MINUTES

OF THE

Audit and Risk Committee Meeting

8 April 2025

|

These minutes were confirmed at a meeting held and signed below by the Presiding Person, at the meeting these minutes were confirmed.

|

MINUTES

OF THE

Audit and Risk Committee Meeting

8 April 2025

|

These minutes were confirmed at a meeting held and signed below by the Presiding Person, at the meeting these minutes were confirmed.

|

Minutes – Audit and Risk Committee Meeting 8 April 2025 Page 1 of 3

SHIRE OF BROOME

Audit and Risk Committee Meeting

Tuesday 8 April 2025

INDEX – Minutes

3. Declarations Of Financial Interest / Impartiality

5.1 3RD QUARTER FINANCE AND COSTING REVIEW 2024-25

5.2 AUDIT FINDINGS PROGRESS UPDATE

6. Matters Behind Closed Doors

MINUTES OF THE Audit and Risk Committee Meeting OF THE SHIRE OF BROOME,

HELD IN THE Council Chambers, Corner Weld and Haas Streets, Broome, ON Tuesday 8 April 2025, COMMENCING AT 10:00AM.

The Chair welcomed elected members and officers and declared the meeting open at 10:08 AM

|

ATTENDANCE |

|

|

|

|

|

|

|

|

|

Members: |

Cr D Male |

Chair, Deputy Shire President |

|

|

|

Shire President C Mitchell |

Shire President |

|

|

|

Cr M Virgo |

|

|

|

|

|

||

|

Apologies: |

Nil |

|

|

|

|

|

|

|

|

|

|

||

|

Leave of Absence: |

Nil |

|

|

|

|

|

|

|

|

|

|

||

|

Officers: |

Mr S Mastrolembo |

Chief Executive Officer |

|

|

|

Mr J Watt |

Director Corporate Services |

|

|

|

Mr J Hall |

Director Infrastructure |

|

|

|

Ms S Becker |

Director Development and Community |

|

|

|

Mr F Mammone |

Manager Financial Services |

|

|

|

Ms K Small |

Finance Contractor |

|

|

|

Ms E Kerr |

Finance Officer |

|

|

|

|

|

|

|

|

|

||

|

Committee Member |

Item No |

Item |

Nature of Interest |

|

Nil. |

|||

|

Minute No. AR/0425/001 Moved: Shire President C Mitchell Seconded: Cr M Virgo That the Minutes of the Audit and Risk Committee held on 18 February 2025, as published and circulated, be confirmed as a true and accurate record of that meeting. |

|

SUMMARY: The Audit and Risk Committee is requested to consider results of the 3rd Quarter Finance and Costing Review (FACR) of the Shire’s budget for the period ended 31 March 2025, including forecast estimates and budget recommendations to 30 June 2025. |

Previous Considerations

SMC 22 August 2024 Item 5.4.1

ARC 29 October 2024 Item 5.1

OMC 31 October 2024 Item 13.1

ARC 18 February 2025 Item 5.2

OMC 27 February 2025 Item 9.4.6

The Shire of Broome has carried out its 3rd Quarter Finance and Costing Review (FACR) for the 2024-25 financial year. This review of the 2024-25 Annual Budget is based on actuals and commitments for the first 9 months of the year from 1 July 2024 to 31 March 2025, and forecasts for the remainder of the financial year.

This process aims to highlight over and under expenditure of funds, and over and under achievement of income targets for the benefit of Executive and Responsible Officers to ensure good fiscal management of their projects and programs.

Once this process is completed, a report is compiled identifying budgets requiring amendments to be adopted by Council. Additionally, a summary provides the financial impact of all proposed budget amendments to the Shire of Broome’s adopted end-of-year forecast, to assist Council to make an informed decision.

It should be noted that the 2024-25 annual budget was adopted at the Special Meeting of Council on 22 August 2024 as a balanced budget.

The Quarter 3 FACR commenced on 20 March 2025. At the start of the Q3 FACR, a net deficit of $87,619 was forecast arising from past budget amendments adopted by Council, including the Quarter 1 and Quarter 2 FACR’s, and amendments stemming from Council’s adoption of the Final 2024 Audit in December 2024. These amendments resulted in an adjusted opening deficit of $87,619.

