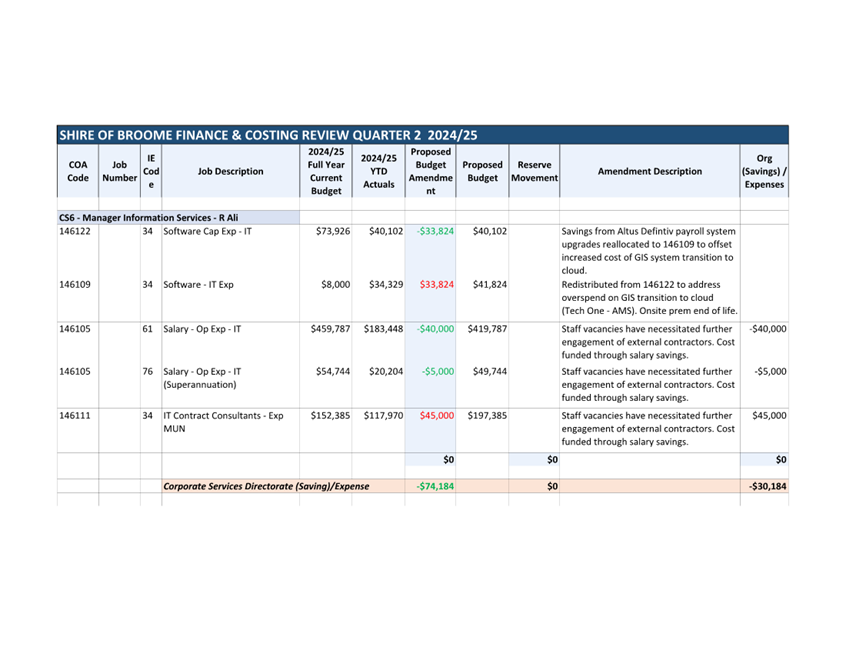

· $45,000 decrease to salary accounts in the Information Services business unit with a corresponding $45,000 increase to fund external ICT support required due to vacancies in key positions.

· $45,000 decrease to salary accounts in the Works business unit with a corresponding $45,000 increase to fund relief staff required due to vacancies in key positions.

· $42,551 in savings following the completion of the Male Oval Toilet Renewals with the savings returned to reserve.