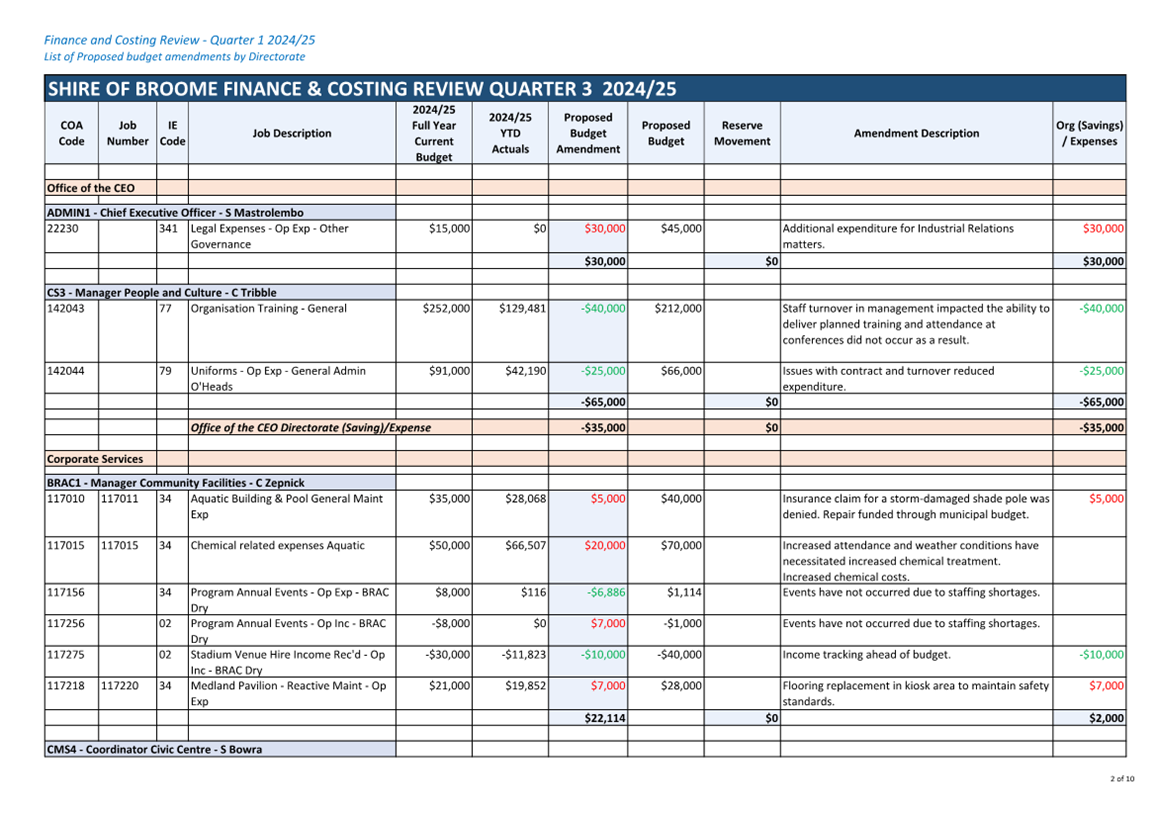

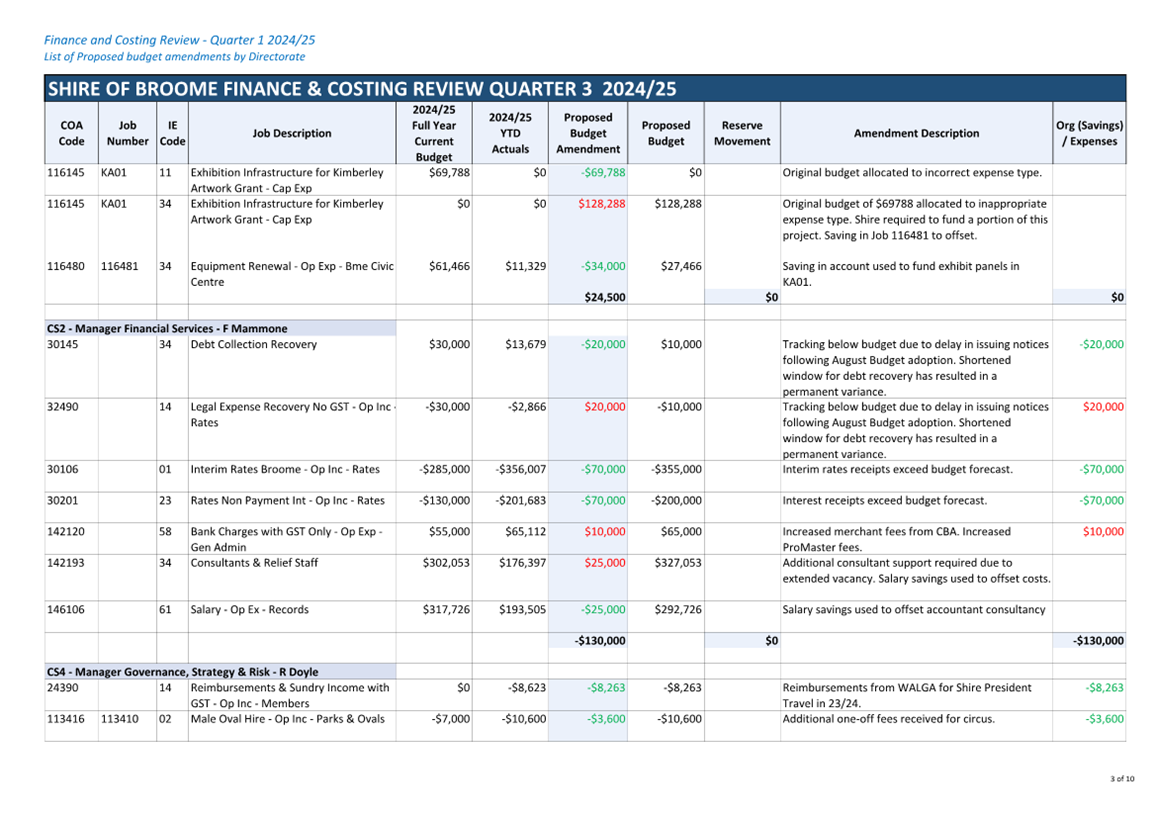

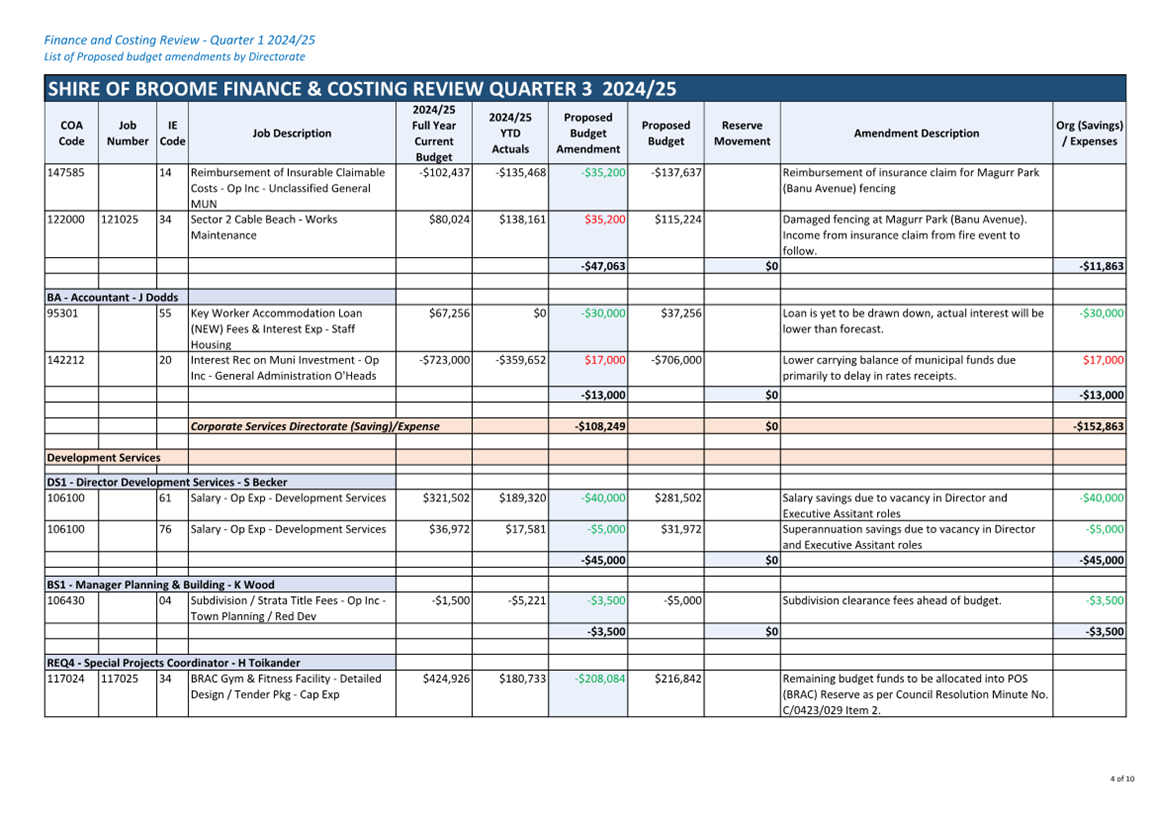

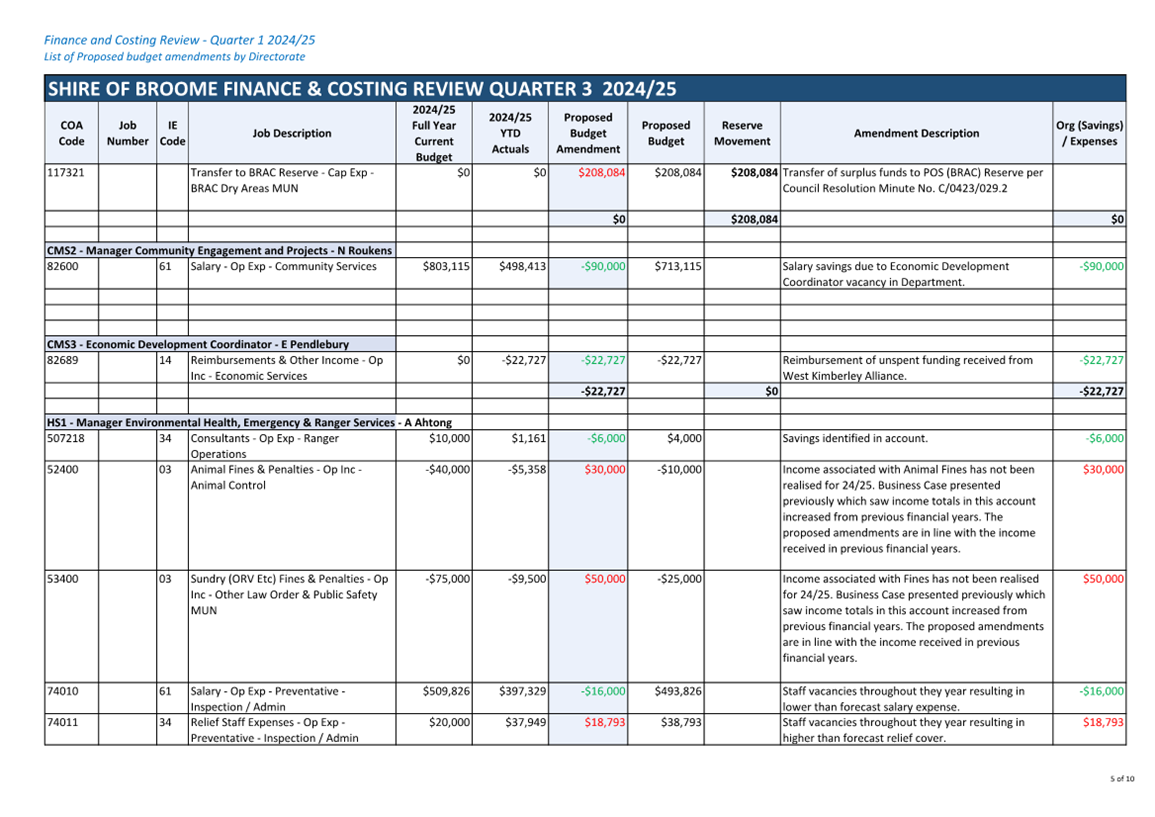

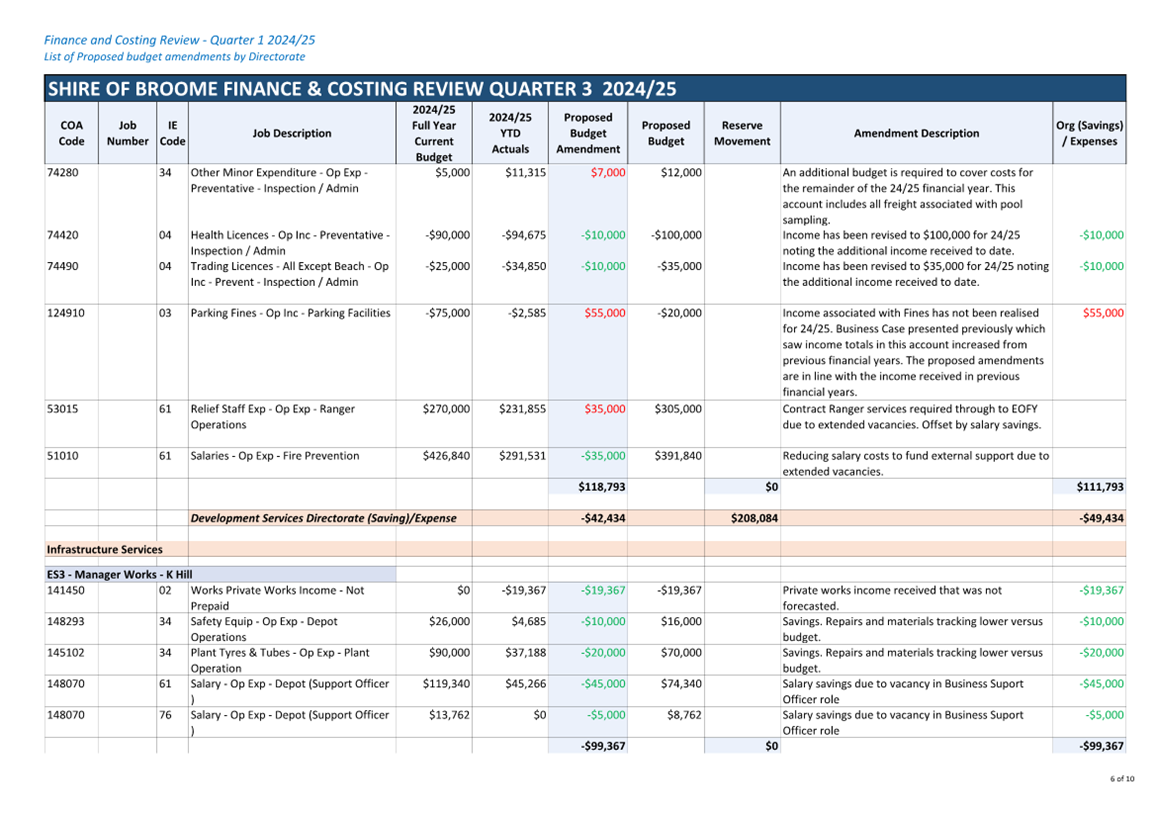

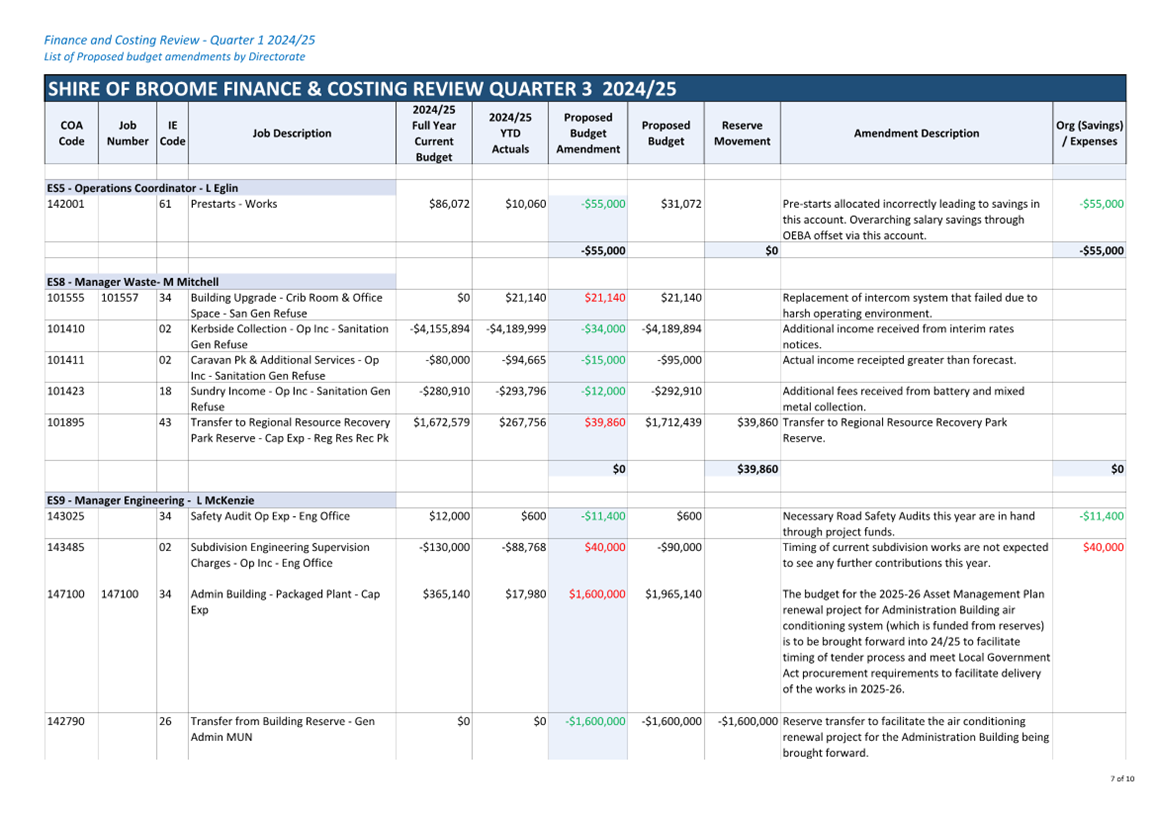

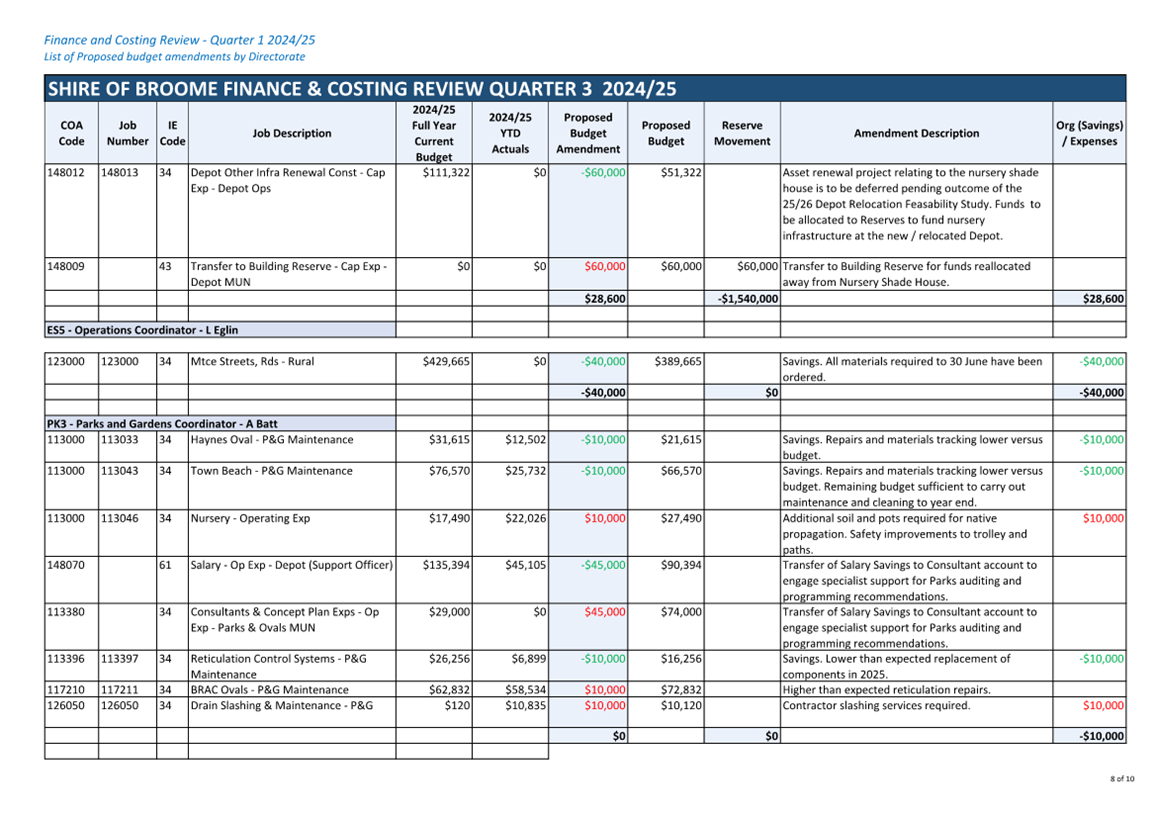

Significant amendments approved through the FACR processes to date include:

· $172,000 additional income at the Waste Management Facility offset by a $100,000 increase in costs (primarily related to dry hire excavator costs required due to BOMAG repairs) resulting in a $72,000 transfer to the Regional Resource Recovery Park Reserve.

· $120,000 decrease to salary accounts in the Ranger Operations business unit with a corresponding $120,000 increase to fund relief staff required due to vacancies.

· $93,984 reduction in insurance costs as the actual premiums received were lower than forecast.

· $88,525 increased income via developer contributions which have been quarantined in reserve for future footpath and drainage works.

· $85,393 savings in salary allocations for A Sporting Chance due to the program being wound up (refer December 12 2024 OMC Item 9.1.1).

· $81,600 increase in expense to engage contractors for the preparation of the 2025/26 annual budget and to review Council’s Long Term Financial Plan.

· $80,000 reduction in loan fees and adjustments due to the delayed draw down of the Key Worker Housing Loan.

· $77,000 loss of interest income due to the delayed issue of rates notices following late budget adoption coupled with less grant funding being held in the municipal bank account.

· $70,000 additional income from planning and building fees. This increase stems largely from increased solar applications.

COMMENT

The Q3 FACR identifies a net cumulative deficit forecast of $193,282 to 30 June 2025.

The above figure represents a budget forecast should all expenditure and income occur as expected. It does not represent the actual end-of-year position which can only be determined as part of the normal annual financial processes at the end of the financial year.

While officers make every effort to ensure the net impact of each FACR is minimal, the net surplus forecast mainly relates to the following proposed amendments:

· A $235,000 reduction in forecast Salaries and Wages, reflecting vacancies in key positions throughout the organisation.

· A $140,000 combined increase in interest received on interim rates and non-payment of rates.

· a $135,000 reduction in forecast income from issue of infringement notices. Business case presented previously saw the budgeted figures increase on prior year actuals. The results in this financial year mirror prior years more closely than originally forecast.

While the forecast for the 2024/25 financial year shows a positive result, it's crucial to acknowledge that the surplus isn't due to inadequate planning or budgeting. Staff turnover and vacancies have affected service delivery, prompting officers to fill gaps with contractors and defer non-essential tasks. Despite challenges, officers have strived to meet community expectations with the available resources. They face a rigorous review in the third quarter, aiming for realistic outcomes on all accounts and projects. Recognising that operating budgets reset at the start of the new financial year, officers strive to optimise their fund allocations to achieve the best outcomes for the community by 30 June.

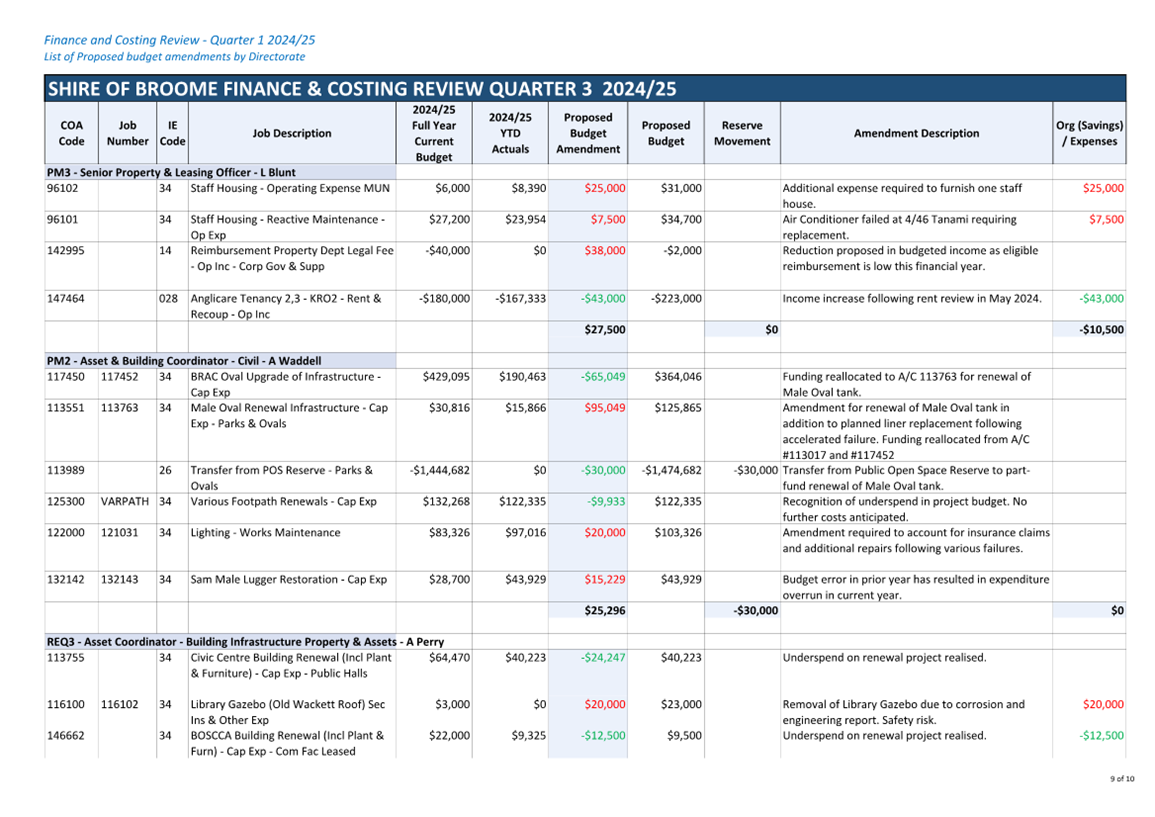

A comprehensive list of accounts (refer to Attachment 1) has been included for perusal by the committee, summarised by Directorate.