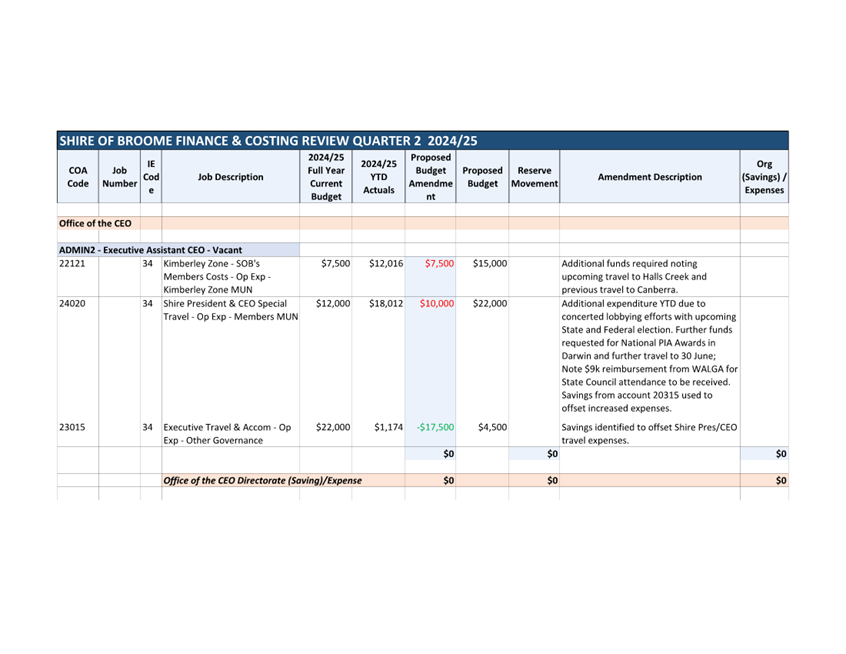

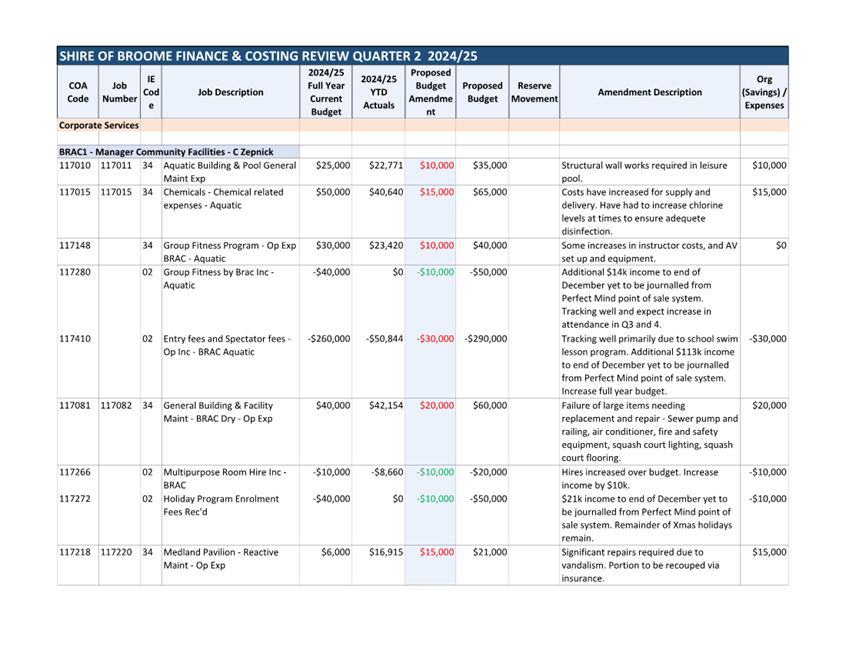

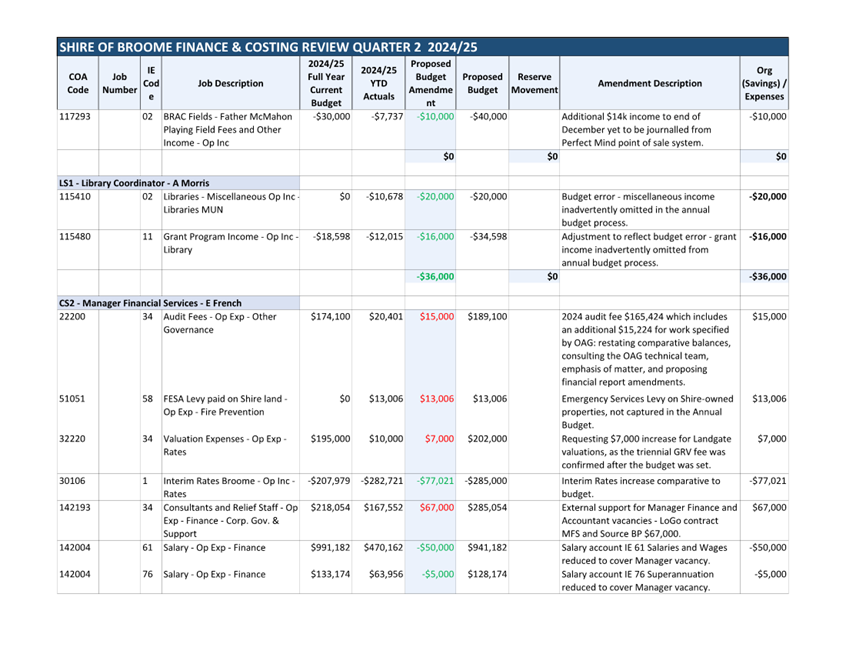

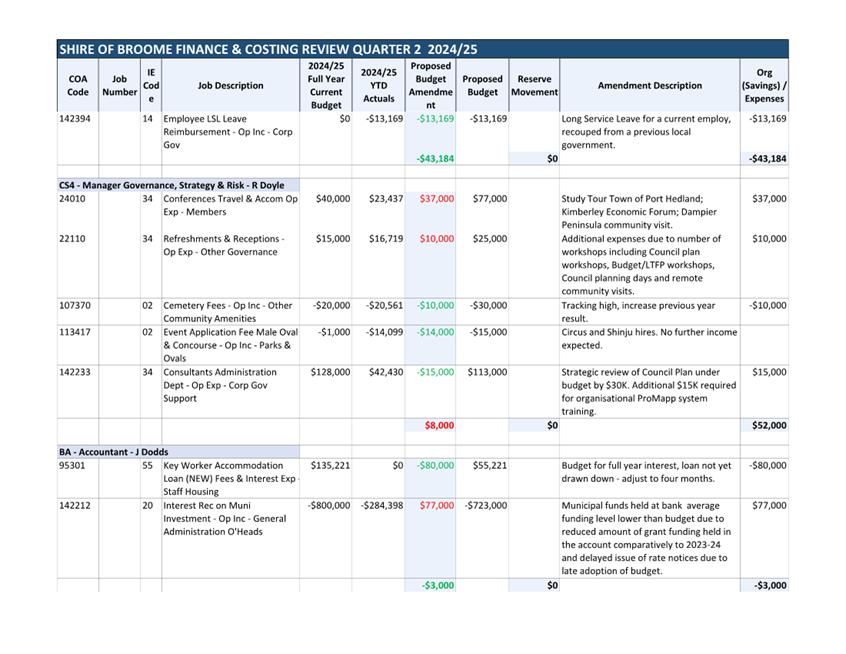

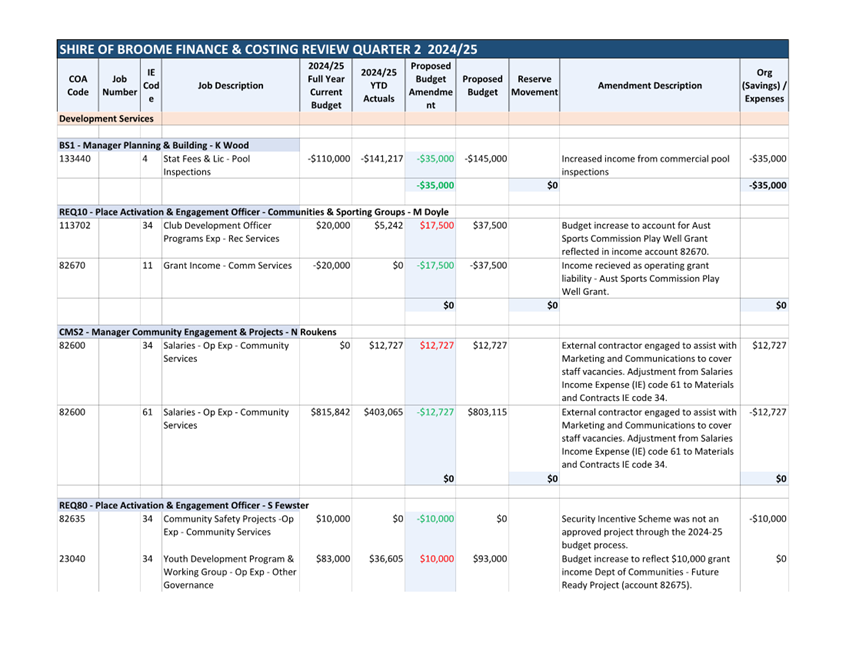

A comprehensive list of accounts has been included for perusal by the committee, presented by Directorate (refer to Attachment 1).

A summary of the results is as follows:

|

SHIRE OF BROOME SUMMARY REPORT |

|||||||||

|

BUDGET IMPACT |

|||||||||

|

2024/25 Adopted Budget |

YTD Adopted Budget

Amends. |

FACR Q2 Overall |

FACR Q2 Org (Saving) / Expense |

FACR Q2 Impact |

YTD Impact |

YTD Overall Position |

|||

|

Office of the CEO |

$0 |

$45,732 |

$0 |

$0 |

$0 |

$45,732 |

$45,732 |

||

|

Corporate Services |

$0 |

$82,995 |

-$74,184 |

-$30,184 |

-$44,000 |

$38,995 |

$8,811 |

||

|

Development Services |

$0 |

-$12,000 |

-$158,201 |

-$122,893 |

-$35,308 |

-$47,308 |

-$170,201 |

||

|

Infrastructure Services |

$0 |

$5,890 |

$120,698 |

$79,183 |

$41,515 |

$47,405 |

$126,588 |

||

|

Council budget amends. |

$0 |

$0 |

$0 |

$0 |

$0 |

$0 |

$0 |

||

|

|

|

0,000* |

$122,617 |

-$111,687 |

-$73,894 |

-$37,793 |

$84,824 |

$10,930 |

|

*Council adopted the annual budget with a predicted end-of-year balanced budget.

CONSULTATION

All amendments have been proposed after consultation with Executive and Responsible Officers at the Shire.

STATUTORY ENVIRONMENT

Local Government (Financial Management) Regulation 1996

r33A. Review of Budget

(1) Between 1 January and the last day of February in each financial year a local government is to carry out a review of its annual budget for that year.