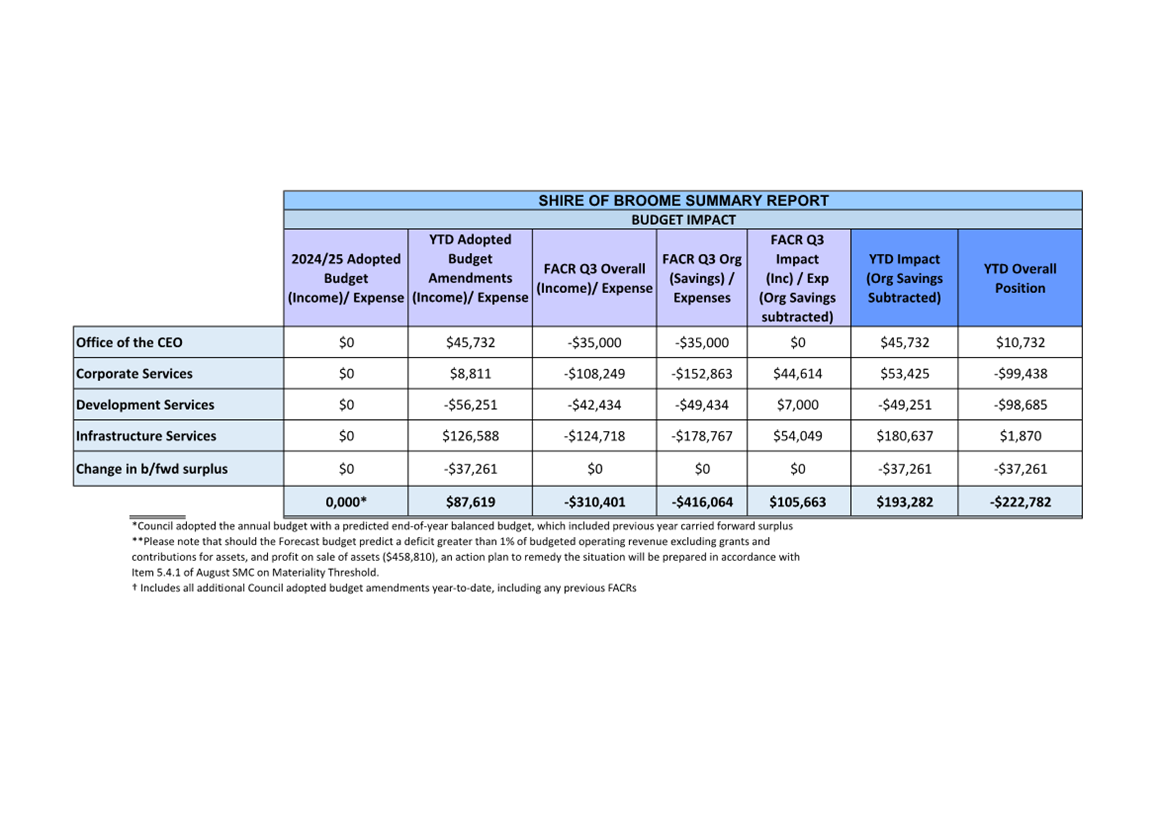

Quarter 3 FACR Result

A summary of the results is as follows:

|

|

SHIRE OF BROOME SUMMARY REPORT |

||||||||

|

BUDGET IMPACT |

|||||||||

|

2023/24 Adopted Budget (Income)/ Expense |

YTD

Adopted Budget Amendments |

FACR Q3 Overall (Income) / Expense |

FACR Q3 Org (Savings) / Expenses |

FACR Q3 Impact (Inc) / Exp (Org Savings subtracted) |

YTD Impact (Org Savings Subtracted) |

YTD Overall Position |

|||

|

Office of the CEO |

$0 |

$45,732 |

-$35,000 |

-$35,000 |

$0 |

$45,732 |

$10,732 |

||

|

Corporate Services |

$0 |

$8,811 |

-$108,249 |

-$152,863 |

$44,614 |

$53,425 |

-$99,438 |

||

|

Development Services |

$0 |

-$56,251 |

-$42,434 |

-$49,434 |

$7,000 |

-$49,251 |

-$98,685 |

||

|

Infrastructure Services |

$0 |

$126,588 |

-$124,718 |

-$178,767 |

$54,049 |

$180,637 |

$1,870 |

||

|

Change in brought forward surplus |

$0 |

-$37,261 |

$0 |

$0 |

$0 |

-$37,261 |

-$37,261 |

||

|

0,000* |

$87,619 |

-$310,401 |

-$416,064 |

$105,663 |

$193,282 |

-$222,782 |

|||

*Council adopted the annual budget with a predicted end-of-year balanced budget, which included previous year carried forward surplus.

CONSULTATION

All amendments have been proposed after consultation with Executive and Responsible Officers at the Shire.

STATUTORY ENVIRONMENT

Local Government (Financial Management) Regulation 1996

r33A. Review of Budget

(1) Between 1 January and the last day of February in each financial year a local government is to carry out a review of its annual budget for that year.

(2A) The review of an annual budget for a financial year must —

(a) consider the local government’s financial performance in the period beginning on 1 July and ending no earlier than 31 December in that financial year; and

(b) consider the local government’s financial position as at the date of the review; and

(c) review the outcomes for the end of that financial year that are forecast in the budget; and

(d) include the following —

(i) the annual budget adopted by the local government;

(ii) an update of each of the estimates included in the annual budget;

(iii) the actual amounts of expenditure, revenue and income as at the date of the review;

(iv) adjacent to each item in the annual budget adopted by the local government that states an amount, the estimated end‑of‑year amount for the item.

(2) The review of an annual budget for a financial year must be submitted to the council on or before 31 March in that financial year.

(3) A council is to consider a review submitted to it and is to determine* whether or not to adopt the review, any parts of the review or any recommendations made in the review.

*Absolute majority required.

(4) Within 14 days after a council has made a determination, a copy of the review and determination is to be provided to the Department.

[Regulation 33A inserted: Gazette 31 Mar 2005 p. 1048‑9; amended: Gazette 20 Jun 2008 p. 2723-4; SL 2023/106 r. 18.]

Local Government Act 1995

6.8. Expenditure from municipal fund not included in annual budget

1) A local government is not to incur expenditure from its municipal fund for an additional purpose except where the expenditure —

(a) is incurred in a financial year before the adoption of the annual budget by the local government;

(b) is authorised in advance by resolution*; or

(c) is authorised in advance by the mayor or president in an emergency.

(1a) In subsection (1) —

“additional purpose” means a purpose for which no expenditure estimate is included in the local government’s annual budget.

POLICY IMPLICATIONS

Nil.

It should be noted that according to the materiality threshold set at the budget adoption, should a deficit achieve 1% of Shire’s operating revenue ($458,810) the Shire must formulate an action plan to remedy the over expenditure.

FINANCIAL IMPLICATIONS

The overall result of the Quarter 3 FACR is a surplus of $310,401. Within this review process, officers identified $416,064 of organisational savings.

Taking the existing net deficit of $87,619 into consideration, being all budget amendments previously endorsed by Council, and the amendments proposed in the Quarter 3 FACR, the net result is a cumulative surplus forecast of $222,782. Organisational Savings of $416,064 have been identified which if approved would result in a net cumulative deficit forecast of $193,282 to 30 June 2025.

The decision to allocate the surplus, identified as "organisation savings," rests with Council. These savings are genuine organisation savings that can be allocated to other areas. Officers are comfortable that the forecast deficit position of $193,282 can be addressed prior to the end of the financial year.

It is recommended that organisational savings of $416,064 is used to reduce the $997,717 approved borrowing to fund Cable Beach Stage A1. This will reduce total borrowings to $581,653 and reduce annual loan repayments from a projected $126,314 to $73,639, providing ongoing savings and improving Council’s debt servicing ratio.

RISK

The Finance and Costing Review (FACR) seeks to provide a best estimate of the end-of-year position for the Shire of Broome at 30 June 2025. Contained within the report are recommendations of amendments to budgets which have financial implications on the estimate of the end-of-year position.

The review does not, however, seek to make amendments below the materiality threshold unless strictly necessary. The materiality thresholds are set at $10,000 for operating budgets and $20,000 for capital budgets. Should a number of accounts exceed their budget within these thresholds, it poses a risk that the predicted final end-of-year position may be understated.

In order to mitigate this risk, the CEO enacted the FACRs to run quarterly and Executive examine each job and account to ensure compliance. In addition, the monthly report provides variance reporting highlighting any discrepancies against budget.

It should also be noted that should Council decide not to adopt the recommendations, it could lead to some initiatives being delayed or cancelled in order to offset the additional expenditure associated with running the Shire’s operations.

STRATEGIC ASPIRATIONS

Performance – We will deliver excellent governance, service and value, for everyone.

Outcome Eleven – Effective leadership, advocacy and governance:

11.2 Deliver best practice governance and risk management.

Outcome Thirteen - Value for money from rates and long term financial sustainability:

13.1 Plan effectively for short and long term financial sustainability.

VOTING REQUIREMENTS

|

(Report Recommendation) Minute No. AR/0425/002 Moved: Cr M Virgo Seconded: Shire President C Mitchell That the Audit and Risk Committee recommends that Council: 1. Receives the Quarter 3 Finance and Costing Review Report for the period ended 31 March 2025; 2. Adopts the operating and capital budget amendment recommendations for the year ended 30 June 2025 as attached (Attachment 1); 3. Approves the allocation of $416,064 of organisational savings as identified within this report to reduce planned borrowings required for Council’s Cable Beach Stage A1 project (GL 114865620); and 4. Notes a forecast net end-of-year deficit position to 30 June 2024 of $193,282 including previously adopted budget amendments and the budget amendments in recommendations 2 and 3. |

|

Quarter 3 Finance and Costing Review 2024-25 |

Minutes – Audit and Risk Committee Meeting 8 April 2025 Page 1 of 3

|

LOCATION/ADDRESS: |

Nil |

|

APPLICANT: |

Nil |

|

FILE: |

COA01 |

|

AUTHOR: |

Manager Financial Services |

|

CONTRIBUTOR/S: |

Nil |

|

RESPONSIBLE OFFICER: |

Director Corporate Services |

|

DISCLOSURE OF INTEREST: |

Nil |

|

SUMMARY: The Audit and Risk Committee are presented a progress update of the findings identified in the: a) 2022/2023 Final Audit Management Report; b) Interim Audit Management Report for year ended 30 June 2024; c) Performance Audit 2024 – Local Government Physical Security Server Room Assets (Emerging Findings); d) 2023/24 Final Audit Management Report; and e) 2024 Regulation 17 Internal Audit Report. |

SMC 21 December 2023 Item 5.4.1

ARC 22 April 2024 Item 6.2

ARC 28 August 2024 Item 5.1, 5.2, 5.3

ARC 29 October 2024 Item 5.2

ARC 10 December 2024 Item 5.1

ARC 10 December 2024 Item 5.2

OMC 12 December 2024 Item 13.1

2022/2023 Final Audit Management Report

The Shire’s Final Audit Management Report for the 2022/2023 financial year was received by Council at the SMC 21 December 2023.

An update of the progress of audit findings contained in the Shire’s 2023 Final Audit Management Report was received by the Audit and Risk Committee (ARC) at the ARC meeting held 22 April 2024 with updates subsequently provided at the August and October ARC meetings.

2023/2024 Interim Audit Management Report

The Shire’s Interim Audit was conducted by RSM Australia (RSM) on behalf of the Office of the Auditor General (OAG) in April 2024. The Interim Audit Management Report was received by the Audit and Risk Committee at the ARC meeting held 28 August 2024 with updates subsequently provided at the October ARC meeting.

2024 Performance Audit – Local Government Physical Security of Server Room Assets (Emerging Findings)

A Performance Audit of 16 non-metropolitan local government entities was undertaken by the OAG to assess the management of local government physical ICT assets to protect them from physical and environmental hazards. Each local government received an Emerging Findings Letter which contained specific findings to the local government and a Summary of Findings Report which was tabled in State Parliament under sections 24 and 25 of the Auditor General Act 2006.

The Emerging Findings Letter and Summary of Findings Report were received by the ARC at the ARC meeting held 28 August 2024 with updates subsequently provided at the October ARC meeting.

Progress Update – Audit Reports

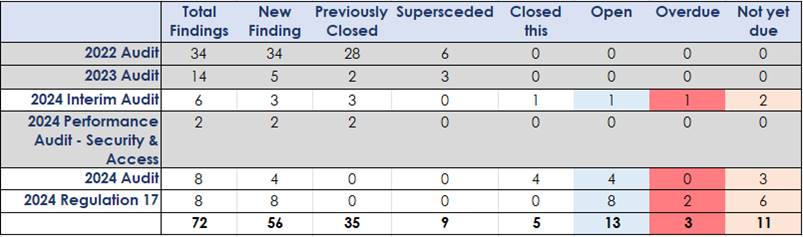

The Audit and Risk Committee received an update on the status of all three audit findings at the ARC meeting held 28 August 2024. Of the 22 findings, 10 were completed, 6 were in progress, and 6 were overdue.

A subsequent progress update was provided at the ARC meeting held 29 October 2024. Of the 22 findings, 14 were completed, 3 were in progress, and 5 were overdue.

It is worth noting that two of the findings in progress address the same issue. This issue was recorded in two separate audit reports because it remained overdue at the time of the second audit (2023/2024 Interim Audit).

Recent Audit Findings

The 2023/24 Final Audit Management Report and the 2024 Regulation 17 Audit were both accepted by the ARC at its meeting held 10 December 2024 and subsequently endorsed by Council the 12 December 2024 Ordinary Meeting of Council (OMC).

2023/2024 Final Audit Management Report

The Shire’s Final Audit Management Report for the 2023/2024 financial year was received by the ARC at the ARC meeting held 10 December 2024 and by Council at the OMC 12 December 2024. The 2024 final audit raised eight internal control improvement recommendations, several which had been previously identified and were existing actions within the improvement register.

Regulation 17 Audit Report

Regulation 17 of the Local Government (Audit) Regulations requires the Chief Executive Officer (CEO) to review the appropriateness and effectiveness of a local government’s systems and procedures in relation to risk management, internal control and legislative compliance at least once every 3 years.

The Shire of Broome (Shire) engaged Paxon Group (Paxon) to undertake this review on behalf of the CEO. Paxon provided 8 recommendations stemming from their review.

COMMENT

a) 2022/2023 Final Audit Management Report

b) 2023/2024 Interim Audit Management Report

c) 2024 Performance Audit – Local Government Physical Security Server Room Assets (Emerging Findings)

Details contained within the report are considered confidential as releasing them publicly would increase the likelihood that identified risks could be the target of fraudulent or illegal activities. Officers are actively addressing the issues identified in the external audits. Each finding is assigned a risk rating by the auditor to help prioritize and schedule actions for resolution.