(2A) The review of an annual budget for a financial year must —

(a) consider the local government’s financial performance in the period beginning on 1 July and ending no earlier than 31 December in that financial year; and

(b) consider the local government’s financial position as at the date of the review; and

(c) review the outcomes for the end of that financial year that are forecast in the budget; and

(d) include the following —

(i) the annual budget adopted by the local government;

(ii) an update of each of the estimates included in the annual budget;

(iii) the actual amounts of expenditure, revenue and income as at the date of the review;

(iv) adjacent to each item in the annual budget adopted by the local government that states an amount, the estimated end‑of‑year amount for the item.

(2) The review of an annual budget for a financial year must be submitted to the council on or before 31 March in that financial year.

(3) A council is to consider a review submitted to it and is to determine* whether or not to adopt the review, any parts of the review or any recommendations made in the review.

*Absolute majority required.

(4) Within 14 days after a council has made a determination, a copy of the review and determination is to be provided to the Department.

[Regulation 33A inserted: Gazette 31 Mar 2005 p. 1048‑9; amended: Gazette 20 Jun 2008 p. 2723-4; SL 2023/106 r. 18.]

Local Government Act 1995

6.8. Expenditure from municipal fund not included in annual budget

1) A local government is not to incur expenditure from its municipal fund for an additional purpose except where the expenditure —

(a) is incurred in a financial year before the adoption of the annual budget by the local government;

(b) is authorised in advance by resolution*; or

(c) is authorised in advance by the mayor or president in an emergency.

(1a) In subsection (1) —

“additional purpose” means a purpose for which no expenditure estimate is included in the local government’s annual budget.

POLICY IMPLICATIONS

Nil.

It should be noted that according to the materiality threshold set at the budget adoption, should a deficit achieve 1% of Shire’s operating revenue ($441,595) the Shire must formulate an action plan to remedy the over expenditure.

FINANCIAL IMPLICATIONS

The net result of budget amendments previously endorsed by Council (including Quarter 1 FACR) is a budget deficit position of $122,617.

The net result of budget amendments proposed through the Quarter 2 FACR will result in a $111,687 surplus.

Council’s approval of the Quarter 2 FACR will result in an overall closing position deficit of $10,930 to 30 June 2025. This figure represents a budget forecast should all expenditure and income occur as expected.

RISK

The Finance and Costing Review (FACR) seeks to provide a best estimate of the end-of-year position for the Shire of Broome at 30 June 2025. Contained within the report are recommendations of amendments to budgets which have financial implications on the estimate of the end-of-year position.

The review does not, however, seek to make amendments below the materiality threshold unless strictly necessary. The materiality thresholds are set at $10,000 for operating budgets and $20,000 for capital budgets. Should a number of accounts exceed their budget within these thresholds, it poses a risk that the predicted final end-of-year position may be understated.

In order to mitigate this risk, the CEO enacted the FACRs to run quarterly and Executive examine each job and account to ensure compliance. In addition, the monthly report provides variance reporting highlighting any discrepancies against budget.

It should also be noted that should Council decide not to adopt the recommendations, it could lead to some initiatives being delayed or cancelled in order to offset the additional expenditure associated with running the Shire’s operations.

STRATEGIC ASPIRATIONS

Performance – We will deliver excellent governance, service and value, for everyone.

Outcome Eleven – Effective leadership, advocacy and governance:

11.2 Deliver best practice governance and risk management.

Outcome Thirteen - Value for money from rates and long term financial sustainability:

13.1 Plan effectively for short and long term financial sustainability.

VOTING REQUIREMENTS

|

That the Audit and Risk Committee recommends that Council: 1. Receives the Quarter 2 Finance and Costing Review Report for the period ended 31 December 2024; 2. Adopts the operating and capital budget amendment recommendations for the year ended 30 June 2025 as attached (Attachment 1); 3. Notes a forecast net end-of-year deficit position to 30 June 2025 of $10,930 including previously adopted budget amendments; and 4. Endorses the Report as the 2024/25 statutory mid-year budget review. |

|

Quarter 2 Finance and Costing Review 2024-25 |

|

|

2024-25 Mid-year Statement of Budget Review |

Agenda – Audit and Risk Committee Meeting 18 February 2025 Page 1 of 4

|

These minutes were confirmed at a meeting held (DD Month Year), and signed below by the Presiding Person, at the meeting these minutes were confirmed.

Signed: ……………………………

|