2023/2024 Final Audit Management Report

Since the last Audit and Risk Committee meeting on October 29, 2024, 3 additional audits have concluded:

· The 2023/2024 Final Audit, conducted by RSM Australia on behalf of the OAG.

· The Regulations 17 Review, performed by Paxon Group.

A summary of findings from these audits are included for reference.

This report provides a high-level overview of outstanding findings and demonstrates the ongoing commitment to addressing identified risks.

February 2024 Progress Update

The table below summarises findings from outstanding audit matters stemming from audits conducted since 2022. It tracks:

· Total findings raised,

· New findings identified in each audit,

· Findings closed as at the last update,

· Findings classified as “superseded” (re-raised in subsequent audits to avoid duplication),

· Findings closed since the last update, and

· Status of open findings (overdue or not yet due).

· Closed Findings: Finding 6 from the 2023/2024 Interim Audit (Timeliness of policy reviews) is now resolved. A Business Operating Procedure and a Council Policy have been approved, marking this finding as complete.

· Superseded Findings: 9 findings from previous audits have been reclassified as "superseded" as they were addressed in subsequent reports.

· Overdue Findings: 2024 Interim Audit - Accuracy of leave balances.

Findings added

Two recent audits have identified additional findings:

2024 Final Audit: Eight findings, including four new findings and four re-raised from prior audits. Of these 8 findings, 4 have been closed this period:

1. Incorrect recognition of Loan Receivable from the Broome Surf Life Saving Club

2. Timeliness and evidence of review of general journals

3. Portable and attractive assets register not maintained

4. Bonds and deposits register not maintained.

2024 Regulation 17 Review: Eight entirely new findings of which none have been resolved and 2 are now overdue:

1. Fraud Control Plan

2. Manual journal approval process and reconciliations.

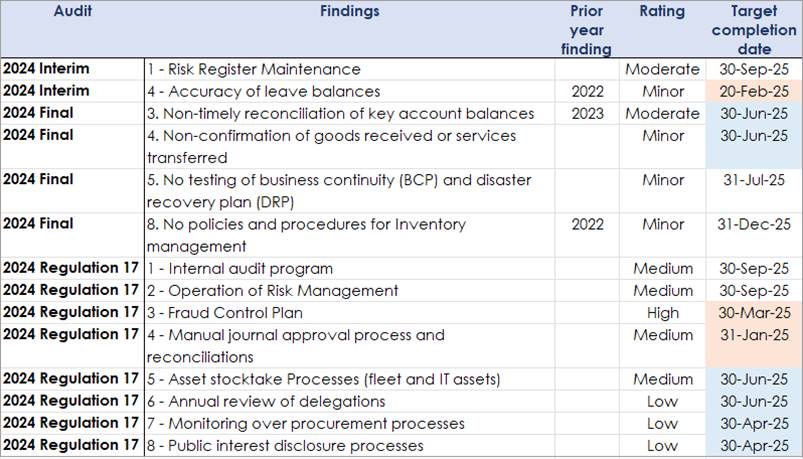

The table below outlines findings by target completion dates and highlights overdue findings and those due for resolution in the next quarter.

2024 Regulation 17 Audit Progress Update

Item 3 Fraud Control Plan 25% complete

The Council Policy Fraud and Corruption Prevention was adopted by Council at the 28 February 2025 Ordinary Meeting of Council.

Item 7 Monitoring over Procurement Processes 50% Complete

Officers have included an oversight and review of procurement processes however have not documented the process to date.

Item 8 Public Interest Disclosure Processes 50% Complete

Council Policy Public Interest Disclosure was adopted by Council at the 28 February 2025 Ordinary Meeting of Council.

The proposed Public Interest Disclosure Officers are due to complete the necessary training by the end of February 2025. Once the training is complete, the draft documents will be presented to Council for consideration at the 22 May 2025 Ordinary Meeting of Council.

Efforts to manage overdue actions have been undertaken. Accountable officers have provided updates regarding the tasks and progress to bring the actions to completion. Where required, new target completion dates are to be presented to OAG for mutual agreement. It is noted that there has only been a 6 week period since the last update was provided to the ARC.

CONSULTATION

Office of the Auditor General

RSM Australia has received the progress updates presented to the Audit and Risk Committee.

STATUTORY ENVIRONMENT

Local Government Act 1995

7.12A (3) Duties of local government with respect to audits

(3) A local government must —

(aa) examine an audit report received by the local government; and

(a) determine if any matters raised by the audit report, require action to be taken by the local government; and

(b) ensure that appropriate action is taken in respect of those matters

POLICY IMPLICATIONS

Nil.

FINANCIAL IMPLICATIONS

No specific financial implications are associated with this item. Remediation of any of the issues raised within the Audit Management Reports or Emerging Finding Letter may require budget allocations to resolve. Where this requires funding outside of the existing 2024/2025 adopted annual budget, Responsible Officers would request budget allocations either through the Shire’s Finance and Costing Review process, or as part of the 2025/2026 annual budget process.

RISK

The audit findings provide management with recommendations particularly to strengthen internal controls and reduce the likelihood of certain risks. Delays in progressing and completing the audit findings can be unfavourable to the organisation, but are also weighed against other demands on Shire resources, and the costs to the community.

STRATEGIC ASPIRATIONS

Performance - We will deliver excellent governance, service & value for everyone.

Outcome 13 - Value for money from rates and long term financial sustainability

Objective 13.1 Plan effectively for short- and long-term financial sustainability

Outcome 14 - Excellence in organisational performance and service delivery

Objective 14.3 Monitor and continuously improve performance levels.

VOTING REQUIREMENTS

|

(Report Recommendation) Minute No. AR/0425/003 Moved: Cr D Male Seconded: Cr M Virgo That the Audit and Risk Committee recommends that Council: 1. Receive the progress update of findings as per Confidential Attachment 1; 2. Notes the progress towards rectification of outstanding findings over the period; 3. Requests the Chief Executive Officer to progress the finalisation of all remaining outstanding findings as soon as practicable. |

|

February 2025 - Audit Progress Update (Confidential to Councillors and Directors Only) This attachment is confidential in accordance with section 5.23(2) of the Local Government Act 1995 section 5.23(2)((f)(i)) as it contains “a matter that if disclosed, could be reasonably expected to impair the effectiveness of any lawful method of procedure for preventing, detecting, investigating or dealing with any contravention or possible contravention of the law”, and section 5.23(2)((f)(ii)) as it contains “a matter that if disclosed, could be reasonably expected to endanger the security of the local governments property”. |

Minutes – Audit and Risk Committee Meeting 8 April 2025 Page 1 of 3

Nil

There being no further business the Chair declared the meeting closed at 10:53 AM